Download as ppt, pdf, or txt

You might also like

- Greece: Old Age, Disability, and SurvivorsDocument8 pagesGreece: Old Age, Disability, and Survivorsmaria_d_kNo ratings yet

- ISSA Report On San MarinoDocument4 pagesISSA Report On San Marinomaria handeNo ratings yet

- Italy: Old Age, Disability, and SurvivorsDocument9 pagesItaly: Old Age, Disability, and SurvivorsTiju ThomasNo ratings yet

- Ecc Gsis SssDocument4 pagesEcc Gsis SssWinnie Ann Daquil LomosadNo ratings yet

- Mauritius: Old Age, Disability, and SurvivorsDocument5 pagesMauritius: Old Age, Disability, and SurvivorsAbhishekNo ratings yet

- Age 60 Old-Age Pension (Pension de Retraite) : Age 60 With at Least 15 YearsDocument4 pagesAge 60 Old-Age Pension (Pension de Retraite) : Age 60 With at Least 15 Yearsnanayaw asareNo ratings yet

- Ocial Security IN Alaysia: Present by Teh Pei ShanDocument19 pagesOcial Security IN Alaysia: Present by Teh Pei ShanPei ShanNo ratings yet

- Summary of Social Security and Private Employee Benefits: SpainDocument4 pagesSummary of Social Security and Private Employee Benefits: SpainEra NogNo ratings yet

- X. Social Welfare Legislation: SSS (RA 1161) ) GSIS (RA 8291 ECC (PD 626) Statement of PoliciesDocument4 pagesX. Social Welfare Legislation: SSS (RA 1161) ) GSIS (RA 8291 ECC (PD 626) Statement of PoliciesLoisse VitugNo ratings yet

- CH - III ContinuedDocument7 pagesCH - III ContinuedAmrina RasadhaNo ratings yet

- Health Insurance: DR - Bharat PaulDocument74 pagesHealth Insurance: DR - Bharat PaulAnonymous So5qPSnNo ratings yet

- Social Security Benefits PESSIDocument38 pagesSocial Security Benefits PESSIpakistanzindabadNo ratings yet

- Social Security: By: Archana PatilDocument17 pagesSocial Security: By: Archana PatilArchana PatilNo ratings yet

- E.S.I.Scheme: Employees' State Insurance (Abbreviated As ESI) Is A Self-FinancingDocument9 pagesE.S.I.Scheme: Employees' State Insurance (Abbreviated As ESI) Is A Self-Financingviren thakkarNo ratings yet

- Introduction To Social Security Around The WorldDocument11 pagesIntroduction To Social Security Around The WorldWest Zone ZTINo ratings yet

- NL Questionnaire ES 2013Document15 pagesNL Questionnaire ES 2013Tiago TeixeiraNo ratings yet

- Handicrafts Artisans Comprehensive Welfare Scheme Rajiv Gandhi Shipi Swasthya Bima YojnaDocument8 pagesHandicrafts Artisans Comprehensive Welfare Scheme Rajiv Gandhi Shipi Swasthya Bima YojnatajenderNo ratings yet

- United Kingdom: Old Age, Disability, and SurvivorsDocument8 pagesUnited Kingdom: Old Age, Disability, and SurvivorsOyong HaryadiNo ratings yet

- Social Welfare Systems - China, Japan, Denmark, FranceDocument43 pagesSocial Welfare Systems - China, Japan, Denmark, Francetruezeta100% (1)

- Social Security....Document16 pagesSocial Security....kirandarshakNo ratings yet

- Social Security Measures Across The Countries : Presented byDocument16 pagesSocial Security Measures Across The Countries : Presented byYuvika SinhaNo ratings yet

- Employees State Insurance SchemeDocument8 pagesEmployees State Insurance SchemeKrishnaveni MurugeshNo ratings yet

- France Healthcare SystemsDocument20 pagesFrance Healthcare SystemsRutvik GandhiNo ratings yet

- Comparative Pensions Systems in Africa PresentationDocument30 pagesComparative Pensions Systems in Africa Presentationnanayaw asareNo ratings yet

- Yemen: Old Age, Disability, and SurvivorsDocument3 pagesYemen: Old Age, Disability, and Survivorssameerfarooq420840No ratings yet

- Social Security SystemDocument14 pagesSocial Security SystemAlvin HallarsisNo ratings yet

- Your Social Security Rights in SpainDocument58 pagesYour Social Security Rights in Spain779635006No ratings yet

- Instrumental Performance 261 WorksheetDocument2 pagesInstrumental Performance 261 Worksheetanak gaulNo ratings yet

- Community II - Other AgenciesDocument42 pagesCommunity II - Other AgenciesAnitha AniNo ratings yet

- Social Security GhanaDocument3 pagesSocial Security GhanaTom RyanNo ratings yet

- Esi Act, 1948Document21 pagesEsi Act, 1948sandeep sureshNo ratings yet

- Abhipedia Social Security Class 5 and 6Document3 pagesAbhipedia Social Security Class 5 and 6manishNo ratings yet

- SchemesDocument80 pagesSchemesDrSanthisree BheesettiNo ratings yet

- Governt Health Insurance SchemeDocument62 pagesGovernt Health Insurance Schemesasmita nayakNo ratings yet

- On "Employee's State Insurance Act 1948" of India.Document20 pagesOn "Employee's State Insurance Act 1948" of India.Anshu Shekhar SinghNo ratings yet

- Important Government Schemes Ministry of Agriculturr Lyst8515Document17 pagesImportant Government Schemes Ministry of Agriculturr Lyst8515Prachi SinghNo ratings yet

- The National Pension Reform and Its Benefits To The Ghanaian WorkerDocument19 pagesThe National Pension Reform and Its Benefits To The Ghanaian WorkerJosephine FrempongNo ratings yet

- Social Security PakistanDocument3 pagesSocial Security PakistanSohaib MehmoodNo ratings yet

- Employees' State Insurance Act, 1948Document6 pagesEmployees' State Insurance Act, 1948Ronan GomezNo ratings yet

- ESICDocument34 pagesESICAanchal Mehta100% (1)

- State Insurance Fund - SynopsisDocument3 pagesState Insurance Fund - SynopsisFrans Emily Perez SalvadorNo ratings yet

- Missoc SSG PT 2020 enDocument61 pagesMissoc SSG PT 2020 enbubulacNo ratings yet

- Phr222-Content-Module 4Document12 pagesPhr222-Content-Module 4Peybi Lazaro ChamchamNo ratings yet

- Esi Act 1948-1Document53 pagesEsi Act 1948-1Takshi BatraNo ratings yet

- Madagascar: Old Age, Disability, and SurvivorsDocument6 pagesMadagascar: Old Age, Disability, and Survivors842janxNo ratings yet

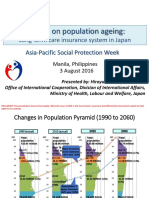

- APSP - Session 9A - Hiroyuki Yamaya - MHLWDocument8 pagesAPSP - Session 9A - Hiroyuki Yamaya - MHLWKristine PresbiteroNo ratings yet

- Health System Model of VietnamDocument20 pagesHealth System Model of Vietnamsneha khuranaNo ratings yet

- Social Security ActDocument5 pagesSocial Security ActArbab Niyaz KhanNo ratings yet

- Govt INSURANCE SchemesDocument3 pagesGovt INSURANCE SchemesshalsmNo ratings yet

- Social Security System in IndiaDocument28 pagesSocial Security System in Indiavaibhav chauhanNo ratings yet

- Purpose, Republic Act No. 1161 As Amended, Otherwise Known As The Social Security LawDocument10 pagesPurpose, Republic Act No. 1161 As Amended, Otherwise Known As The Social Security LawHerrieGabicaNo ratings yet

- Chapter 8 - Social Security and Social InsuranceDocument33 pagesChapter 8 - Social Security and Social Insurancewatts1No ratings yet

- Pension SystemDocument15 pagesPension SystemNitish BhayrauNo ratings yet

- WK 14 - WelfareDocument2 pagesWK 14 - WelfareDinh DanNo ratings yet

- ESI ACT, 1948 (Team 3)Document19 pagesESI ACT, 1948 (Team 3)Rahul RaoNo ratings yet

- Social SecurityDocument15 pagesSocial SecurityMeetoo VikashNo ratings yet

- Occupationalhealth 180403094034Document58 pagesOccupationalhealth 180403094034shravaniNo ratings yet

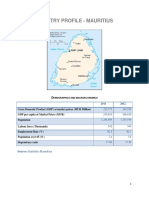

- Mauritius Pension System ProfileDocument9 pagesMauritius Pension System ProfileDarren OwenNo ratings yet

- Pensions in Italy: The guide to pensions in Italy, with the rules for accessing ordinary and early retirement in the public and private systemFrom EverandPensions in Italy: The guide to pensions in Italy, with the rules for accessing ordinary and early retirement in the public and private systemNo ratings yet

- Cost Sheet TheoryDocument3 pagesCost Sheet TheorySurojit SahaNo ratings yet

- Resume Ankur BanerjeeDocument2 pagesResume Ankur BanerjeesanchitNo ratings yet

- Neraca PT Indofood 019,020Document2 pagesNeraca PT Indofood 019,020Nur Abdillah AkmalNo ratings yet

- Bow The KneeDocument12 pagesBow The KneeQueen GersavaNo ratings yet

- You Exec - Timeline Template FreeDocument17 pagesYou Exec - Timeline Template FreeÍcaro Filipe BragaNo ratings yet

- LenskartDocument4 pagesLenskartchirag shahNo ratings yet

- Australian Motorcycle News 24.09.2020Document116 pagesAustralian Motorcycle News 24.09.2020autotech master100% (1)

- Resume MinnieDocument3 pagesResume Minnieapi-290107358No ratings yet

- Liderazgo en Enfermería y Burnout (Pucheu, 2010)Document8 pagesLiderazgo en Enfermería y Burnout (Pucheu, 2010)Carolina Oyarzún PérezNo ratings yet

- CC Brochure 2 Hi-ResDocument2 pagesCC Brochure 2 Hi-ResRashid BumarwaNo ratings yet

- 1-Modern Management Theories andDocument17 pages1-Modern Management Theories andAlia Al ZghoulNo ratings yet

- FM 11.14.18 - ANGELINA County - State Court Complaint - FINALDocument221 pagesFM 11.14.18 - ANGELINA County - State Court Complaint - FINALAshley SlaytonNo ratings yet

- Republic Acts For Urban DevelopmentDocument92 pagesRepublic Acts For Urban DevelopmentAnamarie C. CamasinNo ratings yet

- A Concise Introduction To The Amdo DialeDocument20 pagesA Concise Introduction To The Amdo DialeJason Franklin100% (1)

- Nilai Syair Sayed Idrus Bin Salim Aljufri (Guru Tua) Dan Implikasinya Pada Pendidikan KarakterDocument11 pagesNilai Syair Sayed Idrus Bin Salim Aljufri (Guru Tua) Dan Implikasinya Pada Pendidikan KarakterMuhammad ArmansyahNo ratings yet

- Test 1 For Unit 6Document3 pagesTest 1 For Unit 6Hang TruongNo ratings yet

- Still Electric Fork Truck r60 16 r60 18 r6021 r6010 Spare Parts List deDocument22 pagesStill Electric Fork Truck r60 16 r60 18 r6021 r6010 Spare Parts List depamelacobb190286bef100% (119)

- Motion To Vacate Order of DisbarmentDocument28 pagesMotion To Vacate Order of DisbarmentMark A. Adams JD/MBA100% (3)

- 11 Chapter 7 Travel and TourismDocument19 pages11 Chapter 7 Travel and TourismAditya ThoreNo ratings yet

- The Austrian School - Jesus Huerta de Soto PDFDocument140 pagesThe Austrian School - Jesus Huerta de Soto PDFarminabc67No ratings yet

- Sales and LeaseDocument12 pagesSales and LeaseJemNo ratings yet

- Portfolio Educational PhilosophyDocument3 pagesPortfolio Educational Philosophyapi-507434783No ratings yet

- Ehris Action PlanDocument2 pagesEhris Action PlanDeeh Jae BondaNo ratings yet

- Charismatic Leadership and Social Change: A Weberian PrespectiveDocument9 pagesCharismatic Leadership and Social Change: A Weberian PrespectiveAnonymous CwJeBCAXpNo ratings yet

- What Is The Difference Between Capital Market Line and Security Market LineDocument3 pagesWhat Is The Difference Between Capital Market Line and Security Market LineAnnum Rafique100% (2)

- Corporation Law CasesDocument22 pagesCorporation Law CasesJessica Joyce PenalosaNo ratings yet

- Tijuana Know Your Rights Tourist GuideDocument12 pagesTijuana Know Your Rights Tourist GuideXinJeisan100% (3)

- MIA320 Study Guide 2023 25julyDocument9 pagesMIA320 Study Guide 2023 25julyKatlego MaganoNo ratings yet

- Indonesia's Regional and Global Engagement: Role Theory and State Transformation in Foreign Policy 1st Edition Moch Faisal KarimDocument70 pagesIndonesia's Regional and Global Engagement: Role Theory and State Transformation in Foreign Policy 1st Edition Moch Faisal Karimderek.bambacigno959100% (11)

- Fruit of The Spirit Study GuideDocument14 pagesFruit of The Spirit Study Guidexjamber100% (1)