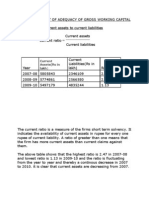

Study ON Working Capital Management: Conducted at HMT Limited, Tractor Bussiness Group, Pinjore

Study ON Working Capital Management: Conducted at HMT Limited, Tractor Bussiness Group, Pinjore

You might also like

- FM 2 Real Project 2Document12 pagesFM 2 Real Project 2Shannan Richards100% (1)

- DNM Vendor BibleDocument93 pagesDNM Vendor BibleWane Stayblur100% (2)

- SampaSoln EXCELDocument4 pagesSampaSoln EXCELRasika Pawar-HaldankarNo ratings yet

- Case Study: Airport Express Metro Line: Project Financing ModelDocument6 pagesCase Study: Airport Express Metro Line: Project Financing ModelrohitmahaliNo ratings yet

- Boulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Document81 pagesBoulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Sita Anuragamayi Claire100% (1)

- The Metatheatre in Rosencrantz and Guildenstern Are DeadDocument2 pagesThe Metatheatre in Rosencrantz and Guildenstern Are DeadKingshuk Mondal67% (3)

- Amy Tsui - Classroom Discourse Research & EthnographyDocument23 pagesAmy Tsui - Classroom Discourse Research & EthnographyMastho ZhengNo ratings yet

- ANALYSIS of Working Capital With Balance Sheet and Profit and LossDocument33 pagesANALYSIS of Working Capital With Balance Sheet and Profit and Losssonabeta07No ratings yet

- The Graph Showing Net Working CapitalDocument31 pagesThe Graph Showing Net Working CapitalPRATIK PALKHENo ratings yet

- Chapter-Iv Data Analysis & InterpretionDocument20 pagesChapter-Iv Data Analysis & InterpretionSubbaRaoNo ratings yet

- Ratio Analysis HyundaiDocument12 pagesRatio Analysis HyundaiAnkit MistryNo ratings yet

- MBA Finance Project Convert - 66-90Document25 pagesMBA Finance Project Convert - 66-90akakahaha010No ratings yet

- ImmanuelDocument25 pagesImmanuelManojManuNo ratings yet

- Ratio AnalysisDocument36 pagesRatio AnalysisAditya SawantNo ratings yet

- Project Report of AnkushDocument21 pagesProject Report of AnkushdinnubhattNo ratings yet

- Uttar Pradesh Revene Sector 3 2013 Chap 2Document26 pagesUttar Pradesh Revene Sector 3 2013 Chap 2rajendra lalNo ratings yet

- Final Project of AccountingDocument23 pagesFinal Project of Accountingpirzada Arslan sabri100% (1)

- Port of Beirut DataDocument46 pagesPort of Beirut DataShubh MandalNo ratings yet

- FINANCIAL ANALYSIS of AMUL - 122742796 PDFDocument7 pagesFINANCIAL ANALYSIS of AMUL - 122742796 PDFbhavin rathodNo ratings yet

- Ratio Analysis: S.ClementDocument32 pagesRatio Analysis: S.ClementJugal ShahNo ratings yet

- A Report On Financial Analysis On BHARTI AIRTEL LTDDocument27 pagesA Report On Financial Analysis On BHARTI AIRTEL LTDJeet DhanakNo ratings yet

- Chapter IV,. 9Document37 pagesChapter IV,. 9Anonymous nTxB1EPvNo ratings yet

- Public Economics ProjectDocument13 pagesPublic Economics ProjectPoulami RoyNo ratings yet

- Analysis and Discussion 6.1 Current RatioDocument86 pagesAnalysis and Discussion 6.1 Current RatioMAYUGAMNo ratings yet

- Project Report On Financial Statement Analysis of Bata Shoes and Servis ShoesDocument22 pagesProject Report On Financial Statement Analysis of Bata Shoes and Servis Shoessujit_ranjanNo ratings yet

- Ques On 1: GNP at Factor Cost (1985 - 2000)Document8 pagesQues On 1: GNP at Factor Cost (1985 - 2000)Reuben RichardNo ratings yet

- Ratio Analysis: Pakistan State OilDocument19 pagesRatio Analysis: Pakistan State OilMUHAMMAD MUDASSAR TAHIR NCBA&ENo ratings yet

- 4 ChapterDocument35 pages4 ChapterantonyNo ratings yet

- Bajaj - Hero Honda ComparisonDocument11 pagesBajaj - Hero Honda ComparisonPunit SardaNo ratings yet

- Financial Reporting and Analysis PDFDocument2 pagesFinancial Reporting and Analysis PDFTushar VatsNo ratings yet

- Financial Ratio Analysis: by Syndicate No. - 5Document16 pagesFinancial Ratio Analysis: by Syndicate No. - 5nehaNo ratings yet

- Current Assets (Rs in Lakh)Document35 pagesCurrent Assets (Rs in Lakh)Jagadeesh MuthikiNo ratings yet

- Profitability Analysis of Tata Motors: AbhinavDocument8 pagesProfitability Analysis of Tata Motors: AbhinavAman KhanNo ratings yet

- Current Assets To Proprieors FundsDocument8 pagesCurrent Assets To Proprieors FundsindramuniNo ratings yet

- Lbo Case StudyDocument6 pagesLbo Case StudyRishabh MishraNo ratings yet

- Ratios of Comp.Document25 pagesRatios of Comp.ashish5016No ratings yet

- Suggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsDocument16 pagesSuggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsMdAnjum1991No ratings yet

- Advanced Financial Accounting: Ratio Analysis and InterpretationDocument21 pagesAdvanced Financial Accounting: Ratio Analysis and InterpretationKowsik RajendranNo ratings yet

- Chapter 7 Prospective Analysis: Valuation Theory and ConceptsDocument7 pagesChapter 7 Prospective Analysis: Valuation Theory and ConceptsWalm KetyNo ratings yet

- A Comparitive Analysis of Working Capital ofDocument19 pagesA Comparitive Analysis of Working Capital ofManasvi MehtaNo ratings yet

- A Comparitive Analysis of Working Capital ofDocument19 pagesA Comparitive Analysis of Working Capital ofManasvi MehtaNo ratings yet

- Research Paper On Working Capital Management Made by Satyam KumarDocument3 pagesResearch Paper On Working Capital Management Made by Satyam Kumarsatyam skNo ratings yet

- Ratio Analysis (Group 5-Glc - Ib)Document53 pagesRatio Analysis (Group 5-Glc - Ib)Nikam PranitNo ratings yet

- Cu R R E N T - R A T I O: Fixed Assets RatioDocument11 pagesCu R R E N T - R A T I O: Fixed Assets RatioRoshan KumarNo ratings yet

- Tanjung Offshore: Turning Attractive Upgrade To BuyDocument4 pagesTanjung Offshore: Turning Attractive Upgrade To Buykhlis81No ratings yet

- NTPC Ratio Analysis - FinalDocument45 pagesNTPC Ratio Analysis - FinalniradharNo ratings yet

- Orissa Electricity Regulatory Commission Bidyut Niyamak Bhavan Unit - Viii, Bhubaneswar - 751 012 No - DIR (T) - 371/09/ Dated-.07.2011Document22 pagesOrissa Electricity Regulatory Commission Bidyut Niyamak Bhavan Unit - Viii, Bhubaneswar - 751 012 No - DIR (T) - 371/09/ Dated-.07.2011havejsnjNo ratings yet

- Assignment: 1: Financial Accounting and AnalysisDocument12 pagesAssignment: 1: Financial Accounting and AnalysisFogey RulzNo ratings yet

- GGP Final2010Document23 pagesGGP Final2010Frank ParkerNo ratings yet

- BF AssignmentDocument13 pagesBF AssignmentMomina waseemNo ratings yet

- Results & Discussion: Table - 1 Gross Profit Ratio Year Gross Profit Net Sales 100 RatioDocument9 pagesResults & Discussion: Table - 1 Gross Profit Ratio Year Gross Profit Net Sales 100 RatioeswariNo ratings yet

- NTPC Ratio Analysis FinalDocument45 pagesNTPC Ratio Analysis FinalDaman Deep SinghNo ratings yet

- Working Capital Management & Operating Cycle: Bajaj AutomobilesDocument22 pagesWorking Capital Management & Operating Cycle: Bajaj Automobilesdivanshugupta1988No ratings yet

- Working Capital ManagementDocument33 pagesWorking Capital ManagementPRATIK PALKHENo ratings yet

- Overall Budgetary Position 2009-10: Chart - 1Document43 pagesOverall Budgetary Position 2009-10: Chart - 1reddygantasri31No ratings yet

- Ratios OriginaDocument19 pagesRatios OriginaVivek RajNo ratings yet

- AnalysisDocument8 pagesAnalysisAnjali AnandNo ratings yet

- Mcdonal's Finanical RatiosDocument11 pagesMcdonal's Finanical RatiosFahad Khan TareenNo ratings yet

- Working Capital Ppt-3Document34 pagesWorking Capital Ppt-3bala muraliNo ratings yet

- Finance&Accounts T3 SolutionDocument4 pagesFinance&Accounts T3 Solutionkanika thakurNo ratings yet

- Project Analysis: Principles of Corporate FinanceDocument16 pagesProject Analysis: Principles of Corporate FinancechooisinNo ratings yet

- Ashok Leyland LTD Company AnalysisDocument13 pagesAshok Leyland LTD Company AnalysisRaghav100% (30)

- Building Inspection Service Revenues World Summary: Market Values & Financials by CountryFrom EverandBuilding Inspection Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Nabard (National Bank For Agriculture and Rural Development)Document21 pagesNabard (National Bank For Agriculture and Rural Development)ds_frnship4235No ratings yet

- Clinic Management System Project For Final Year: Sarfaraj AlamDocument6 pagesClinic Management System Project For Final Year: Sarfaraj AlamUDAY SOLUTIONSNo ratings yet

- Me 425 (Case Study) Raymar B. AquinoDocument3 pagesMe 425 (Case Study) Raymar B. AquinoJoan Joy BalgosNo ratings yet

- Municipality of San Narciso Vs Mendez Sr. DigestDocument2 pagesMunicipality of San Narciso Vs Mendez Sr. DigestMark MlsNo ratings yet

- Ice Breakers and Team Builders PacketDocument54 pagesIce Breakers and Team Builders Packetnissefar007100% (1)

- Blkpay 20230518Document4 pagesBlkpay 20230518Raman GoyalNo ratings yet

- FC CantocoralvocalDocument320 pagesFC Cantocoralvocalfelix miguelNo ratings yet

- Alternative DevelopmentDocument28 pagesAlternative DevelopmentOmar100% (1)

- KC CVDocument2 pagesKC CVVishal KeshriNo ratings yet

- Greatest Robbery of A Government Guinness World RecordsDocument1 pageGreatest Robbery of A Government Guinness World Recordsrex ceeNo ratings yet

- WFP ToR For Assistance To Syrian Refugees PDFDocument38 pagesWFP ToR For Assistance To Syrian Refugees PDFRuNo ratings yet

- A. Kroeber - The Superorganic PDFDocument64 pagesA. Kroeber - The Superorganic PDFmissmouNo ratings yet

- 17 Atci Overseas Corporation v. Ma Josefa Echin GR No 178551Document3 pages17 Atci Overseas Corporation v. Ma Josefa Echin GR No 178551Paula TorobaNo ratings yet

- WUS101-BUSINESS PLAN FORMAT - English MAC2020Document19 pagesWUS101-BUSINESS PLAN FORMAT - English MAC2020Ahmad Mujahid Che RahimiNo ratings yet

- Turn in For LTC MANDAL NCDocument2 pagesTurn in For LTC MANDAL NCMary Anne GamboaNo ratings yet

- Latest RFQ (Hospet Bellary Karntaka Dated - 29102010Document69 pagesLatest RFQ (Hospet Bellary Karntaka Dated - 29102010xanblakeNo ratings yet

- WhizKids Questions-UneditedDocument5 pagesWhizKids Questions-UneditedSVTKhsiaNo ratings yet

- Kelvion Walker Vs Amy WilburnDocument63 pagesKelvion Walker Vs Amy WilburnHorrible CrimeNo ratings yet

- 5yr Prog Case Digests PDFDocument346 pages5yr Prog Case Digests PDFMary Neil GalvisoNo ratings yet

- 02.13-02.17 - Sales Activity Report (Vivi)Document2 pages02.13-02.17 - Sales Activity Report (Vivi)ptsoutherntristar0No ratings yet

- Joycelyn PabloDocument6 pagesJoycelyn PabloAriza ValenciaNo ratings yet

- Assignment in Psychology of Law EnforcementDocument4 pagesAssignment in Psychology of Law EnforcementKRISTINE DEE L VELASCONo ratings yet

- Barriers To International TradeDocument12 pagesBarriers To International TraderajeshratnavelsamyNo ratings yet

- Comp Literacy - Chapter 6 Computer Ethic and SecurityDocument21 pagesComp Literacy - Chapter 6 Computer Ethic and SecuritySheikh VerstappenNo ratings yet

- Outsorcing ContractsDocument113 pagesOutsorcing ContractsfilipeammoreiraNo ratings yet

- Exam NotesDocument104 pagesExam NotesJezMillerNo ratings yet

Download as ppt, pdf, or txt

You might also like

- FM 2 Real Project 2Document12 pagesFM 2 Real Project 2Shannan Richards100% (1)

- DNM Vendor BibleDocument93 pagesDNM Vendor BibleWane Stayblur100% (2)

- SampaSoln EXCELDocument4 pagesSampaSoln EXCELRasika Pawar-HaldankarNo ratings yet

- Case Study: Airport Express Metro Line: Project Financing ModelDocument6 pagesCase Study: Airport Express Metro Line: Project Financing ModelrohitmahaliNo ratings yet

- Boulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Document81 pagesBoulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Sita Anuragamayi Claire100% (1)

- The Metatheatre in Rosencrantz and Guildenstern Are DeadDocument2 pagesThe Metatheatre in Rosencrantz and Guildenstern Are DeadKingshuk Mondal67% (3)

- Amy Tsui - Classroom Discourse Research & EthnographyDocument23 pagesAmy Tsui - Classroom Discourse Research & EthnographyMastho ZhengNo ratings yet

- ANALYSIS of Working Capital With Balance Sheet and Profit and LossDocument33 pagesANALYSIS of Working Capital With Balance Sheet and Profit and Losssonabeta07No ratings yet

- The Graph Showing Net Working CapitalDocument31 pagesThe Graph Showing Net Working CapitalPRATIK PALKHENo ratings yet

- Chapter-Iv Data Analysis & InterpretionDocument20 pagesChapter-Iv Data Analysis & InterpretionSubbaRaoNo ratings yet

- Ratio Analysis HyundaiDocument12 pagesRatio Analysis HyundaiAnkit MistryNo ratings yet

- MBA Finance Project Convert - 66-90Document25 pagesMBA Finance Project Convert - 66-90akakahaha010No ratings yet

- ImmanuelDocument25 pagesImmanuelManojManuNo ratings yet

- Ratio AnalysisDocument36 pagesRatio AnalysisAditya SawantNo ratings yet

- Project Report of AnkushDocument21 pagesProject Report of AnkushdinnubhattNo ratings yet

- Uttar Pradesh Revene Sector 3 2013 Chap 2Document26 pagesUttar Pradesh Revene Sector 3 2013 Chap 2rajendra lalNo ratings yet

- Final Project of AccountingDocument23 pagesFinal Project of Accountingpirzada Arslan sabri100% (1)

- Port of Beirut DataDocument46 pagesPort of Beirut DataShubh MandalNo ratings yet

- FINANCIAL ANALYSIS of AMUL - 122742796 PDFDocument7 pagesFINANCIAL ANALYSIS of AMUL - 122742796 PDFbhavin rathodNo ratings yet

- Ratio Analysis: S.ClementDocument32 pagesRatio Analysis: S.ClementJugal ShahNo ratings yet

- A Report On Financial Analysis On BHARTI AIRTEL LTDDocument27 pagesA Report On Financial Analysis On BHARTI AIRTEL LTDJeet DhanakNo ratings yet

- Chapter IV,. 9Document37 pagesChapter IV,. 9Anonymous nTxB1EPvNo ratings yet

- Public Economics ProjectDocument13 pagesPublic Economics ProjectPoulami RoyNo ratings yet

- Analysis and Discussion 6.1 Current RatioDocument86 pagesAnalysis and Discussion 6.1 Current RatioMAYUGAMNo ratings yet

- Project Report On Financial Statement Analysis of Bata Shoes and Servis ShoesDocument22 pagesProject Report On Financial Statement Analysis of Bata Shoes and Servis Shoessujit_ranjanNo ratings yet

- Ques On 1: GNP at Factor Cost (1985 - 2000)Document8 pagesQues On 1: GNP at Factor Cost (1985 - 2000)Reuben RichardNo ratings yet

- Ratio Analysis: Pakistan State OilDocument19 pagesRatio Analysis: Pakistan State OilMUHAMMAD MUDASSAR TAHIR NCBA&ENo ratings yet

- 4 ChapterDocument35 pages4 ChapterantonyNo ratings yet

- Bajaj - Hero Honda ComparisonDocument11 pagesBajaj - Hero Honda ComparisonPunit SardaNo ratings yet

- Financial Reporting and Analysis PDFDocument2 pagesFinancial Reporting and Analysis PDFTushar VatsNo ratings yet

- Financial Ratio Analysis: by Syndicate No. - 5Document16 pagesFinancial Ratio Analysis: by Syndicate No. - 5nehaNo ratings yet

- Current Assets (Rs in Lakh)Document35 pagesCurrent Assets (Rs in Lakh)Jagadeesh MuthikiNo ratings yet

- Profitability Analysis of Tata Motors: AbhinavDocument8 pagesProfitability Analysis of Tata Motors: AbhinavAman KhanNo ratings yet

- Current Assets To Proprieors FundsDocument8 pagesCurrent Assets To Proprieors FundsindramuniNo ratings yet

- Lbo Case StudyDocument6 pagesLbo Case StudyRishabh MishraNo ratings yet

- Ratios of Comp.Document25 pagesRatios of Comp.ashish5016No ratings yet

- Suggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsDocument16 pagesSuggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsMdAnjum1991No ratings yet

- Advanced Financial Accounting: Ratio Analysis and InterpretationDocument21 pagesAdvanced Financial Accounting: Ratio Analysis and InterpretationKowsik RajendranNo ratings yet

- Chapter 7 Prospective Analysis: Valuation Theory and ConceptsDocument7 pagesChapter 7 Prospective Analysis: Valuation Theory and ConceptsWalm KetyNo ratings yet

- A Comparitive Analysis of Working Capital ofDocument19 pagesA Comparitive Analysis of Working Capital ofManasvi MehtaNo ratings yet

- A Comparitive Analysis of Working Capital ofDocument19 pagesA Comparitive Analysis of Working Capital ofManasvi MehtaNo ratings yet

- Research Paper On Working Capital Management Made by Satyam KumarDocument3 pagesResearch Paper On Working Capital Management Made by Satyam Kumarsatyam skNo ratings yet

- Ratio Analysis (Group 5-Glc - Ib)Document53 pagesRatio Analysis (Group 5-Glc - Ib)Nikam PranitNo ratings yet

- Cu R R E N T - R A T I O: Fixed Assets RatioDocument11 pagesCu R R E N T - R A T I O: Fixed Assets RatioRoshan KumarNo ratings yet

- Tanjung Offshore: Turning Attractive Upgrade To BuyDocument4 pagesTanjung Offshore: Turning Attractive Upgrade To Buykhlis81No ratings yet

- NTPC Ratio Analysis - FinalDocument45 pagesNTPC Ratio Analysis - FinalniradharNo ratings yet

- Orissa Electricity Regulatory Commission Bidyut Niyamak Bhavan Unit - Viii, Bhubaneswar - 751 012 No - DIR (T) - 371/09/ Dated-.07.2011Document22 pagesOrissa Electricity Regulatory Commission Bidyut Niyamak Bhavan Unit - Viii, Bhubaneswar - 751 012 No - DIR (T) - 371/09/ Dated-.07.2011havejsnjNo ratings yet

- Assignment: 1: Financial Accounting and AnalysisDocument12 pagesAssignment: 1: Financial Accounting and AnalysisFogey RulzNo ratings yet

- GGP Final2010Document23 pagesGGP Final2010Frank ParkerNo ratings yet

- BF AssignmentDocument13 pagesBF AssignmentMomina waseemNo ratings yet

- Results & Discussion: Table - 1 Gross Profit Ratio Year Gross Profit Net Sales 100 RatioDocument9 pagesResults & Discussion: Table - 1 Gross Profit Ratio Year Gross Profit Net Sales 100 RatioeswariNo ratings yet

- NTPC Ratio Analysis FinalDocument45 pagesNTPC Ratio Analysis FinalDaman Deep SinghNo ratings yet

- Working Capital Management & Operating Cycle: Bajaj AutomobilesDocument22 pagesWorking Capital Management & Operating Cycle: Bajaj Automobilesdivanshugupta1988No ratings yet

- Working Capital ManagementDocument33 pagesWorking Capital ManagementPRATIK PALKHENo ratings yet

- Overall Budgetary Position 2009-10: Chart - 1Document43 pagesOverall Budgetary Position 2009-10: Chart - 1reddygantasri31No ratings yet

- Ratios OriginaDocument19 pagesRatios OriginaVivek RajNo ratings yet

- AnalysisDocument8 pagesAnalysisAnjali AnandNo ratings yet

- Mcdonal's Finanical RatiosDocument11 pagesMcdonal's Finanical RatiosFahad Khan TareenNo ratings yet

- Working Capital Ppt-3Document34 pagesWorking Capital Ppt-3bala muraliNo ratings yet

- Finance&Accounts T3 SolutionDocument4 pagesFinance&Accounts T3 Solutionkanika thakurNo ratings yet

- Project Analysis: Principles of Corporate FinanceDocument16 pagesProject Analysis: Principles of Corporate FinancechooisinNo ratings yet

- Ashok Leyland LTD Company AnalysisDocument13 pagesAshok Leyland LTD Company AnalysisRaghav100% (30)

- Building Inspection Service Revenues World Summary: Market Values & Financials by CountryFrom EverandBuilding Inspection Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Nabard (National Bank For Agriculture and Rural Development)Document21 pagesNabard (National Bank For Agriculture and Rural Development)ds_frnship4235No ratings yet

- Clinic Management System Project For Final Year: Sarfaraj AlamDocument6 pagesClinic Management System Project For Final Year: Sarfaraj AlamUDAY SOLUTIONSNo ratings yet

- Me 425 (Case Study) Raymar B. AquinoDocument3 pagesMe 425 (Case Study) Raymar B. AquinoJoan Joy BalgosNo ratings yet

- Municipality of San Narciso Vs Mendez Sr. DigestDocument2 pagesMunicipality of San Narciso Vs Mendez Sr. DigestMark MlsNo ratings yet

- Ice Breakers and Team Builders PacketDocument54 pagesIce Breakers and Team Builders Packetnissefar007100% (1)

- Blkpay 20230518Document4 pagesBlkpay 20230518Raman GoyalNo ratings yet

- FC CantocoralvocalDocument320 pagesFC Cantocoralvocalfelix miguelNo ratings yet

- Alternative DevelopmentDocument28 pagesAlternative DevelopmentOmar100% (1)

- KC CVDocument2 pagesKC CVVishal KeshriNo ratings yet

- Greatest Robbery of A Government Guinness World RecordsDocument1 pageGreatest Robbery of A Government Guinness World Recordsrex ceeNo ratings yet

- WFP ToR For Assistance To Syrian Refugees PDFDocument38 pagesWFP ToR For Assistance To Syrian Refugees PDFRuNo ratings yet

- A. Kroeber - The Superorganic PDFDocument64 pagesA. Kroeber - The Superorganic PDFmissmouNo ratings yet

- 17 Atci Overseas Corporation v. Ma Josefa Echin GR No 178551Document3 pages17 Atci Overseas Corporation v. Ma Josefa Echin GR No 178551Paula TorobaNo ratings yet

- WUS101-BUSINESS PLAN FORMAT - English MAC2020Document19 pagesWUS101-BUSINESS PLAN FORMAT - English MAC2020Ahmad Mujahid Che RahimiNo ratings yet

- Turn in For LTC MANDAL NCDocument2 pagesTurn in For LTC MANDAL NCMary Anne GamboaNo ratings yet

- Latest RFQ (Hospet Bellary Karntaka Dated - 29102010Document69 pagesLatest RFQ (Hospet Bellary Karntaka Dated - 29102010xanblakeNo ratings yet

- WhizKids Questions-UneditedDocument5 pagesWhizKids Questions-UneditedSVTKhsiaNo ratings yet

- Kelvion Walker Vs Amy WilburnDocument63 pagesKelvion Walker Vs Amy WilburnHorrible CrimeNo ratings yet

- 5yr Prog Case Digests PDFDocument346 pages5yr Prog Case Digests PDFMary Neil GalvisoNo ratings yet

- 02.13-02.17 - Sales Activity Report (Vivi)Document2 pages02.13-02.17 - Sales Activity Report (Vivi)ptsoutherntristar0No ratings yet

- Joycelyn PabloDocument6 pagesJoycelyn PabloAriza ValenciaNo ratings yet

- Assignment in Psychology of Law EnforcementDocument4 pagesAssignment in Psychology of Law EnforcementKRISTINE DEE L VELASCONo ratings yet

- Barriers To International TradeDocument12 pagesBarriers To International TraderajeshratnavelsamyNo ratings yet

- Comp Literacy - Chapter 6 Computer Ethic and SecurityDocument21 pagesComp Literacy - Chapter 6 Computer Ethic and SecuritySheikh VerstappenNo ratings yet

- Outsorcing ContractsDocument113 pagesOutsorcing ContractsfilipeammoreiraNo ratings yet

- Exam NotesDocument104 pagesExam NotesJezMillerNo ratings yet