Download as pptx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- BS4Document4 pagesBS4Von Andrei MedinaNo ratings yet

- Aspects of Contracts Assignment Brief 2-2 YasminDocument7 pagesAspects of Contracts Assignment Brief 2-2 YasminMuhammad akhtarNo ratings yet

- Presentation 4 Business EnvironmentDocument38 pagesPresentation 4 Business EnvironmentMuhammad akhtarNo ratings yet

- Introduction To Managing Financial Resources and Decisions Lecture 1Document17 pagesIntroduction To Managing Financial Resources and Decisions Lecture 1Muhammad akhtarNo ratings yet

- Medium Term Financing: Prepared By: Muhammad AkhtarDocument31 pagesMedium Term Financing: Prepared By: Muhammad AkhtarMuhammad akhtarNo ratings yet

- General Business Pathway: 30 CreditDocument2 pagesGeneral Business Pathway: 30 CreditMuhammad akhtarNo ratings yet

- Lecture01 Company LawDocument35 pagesLecture01 Company LawMuhammad akhtarNo ratings yet

- Analysis of Financial Statements.: Prepared By: Muhammad AkhtarDocument23 pagesAnalysis of Financial Statements.: Prepared By: Muhammad AkhtarMuhammad akhtarNo ratings yet

- Baumol Miller ModelDocument34 pagesBaumol Miller ModelShuvro RahmanNo ratings yet

- Notice: Premerger Notification Waiting Periods Early TerminationsDocument5 pagesNotice: Premerger Notification Waiting Periods Early TerminationsJustia.comNo ratings yet

- Arbitrage Opportunity Between Indian Stocks and Their ADR'sDocument12 pagesArbitrage Opportunity Between Indian Stocks and Their ADR'scrajkumarsinghNo ratings yet

- FAR 1st PreboardDocument10 pagesFAR 1st PreboardLui100% (2)

- FAP Midterm (A)Document3 pagesFAP Midterm (A)musharraf anjumNo ratings yet

- RTP CA Final New Course Paper 2 Strategic Financial ManagemeDocument26 pagesRTP CA Final New Course Paper 2 Strategic Financial ManagemeTusharNo ratings yet

- Ch06 Takeover TacticsDocument82 pagesCh06 Takeover TacticsLinh KhánhNo ratings yet

- Intermediate Accounting IIDocument10 pagesIntermediate Accounting IILexNo ratings yet

- Piercing of Corporate VeilDocument4 pagesPiercing of Corporate VeilRhic Ryanlhee Vergara FabsNo ratings yet

- AcFn 611-ch VII Revised PDFDocument63 pagesAcFn 611-ch VII Revised PDFtemedebereNo ratings yet

- Kushner, JaredDocument54 pagesKushner, JaredM Mali100% (2)

- Review Part1IA2.Docx 1Document73 pagesReview Part1IA2.Docx 1HAZELMAE JEMINEZNo ratings yet

- Books Archives - ValueVirtuoso ... Contrarian Value InvestingDocument14 pagesBooks Archives - ValueVirtuoso ... Contrarian Value InvestingBanderlei SilvaNo ratings yet

- Amortization and Impair of Intangible AssetsDocument3 pagesAmortization and Impair of Intangible AssetsCJ alandyNo ratings yet

- Chapter 3 Fa5Document22 pagesChapter 3 Fa5Noriani Binti SambriNo ratings yet

- Short Term Financial PlanningDocument16 pagesShort Term Financial Planningrana sarfaraxNo ratings yet

- Financial Report: Prepared By: Jackielou R. GallardeDocument5 pagesFinancial Report: Prepared By: Jackielou R. GallardeAndrew Arciosa CalsoNo ratings yet

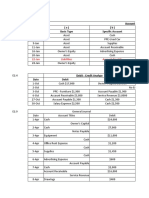

- Account Debited (A) (B) Date Basic Type Specific AccountDocument12 pagesAccount Debited (A) (B) Date Basic Type Specific AccountVALENCIA TORENTHANo ratings yet

- Accounting For Non-ABM - Accounting Equation and The Double-Entry System - Module 2 AsynchronousDocument29 pagesAccounting For Non-ABM - Accounting Equation and The Double-Entry System - Module 2 AsynchronousPamela PerezNo ratings yet

- CC2 - The Financial Detective, 2005Document4 pagesCC2 - The Financial Detective, 2005Aldren Delina RiveraNo ratings yet

- Company ProjectDocument14 pagesCompany ProjectMayank Sahu0% (1)

- Answers Homework # 21 - Financial Reporting III-CashflowDocument6 pagesAnswers Homework # 21 - Financial Reporting III-CashflowRaman ANo ratings yet

- 富達環球科技基金 說明Document7 pages富達環球科技基金 說明Terence LamNo ratings yet

- The Financial Environment: © 2008 John Wiley and SonsDocument39 pagesThe Financial Environment: © 2008 John Wiley and SonscelNo ratings yet

- MFRS101 Presentation of Financial StatemntsDocument8 pagesMFRS101 Presentation of Financial StatemntsIsmahani HaniNo ratings yet

- Deduction PDFDocument207 pagesDeduction PDFdeepluthra6No ratings yet

- CH 7 Cost of CapitalDocument58 pagesCH 7 Cost of CapitalNikita AggarwalNo ratings yet

- Title Xiv DissolutionDocument5 pagesTitle Xiv DissolutionMeAnn Tumbaga0% (1)

- BIR Ruling DA-141-99Document3 pagesBIR Ruling DA-141-99racheltanuy6557100% (1)