Download as ppt, pdf, or txt

You might also like

- Fundamentals of Accountancy Business and Management 1 ModuleDocument33 pagesFundamentals of Accountancy Business and Management 1 ModulePoopie poop89% (9)

- DOJ MCL 08-006-Revised Rules Governing Philippine Citizenship Under Republic Act (Ra) 9225Document7 pagesDOJ MCL 08-006-Revised Rules Governing Philippine Citizenship Under Republic Act (Ra) 9225Angela CanaresNo ratings yet

- DNM Vendor BibleDocument93 pagesDNM Vendor BibleWane Stayblur100% (2)

- Abm PPT Week 1 and 2Document50 pagesAbm PPT Week 1 and 2Robertojr sembranoNo ratings yet

- Module 1 PDFDocument21 pagesModule 1 PDFIj Ilarde50% (2)

- Fundamental of AccountingDocument45 pagesFundamental of Accountingckvirtualize100% (6)

- Boulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Document81 pagesBoulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Sita Anuragamayi Claire100% (1)

- Road Construction On Sabkha SoilsDocument6 pagesRoad Construction On Sabkha Soilsganguly147147No ratings yet

- Payment of WagesDocument2 pagesPayment of WagesRoizki Edward Marquez100% (1)

- Nature of Accounting 3Document5 pagesNature of Accounting 3Stela Marie CarandangNo ratings yet

- Chapter 1Document22 pagesChapter 1Abdiwahab AbdikadirNo ratings yet

- 1.1 Inroduction To AccountingDocument3 pages1.1 Inroduction To AccountingTvet AcnNo ratings yet

- 001+002 Advanced Accounting Theory-15.12.2020Document11 pages001+002 Advanced Accounting Theory-15.12.2020Haider Salahaldin ArefNo ratings yet

- Accounting Theory Lecture Note 2Document12 pagesAccounting Theory Lecture Note 2Temitope MuinatNo ratings yet

- AFM Chapter 01Document72 pagesAFM Chapter 01oib ameyaNo ratings yet

- Auditing Symposium XII 1994-p7-44Document38 pagesAuditing Symposium XII 1994-p7-44abigiyaberhanhNo ratings yet

- Accounting For Managers - All in OneDocument445 pagesAccounting For Managers - All in OneYaredNo ratings yet

- Financial Accounting Part IDocument18 pagesFinancial Accounting Part Idannydoly100% (1)

- Prof - Yonas AFM Chapter-1Document221 pagesProf - Yonas AFM Chapter-1ayelelemmaNo ratings yet

- FABMDocument11 pagesFABManglnparungaoNo ratings yet

- MMCO Continuing Professional Development Training Center (CPDTC)Document78 pagesMMCO Continuing Professional Development Training Center (CPDTC)Anjelikka SingianNo ratings yet

- FAR 2018.11.17 18 FreeDocument5 pagesFAR 2018.11.17 18 Freeiraleigh17No ratings yet

- 11 Fabm1 Q3 - M1Document13 pages11 Fabm1 Q3 - M1Syrwin SedaNo ratings yet

- Introduction To Accounting: Earning BjectivesDocument22 pagesIntroduction To Accounting: Earning BjectivesVashirAhmadNo ratings yet

- FUNAC REVIEWERDocument72 pagesFUNAC REVIEWERmanuelsophia.cpaNo ratings yet

- Financial Accounting and Reporting - Week 1 Topic 1 - Overview of AccountingDocument9 pagesFinancial Accounting and Reporting - Week 1 Topic 1 - Overview of AccountingLuisitoNo ratings yet

- ACTBAS 1 Downloaded Lecture NotesDocument89 pagesACTBAS 1 Downloaded Lecture NotesKarla Eunice Aquino Chan100% (1)

- Introduction To Accounting Definition of Accounting: - American Accounting Association (AAA)Document7 pagesIntroduction To Accounting Definition of Accounting: - American Accounting Association (AAA)Rovic GalangcoNo ratings yet

- AF The World of AccountingDocument11 pagesAF The World of AccountingEduardo Enriquez0% (1)

- Class 11 Accountancy NCERT Textbook Chapter 1 Introduction To AccountingDocument27 pagesClass 11 Accountancy NCERT Textbook Chapter 1 Introduction To AccountingAngela BinoyNo ratings yet

- Basic AccountingDocument3 pagesBasic AccountingStephanieNo ratings yet

- Sample of Accounting TextDocument9 pagesSample of Accounting TextAltrupassionate girlNo ratings yet

- Introduction To AccountingDocument22 pagesIntroduction To AccountingAnamika Singh PariharNo ratings yet

- Introduction To AccountingDocument20 pagesIntroduction To AccountingJosh ChuaNo ratings yet

- Introduction of Fund Flow Statement: Chapter-1Document102 pagesIntroduction of Fund Flow Statement: Chapter-1Manjunath RkNo ratings yet

- Introduction To Accounting: Earning BjectivesDocument22 pagesIntroduction To Accounting: Earning Bjectiveslalu morwalNo ratings yet

- Fundamentals of ABM 01 Lesson 1 and 2Document29 pagesFundamentals of ABM 01 Lesson 1 and 2Aldin J PototNo ratings yet

- Confras Module 1Document10 pagesConfras Module 1Lovely Anne LeyesaNo ratings yet

- ACC223 ModuleDocument73 pagesACC223 Module22-52403No ratings yet

- Introduction of Accounting (ABO)Document9 pagesIntroduction of Accounting (ABO)AbbyNo ratings yet

- Introduction To Accounting: Earning BjectivesDocument22 pagesIntroduction To Accounting: Earning BjectivesSIDHI VINAYAKNo ratings yet

- Introduction To Accounting: Earning BjectivesDocument22 pagesIntroduction To Accounting: Earning BjectiveskofirNo ratings yet

- Lesson 1: Introduction To AccountingDocument6 pagesLesson 1: Introduction To AccountingSherwin Hila GammadNo ratings yet

- Mark Edzon A. Bello: ACCY 101 - Fundamentals of Accounting Notre Dame of Marbel UniversityDocument26 pagesMark Edzon A. Bello: ACCY 101 - Fundamentals of Accounting Notre Dame of Marbel UniversityAngel Grace Asuncion0% (1)

- Lesson 1 Introduction To AccountingDocument33 pagesLesson 1 Introduction To AccountingAko si ZoorielNo ratings yet

- Fall Semester 2023-24 Freshers - MGT1125 - TH - AP2023243000008 - Reference-Material-IDocument12 pagesFall Semester 2023-24 Freshers - MGT1125 - TH - AP2023243000008 - Reference-Material-IdandamrajuadityaNo ratings yet

- Principles of AccountingDocument11 pagesPrinciples of AccountingFariza YscondidoNo ratings yet

- Lesson 1: Introduction To AccountingDocument2 pagesLesson 1: Introduction To AccountingMica Bengson TolentinoNo ratings yet

- BRFABM1Document59 pagesBRFABM1tenderjuicyiyyyNo ratings yet

- Introduction To Accounting Theory (1.2)Document39 pagesIntroduction To Accounting Theory (1.2)ika_simple89No ratings yet

- ABO Notes 1Document33 pagesABO Notes 1Rhea MendozaNo ratings yet

- MODULE 1-A AccountingDocument15 pagesMODULE 1-A AccountingRodmar SumugatNo ratings yet

- NOTESabm 11Document3 pagesNOTESabm 11Ina Vei AnchetaNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document5 pagesFundamentals of Accountancy, Business and Management 1Remar Jhon PaineNo ratings yet

- 1 - Introduction To AccountingDocument27 pages1 - Introduction To AccountingIra monick codillaNo ratings yet

- Accounting Overview Standard Setting Conceptual Framework - Docx-1Document23 pagesAccounting Overview Standard Setting Conceptual Framework - Docx-1Thricia Lou OpialaNo ratings yet

- Accounting For Managers.: Corporate MBADocument72 pagesAccounting For Managers.: Corporate MBATerry VincenzoNo ratings yet

- ACTG 1 Summary of LessonDocument5 pagesACTG 1 Summary of LessonTrisha Lei RegisNo ratings yet

- Accounting Theory DevelopmentDocument24 pagesAccounting Theory DevelopmentRajipah OsmanNo ratings yet

- Handouts Acctg 1Document11 pagesHandouts Acctg 1leizlNo ratings yet

- Handouts Acctg 1Document14 pagesHandouts Acctg 1technician laoNo ratings yet

- Notes Unit 1 Introduction To AccountingDocument22 pagesNotes Unit 1 Introduction To Accountingpankhurikiran68No ratings yet

- Introduction To Accounting Quiz 1Document2 pagesIntroduction To Accounting Quiz 1Christian James EdadesNo ratings yet

- Introduction To AccountingDocument21 pagesIntroduction To AccountingZybel RosalesNo ratings yet

- UKAYDocument3 pagesUKAYQueenie AlgireNo ratings yet

- Vegetable SpaghettiDocument1 pageVegetable SpaghettiQueenie AlgireNo ratings yet

- IWD Briefing Document enDocument3 pagesIWD Briefing Document enQueenie AlgireNo ratings yet

- How To Write Macros in ExcelDocument14 pagesHow To Write Macros in ExcelQueenie AlgireNo ratings yet

- Presentation of Financial Statements: IFRS Is Similar But Differences May Relate ToDocument11 pagesPresentation of Financial Statements: IFRS Is Similar But Differences May Relate ToQueenie AlgireNo ratings yet

- 6 Overview of Management AccountingDocument15 pages6 Overview of Management AccountingQueenie AlgireNo ratings yet

- SK Officials: "Mamamayang Nagkaka-Isa Tungo Sa Ika-Uunlad NG Barangay"Document1 pageSK Officials: "Mamamayang Nagkaka-Isa Tungo Sa Ika-Uunlad NG Barangay"Queenie AlgireNo ratings yet

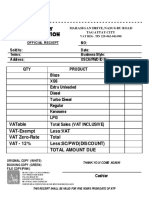

- NO: Sold To: Date: Terms: Business Style: Address: Osca/Pwd Id NoDocument6 pagesNO: Sold To: Date: Terms: Business Style: Address: Osca/Pwd Id NoQueenie AlgireNo ratings yet

- Wk2 1Document43 pagesWk2 1Queenie AlgireNo ratings yet

- Would You Be Willing To Give Up Everything For Your Friends?Document8 pagesWould You Be Willing To Give Up Everything For Your Friends?Queenie AlgireNo ratings yet

- Literary Theory and Schools of CriticismDocument30 pagesLiterary Theory and Schools of CriticismMaravilla JayNo ratings yet

- 4th Semester (Previous YEar Question Paper)Document88 pages4th Semester (Previous YEar Question Paper)HassanNo ratings yet

- Thirty Sixth Annual Report & Accounts: 2020Document80 pagesThirty Sixth Annual Report & Accounts: 2020Mahafuz D. UchsashNo ratings yet

- 04 Snehal Fadale Assignment 2Document10 pages04 Snehal Fadale Assignment 2Snehal FadaleNo ratings yet

- Business Secrets of The Trappist MonksDocument6 pagesBusiness Secrets of The Trappist MonksRaja Wajahat100% (2)

- Water ManagementDocument6 pagesWater Managementjuzreel100% (1)

- Effect of Digitalization and Impact of Employee's PerformanceDocument9 pagesEffect of Digitalization and Impact of Employee's PerformanceAMNA KHAN FITNESSSNo ratings yet

- QS World University Rankings 2020 - Las Mejores Universidades Mundiales - Universidades PrincipalesDocument36 pagesQS World University Rankings 2020 - Las Mejores Universidades Mundiales - Universidades PrincipalesSamael AstarothNo ratings yet

- Transfer Pricing Country Profile BulgariaDocument16 pagesTransfer Pricing Country Profile BulgariaIoanna ZlatevaNo ratings yet

- Chapter 1Document25 pagesChapter 1Naman PalindromeNo ratings yet

- KC CVDocument2 pagesKC CVVishal KeshriNo ratings yet

- Beauty IndustryDocument20 pagesBeauty Industryapi-593844395No ratings yet

- SEIP EDC - BracU InvitationDocument2 pagesSEIP EDC - BracU InvitationMd. Sazzad Hasan.No ratings yet

- JIT CostingDocument2 pagesJIT CostinghellokittysaranghaeNo ratings yet

- Jagdishbhai Madhubhai Patel Vs Saraswatiben Wd/O Asharam ... On 29 July, 2019Document34 pagesJagdishbhai Madhubhai Patel Vs Saraswatiben Wd/O Asharam ... On 29 July, 2019mentorNo ratings yet

- Comp Literacy - Chapter 6 Computer Ethic and SecurityDocument21 pagesComp Literacy - Chapter 6 Computer Ethic and SecuritySheikh VerstappenNo ratings yet

- English Verb - To FlyDocument3 pagesEnglish Verb - To FlyCin Dy E PilNo ratings yet

- Set B: Part 1 A) Using Suitable Software, Prepare The Following Documentations For of SESB SDN BHDDocument12 pagesSet B: Part 1 A) Using Suitable Software, Prepare The Following Documentations For of SESB SDN BHDdini sofiaNo ratings yet

- ConstiLaw - Rubi Vs Provincial Board of MIndoro (39 Phil 660)Document1 pageConstiLaw - Rubi Vs Provincial Board of MIndoro (39 Phil 660)Lu CasNo ratings yet

- Demurrer or Dismiss Debt Collector For Lack of Standing To Sue No Certificate of Authority Secretary of State Foreclosure Credit Cards PDFDocument15 pagesDemurrer or Dismiss Debt Collector For Lack of Standing To Sue No Certificate of Authority Secretary of State Foreclosure Credit Cards PDFאלוהי לוֹחֶםNo ratings yet

- College Schedule: Thursday Friday Saturday Sunday MondayDocument5 pagesCollege Schedule: Thursday Friday Saturday Sunday MondayGomv ConsNo ratings yet

- Castillo v. CruzDocument2 pagesCastillo v. CruzLuna BaciNo ratings yet

- Global MarketingDocument41 pagesGlobal Marketingmelisgozturk100% (2)

- Internship Report On Performance Appraisal System of Janata Bank LimitedDocument47 pagesInternship Report On Performance Appraisal System of Janata Bank LimitedFahimNo ratings yet

- Cash Flow With SolutionsDocument80 pagesCash Flow With SolutionsPhebieon MukwenhaNo ratings yet