Download as ppt, pdf, or txt

You might also like

- Company Valuation Under IFRS - 3rd edition: Interpreting and forecasting accounts using International Financial Reporting StandardsFrom EverandCompany Valuation Under IFRS - 3rd edition: Interpreting and forecasting accounts using International Financial Reporting StandardsNo ratings yet

- Ooredoo Group - RFP - MODE - Commercial ProposalDocument7 pagesOoredoo Group - RFP - MODE - Commercial ProposalAntony KanyokoNo ratings yet

- Shanta Holdings Limited-PtdDocument13 pagesShanta Holdings Limited-Ptdnasir100% (1)

- Indusind BankDocument65 pagesIndusind BankNadeem KhanNo ratings yet

- R12 - Bank Account Transfer Ver 1.0Document644 pagesR12 - Bank Account Transfer Ver 1.0phanisure100% (5)

- Bismillah Group Scam and Banking Sector CorruptionDocument18 pagesBismillah Group Scam and Banking Sector CorruptionJakir_bnkNo ratings yet

- Arthneeti: All The Best!Document10 pagesArthneeti: All The Best!Kanav GuptaNo ratings yet

- ID#16102091 Pranta Sarker Accounting.Document64 pagesID#16102091 Pranta Sarker Accounting.AshrafulNo ratings yet

- CUB-Loan PolicyDocument62 pagesCUB-Loan PolicyHariNo ratings yet

- Banking 1Document20 pagesBanking 1Akash BdNo ratings yet

- Best Practices 2 Sindhu Durg DCCB PDFDocument13 pagesBest Practices 2 Sindhu Durg DCCB PDFPRALHADNo ratings yet

- Presentation To Analysts: June 2016 (In INR)Document39 pagesPresentation To Analysts: June 2016 (In INR)anasNo ratings yet

- 2020 Annual ENGDocument145 pages2020 Annual ENGwmdn88mrdkNo ratings yet

- Evaluation of Financial Performance of Social Islami Bank Limited, Jubilee Road BranchDocument20 pagesEvaluation of Financial Performance of Social Islami Bank Limited, Jubilee Road BranchNusrat IslamNo ratings yet

- Internship Arif FinalDocument58 pagesInternship Arif Finalটিটন চাকমাNo ratings yet

- C Project-2-2Document44 pagesC Project-2-2Rajesh Kumar roulNo ratings yet

- HBL Markup ComparisonDocument12 pagesHBL Markup ComparisonNoor NaazNo ratings yet

- MBA Final AssignmentDocument106 pagesMBA Final AssignmentMuhammad AzeemNo ratings yet

- Debt Recovery ManagementDocument9 pagesDebt Recovery Managementarchanaik27No ratings yet

- 2q 2017 FactsheetDocument2 pages2q 2017 Factsheetbnr8jjtjnjNo ratings yet

- Annual Report 2019 - 07-31-2020Document336 pagesAnnual Report 2019 - 07-31-2020PrincessNo ratings yet

- Internship Report On Exim Bank LTDDocument26 pagesInternship Report On Exim Bank LTDShafayet JamilNo ratings yet

- Department of Business AdministrationDocument57 pagesDepartment of Business AdministrationaneescreativeNo ratings yet

- TYBBA Fin ProjectDocument30 pagesTYBBA Fin ProjectShaikh FarheenNo ratings yet

- Muthoot Finance: and The Gold Loan BusinessDocument15 pagesMuthoot Finance: and The Gold Loan BusinessRobbie ShawNo ratings yet

- Study Material 2018 Czc-BhopalDocument233 pagesStudy Material 2018 Czc-BhopalCA Alpesh TatedNo ratings yet

- Pubali Bank - The Organizational StractureDocument21 pagesPubali Bank - The Organizational StractureNabila T. Chowdhury100% (4)

- FBL Annual Report 2019Document130 pagesFBL Annual Report 2019Fuaad DodooNo ratings yet

- National Bank of Pakistan: ChairmanDocument32 pagesNational Bank of Pakistan: ChairmanfarrukhNo ratings yet

- 1.1 2 1.2 Objectives of The Study 2 1.3 Methodology of The Study 2 1.4 3Document66 pages1.1 2 1.2 Objectives of The Study 2 1.3 Methodology of The Study 2 1.4 3Tamim SikderNo ratings yet

- Farmington Bank 1 Company Overview: 1.1 DescriptionDocument3 pagesFarmington Bank 1 Company Overview: 1.1 DescriptionAaron GenotaNo ratings yet

- New Banking License Catalyst For Consolidation 081010Document3 pagesNew Banking License Catalyst For Consolidation 081010kotler_2006No ratings yet

- SAMADHAAN Case StudyDocument7 pagesSAMADHAAN Case StudyharshNo ratings yet

- Meezan BankDocument39 pagesMeezan BankAsif Ali0% (2)

- Chapter 3Document19 pagesChapter 3extra fileNo ratings yet

- Developing A Strategic Plan For Brac BanDocument40 pagesDeveloping A Strategic Plan For Brac BanpasdNo ratings yet

- SHB Business Review 2016Document60 pagesSHB Business Review 2016KaiNo ratings yet

- FBL 2018 Annual ReportDocument136 pagesFBL 2018 Annual ReportFuaad DodooNo ratings yet

- Bank Fund 435Document28 pagesBank Fund 435sakildiuNo ratings yet

- Diwali Picks October - Fundamental DeskDocument16 pagesDiwali Picks October - Fundamental DeskSenthil KumarNo ratings yet

- MangalDocument17 pagesMangalprajapati kumar paswanNo ratings yet

- Internship Presentation On: Credit Management of Standard Bank Limited: A Study On Kumira Branch, ChittagongDocument16 pagesInternship Presentation On: Credit Management of Standard Bank Limited: A Study On Kumira Branch, ChittagongMS Sojib ChowdhuryNo ratings yet

- Boi ProjectDocument133 pagesBoi ProjectrupalijaiswalNo ratings yet

- A Comparative Financial Analysis of ONE Corporation and TWO CorporationDocument31 pagesA Comparative Financial Analysis of ONE Corporation and TWO CorporationAce Polaris Channel100% (1)

- 01 NIC Annual Report 64-65Document84 pages01 NIC Annual Report 64-65Ronit KcNo ratings yet

- Investment AnalysisDocument11 pagesInvestment AnalysisFendi SamsudinNo ratings yet

- Dina Nath Kumar: Nse Symbol: Indianb BSE Scrip Code-532814Document48 pagesDina Nath Kumar: Nse Symbol: Indianb BSE Scrip Code-532814dipesh.shopNo ratings yet

- Growth Story & Successful Market EntryDocument14 pagesGrowth Story & Successful Market Entryrajshekhar87No ratings yet

- Working Capital: Apl Apollo Tubes LTDDocument17 pagesWorking Capital: Apl Apollo Tubes LTDDhirajsharma123No ratings yet

- Equinomics Stock Note Karnataka Bank June 29, 2018Document4 pagesEquinomics Stock Note Karnataka Bank June 29, 2018g_ayyanarNo ratings yet

- Retail Equity Highlight FundsDocument4 pagesRetail Equity Highlight FundsRavi KumarNo ratings yet

- Analysis of Private Sector Banks - Investor'S PerspectiveDocument55 pagesAnalysis of Private Sector Banks - Investor'S Perspectivemonal_bhattadNo ratings yet

- Executive Summary: Rizal Commercial Banking CorporationDocument6 pagesExecutive Summary: Rizal Commercial Banking CorporationMon Toribio AtractivoNo ratings yet

- Interview Special-2016Document36 pagesInterview Special-2016Sneha Abhash SinghNo ratings yet

- Internship ReportDocument48 pagesInternship ReportIftekhar Abid FahimNo ratings yet

- Valuation of HDFCDocument21 pagesValuation of HDFCG Nagarajan0% (1)

- Fostering Growth Opportunities: Hong Leong Finance LimitedDocument144 pagesFostering Growth Opportunities: Hong Leong Finance LimitedSassy TanNo ratings yet

- FIM PresentationDocument14 pagesFIM Presentationsomeone specialNo ratings yet

- Bank of BarodaDocument35 pagesBank of BarodaAmangorayaNo ratings yet

- Annual Report 2020Document160 pagesAnnual Report 2020SOBANAA SUNDARNo ratings yet

- Prepared By:: Sakia Sultana ID: EB143221Document83 pagesPrepared By:: Sakia Sultana ID: EB143221Naomii HoneyNo ratings yet

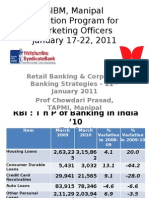

- 10 International Conference On Problem and Possibilities in Online Education in ManagementDocument39 pages10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadNo ratings yet

- Second Innings September 2019Document52 pagesSecond Innings September 2019Prof Dr Chowdari PrasadNo ratings yet

- Social Entrepreneurship2015Document45 pagesSocial Entrepreneurship2015Prof Dr Chowdari PrasadNo ratings yet

- Performance of Crowd Funding in India: Issues and ChallengesDocument19 pagesPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Prof Chowdari Prasad CV 26112018Document11 pagesProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadNo ratings yet

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsDocument15 pagesA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadNo ratings yet

- Tapmi Update 2013Document120 pagesTapmi Update 2013Prof Dr Chowdari PrasadNo ratings yet

- Consumer Protection Act 1986Document41 pagesConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Digital Banking in India 2016Document21 pagesDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- HR As A Strategic Business PartnerDocument36 pagesHR As A Strategic Business PartnerProf Dr Chowdari PrasadNo ratings yet

- List of Books On Micro FinanceDocument32 pagesList of Books On Micro FinanceProf Dr Chowdari Prasad71% (7)

- Recent Trends of PE Funding in IndiaDocument38 pagesRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadNo ratings yet

- Lean and Green Banking in India 2012Document20 pagesLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- MFI National ConferenceDocument12 pagesMFI National ConferenceProf Dr Chowdari PrasadNo ratings yet

- Myths of Microfinance - Global South Development Magazine JAN 2011Document42 pagesMyths of Microfinance - Global South Development Magazine JAN 2011Silver Lining CreationNo ratings yet

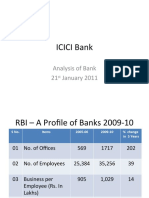

- Icici Bank: Analysis of Bank 21 January 2011Document6 pagesIcici Bank: Analysis of Bank 21 January 2011Prof Dr Chowdari PrasadNo ratings yet

- Profile of Banks 2010-11Document99 pagesProfile of Banks 2010-11Vishesh KumarNo ratings yet

- Women Achievers Ebook2Document95 pagesWomen Achievers Ebook2Prof Dr Chowdari PrasadNo ratings yet

- The Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Document11 pagesThe Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Prof Dr Chowdari PrasadNo ratings yet

- Sibm, RBCBDocument20 pagesSibm, RBCBProf Dr Chowdari PrasadNo ratings yet

- TAPMI ManipalDocument18 pagesTAPMI ManipalProf Dr Chowdari Prasad100% (1)

- Roc Forms & Secretarial PracticeDocument11 pagesRoc Forms & Secretarial PracticeSankaran SwaminathanNo ratings yet

- Merchant Banking (In The Light of SEBI (Merchat Bankers) Regulations, 1992)Document38 pagesMerchant Banking (In The Light of SEBI (Merchat Bankers) Regulations, 1992)Parul PrasadNo ratings yet

- Ps-User SecretsDocument28 pagesPs-User SecretsEdilson GomesNo ratings yet

- Centre Issues First Zero-Coupon Recap Bonds of 5,500 CR: P&SB To Park Investment in HTM Category Raises ConcernDocument16 pagesCentre Issues First Zero-Coupon Recap Bonds of 5,500 CR: P&SB To Park Investment in HTM Category Raises ConcernGopalakrishnan SivasamyNo ratings yet

- Idbi Objectives and Functions of IDBI ObjectivesDocument2 pagesIdbi Objectives and Functions of IDBI ObjectivesRohit Pandey0% (1)

- Template JIBERDocument4 pagesTemplate JIBERAnita Nida SariNo ratings yet

- Dictionary of EconomicsDocument225 pagesDictionary of EconomicsMushtak Shaikh100% (1)

- Sap Fico Configuration DocumentDocument82 pagesSap Fico Configuration DocumentPham Anh TaiNo ratings yet

- Debit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedDocument1 pageDebit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When Presentedsujeet kumarNo ratings yet

- A Study On Awareness and Satisfaction Level of GoldDocument3 pagesA Study On Awareness and Satisfaction Level of Goldjay.kum50% (2)

- Annex 5: Practical Guide To Procedures For Programme Estimates - Project Approach (Version 4.0) - Annex 5Document17 pagesAnnex 5: Practical Guide To Procedures For Programme Estimates - Project Approach (Version 4.0) - Annex 5jaimeNo ratings yet

- Jeremy RothfieldDocument53 pagesJeremy RothfieldJeremy RothfieldNo ratings yet

- Income From Other SourcesDocument11 pagesIncome From Other Sourcessrocky2000100% (1)

- QuiChap012 PDFDocument108 pagesQuiChap012 PDFIvan YaoNo ratings yet

- DavyDocument8 pagesDavyAhmedRiaz64No ratings yet

- The Greek Public Debt Misery The Right Cure Should Follow The Right Diagnosis ZDDocument2 pagesThe Greek Public Debt Misery The Right Cure Should Follow The Right Diagnosis ZDBruegelNo ratings yet

- AfghanistanDocument25 pagesAfghanistanSarah SyNo ratings yet

- Capital Float 2015Document13 pagesCapital Float 2015Anmol JainNo ratings yet

- Supplemental Module B - Receipts and DisbursementsDocument11 pagesSupplemental Module B - Receipts and DisbursementsShekinah Grace SantuaNo ratings yet

- Booklet ccx18Document17 pagesBooklet ccx18Andres Villegas MesaNo ratings yet

- Credit BureausDocument15 pagesCredit BureausGauri MittalNo ratings yet

- AccountStatement HRFDocument14 pagesAccountStatement HRFshikhil665No ratings yet

- Application Form For Investor Settlement AccountDocument6 pagesApplication Form For Investor Settlement AccountmentorNo ratings yet

- COA - M2013-004 Revised Cash Examination ManualDocument106 pagesCOA - M2013-004 Revised Cash Examination Manualerrol100% (3)

- Shovon HRM 422 ReportDocument62 pagesShovon HRM 422 ReportRakibul Hassan RabbiNo ratings yet

- ALCO and Operational Risk Management at CITI Bank: Name Student ID Instructor DateDocument16 pagesALCO and Operational Risk Management at CITI Bank: Name Student ID Instructor DateAbrarNo ratings yet

- Bank of America Research PaperDocument7 pagesBank of America Research Paperfyr60xv7100% (1)

- Nido Home Finance LimitedDocument640 pagesNido Home Finance LimitedchhedamalayNo ratings yet