Download as ppt, pdf, or txt

You might also like

- A11vo Rexroth Repair Manual DocumentDocument5 pagesA11vo Rexroth Repair Manual DocumentFill Jose80% (5)

- Coca-Cola: Residual Income Valuation Exercise & Coca-Cola: Residual Income Valuation Exercise (TN)Document7 pagesCoca-Cola: Residual Income Valuation Exercise & Coca-Cola: Residual Income Valuation Exercise (TN)sarthak mendiratta100% (1)

- Case 5Document12 pagesCase 5JIAXUAN WANGNo ratings yet

- Case 5 Midland Energy Case ProjectDocument7 pagesCase 5 Midland Energy Case ProjectCourse HeroNo ratings yet

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankNo ratings yet

- MFIN Case Write-UpDocument7 pagesMFIN Case Write-UpUMMUSNUR OZCANNo ratings yet

- Obscurity: Undesirability: P/E: Screening CriteriaDocument21 pagesObscurity: Undesirability: P/E: Screening Criteria/jncjdncjdnNo ratings yet

- 2021 OctDocument64 pages2021 OctAhm Ferdous100% (1)

- Clarkson Lumber CaseDocument27 pagesClarkson Lumber CaseGovardan SureshNo ratings yet

- Section A - Group DDocument6 pagesSection A - Group DAbhishek Verma100% (1)

- Clarkson Lumbar CompanyDocument41 pagesClarkson Lumbar CompanyTheOxyCleanGuyNo ratings yet

- Michael McClintock Case1Document2 pagesMichael McClintock Case1Mike MCNo ratings yet

- Student SpreadsheetDocument14 pagesStudent SpreadsheetPriyanka Agarwal0% (1)

- Clarkson TemplateDocument7 pagesClarkson TemplateJeffery KaoNo ratings yet

- Sun Microsystems Case JasdeepDocument6 pagesSun Microsystems Case JasdeepJasdeep SinghNo ratings yet

- Ceres SpreadsheetDocument1 pageCeres SpreadsheetShannan RichardsNo ratings yet

- Introduction To Database Systems Relational Model and AlgebraDocument76 pagesIntroduction To Database Systems Relational Model and Algebraxc33No ratings yet

- Cases RJR Nabisco 90 & 91 - Assignment QuestionsDocument1 pageCases RJR Nabisco 90 & 91 - Assignment QuestionsBrunoPereiraNo ratings yet

- In-Class Project 2: Due 4/13/2019 Your Name: Valuation of The Leveraged Buyout (LBO) of RJR Nabisco 1. Cash Flow EstimatesDocument5 pagesIn-Class Project 2: Due 4/13/2019 Your Name: Valuation of The Leveraged Buyout (LBO) of RJR Nabisco 1. Cash Flow EstimatesDinhkhanh NguyenNo ratings yet

- VIB Case Study On RJR NabiscoDocument1 pageVIB Case Study On RJR NabiscoSatyajeet SenapatiNo ratings yet

- RJRDocument4 pagesRJRliyulongNo ratings yet

- Case Analysis - Compania de Telefonos de ChileDocument4 pagesCase Analysis - Compania de Telefonos de ChileSubrata BasakNo ratings yet

- RJR Nabisco ValuationDocument33 pagesRJR Nabisco ValuationKrishna Chaitanya KothapalliNo ratings yet

- Clarkson Lumber Analysis - TylerDocument9 pagesClarkson Lumber Analysis - TylerTyler TreadwayNo ratings yet

- Kraft Foods Case SummaryDocument2 pagesKraft Foods Case Summaryrkodo1126No ratings yet

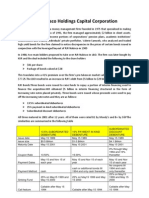

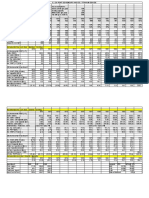

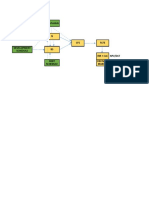

- RJR Nabisco Holdings Capital CorporationDocument3 pagesRJR Nabisco Holdings Capital CorporationManogana RasaNo ratings yet

- Seagate NewDocument22 pagesSeagate NewKaran VasheeNo ratings yet

- Nabisco - Sol v0.1 PDFDocument13 pagesNabisco - Sol v0.1 PDFMohit Khandelwal100% (1)

- Netscape ProformaDocument6 pagesNetscape ProformabobscribdNo ratings yet

- RJR Nabisco ValuationDocument38 pagesRJR Nabisco ValuationJCNo ratings yet

- Clarkson Lumber Co Calculations For StudentsDocument27 pagesClarkson Lumber Co Calculations For StudentsQuetzi AguirreNo ratings yet

- Winfield Refuse. - Case QuestionsDocument1 pageWinfield Refuse. - Case QuestionsthoroftedalNo ratings yet

- In Re RJR Nabisco Inc.Document3 pagesIn Re RJR Nabisco Inc.viva_33No ratings yet

- Daktronics E Dividend Policy in 2010Document26 pagesDaktronics E Dividend Policy in 2010IBRAHIM KHANNo ratings yet

- Case Sheet - Ameritrade: GROUP 16: Answer 9Document31 pagesCase Sheet - Ameritrade: GROUP 16: Answer 9tripti maheshwariNo ratings yet

- Final AssignmentDocument15 pagesFinal AssignmentUttam DwaNo ratings yet

- Practice Casestudy SolutionsDocument6 pagesPractice Casestudy SolutionsnurNo ratings yet

- Sneaker Excel Sheet For Risk AnalysisDocument11 pagesSneaker Excel Sheet For Risk AnalysisSuperGuyNo ratings yet

- Dell CaseDocument3 pagesDell CaseJuan Diego Vasquez BeraunNo ratings yet

- HP Case Competition PresentationDocument17 pagesHP Case Competition PresentationNatalia HernandezNo ratings yet

- Tire City AssignmentDocument6 pagesTire City AssignmentXRiloXNo ratings yet

- Case Assignment - RJR NabiscoDocument1 pageCase Assignment - RJR NabiscoMuhammad Rehan NasirNo ratings yet

- Sampa Video Case ExhibitsDocument1 pageSampa Video Case ExhibitsOnal RautNo ratings yet

- Koito Case Questions 2,3,4Document2 pagesKoito Case Questions 2,3,4Simo RajyNo ratings yet

- M&a Assignment - Syndicate C FINALDocument8 pagesM&a Assignment - Syndicate C FINALNikhil ReddyNo ratings yet

- Case 8 Finance CPK - Syndicate 2 YP56BDocument13 pagesCase 8 Finance CPK - Syndicate 2 YP56BBerni RahmanNo ratings yet

- Butler Lumber CoDocument2 pagesButler Lumber Cokumarsharma123No ratings yet

- Nike Inc Cost of Capital (MBA)Document8 pagesNike Inc Cost of Capital (MBA)Majid ALee100% (1)

- Titanium Dioxide and Super Project Prof. Joshy JacobDocument3 pagesTitanium Dioxide and Super Project Prof. Joshy JacobSIDDHARTH SINGHNo ratings yet

- Mercury Athletic FootwearDocument4 pagesMercury Athletic FootwearAbhishek KumarNo ratings yet

- ATC Valuation - Solution Along With All The ExhibitsDocument20 pagesATC Valuation - Solution Along With All The ExhibitsAbiNo ratings yet

- Winfield Refuse Management Inc. Raising Debt vs. EquityDocument13 pagesWinfield Refuse Management Inc. Raising Debt vs. EquitynmenalopezNo ratings yet

- Monmouth IncDocument7 pagesMonmouth Incdineshjn20000% (2)

- Ocean Carriers Case Group 5Document27 pagesOcean Carriers Case Group 5HarveyNo ratings yet

- Bond Problem - Fixed Income ValuationDocument1 pageBond Problem - Fixed Income ValuationAbhishek Garg0% (2)

- ACC 309 Final Project Student WorkbookDocument46 pagesACC 309 Final Project Student Workbooknick george100% (1)

- Hello GunaDocument10 pagesHello GunaMajed Abou AlkhirNo ratings yet

- 7-Basic - Model - FSA - 2 (Tax) - Rev-5Document14 pages7-Basic - Model - FSA - 2 (Tax) - Rev-5kIkiNo ratings yet

- Financial MStatements Ceres MGardening MCompanyDocument11 pagesFinancial MStatements Ceres MGardening MCompanyRodnix MablungNo ratings yet

- Spyder Student ExcelDocument21 pagesSpyder Student ExcelNatasha PerryNo ratings yet

- AIRASIADocument4 pagesAIRASIAFranck Jeremy MoogNo ratings yet

- Ceres Gardening Company Submission TemplateDocument9 pagesCeres Gardening Company Submission TemplateAkshay RoyNo ratings yet

- 4019 XLS EngDocument4 pages4019 XLS EngAnonymous 1997No ratings yet

- 19 PDFDocument33 pages19 PDF9183290782No ratings yet

- Maven Tutorial PDFDocument122 pagesMaven Tutorial PDFAdriana RodriguezNo ratings yet

- 11 Obd IiDocument30 pages11 Obd IiSimon SimonNo ratings yet

- 2020-11-03 Minutes - Etobicoke York Community CouncilDocument18 pages2020-11-03 Minutes - Etobicoke York Community CouncilAlan FrischNo ratings yet

- CE8591 FE Notes Eswa - by WWW - Easyengineering.net 1Document103 pagesCE8591 FE Notes Eswa - by WWW - Easyengineering.net 1seraphintetang38No ratings yet

- Melt Pressure Transmitters Ke Series Performance Level C': Output 4... 20maDocument6 pagesMelt Pressure Transmitters Ke Series Performance Level C': Output 4... 20maedgar covarrubiasNo ratings yet

- Chemical ContactDocument118 pagesChemical ContactkasvikrajNo ratings yet

- Budget Circular No. 2024-1 Dated April 4 2024 Clothing AllowanceDocument8 pagesBudget Circular No. 2024-1 Dated April 4 2024 Clothing AllowanceAgnes FernandezNo ratings yet

- NF EN 246 - D18 - 204 2003-General Specifications For Flow Rate RegulatorsDocument19 pagesNF EN 246 - D18 - 204 2003-General Specifications For Flow Rate RegulatorslouisNo ratings yet

- Wiper BladesDocument11 pagesWiper BladesErick MuraguriNo ratings yet

- Toyota Training Automatic Transmission BasicsDocument20 pagesToyota Training Automatic Transmission Basicsnorman100% (41)

- CH 18: Dividend PolicyDocument55 pagesCH 18: Dividend PolicySaba MalikNo ratings yet

- ORACLE Security Solution: Ray ShihDocument71 pagesORACLE Security Solution: Ray ShihabidouNo ratings yet

- Intermediate III - Wise UpDocument13 pagesIntermediate III - Wise UpWashington JuniorNo ratings yet

- The 1 1 M Hypersonic Wind Tunnel KochelTullahoma 1Document20 pagesThe 1 1 M Hypersonic Wind Tunnel KochelTullahoma 1Ivan BasicNo ratings yet

- Baghouse Filter Modular Pulse Jet Type: Operation and ApplicationDocument5 pagesBaghouse Filter Modular Pulse Jet Type: Operation and ApplicationBudy AndikaNo ratings yet

- Sensore Serie Elité CMF - INGLDocument100 pagesSensore Serie Elité CMF - INGLMahmoud Abd-Elhamid Abu EyadNo ratings yet

- Program Appropriation and Obligation by Object: Budget Year 2012Document2 pagesProgram Appropriation and Obligation by Object: Budget Year 2012Reslyn YanocNo ratings yet

- Swift Training Managing-Alliance-Access-And-Entry 57523 v3Document2 pagesSwift Training Managing-Alliance-Access-And-Entry 57523 v3rajesh.talabattulaNo ratings yet

- First Order Ordinary Differential Equations (1 Order - ODE)Document3 pagesFirst Order Ordinary Differential Equations (1 Order - ODE)Naga MerahNo ratings yet

- Deed of Donation TemplateDocument2 pagesDeed of Donation TemplateCe JeyNo ratings yet

- Industry 4.0 and Marketing - Towards An Integrated Future Research AgendaDocument20 pagesIndustry 4.0 and Marketing - Towards An Integrated Future Research AgendaElma AvdagicNo ratings yet

- Factors Influencing Artificial Intelligence Adoption in The Accounting Profession - The Case of Public Sector in KuwaitDocument25 pagesFactors Influencing Artificial Intelligence Adoption in The Accounting Profession - The Case of Public Sector in Kuwaittoky daikiNo ratings yet

- James Kacouris Sues Facebook, Zuckerberg and Wehner in Class ActionDocument17 pagesJames Kacouris Sues Facebook, Zuckerberg and Wehner in Class ActionJack PurcherNo ratings yet

- Centroid - Centre of Gravity - Mechanical Engineering (MCQ) Questions and AnswersDocument5 pagesCentroid - Centre of Gravity - Mechanical Engineering (MCQ) Questions and AnswersNitik Kumar0% (1)

- Fcgen h2pm Ultracap 5 0 Data SheetDocument2 pagesFcgen h2pm Ultracap 5 0 Data SheetULLAS VAGHRINo ratings yet

- Business Plan TemplateDocument18 pagesBusiness Plan TemplateFranca RectoNo ratings yet