LectureSlides Chp4

LectureSlides Chp4

You might also like

- Spa Gold BullionDocument19 pagesSpa Gold BullionCarlos Cerqueira Lima67% (3)

- Economics of Strategy: Seventh EditionDocument50 pagesEconomics of Strategy: Seventh EditionMacNo ratings yet

- (Cambridge Historical Studies in American Law and Society) Michael Grossberg-A Judgment For Solomon - The D'hauteville Case and Legal Experience in Antebellum America-Cambridge University P PDFDocument292 pages(Cambridge Historical Studies in American Law and Society) Michael Grossberg-A Judgment For Solomon - The D'hauteville Case and Legal Experience in Antebellum America-Cambridge University P PDFAsep KusnaliNo ratings yet

- Econ Un3025 002 Course Syllabus FinalDocument12 pagesEcon Un3025 002 Course Syllabus FinalBri MinNo ratings yet

- Lunsford Guide Instructor NotesDocument492 pagesLunsford Guide Instructor NotesPArk100100% (3)

- CH 06Document12 pagesCH 06leisurelarry999No ratings yet

- Report of The 2013 Election Review PanelDocument20 pagesReport of The 2013 Election Review PanelJesse FerrerasNo ratings yet

- The Madisonian MachineDocument44 pagesThe Madisonian MachineFIXMYLOANNo ratings yet

- The Journal of Law, Volume 1, Number 1Document226 pagesThe Journal of Law, Volume 1, Number 1PheresNo ratings yet

- The Myth of Manipulation The Economics of Minimum WageDocument65 pagesThe Myth of Manipulation The Economics of Minimum WageAndrew Joliet100% (1)

- Data Integrity BookDocument2 pagesData Integrity BookTim Sandle100% (1)

- PM Case PPT - Le Petit ChefDocument44 pagesPM Case PPT - Le Petit Chefbhupendrayadav786100% (2)

- Monopoly RulesDocument5 pagesMonopoly RulesscribdjoeluNo ratings yet

- Summary Cost Accounting Horngren Et AllDocument35 pagesSummary Cost Accounting Horngren Et AllFreya Evangeline100% (1)

- Economics of Strategy: The Horizontal Boundaries of The FirmDocument50 pagesEconomics of Strategy: The Horizontal Boundaries of The FirmMacNo ratings yet

- UMKC Econ431 Fall 2012 SyllabusDocument25 pagesUMKC Econ431 Fall 2012 SyllabusMitch GreenNo ratings yet

- Economics of Strategy: Competitors and CompetitionDocument50 pagesEconomics of Strategy: Competitors and CompetitionMacNo ratings yet

- The Evolution of The Modern Firm: Chapter ContentsDocument14 pagesThe Evolution of The Modern Firm: Chapter Contentsleisurelarry999No ratings yet

- CH 09Document10 pagesCH 09leisurelarry999No ratings yet

- ECON3Document20 pagesECON3Christelle De Los CientosNo ratings yet

- Economics of Strategy (Rješenja)Document227 pagesEconomics of Strategy (Rješenja)Antonio Hrvoje ŽupićNo ratings yet

- CH 05Document14 pagesCH 05leisurelarry999No ratings yet

- CH 07Document13 pagesCH 07leisurelarry999No ratings yet

- 8 Week Lsat Study Schedule 2017Document19 pages8 Week Lsat Study Schedule 2017Anonymous xgqcVDsgrHNo ratings yet

- Test Bank For Economics of Strategy 7th Edition by DranoveDocument14 pagesTest Bank For Economics of Strategy 7th Edition by Dranovewinry100% (1)

- CH 03Document21 pagesCH 03leisurelarry999100% (1)

- Environment, Power and Culture: Chapter ContentsDocument11 pagesEnvironment, Power and Culture: Chapter Contentsleisurelarry999No ratings yet

- Gmat 6 Ed Og 2019 v2 Problem List Course PDFDocument16 pagesGmat 6 Ed Og 2019 v2 Problem List Course PDFAnubhav ZarabiNo ratings yet

- 2 - Intro To Logical ReasoningDocument12 pages2 - Intro To Logical ReasoningLISA GOLDMANNo ratings yet

- CH 02Document51 pagesCH 02İlke ErçakarNo ratings yet

- Goodman V GallantDocument12 pagesGoodman V GallantAnonymous Azxx3Kp9No ratings yet

- Blanchard Macroeconomicsw7550Document49 pagesBlanchard Macroeconomicsw7550yzl100% (1)

- International Accounting Chap 006Document39 pagesInternational Accounting Chap 006ChuckNo ratings yet

- Besanko Economics of Strategy Ch9Document43 pagesBesanko Economics of Strategy Ch9Ginny WanNo ratings yet

- Essentials of Economic Theory: As Applied to Modern Problems of Industry and Public PolicyFrom EverandEssentials of Economic Theory: As Applied to Modern Problems of Industry and Public PolicyNo ratings yet

- Industry Competitiveness AnalysisDocument49 pagesIndustry Competitiveness AnalysistunggaltriNo ratings yet

- IT 426 Project ManagementDocument4 pagesIT 426 Project ManagementMubashra AhmedNo ratings yet

- U.S. Senate Hearing on Wartime Executive Power and National Security Agency's Surveillance AuthorityFrom EverandU.S. Senate Hearing on Wartime Executive Power and National Security Agency's Surveillance AuthorityNo ratings yet

- Supply and Demand Is Perhaps One of The Most Fundamental Concepts of Economics and It Is The Backbone of A Market EconomyDocument7 pagesSupply and Demand Is Perhaps One of The Most Fundamental Concepts of Economics and It Is The Backbone of A Market EconomyJed FarrellNo ratings yet

- Besanko HarvardDocument228 pagesBesanko Harvardkjmnlkmh100% (1)

- Industrial Economics and Organisation: Conventional and Islamic PerspectivesFrom EverandIndustrial Economics and Organisation: Conventional and Islamic PerspectivesNo ratings yet

- Polar Bear Pirates and Their Quest to Engage the Sleepwalkers: Motivate everyday people to deliver extraordinary resultsFrom EverandPolar Bear Pirates and Their Quest to Engage the Sleepwalkers: Motivate everyday people to deliver extraordinary resultsRating: 4 out of 5 stars4/5 (2)

- Tax Policy and the Economy, Volume 36From EverandTax Policy and the Economy, Volume 36Robert A. MoffittNo ratings yet

- Trained Capacities: John Dewey, Rhetoric, and Democratic PracticeFrom EverandTrained Capacities: John Dewey, Rhetoric, and Democratic PracticeNo ratings yet

- Consumer Behaviour and Utility MaximizationDocument8 pagesConsumer Behaviour and Utility MaximizationJagmohan KalsiNo ratings yet

- The Five PM Lifecyle ModelsDocument3 pagesThe Five PM Lifecyle ModelsJohn N. Constance100% (1)

- A312 SyllabusDocument7 pagesA312 SyllabusHenry ZhuNo ratings yet

- ANTITRUST ECONOMICS AT A TIME OF UPHEAVALFrom EverandANTITRUST ECONOMICS AT A TIME OF UPHEAVALJohn E. KwokaNo ratings yet

- Harvard Referencing: Guide: (Please Note: This Document Was Downloaded From Citethisforme Web Tool, URL )Document13 pagesHarvard Referencing: Guide: (Please Note: This Document Was Downloaded From Citethisforme Web Tool, URL )Benjamin K JaravazaNo ratings yet

- Breaking the Deadlock: The 2000 Election, the Constitution, and the CourtsFrom EverandBreaking the Deadlock: The 2000 Election, the Constitution, and the CourtsRating: 4 out of 5 stars4/5 (4)

- Dec LSAT 2016 Sec 3 PDFDocument8 pagesDec LSAT 2016 Sec 3 PDFSagar PatelNo ratings yet

- Introduction To Business Law Notes: Chapter 1: ContractsDocument11 pagesIntroduction To Business Law Notes: Chapter 1: ContractsRoger Ordoño ManzanasNo ratings yet

- Sec 3 Sep 2016 LSATDocument8 pagesSec 3 Sep 2016 LSATSagar Patel100% (1)

- Questions 1-11 Are Based On The Following PassageDocument3 pagesQuestions 1-11 Are Based On The Following PassageMing db50% (2)

- Micro EconomicsDocument32 pagesMicro Economicsmariyam mohammadNo ratings yet

- LectureSlides Chp6Document24 pagesLectureSlides Chp6hislove00No ratings yet

- LectureSlides Chps3Document7 pagesLectureSlides Chps3hislove00No ratings yet

- Chapter 1 Appendix: Making and Using GraphsDocument10 pagesChapter 1 Appendix: Making and Using Graphshislove00No ratings yet

- Chapters 1 and 2: - Chapter 1 - Getting Started - Chapter 2 - The U.S. and GlobalDocument28 pagesChapters 1 and 2: - Chapter 1 - Getting Started - Chapter 2 - The U.S. and Globalhislove00No ratings yet

- GDP: A Measure of Total Production and IncomeDocument27 pagesGDP: A Measure of Total Production and Incomehislove00No ratings yet

- Business PlanDocument4 pagesBusiness PlanMaria Mendoza AlejandriaNo ratings yet

- Business Level StrategyDocument35 pagesBusiness Level StrategyShiva Kumar Dunaboina100% (1)

- August September 2018 PDFDocument36 pagesAugust September 2018 PDFSanthosh GarapatiNo ratings yet

- Tutorial 5 Solutions FM 201Document6 pagesTutorial 5 Solutions FM 201Achal ChandNo ratings yet

- Valuation Ratios and The Long Run Stock Market OutlookDocument46 pagesValuation Ratios and The Long Run Stock Market OutlookMuhammad Saeed BabarNo ratings yet

- Business Events News For Fri 07 Nov 2014 - High DDR 'Til New Rooms Avail, WCC Gets Green Light, Double Bay Opens, New ICCA Head, and Much MoreDocument3 pagesBusiness Events News For Fri 07 Nov 2014 - High DDR 'Til New Rooms Avail, WCC Gets Green Light, Double Bay Opens, New ICCA Head, and Much MoreBusiness Events NewsNo ratings yet

- Cost Volume Profit AnalysisDocument7 pagesCost Volume Profit Analysissofyan timotyNo ratings yet

- Thesis On Consumer Perception Towards Online Grocery ShoppingDocument53 pagesThesis On Consumer Perception Towards Online Grocery ShoppingPrabhat Ekka100% (2)

- Project NotesDocument82 pagesProject NotesNitesh KhandelwalNo ratings yet

- Liabilities PDFDocument6 pagesLiabilities PDFIya KangNo ratings yet

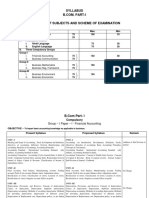

- Syllabus Grouping of Subjects and Scheme of ExaminationDocument29 pagesSyllabus Grouping of Subjects and Scheme of ExaminationAbhisek AgrawalNo ratings yet

- PEST and SWOT Analysis of MICE Industry in SingaporeDocument5 pagesPEST and SWOT Analysis of MICE Industry in SingaporeMukesh RanaNo ratings yet

- The Set Up: Weekly Puzzle #2: Price or Value?Document2 pagesThe Set Up: Weekly Puzzle #2: Price or Value?PetraNo ratings yet

- Price Elasticity of DemandDocument4 pagesPrice Elasticity of DemandMADmanTalksNo ratings yet

- Classification of Cost. (ODA, ODAIT, ODFB&ODEF)Document4 pagesClassification of Cost. (ODA, ODAIT, ODFB&ODEF)rofoba6609No ratings yet

- Economics in Business Decision Making-I (Micro)Document2 pagesEconomics in Business Decision Making-I (Micro)Abinash oinamNo ratings yet

- RAW CASHEW COST - DocxfinalDocument4 pagesRAW CASHEW COST - DocxfinalBrijesh Panchal100% (1)

- Real Estate Project Analysis: Project: Collina Tinta Location: Hurricane, UtahDocument25 pagesReal Estate Project Analysis: Project: Collina Tinta Location: Hurricane, UtahHema MahourNo ratings yet

- Intermediate May 2019 B5Document23 pagesIntermediate May 2019 B5PASTORYNo ratings yet

- Brambles 1Document15 pagesBrambles 1hotshot2004No ratings yet

- Thesis ProposalDocument13 pagesThesis ProposalBettina MaynardNo ratings yet

- Leather Industry of BangladeshDocument18 pagesLeather Industry of BangladeshSamin Yeaser Khan100% (1)

- Charisse T. Abordo John Wendell D. EscosesDocument66 pagesCharisse T. Abordo John Wendell D. EscosesCharisse AbordoNo ratings yet

- Jasch, Christine. The Use of Environmental Management Accounting (EMA) For Identifying Environmental CostsDocument11 pagesJasch, Christine. The Use of Environmental Management Accounting (EMA) For Identifying Environmental CostsTitoHeidyYantoNo ratings yet

- Economics I 1005Document23 pagesEconomics I 1005meetwithsanjay100% (1)

Download as ppt, pdf, or txt

You might also like

- Spa Gold BullionDocument19 pagesSpa Gold BullionCarlos Cerqueira Lima67% (3)

- Economics of Strategy: Seventh EditionDocument50 pagesEconomics of Strategy: Seventh EditionMacNo ratings yet

- (Cambridge Historical Studies in American Law and Society) Michael Grossberg-A Judgment For Solomon - The D'hauteville Case and Legal Experience in Antebellum America-Cambridge University P PDFDocument292 pages(Cambridge Historical Studies in American Law and Society) Michael Grossberg-A Judgment For Solomon - The D'hauteville Case and Legal Experience in Antebellum America-Cambridge University P PDFAsep KusnaliNo ratings yet

- Econ Un3025 002 Course Syllabus FinalDocument12 pagesEcon Un3025 002 Course Syllabus FinalBri MinNo ratings yet

- Lunsford Guide Instructor NotesDocument492 pagesLunsford Guide Instructor NotesPArk100100% (3)

- CH 06Document12 pagesCH 06leisurelarry999No ratings yet

- Report of The 2013 Election Review PanelDocument20 pagesReport of The 2013 Election Review PanelJesse FerrerasNo ratings yet

- The Madisonian MachineDocument44 pagesThe Madisonian MachineFIXMYLOANNo ratings yet

- The Journal of Law, Volume 1, Number 1Document226 pagesThe Journal of Law, Volume 1, Number 1PheresNo ratings yet

- The Myth of Manipulation The Economics of Minimum WageDocument65 pagesThe Myth of Manipulation The Economics of Minimum WageAndrew Joliet100% (1)

- Data Integrity BookDocument2 pagesData Integrity BookTim Sandle100% (1)

- PM Case PPT - Le Petit ChefDocument44 pagesPM Case PPT - Le Petit Chefbhupendrayadav786100% (2)

- Monopoly RulesDocument5 pagesMonopoly RulesscribdjoeluNo ratings yet

- Summary Cost Accounting Horngren Et AllDocument35 pagesSummary Cost Accounting Horngren Et AllFreya Evangeline100% (1)

- Economics of Strategy: The Horizontal Boundaries of The FirmDocument50 pagesEconomics of Strategy: The Horizontal Boundaries of The FirmMacNo ratings yet

- UMKC Econ431 Fall 2012 SyllabusDocument25 pagesUMKC Econ431 Fall 2012 SyllabusMitch GreenNo ratings yet

- Economics of Strategy: Competitors and CompetitionDocument50 pagesEconomics of Strategy: Competitors and CompetitionMacNo ratings yet

- The Evolution of The Modern Firm: Chapter ContentsDocument14 pagesThe Evolution of The Modern Firm: Chapter Contentsleisurelarry999No ratings yet

- CH 09Document10 pagesCH 09leisurelarry999No ratings yet

- ECON3Document20 pagesECON3Christelle De Los CientosNo ratings yet

- Economics of Strategy (Rješenja)Document227 pagesEconomics of Strategy (Rješenja)Antonio Hrvoje ŽupićNo ratings yet

- CH 05Document14 pagesCH 05leisurelarry999No ratings yet

- CH 07Document13 pagesCH 07leisurelarry999No ratings yet

- 8 Week Lsat Study Schedule 2017Document19 pages8 Week Lsat Study Schedule 2017Anonymous xgqcVDsgrHNo ratings yet

- Test Bank For Economics of Strategy 7th Edition by DranoveDocument14 pagesTest Bank For Economics of Strategy 7th Edition by Dranovewinry100% (1)

- CH 03Document21 pagesCH 03leisurelarry999100% (1)

- Environment, Power and Culture: Chapter ContentsDocument11 pagesEnvironment, Power and Culture: Chapter Contentsleisurelarry999No ratings yet

- Gmat 6 Ed Og 2019 v2 Problem List Course PDFDocument16 pagesGmat 6 Ed Og 2019 v2 Problem List Course PDFAnubhav ZarabiNo ratings yet

- 2 - Intro To Logical ReasoningDocument12 pages2 - Intro To Logical ReasoningLISA GOLDMANNo ratings yet

- CH 02Document51 pagesCH 02İlke ErçakarNo ratings yet

- Goodman V GallantDocument12 pagesGoodman V GallantAnonymous Azxx3Kp9No ratings yet

- Blanchard Macroeconomicsw7550Document49 pagesBlanchard Macroeconomicsw7550yzl100% (1)

- International Accounting Chap 006Document39 pagesInternational Accounting Chap 006ChuckNo ratings yet

- Besanko Economics of Strategy Ch9Document43 pagesBesanko Economics of Strategy Ch9Ginny WanNo ratings yet

- Essentials of Economic Theory: As Applied to Modern Problems of Industry and Public PolicyFrom EverandEssentials of Economic Theory: As Applied to Modern Problems of Industry and Public PolicyNo ratings yet

- Industry Competitiveness AnalysisDocument49 pagesIndustry Competitiveness AnalysistunggaltriNo ratings yet

- IT 426 Project ManagementDocument4 pagesIT 426 Project ManagementMubashra AhmedNo ratings yet

- U.S. Senate Hearing on Wartime Executive Power and National Security Agency's Surveillance AuthorityFrom EverandU.S. Senate Hearing on Wartime Executive Power and National Security Agency's Surveillance AuthorityNo ratings yet

- Supply and Demand Is Perhaps One of The Most Fundamental Concepts of Economics and It Is The Backbone of A Market EconomyDocument7 pagesSupply and Demand Is Perhaps One of The Most Fundamental Concepts of Economics and It Is The Backbone of A Market EconomyJed FarrellNo ratings yet

- Besanko HarvardDocument228 pagesBesanko Harvardkjmnlkmh100% (1)

- Industrial Economics and Organisation: Conventional and Islamic PerspectivesFrom EverandIndustrial Economics and Organisation: Conventional and Islamic PerspectivesNo ratings yet

- Polar Bear Pirates and Their Quest to Engage the Sleepwalkers: Motivate everyday people to deliver extraordinary resultsFrom EverandPolar Bear Pirates and Their Quest to Engage the Sleepwalkers: Motivate everyday people to deliver extraordinary resultsRating: 4 out of 5 stars4/5 (2)

- Tax Policy and the Economy, Volume 36From EverandTax Policy and the Economy, Volume 36Robert A. MoffittNo ratings yet

- Trained Capacities: John Dewey, Rhetoric, and Democratic PracticeFrom EverandTrained Capacities: John Dewey, Rhetoric, and Democratic PracticeNo ratings yet

- Consumer Behaviour and Utility MaximizationDocument8 pagesConsumer Behaviour and Utility MaximizationJagmohan KalsiNo ratings yet

- The Five PM Lifecyle ModelsDocument3 pagesThe Five PM Lifecyle ModelsJohn N. Constance100% (1)

- A312 SyllabusDocument7 pagesA312 SyllabusHenry ZhuNo ratings yet

- ANTITRUST ECONOMICS AT A TIME OF UPHEAVALFrom EverandANTITRUST ECONOMICS AT A TIME OF UPHEAVALJohn E. KwokaNo ratings yet

- Harvard Referencing: Guide: (Please Note: This Document Was Downloaded From Citethisforme Web Tool, URL )Document13 pagesHarvard Referencing: Guide: (Please Note: This Document Was Downloaded From Citethisforme Web Tool, URL )Benjamin K JaravazaNo ratings yet

- Breaking the Deadlock: The 2000 Election, the Constitution, and the CourtsFrom EverandBreaking the Deadlock: The 2000 Election, the Constitution, and the CourtsRating: 4 out of 5 stars4/5 (4)

- Dec LSAT 2016 Sec 3 PDFDocument8 pagesDec LSAT 2016 Sec 3 PDFSagar PatelNo ratings yet

- Introduction To Business Law Notes: Chapter 1: ContractsDocument11 pagesIntroduction To Business Law Notes: Chapter 1: ContractsRoger Ordoño ManzanasNo ratings yet

- Sec 3 Sep 2016 LSATDocument8 pagesSec 3 Sep 2016 LSATSagar Patel100% (1)

- Questions 1-11 Are Based On The Following PassageDocument3 pagesQuestions 1-11 Are Based On The Following PassageMing db50% (2)

- Micro EconomicsDocument32 pagesMicro Economicsmariyam mohammadNo ratings yet

- LectureSlides Chp6Document24 pagesLectureSlides Chp6hislove00No ratings yet

- LectureSlides Chps3Document7 pagesLectureSlides Chps3hislove00No ratings yet

- Chapter 1 Appendix: Making and Using GraphsDocument10 pagesChapter 1 Appendix: Making and Using Graphshislove00No ratings yet

- Chapters 1 and 2: - Chapter 1 - Getting Started - Chapter 2 - The U.S. and GlobalDocument28 pagesChapters 1 and 2: - Chapter 1 - Getting Started - Chapter 2 - The U.S. and Globalhislove00No ratings yet

- GDP: A Measure of Total Production and IncomeDocument27 pagesGDP: A Measure of Total Production and Incomehislove00No ratings yet

- Business PlanDocument4 pagesBusiness PlanMaria Mendoza AlejandriaNo ratings yet

- Business Level StrategyDocument35 pagesBusiness Level StrategyShiva Kumar Dunaboina100% (1)

- August September 2018 PDFDocument36 pagesAugust September 2018 PDFSanthosh GarapatiNo ratings yet

- Tutorial 5 Solutions FM 201Document6 pagesTutorial 5 Solutions FM 201Achal ChandNo ratings yet

- Valuation Ratios and The Long Run Stock Market OutlookDocument46 pagesValuation Ratios and The Long Run Stock Market OutlookMuhammad Saeed BabarNo ratings yet

- Business Events News For Fri 07 Nov 2014 - High DDR 'Til New Rooms Avail, WCC Gets Green Light, Double Bay Opens, New ICCA Head, and Much MoreDocument3 pagesBusiness Events News For Fri 07 Nov 2014 - High DDR 'Til New Rooms Avail, WCC Gets Green Light, Double Bay Opens, New ICCA Head, and Much MoreBusiness Events NewsNo ratings yet

- Cost Volume Profit AnalysisDocument7 pagesCost Volume Profit Analysissofyan timotyNo ratings yet

- Thesis On Consumer Perception Towards Online Grocery ShoppingDocument53 pagesThesis On Consumer Perception Towards Online Grocery ShoppingPrabhat Ekka100% (2)

- Project NotesDocument82 pagesProject NotesNitesh KhandelwalNo ratings yet

- Liabilities PDFDocument6 pagesLiabilities PDFIya KangNo ratings yet

- Syllabus Grouping of Subjects and Scheme of ExaminationDocument29 pagesSyllabus Grouping of Subjects and Scheme of ExaminationAbhisek AgrawalNo ratings yet

- PEST and SWOT Analysis of MICE Industry in SingaporeDocument5 pagesPEST and SWOT Analysis of MICE Industry in SingaporeMukesh RanaNo ratings yet

- The Set Up: Weekly Puzzle #2: Price or Value?Document2 pagesThe Set Up: Weekly Puzzle #2: Price or Value?PetraNo ratings yet

- Price Elasticity of DemandDocument4 pagesPrice Elasticity of DemandMADmanTalksNo ratings yet

- Classification of Cost. (ODA, ODAIT, ODFB&ODEF)Document4 pagesClassification of Cost. (ODA, ODAIT, ODFB&ODEF)rofoba6609No ratings yet

- Economics in Business Decision Making-I (Micro)Document2 pagesEconomics in Business Decision Making-I (Micro)Abinash oinamNo ratings yet

- RAW CASHEW COST - DocxfinalDocument4 pagesRAW CASHEW COST - DocxfinalBrijesh Panchal100% (1)

- Real Estate Project Analysis: Project: Collina Tinta Location: Hurricane, UtahDocument25 pagesReal Estate Project Analysis: Project: Collina Tinta Location: Hurricane, UtahHema MahourNo ratings yet

- Intermediate May 2019 B5Document23 pagesIntermediate May 2019 B5PASTORYNo ratings yet

- Brambles 1Document15 pagesBrambles 1hotshot2004No ratings yet

- Thesis ProposalDocument13 pagesThesis ProposalBettina MaynardNo ratings yet

- Leather Industry of BangladeshDocument18 pagesLeather Industry of BangladeshSamin Yeaser Khan100% (1)

- Charisse T. Abordo John Wendell D. EscosesDocument66 pagesCharisse T. Abordo John Wendell D. EscosesCharisse AbordoNo ratings yet

- Jasch, Christine. The Use of Environmental Management Accounting (EMA) For Identifying Environmental CostsDocument11 pagesJasch, Christine. The Use of Environmental Management Accounting (EMA) For Identifying Environmental CostsTitoHeidyYantoNo ratings yet

- Economics I 1005Document23 pagesEconomics I 1005meetwithsanjay100% (1)