Chapter-3: Adjusting The Accounts

Chapter-3: Adjusting The Accounts

You might also like

- Theories of Crime CausationDocument59 pagesTheories of Crime CausationRey John Dizon88% (32)

- Adjusting Account, WORK SHEET-FINALDocument43 pagesAdjusting Account, WORK SHEET-FINALChowdhury Mobarrat Haider Adnan100% (1)

- Chapter-3: Adjusting The AccountsDocument30 pagesChapter-3: Adjusting The Accountssadif sayeedNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionArif HossainNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionMohammed Merajul IslamNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionFarhan TariqNo ratings yet

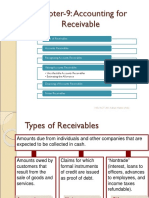

- Chapter-9: Accounting For Receivable: Types of ReceivablesDocument24 pagesChapter-9: Accounting For Receivable: Types of ReceivablesMohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For ReceivableDocument24 pagesChapter-9: Accounting For ReceivableArif HossainNo ratings yet

- Adjustments 20200216101400Document44 pagesAdjustments 20200216101400Chi Cheng100% (1)

- Chapter 3Document15 pagesChapter 3clara2300181No ratings yet

- Mba Eekm W2Document28 pagesMba Eekm W2Mon ThuNo ratings yet

- Accounting: John Wiley & Sons, IncDocument37 pagesAccounting: John Wiley & Sons, Incshafaat_90100% (1)

- Chapter 3-Adjusting The AccountsDocument26 pagesChapter 3-Adjusting The Accountsbebybey100% (1)

- Chapter-5: Accounting For Merchandising OperationsDocument36 pagesChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamNo ratings yet

- The Account Steps in The Recording Process The Trial BalanceDocument17 pagesThe Account Steps in The Recording Process The Trial BalanceMohammed Merajul IslamNo ratings yet

- Chapter 11Document32 pagesChapter 11Mohammed Merajul IslamNo ratings yet

- Chapter 4 End of The Period Adjustments Final ModuleDocument75 pagesChapter 4 End of The Period Adjustments Final ModuleRian Hanz AlbercaNo ratings yet

- Ch03 Adjusting The AccountsDocument85 pagesCh03 Adjusting The AccountsKarl MangligotNo ratings yet

- Chapter 3 PresentationDocument48 pagesChapter 3 Presentationhosie.oqbeNo ratings yet

- Adjusting The AccountsDocument36 pagesAdjusting The AccountsTasim Ishraque100% (1)

- Lecture04B-Adjusting AC CycleDocument61 pagesLecture04B-Adjusting AC Cycle錢永健No ratings yet

- Overview of Financial Statements: Basic Activities of BusinessesDocument30 pagesOverview of Financial Statements: Basic Activities of BusinesseslelahakuNo ratings yet

- Lecture Slides - Chapter 3 4Document82 pagesLecture Slides - Chapter 3 4Bùi Phan Ý Nhi100% (1)

- 03 - Adjusting EntriesDocument3 pages03 - Adjusting EntriesJamie ToriagaNo ratings yet

- Financial Accounting, 4eDocument42 pagesFinancial Accounting, 4eabdirahman mohamed100% (1)

- TM 4Document69 pagesTM 4yogi bedebusNo ratings yet

- Chapter 3: Preparing Financial StatementsDocument17 pagesChapter 3: Preparing Financial StatementsSittie Haynah Moominah BualanNo ratings yet

- Completing The Accounting CycleDocument46 pagesCompleting The Accounting CycleGaluh Boga Kuswara100% (1)

- Ccounting Principles,: Weygandt, Kieso, & KimmelDocument58 pagesCcounting Principles,: Weygandt, Kieso, & Kimmelpiash246100% (2)

- Summary Book Accounting PrinciplesDocument10 pagesSummary Book Accounting PrinciplesAvie ZabatNo ratings yet

- Accounting Process and Adjusting EntriesDocument7 pagesAccounting Process and Adjusting EntriesPeter ShangNo ratings yet

- Chapter 7 - AdjustmentsDocument70 pagesChapter 7 - AdjustmentsMinetteGabriel100% (1)

- Adjusting The AccountsDocument79 pagesAdjusting The AccountsaccpackmlbbNo ratings yet

- Adjusting EntriesDocument69 pagesAdjusting EntriesMadia Mujib100% (1)

- Measuring Profitability and Financial Position On The Financial Statements Chapter 4Document66 pagesMeasuring Profitability and Financial Position On The Financial Statements Chapter 4Rupesh Pol100% (1)

- Acct 2021 CH 2 Completion of The WorksheetDocument20 pagesAcct 2021 CH 2 Completion of The WorksheetAlemu BelayNo ratings yet

- Case 2 Adjusting Entries F 18Document6 pagesCase 2 Adjusting Entries F 18rcbcsk csk0% (1)

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document20 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB Cloyd100% (1)

- BUS 211 - Ch. 3 - Week 6Document37 pagesBUS 211 - Ch. 3 - Week 6memeaaNo ratings yet

- Adjusting Entry - LectureDocument9 pagesAdjusting Entry - LectureMaDine 19100% (2)

- CH 4 Classpack With SolutionsDocument24 pagesCH 4 Classpack With SolutionsjimenaNo ratings yet

- FA Week 3Document20 pagesFA Week 3Khánh AnNo ratings yet

- Lecture - 3 - Adjusting - Accounts - NUS ACC1002 2020 SpringDocument48 pagesLecture - 3 - Adjusting - Accounts - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- BUS 501 Chapter 3Document72 pagesBUS 501 Chapter 3Abu Tawbid Khan BadhanNo ratings yet

- Lecture 3 - Adjusting The AccountsDocument72 pagesLecture 3 - Adjusting The AccountsS. M. Fahmidunnabi 2035150660No ratings yet

- Lecture 3 - Adjusting The AccountsDocument62 pagesLecture 3 - Adjusting The AccountsNayeem Ahamed AdorNo ratings yet

- Adjusting Entries1Document20 pagesAdjusting Entries1Timothy CaragNo ratings yet

- Adjusting EntriesDocument3 pagesAdjusting EntriesMarini HernandezNo ratings yet

- Session 1 Introduction To Financial AccountingDocument26 pagesSession 1 Introduction To Financial AccountingTSNo ratings yet

- SAP User Guide Accrual DeferalDocument48 pagesSAP User Guide Accrual DeferalwiwNo ratings yet

- Adjusting Journal EntriesDocument34 pagesAdjusting Journal Entriesロザリーロザレス ロザリー・マキルNo ratings yet

- Chapter 4 Accrual Accounting Concepts - SakaiDocument37 pagesChapter 4 Accrual Accounting Concepts - SakaimarkassalNo ratings yet

- ACCY901 Accounting Foundations For Professionals: Topic 3 Accrual Accounting and Adjusting EntriesDocument35 pagesACCY901 Accounting Foundations For Professionals: Topic 3 Accrual Accounting and Adjusting Entriesvenkatachalam radhakrishnan100% (1)

- CH 03Document81 pagesCH 03Nguyen Khanh LinhNo ratings yet

- Adjusting The Accounts: Accounting Principles, 8 EditionDocument44 pagesAdjusting The Accounts: Accounting Principles, 8 EditionSheikh Azizul IslamNo ratings yet

- Adjusting Entries - ReviewerDocument2 pagesAdjusting Entries - ReviewerPeter Jonathan ObianoNo ratings yet

- WK 3 Accrual Accounting Concepts 2 Slides Per PageDocument23 pagesWK 3 Accrual Accounting Concepts 2 Slides Per PageThùy Linh Lê Thị100% (1)

- Adjusting The AccountsDocument6 pagesAdjusting The AccountsKena Montes Dela PeñaNo ratings yet

- Adjusting The Accounts: Accounting PrinciplesDocument50 pagesAdjusting The Accounts: Accounting PrinciplesAbdullah Al AminNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Chapter 11Document32 pagesChapter 11Mohammed Merajul IslamNo ratings yet

- Chapter - 8: Fraud, Internal Control & CashDocument14 pagesChapter - 8: Fraud, Internal Control & CashMohammed Merajul IslamNo ratings yet

- CH-10: Plant Assets, Natural Resources, and Intangible AssetsDocument44 pagesCH-10: Plant Assets, Natural Resources, and Intangible AssetsMohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For Receivable: Types of ReceivablesDocument24 pagesChapter-9: Accounting For Receivable: Types of ReceivablesMohammed Merajul IslamNo ratings yet

- Chapter-5: Accounting For Merchandising OperationsDocument36 pagesChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamNo ratings yet

- The Account Steps in The Recording Process The Trial BalanceDocument17 pagesThe Account Steps in The Recording Process The Trial BalanceMohammed Merajul IslamNo ratings yet

- CH-4: Completing The Accounting Cycle: Using A WorksheetDocument18 pagesCH-4: Completing The Accounting Cycle: Using A WorksheetMohammed Merajul IslamNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionMohammed Merajul IslamNo ratings yet

- Malankara Catholic Church Sui Iuris: Juridical Status and Power of GovernanceDocument26 pagesMalankara Catholic Church Sui Iuris: Juridical Status and Power of GovernanceDr. Thomas Kuzhinapurath100% (6)

- M607 L01 SolutionDocument7 pagesM607 L01 SolutionRonak PatelNo ratings yet

- TIK Single Touch Payroll Processing GuideDocument23 pagesTIK Single Touch Payroll Processing GuideMargaret MationgNo ratings yet

- Cash Receipt Template 3 WordDocument1 pageCash Receipt Template 3 WordSaqlain MalikNo ratings yet

- 03 Tiongson Cayetano Et Al Vs Court of Appeals Et AlDocument6 pages03 Tiongson Cayetano Et Al Vs Court of Appeals Et Alrandelrocks2No ratings yet

- Online Edd Without DissertationDocument4 pagesOnline Edd Without DissertationCustomPaperWritingServiceSingapore100% (1)

- Profiles of For-Profit Education Management Companies: Fifth Annual Report 2002-2003Document115 pagesProfiles of For-Profit Education Management Companies: Fifth Annual Report 2002-2003National Education Policy CenterNo ratings yet

- Lecture 03 - ECO 209 - W2013 PDFDocument69 pagesLecture 03 - ECO 209 - W2013 PDF123No ratings yet

- Blue Economy CourseDocument2 pagesBlue Economy CourseKenneth FrancisNo ratings yet

- Economic Survey 2017-18Document350 pagesEconomic Survey 2017-18Subhransu Sekhar SwainNo ratings yet

- Wycliffe BibleDocument752 pagesWycliffe Biblee.lixandruNo ratings yet

- Iqwq-Ft-Rspds-00-120103 - 1 Preservation During Shipping and ConstructionDocument31 pagesIqwq-Ft-Rspds-00-120103 - 1 Preservation During Shipping and Constructionjacksonbello34No ratings yet

- Milvik ProposalDocument29 pagesMilvik ProposalMin HajNo ratings yet

- Ers. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewDocument10 pagesErs. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewVolcaneum100% (2)

- emPower-API-Specification-v0 90 PDFDocument26 pagesemPower-API-Specification-v0 90 PDFPape Mignane FayeNo ratings yet

- Coraline QuotesDocument2 pagesCoraline Quotes145099No ratings yet

- 中文打字机一个世纪的汉字突围史 美墨磊宁Thomas S Mullaney Z-LibraryDocument490 pages中文打字机一个世纪的汉字突围史 美墨磊宁Thomas S Mullaney Z-Libraryxxx caoNo ratings yet

- Froebel Adventure Play History, Froebel and Lady Allen of HurtwoodDocument3 pagesFroebel Adventure Play History, Froebel and Lady Allen of HurtwoodLifeinthemix_FroebelNo ratings yet

- The FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationDocument27 pagesThe FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationAli SaeedNo ratings yet

- Expert Days 2018: SUSE Enterprise StorageDocument15 pagesExpert Days 2018: SUSE Enterprise StorageArturoNo ratings yet

- CP T Chotpradit 12723584Document287 pagesCP T Chotpradit 12723584Maxim ZagorskyNo ratings yet

- Brown 2003Document12 pagesBrown 2003sziágyi zsófiaNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- Histtory and Importance of HadithDocument31 pagesHisttory and Importance of HadithAbdullah AhsanNo ratings yet

- Digest Partnership CaseDocument12 pagesDigest Partnership Casejaynard9150% (2)

- Other Hands - Issue #15-16, Supplement PDFDocument8 pagesOther Hands - Issue #15-16, Supplement PDFAlHazredNo ratings yet

- Master Builder: PlusDocument31 pagesMaster Builder: PluswinataNo ratings yet

- ProjectDocument3 pagesProjectKimzee kingNo ratings yet

- ED Hiring GuideDocument20 pagesED Hiring Guidechokx008No ratings yet

Download as ppt, pdf, or txt

You might also like

- Theories of Crime CausationDocument59 pagesTheories of Crime CausationRey John Dizon88% (32)

- Adjusting Account, WORK SHEET-FINALDocument43 pagesAdjusting Account, WORK SHEET-FINALChowdhury Mobarrat Haider Adnan100% (1)

- Chapter-3: Adjusting The AccountsDocument30 pagesChapter-3: Adjusting The Accountssadif sayeedNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionArif HossainNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionMohammed Merajul IslamNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionFarhan TariqNo ratings yet

- Chapter-9: Accounting For Receivable: Types of ReceivablesDocument24 pagesChapter-9: Accounting For Receivable: Types of ReceivablesMohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For ReceivableDocument24 pagesChapter-9: Accounting For ReceivableArif HossainNo ratings yet

- Adjustments 20200216101400Document44 pagesAdjustments 20200216101400Chi Cheng100% (1)

- Chapter 3Document15 pagesChapter 3clara2300181No ratings yet

- Mba Eekm W2Document28 pagesMba Eekm W2Mon ThuNo ratings yet

- Accounting: John Wiley & Sons, IncDocument37 pagesAccounting: John Wiley & Sons, Incshafaat_90100% (1)

- Chapter 3-Adjusting The AccountsDocument26 pagesChapter 3-Adjusting The Accountsbebybey100% (1)

- Chapter-5: Accounting For Merchandising OperationsDocument36 pagesChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamNo ratings yet

- The Account Steps in The Recording Process The Trial BalanceDocument17 pagesThe Account Steps in The Recording Process The Trial BalanceMohammed Merajul IslamNo ratings yet

- Chapter 11Document32 pagesChapter 11Mohammed Merajul IslamNo ratings yet

- Chapter 4 End of The Period Adjustments Final ModuleDocument75 pagesChapter 4 End of The Period Adjustments Final ModuleRian Hanz AlbercaNo ratings yet

- Ch03 Adjusting The AccountsDocument85 pagesCh03 Adjusting The AccountsKarl MangligotNo ratings yet

- Chapter 3 PresentationDocument48 pagesChapter 3 Presentationhosie.oqbeNo ratings yet

- Adjusting The AccountsDocument36 pagesAdjusting The AccountsTasim Ishraque100% (1)

- Lecture04B-Adjusting AC CycleDocument61 pagesLecture04B-Adjusting AC Cycle錢永健No ratings yet

- Overview of Financial Statements: Basic Activities of BusinessesDocument30 pagesOverview of Financial Statements: Basic Activities of BusinesseslelahakuNo ratings yet

- Lecture Slides - Chapter 3 4Document82 pagesLecture Slides - Chapter 3 4Bùi Phan Ý Nhi100% (1)

- 03 - Adjusting EntriesDocument3 pages03 - Adjusting EntriesJamie ToriagaNo ratings yet

- Financial Accounting, 4eDocument42 pagesFinancial Accounting, 4eabdirahman mohamed100% (1)

- TM 4Document69 pagesTM 4yogi bedebusNo ratings yet

- Chapter 3: Preparing Financial StatementsDocument17 pagesChapter 3: Preparing Financial StatementsSittie Haynah Moominah BualanNo ratings yet

- Completing The Accounting CycleDocument46 pagesCompleting The Accounting CycleGaluh Boga Kuswara100% (1)

- Ccounting Principles,: Weygandt, Kieso, & KimmelDocument58 pagesCcounting Principles,: Weygandt, Kieso, & Kimmelpiash246100% (2)

- Summary Book Accounting PrinciplesDocument10 pagesSummary Book Accounting PrinciplesAvie ZabatNo ratings yet

- Accounting Process and Adjusting EntriesDocument7 pagesAccounting Process and Adjusting EntriesPeter ShangNo ratings yet

- Chapter 7 - AdjustmentsDocument70 pagesChapter 7 - AdjustmentsMinetteGabriel100% (1)

- Adjusting The AccountsDocument79 pagesAdjusting The AccountsaccpackmlbbNo ratings yet

- Adjusting EntriesDocument69 pagesAdjusting EntriesMadia Mujib100% (1)

- Measuring Profitability and Financial Position On The Financial Statements Chapter 4Document66 pagesMeasuring Profitability and Financial Position On The Financial Statements Chapter 4Rupesh Pol100% (1)

- Acct 2021 CH 2 Completion of The WorksheetDocument20 pagesAcct 2021 CH 2 Completion of The WorksheetAlemu BelayNo ratings yet

- Case 2 Adjusting Entries F 18Document6 pagesCase 2 Adjusting Entries F 18rcbcsk csk0% (1)

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document20 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB Cloyd100% (1)

- BUS 211 - Ch. 3 - Week 6Document37 pagesBUS 211 - Ch. 3 - Week 6memeaaNo ratings yet

- Adjusting Entry - LectureDocument9 pagesAdjusting Entry - LectureMaDine 19100% (2)

- CH 4 Classpack With SolutionsDocument24 pagesCH 4 Classpack With SolutionsjimenaNo ratings yet

- FA Week 3Document20 pagesFA Week 3Khánh AnNo ratings yet

- Lecture - 3 - Adjusting - Accounts - NUS ACC1002 2020 SpringDocument48 pagesLecture - 3 - Adjusting - Accounts - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- BUS 501 Chapter 3Document72 pagesBUS 501 Chapter 3Abu Tawbid Khan BadhanNo ratings yet

- Lecture 3 - Adjusting The AccountsDocument72 pagesLecture 3 - Adjusting The AccountsS. M. Fahmidunnabi 2035150660No ratings yet

- Lecture 3 - Adjusting The AccountsDocument62 pagesLecture 3 - Adjusting The AccountsNayeem Ahamed AdorNo ratings yet

- Adjusting Entries1Document20 pagesAdjusting Entries1Timothy CaragNo ratings yet

- Adjusting EntriesDocument3 pagesAdjusting EntriesMarini HernandezNo ratings yet

- Session 1 Introduction To Financial AccountingDocument26 pagesSession 1 Introduction To Financial AccountingTSNo ratings yet

- SAP User Guide Accrual DeferalDocument48 pagesSAP User Guide Accrual DeferalwiwNo ratings yet

- Adjusting Journal EntriesDocument34 pagesAdjusting Journal Entriesロザリーロザレス ロザリー・マキルNo ratings yet

- Chapter 4 Accrual Accounting Concepts - SakaiDocument37 pagesChapter 4 Accrual Accounting Concepts - SakaimarkassalNo ratings yet

- ACCY901 Accounting Foundations For Professionals: Topic 3 Accrual Accounting and Adjusting EntriesDocument35 pagesACCY901 Accounting Foundations For Professionals: Topic 3 Accrual Accounting and Adjusting Entriesvenkatachalam radhakrishnan100% (1)

- CH 03Document81 pagesCH 03Nguyen Khanh LinhNo ratings yet

- Adjusting The Accounts: Accounting Principles, 8 EditionDocument44 pagesAdjusting The Accounts: Accounting Principles, 8 EditionSheikh Azizul IslamNo ratings yet

- Adjusting Entries - ReviewerDocument2 pagesAdjusting Entries - ReviewerPeter Jonathan ObianoNo ratings yet

- WK 3 Accrual Accounting Concepts 2 Slides Per PageDocument23 pagesWK 3 Accrual Accounting Concepts 2 Slides Per PageThùy Linh Lê Thị100% (1)

- Adjusting The AccountsDocument6 pagesAdjusting The AccountsKena Montes Dela PeñaNo ratings yet

- Adjusting The Accounts: Accounting PrinciplesDocument50 pagesAdjusting The Accounts: Accounting PrinciplesAbdullah Al AminNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Chapter 11Document32 pagesChapter 11Mohammed Merajul IslamNo ratings yet

- Chapter - 8: Fraud, Internal Control & CashDocument14 pagesChapter - 8: Fraud, Internal Control & CashMohammed Merajul IslamNo ratings yet

- CH-10: Plant Assets, Natural Resources, and Intangible AssetsDocument44 pagesCH-10: Plant Assets, Natural Resources, and Intangible AssetsMohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For Receivable: Types of ReceivablesDocument24 pagesChapter-9: Accounting For Receivable: Types of ReceivablesMohammed Merajul IslamNo ratings yet

- Chapter-5: Accounting For Merchandising OperationsDocument36 pagesChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamNo ratings yet

- The Account Steps in The Recording Process The Trial BalanceDocument17 pagesThe Account Steps in The Recording Process The Trial BalanceMohammed Merajul IslamNo ratings yet

- CH-4: Completing The Accounting Cycle: Using A WorksheetDocument18 pagesCH-4: Completing The Accounting Cycle: Using A WorksheetMohammed Merajul IslamNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionMohammed Merajul IslamNo ratings yet

- Malankara Catholic Church Sui Iuris: Juridical Status and Power of GovernanceDocument26 pagesMalankara Catholic Church Sui Iuris: Juridical Status and Power of GovernanceDr. Thomas Kuzhinapurath100% (6)

- M607 L01 SolutionDocument7 pagesM607 L01 SolutionRonak PatelNo ratings yet

- TIK Single Touch Payroll Processing GuideDocument23 pagesTIK Single Touch Payroll Processing GuideMargaret MationgNo ratings yet

- Cash Receipt Template 3 WordDocument1 pageCash Receipt Template 3 WordSaqlain MalikNo ratings yet

- 03 Tiongson Cayetano Et Al Vs Court of Appeals Et AlDocument6 pages03 Tiongson Cayetano Et Al Vs Court of Appeals Et Alrandelrocks2No ratings yet

- Online Edd Without DissertationDocument4 pagesOnline Edd Without DissertationCustomPaperWritingServiceSingapore100% (1)

- Profiles of For-Profit Education Management Companies: Fifth Annual Report 2002-2003Document115 pagesProfiles of For-Profit Education Management Companies: Fifth Annual Report 2002-2003National Education Policy CenterNo ratings yet

- Lecture 03 - ECO 209 - W2013 PDFDocument69 pagesLecture 03 - ECO 209 - W2013 PDF123No ratings yet

- Blue Economy CourseDocument2 pagesBlue Economy CourseKenneth FrancisNo ratings yet

- Economic Survey 2017-18Document350 pagesEconomic Survey 2017-18Subhransu Sekhar SwainNo ratings yet

- Wycliffe BibleDocument752 pagesWycliffe Biblee.lixandruNo ratings yet

- Iqwq-Ft-Rspds-00-120103 - 1 Preservation During Shipping and ConstructionDocument31 pagesIqwq-Ft-Rspds-00-120103 - 1 Preservation During Shipping and Constructionjacksonbello34No ratings yet

- Milvik ProposalDocument29 pagesMilvik ProposalMin HajNo ratings yet

- Ers. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewDocument10 pagesErs. Co M: JANA Master Fund, Ltd. Performance Update - December 2010 Fourth Quarter and Year in ReviewVolcaneum100% (2)

- emPower-API-Specification-v0 90 PDFDocument26 pagesemPower-API-Specification-v0 90 PDFPape Mignane FayeNo ratings yet

- Coraline QuotesDocument2 pagesCoraline Quotes145099No ratings yet

- 中文打字机一个世纪的汉字突围史 美墨磊宁Thomas S Mullaney Z-LibraryDocument490 pages中文打字机一个世纪的汉字突围史 美墨磊宁Thomas S Mullaney Z-Libraryxxx caoNo ratings yet

- Froebel Adventure Play History, Froebel and Lady Allen of HurtwoodDocument3 pagesFroebel Adventure Play History, Froebel and Lady Allen of HurtwoodLifeinthemix_FroebelNo ratings yet

- The FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationDocument27 pagesThe FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationAli SaeedNo ratings yet

- Expert Days 2018: SUSE Enterprise StorageDocument15 pagesExpert Days 2018: SUSE Enterprise StorageArturoNo ratings yet

- CP T Chotpradit 12723584Document287 pagesCP T Chotpradit 12723584Maxim ZagorskyNo ratings yet

- Brown 2003Document12 pagesBrown 2003sziágyi zsófiaNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- Histtory and Importance of HadithDocument31 pagesHisttory and Importance of HadithAbdullah AhsanNo ratings yet

- Digest Partnership CaseDocument12 pagesDigest Partnership Casejaynard9150% (2)

- Other Hands - Issue #15-16, Supplement PDFDocument8 pagesOther Hands - Issue #15-16, Supplement PDFAlHazredNo ratings yet

- Master Builder: PlusDocument31 pagesMaster Builder: PluswinataNo ratings yet

- ProjectDocument3 pagesProjectKimzee kingNo ratings yet

- ED Hiring GuideDocument20 pagesED Hiring Guidechokx008No ratings yet