Download as ppt, pdf, or txt

You might also like

- Pceia - Bi Full NotesDocument407 pagesPceia - Bi Full Notesmohdhafizmdali100% (4)

- A Project ON: " Ulip" (A Study On Security AND Investment Plan)Document80 pagesA Project ON: " Ulip" (A Study On Security AND Investment Plan)parag1230100% (1)

- Chapter 1Document31 pagesChapter 1YUSLINA BINTI ABDUL GHAN1No ratings yet

- InsurancelawDocument136 pagesInsurancelawStuti SinhaNo ratings yet

- Unit 2 InsuranceDocument43 pagesUnit 2 InsuranceNikita ShekhawatNo ratings yet

- Unit IVDocument59 pagesUnit IVsonuNo ratings yet

- Advantages of InsuranceDocument3 pagesAdvantages of InsuranceGursharan Saggu0% (1)

- Summer Internship Project With Prudent Corporate Advisory Services LTD Comparison of Kotak Mahindra ULIP With Other Private Insurance PlayersDocument40 pagesSummer Internship Project With Prudent Corporate Advisory Services LTD Comparison of Kotak Mahindra ULIP With Other Private Insurance Playersk3k.k3kNo ratings yet

- Unit - 5 InsuranceDocument82 pagesUnit - 5 InsuranceSwapnil SonjeNo ratings yet

- Nature of InsuranceDocument31 pagesNature of InsurancemeeyaNo ratings yet

- Pb502 - Insurance and Takaful: Principle and Practice - Chapter 1 Introduction To InsuranceDocument6 pagesPb502 - Insurance and Takaful: Principle and Practice - Chapter 1 Introduction To InsuranceChrystal Joynre Elizabeth JouesNo ratings yet

- B&I unit-3&4Document37 pagesB&I unit-3&4nilofar.shaikhNo ratings yet

- Introduction of Insurance NOTESDocument7 pagesIntroduction of Insurance NOTESReva JaiswalNo ratings yet

- UNIT-3: Introduction To InsuranceDocument36 pagesUNIT-3: Introduction To InsuranceEdenNo ratings yet

- COMPANY PprrooffileDocument12 pagesCOMPANY PprrooffileKai MK4No ratings yet

- CH 3Document21 pagesCH 3mikiyas zeyedeNo ratings yet

- Ibis Unit 03Document28 pagesIbis Unit 03bhagyashripande321No ratings yet

- InsuranceDocument144 pagesInsuranceShubhampratapsNo ratings yet

- Insurance & UTIDocument22 pagesInsurance & UTIReeta Singh100% (1)

- Function's of Insurance . by Aftab MullaDocument12 pagesFunction's of Insurance . by Aftab MullaImran Khan SharNo ratings yet

- Executive SummaryDocument25 pagesExecutive SummaryRitika MahenNo ratings yet

- Insurance ManagementDocument25 pagesInsurance ManagementDeepak ParidaNo ratings yet

- Importance and Benefits of InsuranceDocument7 pagesImportance and Benefits of InsurancePooja TripathiNo ratings yet

- Chapter - 1Document51 pagesChapter - 1Ankur SheelNo ratings yet

- Introduction To InsuranceDocument15 pagesIntroduction To InsuranceInza NsaNo ratings yet

- Insurance: 1 Lesson 1 Introduction To InsuranceDocument14 pagesInsurance: 1 Lesson 1 Introduction To Insurancevipul sutharNo ratings yet

- Meaning & Definition of Insurance-: Chapter-1 IntroductionDocument8 pagesMeaning & Definition of Insurance-: Chapter-1 IntroductionDeep GujareNo ratings yet

- Introduction To Insurance: Asstt. Professor, SRCC, University of DelhiDocument30 pagesIntroduction To Insurance: Asstt. Professor, SRCC, University of DelhikanikaNo ratings yet

- Q. 24Document2 pagesQ. 24Faisi PrinceNo ratings yet

- Nature InsuranceDocument18 pagesNature Insurancep133020No ratings yet

- RISK Chapter 3Document13 pagesRISK Chapter 3Taresa AdugnaNo ratings yet

- Impact of Privatization On Insurance SectorDocument44 pagesImpact of Privatization On Insurance SectorPranav ViraNo ratings yet

- 9th Chap Insurance & Business RiskDocument9 pages9th Chap Insurance & Business Riskbaigz0918No ratings yet

- Name: Adejayan Damilola ToluDocument5 pagesName: Adejayan Damilola Tolumicheal chrisNo ratings yet

- Project - Final in The MakingDocument55 pagesProject - Final in The MakingShivansh OhriNo ratings yet

- Insurance Chapter 1Document8 pagesInsurance Chapter 1Yong Ee VonnNo ratings yet

- Pceia BiDocument407 pagesPceia BiWenny Khoo100% (1)

- Apollo MunichDocument52 pagesApollo MunichSumit ManglaniNo ratings yet

- 1 Lesson 1 Introduction To InsuranceDocument61 pages1 Lesson 1 Introduction To InsurancerachitNo ratings yet

- Insurance ManagementDocument71 pagesInsurance Managementmesfinabera180No ratings yet

- INTRODUCTIONDocument20 pagesINTRODUCTIONLEARN WITH AGALYANo ratings yet

- Insurance AssignmentDocument114 pagesInsurance AssignmentNewton BiswasNo ratings yet

- General InsuranceDocument100 pagesGeneral InsuranceShivani YadavNo ratings yet

- My ProjectDocument82 pagesMy Projectdhruv_jagtapNo ratings yet

- Basics of Business Insurance - NotesDocument41 pagesBasics of Business Insurance - Notesjeganrajraj100% (1)

- AssignmentDocument8 pagesAssignmentkalina.sintayehuNo ratings yet

- Introduction To Insurance and Risk ManagementDocument12 pagesIntroduction To Insurance and Risk ManagementJake GuataNo ratings yet

- Summer Training Project Report ON Selection and Recruitment: Shah Satnam Ji P.G. Girl'S College, Sirsa (Haryana)Document86 pagesSummer Training Project Report ON Selection and Recruitment: Shah Satnam Ji P.G. Girl'S College, Sirsa (Haryana)Paras SukhijaNo ratings yet

- Chap Iii - FinaldraftDocument12 pagesChap Iii - FinaldraftOjo Meow GovindhNo ratings yet

- Lec 1Document14 pagesLec 1Ameen KolachiNo ratings yet

- Risk Management Lecture Note CH 3-7Document77 pagesRisk Management Lecture Note CH 3-7Meklit TenaNo ratings yet

- POI MaterialDocument11 pagesPOI MaterialMukesh ChoudharyNo ratings yet

- IRDADocument18 pagesIRDArameez.amex5067No ratings yet

- Micro Insurance ProjectDocument12 pagesMicro Insurance ProjectSushil PrajapatNo ratings yet

- Insurance NotesDocument46 pagesInsurance Notespuru100% (1)

- Functions of InsuranceDocument26 pagesFunctions of InsurancenikschopraNo ratings yet

- Insurance, Regulations and Loss Prevention : Basic Rules for the Industry Insurance: Business strategy books, #5From EverandInsurance, Regulations and Loss Prevention : Basic Rules for the Industry Insurance: Business strategy books, #5No ratings yet

- Government Bonds Bond - IN0020190362 Bond - IN0020170026Document4 pagesGovernment Bonds Bond - IN0020190362 Bond - IN0020170026Arif AhmedNo ratings yet

- Brief History of The ASEAN (1967 Present)Document6 pagesBrief History of The ASEAN (1967 Present)Redmond YuNo ratings yet

- Ibp Exemption List 211222 182126Document9 pagesIbp Exemption List 211222 182126Muhammad TalhaNo ratings yet

- American International Group Inc and SubsidiariesDocument14 pagesAmerican International Group Inc and SubsidiariesFOXBusiness.com50% (2)

- Chapter 4 Financial InvestmentDocument53 pagesChapter 4 Financial InvestmentAngelica Joy ManaoisNo ratings yet

- Direct Credit Facility Form: Important NotesDocument1 pageDirect Credit Facility Form: Important NotesOrange HazelNo ratings yet

- tOO BiG To fAiL LOan MOdIFiCATioN FOrm r.1.A.002.B.XXXXDocument6 pagestOO BiG To fAiL LOan MOdIFiCATioN FOrm r.1.A.002.B.XXXXchunga85No ratings yet

- Partnership Dissolution ProblemsDocument9 pagesPartnership Dissolution ProblemsKristel DayritNo ratings yet

- Seek Overview 2008-2016 - Inflation-Adjusted VersionDocument4 pagesSeek Overview 2008-2016 - Inflation-Adjusted VersionBecca SchimmelNo ratings yet

- 1Document3 pages1Stook01701No ratings yet

- Management Accounting Problem Unit 5Document7 pagesManagement Accounting Problem Unit 5princeNo ratings yet

- Business Law MCQDocument4 pagesBusiness Law MCQPoonam PraveenNo ratings yet

- Inventories Valuation ConceptDocument13 pagesInventories Valuation ConceptSumit SahuNo ratings yet

- Call Option HandoutDocument4 pagesCall Option Handoutrenee Benjamin-GibbsNo ratings yet

- Savings and Investments Pricing Guide 2023Document21 pagesSavings and Investments Pricing Guide 2023Thanduxolo MlamuliNo ratings yet

- Capital Budgeting Assignment QuestionsDocument3 pagesCapital Budgeting Assignment QuestionsNgaiza3No ratings yet

- Account Statement 25-05-2023T02 58 36Document1 pageAccount Statement 25-05-2023T02 58 36SHEHERYAR QAZI 26488No ratings yet

- Module 3 Divisible ProfitsDocument8 pagesModule 3 Divisible ProfitsVijay KumarNo ratings yet

- Ibm Final PDFDocument24 pagesIbm Final PDFRajamaniNo ratings yet

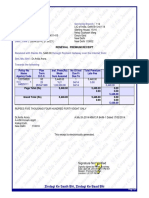

- Renewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchDocument1 pageRenewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchAnirudh AroraNo ratings yet

- Empresa Quimica Industrial LR108549 PDFDocument1 pageEmpresa Quimica Industrial LR108549 PDFMARGARITA RODRIGUEZNo ratings yet

- Examen Engels Market Leader U9!10!11 andDocument9 pagesExamen Engels Market Leader U9!10!11 andVinh VoNo ratings yet

- Working Capital Black BookDocument35 pagesWorking Capital Black Bookomprakash shindeNo ratings yet

- Audit Process and Audit Planning With AnswerDocument12 pagesAudit Process and Audit Planning With AnswerR100% (1)

- Juhayna Food Industries Swot Analysis BacDocument13 pagesJuhayna Food Industries Swot Analysis Backeroules samirNo ratings yet

- Laptop InvoiceDocument1 pageLaptop InvoicePranjal ThakurNo ratings yet

- Financial and Business Risk Management 1 PDFDocument75 pagesFinancial and Business Risk Management 1 PDFrochelleandgelloNo ratings yet

- Report of Investigation: Burns Philp and Co LTDDocument41 pagesReport of Investigation: Burns Philp and Co LTDa_bleem_userNo ratings yet

- Salary INCOME - ITDocument64 pagesSalary INCOME - ITHrishikesh AshtaputreNo ratings yet

- Financial Literacy Test Grade 11 Entrepreneurship Mr. Valley Student NameDocument8 pagesFinancial Literacy Test Grade 11 Entrepreneurship Mr. Valley Student Nameapi-350400617No ratings yet