Download as ppt, pdf, or txt

You might also like

- Top Notch Fundamentals Unit 11 AssessmentDocument8 pagesTop Notch Fundamentals Unit 11 AssessmentBe Haj50% (2)

- The Biological Enterprise Sex Mind Profit From Human Engineering To Sociobiology - Donna HarawayDocument32 pagesThe Biological Enterprise Sex Mind Profit From Human Engineering To Sociobiology - Donna HarawayLucas Rodrigues100% (1)

- Chapter 3 - Job Order Costing-01022021 - GLDocument66 pagesChapter 3 - Job Order Costing-01022021 - GLStavria KalliNo ratings yet

- Product Costing and Cost Accumulation in A Batch Production EnvironmentDocument58 pagesProduct Costing and Cost Accumulation in A Batch Production EnvironmentWali NoorzadNo ratings yet

- Product Costing and Cost Accumulation in A Batch Production EnvironmentDocument50 pagesProduct Costing and Cost Accumulation in A Batch Production EnvironmentAbdelrahman El-shafaeeNo ratings yet

- Product Costing1Document75 pagesProduct Costing1kukuh setiawanNo ratings yet

- Product Costing and Cost Accumulation in A Batch Production EnvironmentDocument56 pagesProduct Costing and Cost Accumulation in A Batch Production Environmentsunanda mNo ratings yet

- Ronald Hilton Chapter 3Document25 pagesRonald Hilton Chapter 3Difen L HaradiniNo ratings yet

- Costing SystemDocument89 pagesCosting SystemYonathan ShiferawNo ratings yet

- Chapter 21 - Process CostingDocument58 pagesChapter 21 - Process Costingbinzcqtak16No ratings yet

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument25 pagesBasic Cost Management Concepts and Accounting For Mass Customization OperationsTalitha ApsariNo ratings yet

- Chap004 7e EditedDocument47 pagesChap004 7e EditedfarahNo ratings yet

- 6un44rh0q - Cost Accounting and ControlDocument75 pages6un44rh0q - Cost Accounting and ControlJustine Marie BalderasNo ratings yet

- Cost Accounting SystemsDocument4 pagesCost Accounting SystemsEDELYN PoblacionNo ratings yet

- CH 21Document70 pagesCH 21Shakib Ahmed Emon 0389No ratings yet

- LH - 04 - CAC - Job Order Costing - StudentDocument16 pagesLH - 04 - CAC - Job Order Costing - StudentRaven Claire ContrerasNo ratings yet

- Management Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakDocument58 pagesManagement Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakSiddharthNo ratings yet

- ACCY918 T3 2023 Wk3 Process Costing Lecture NoteDocument82 pagesACCY918 T3 2023 Wk3 Process Costing Lecture NoteNIRAJ SharmaNo ratings yet

- CMA I - Chapter 4, Process CostingDocument68 pagesCMA I - Chapter 4, Process CostingLakachew GetasewNo ratings yet

- UntitledDocument16 pagesUntitledMaria Nena LoretoNo ratings yet

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument89 pagesBasic Cost Management Concepts and Accounting For Mass Customization OperationsabeeraNo ratings yet

- IffatZehra - 2972 - 15876 - 1 - Chap 3 - Process CostingDocument77 pagesIffatZehra - 2972 - 15876 - 1 - Chap 3 - Process CostingSabeeh Mustafa ZubairiNo ratings yet

- Activity-Based Costing: John Wiley & Sons, Inc. © 2005Document22 pagesActivity-Based Costing: John Wiley & Sons, Inc. © 2005Gennelyn Grace PeñaredondoNo ratings yet

- LH 04 CAC Job Order Costing StudentDocument19 pagesLH 04 CAC Job Order Costing Studentaincrad152251No ratings yet

- Chapter 3 - Virtual - Classroom-M.Document61 pagesChapter 3 - Virtual - Classroom-M.rebeccahf7No ratings yet

- Activity BasedcostingsystemDocument35 pagesActivity Basedcostingsystemsunil27No ratings yet

- Chapter 5Document29 pagesChapter 5spambryan888No ratings yet

- Notes 1Document3 pagesNotes 1Bercasio KelvinNo ratings yet

- Understanding Costs For Management Decisions: Uaa - Acct 650 Seminar in Executive Uses of Accounting Dr. Fred BarbeeDocument92 pagesUnderstanding Costs For Management Decisions: Uaa - Acct 650 Seminar in Executive Uses of Accounting Dr. Fred BarbeeAhmed RazaNo ratings yet

- Chapter 2 Cost ClassificationsDocument18 pagesChapter 2 Cost Classificationsmarizemeyer2No ratings yet

- Management Accounting Session 3 Job Order Costing: Indian Institute of Management RohtakDocument52 pagesManagement Accounting Session 3 Job Order Costing: Indian Institute of Management RohtakSiddharthNo ratings yet

- Cost AnalysisDocument36 pagesCost AnalysisHarisagar ThulasiramanNo ratings yet

- CHPT 03 HODocument22 pagesCHPT 03 HOKerby Gail RulonaNo ratings yet

- Cost TutorialDocument26 pagesCost TutorialedrianclydeNo ratings yet

- Chapter 2 Cost Terms Concepts and ClassificationsDocument51 pagesChapter 2 Cost Terms Concepts and ClassificationsMulugeta Girma100% (1)

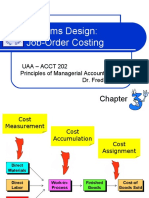

- Systems Design: Job-Order Costing: Chapter ThreeDocument86 pagesSystems Design: Job-Order Costing: Chapter Threesaka haiNo ratings yet

- Job CostingDocument9 pagesJob CostingParikshit KunduNo ratings yet

- Session 5 Job CostingDocument58 pagesSession 5 Job CostingJoeyNo ratings yet

- Systems Design: Job-Order Costing: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeDocument22 pagesSystems Design: Job-Order Costing: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeOrnica BalesNo ratings yet

- Chapter 3 System Design Job Order Costing SystemDocument76 pagesChapter 3 System Design Job Order Costing SystemMulugeta GirmaNo ratings yet

- Product Cost Flows and Business OrganizationsDocument48 pagesProduct Cost Flows and Business OrganizationsGaluh Boga KuswaraNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinNo ratings yet

- PPB Co Training - Product Costing: by Sudhakara Reddy JakkuDocument24 pagesPPB Co Training - Product Costing: by Sudhakara Reddy Jakkuabhi2244inNo ratings yet

- Highlight The Proper Classification of The Cost Items/expenses Non-Manufacturing Costs/Period CostsDocument1 pageHighlight The Proper Classification of The Cost Items/expenses Non-Manufacturing Costs/Period CostsHarold GarciaNo ratings yet

- Activity Based CostingDocument27 pagesActivity Based CostingsurendarNo ratings yet

- AF3112 Management Accounting 2: Process CostingDocument66 pagesAF3112 Management Accounting 2: Process Costing行歌No ratings yet

- Lecture-8.2 Job Order Costing (Theory With Problem)Document13 pagesLecture-8.2 Job Order Costing (Theory With Problem)Nazmul-Hassan Sumon100% (2)

- Context of ManufacturingDocument23 pagesContext of ManufacturingmashalerahNo ratings yet

- BMFP 4512 Chapter-3B PresentationDocument118 pagesBMFP 4512 Chapter-3B PresentationHaery SihombingNo ratings yet

- Chapter 5 - Job Order CostingDocument20 pagesChapter 5 - Job Order CostingviraNo ratings yet

- Cost I Ch. 3Document57 pagesCost I Ch. 3Magarsaa AmaanNo ratings yet

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument116 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinImran RafiqNo ratings yet

- Job-Order Costing and Modern Manufacturing PracticesDocument32 pagesJob-Order Costing and Modern Manufacturing PracticesPriyadarshi Saini100% (1)

- Job Order CostingDocument81 pagesJob Order CostingmohsinNo ratings yet

- Akb Bab4Document37 pagesAkb Bab4MulyaniNo ratings yet

- Cost Accounting Part 1Document21 pagesCost Accounting Part 1Mostafa ElgendyNo ratings yet

- Product CostingDocument29 pagesProduct CostingBen ShahbandarNo ratings yet

- ABC Analysis and Process Costing MCQsDocument8 pagesABC Analysis and Process Costing MCQsMantasha ShaikhNo ratings yet

- Job and Process IDocument19 pagesJob and Process IsajjadNo ratings yet

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument54 pagesBasic Cost Management Concepts and Accounting For Mass Customization OperationsAshesh DasNo ratings yet

- ABC Costing PDFDocument33 pagesABC Costing PDFDrpranav SaraswatNo ratings yet

- Behaviorism and Language LearningDocument8 pagesBehaviorism and Language LearningJonas Nhl100% (1)

- Nucl - Phys.B v.594Document784 pagesNucl - Phys.B v.594buddy72No ratings yet

- Ibf AssignmentDocument55 pagesIbf AssignmentrashiNo ratings yet

- CEO Monetization Playbook - VvimpDocument28 pagesCEO Monetization Playbook - VvimpvkandulaNo ratings yet

- Daily Activity Report: - KSA TeamDocument2 pagesDaily Activity Report: - KSA TeamHaidar Ali ZaidiNo ratings yet

- Who - Global Report Measles N Rubela 2015 PDFDocument56 pagesWho - Global Report Measles N Rubela 2015 PDFAbongky AbroeryNo ratings yet

- Medieval Ages - Plainchant-1Document3 pagesMedieval Ages - Plainchant-1Hannah TrippNo ratings yet

- Statistical MechanicsDocument25 pagesStatistical MechanicsKaren MorenoNo ratings yet

- RDC SolarDocument35 pagesRDC SolarRitabrata DharNo ratings yet

- Water PumpsDocument4 pagesWater PumpsEphremHailuNo ratings yet

- Property Notes A.Y. 2011-2012 Atty. Lopez-Rosario LecturesDocument7 pagesProperty Notes A.Y. 2011-2012 Atty. Lopez-Rosario LecturesAlit Dela CruzNo ratings yet

- Transparent Governance in An Age of AbundanceDocument452 pagesTransparent Governance in An Age of AbundancePamela GaviñoNo ratings yet

- Rav Kaduri ZTVKL TDocument11 pagesRav Kaduri ZTVKL TGregory HooNo ratings yet

- Effect of Occupational Safety and Health Risk Management On The Rate of Work - Related Accidents in The Bulgarian Furniture IndustryDocument15 pagesEffect of Occupational Safety and Health Risk Management On The Rate of Work - Related Accidents in The Bulgarian Furniture IndustryFaizahNo ratings yet

- Project Report - Study and Comparative Analysis of Special Loyalty Program Run by Telecom Operator - Vodafone - Jaipur (Raj.)Document103 pagesProject Report - Study and Comparative Analysis of Special Loyalty Program Run by Telecom Operator - Vodafone - Jaipur (Raj.)Ritesh GoyalNo ratings yet

- DS TasklistDocument5 pagesDS TasklistRiska Kurnianto SkaNo ratings yet

- Ies, Iia and IpDocument46 pagesIes, Iia and IpRosalie E. BalhagNo ratings yet

- Embassy ReitDocument386 pagesEmbassy ReitReTHINK INDIANo ratings yet

- General Course ExpectationsDocument2 pagesGeneral Course ExpectationsJoshuaNo ratings yet

- Exam Paper For English Year 3Document8 pagesExam Paper For English Year 3Safrena DifErraNo ratings yet

- OnlineSvcsConsolidatedSLA (WW) (English) (February2024) (CR)Document118 pagesOnlineSvcsConsolidatedSLA (WW) (English) (February2024) (CR)Uriel TijerinoNo ratings yet

- ZW InstructionsManualDocument36 pagesZW InstructionsManualJulio SantosNo ratings yet

- Choose The Right Word:: Up (x2) Bad Sourness No (x2) Go (x2) Big (x3) There Wrong HideDocument2 pagesChoose The Right Word:: Up (x2) Bad Sourness No (x2) Go (x2) Big (x3) There Wrong HideDayani BravoNo ratings yet

- 5S Color Chart: Equipment SafetyDocument1 page5S Color Chart: Equipment SafetyOP AryaNo ratings yet

- J OperatorDocument6 pagesJ OperatorManikandan SundararajNo ratings yet

- New Asian Writing: Hantu: A Malaysian Ghost Story' by J.C. Martin (Malaysia)Document10 pagesNew Asian Writing: Hantu: A Malaysian Ghost Story' by J.C. Martin (Malaysia)maithis chandranNo ratings yet

- Pixel Tactics Rules Summary v1Document2 pagesPixel Tactics Rules Summary v1Vicente Martínez LópezNo ratings yet

- Report On The Marketing Strategy Of: Submitted ToDocument15 pagesReport On The Marketing Strategy Of: Submitted ToMd Basit Chowdhury 1831829630No ratings yet