Flow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking at

Flow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking at

You might also like

- Admission Letter ATUDocument1 pageAdmission Letter ATUIsaac Clarity MensahNo ratings yet

- Name: Ahmed Idris Abaker K Customer No: 2812095 Account Type: Saving Account Currency: SDG Issue Date: 19-03-2023Document17 pagesName: Ahmed Idris Abaker K Customer No: 2812095 Account Type: Saving Account Currency: SDG Issue Date: 19-03-2023Ahmed EdrisNo ratings yet

- NC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerDocument34 pagesNC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerSheila Mae Lira100% (2)

- Financial Accounting Chapter 3Document5 pagesFinancial Accounting Chapter 3NiraniyaNo ratings yet

- Chapter 3: Managerial Accounting - Job Order CostingDocument2 pagesChapter 3: Managerial Accounting - Job Order Costingagm25No ratings yet

- Introducing Financial Statements and Transaction AnalysisDocument64 pagesIntroducing Financial Statements and Transaction AnalysisHazim AbualolaNo ratings yet

- Accounting & FinanceDocument17 pagesAccounting & FinanceInbasaat PirzadaNo ratings yet

- ACM 31 Lec2Document18 pagesACM 31 Lec2Vishal AmbadNo ratings yet

- CH 5Document58 pagesCH 5marwan2004acctNo ratings yet

- Introduction To AccountingDocument15 pagesIntroduction To Accountingluna dupontNo ratings yet

- Accounting and Financial Management in LogisticsDocument23 pagesAccounting and Financial Management in LogisticsWah KhaingNo ratings yet

- Account TitlesDocument4 pagesAccount TitlesChristian VelascoNo ratings yet

- An Introduction To Business and AccountingDocument43 pagesAn Introduction To Business and AccountingKeo VannuthNo ratings yet

- FCFChap002 - Financial StatementsDocument23 pagesFCFChap002 - Financial StatementsSozia TanNo ratings yet

- Financial Accounting - An Introduction: DR Vandana Bhama FORE School of Management, DelhiDocument30 pagesFinancial Accounting - An Introduction: DR Vandana Bhama FORE School of Management, DelhiShavik BaralNo ratings yet

- Balance Sheet: by Dr. ArchanaDocument19 pagesBalance Sheet: by Dr. ArchanaHan JeeNo ratings yet

- 2.2 Financial StatementsDocument38 pages2.2 Financial StatementsNefarioDMNo ratings yet

- Managing The Venture's Financial ResourcesDocument28 pagesManaging The Venture's Financial ResourcesAnto DNo ratings yet

- Analusis of Financial StatementDocument28 pagesAnalusis of Financial StatementAjaykumar MauryaNo ratings yet

- Financial Accounting: Balance SheetDocument53 pagesFinancial Accounting: Balance SheetSNo ratings yet

- Financial Reporting and Analysis - SIGFi - Finance HandbookDocument12 pagesFinancial Reporting and Analysis - SIGFi - Finance HandbookSneha TatiNo ratings yet

- EBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and CoronavirusDocument24 pagesEBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and Coronavirusks frNo ratings yet

- FRA-NewDocument31 pagesFRA-NewAbhishek DograNo ratings yet

- Types of Major AccountsDocument43 pagesTypes of Major AccountsMaeshien Posiquit AboNo ratings yet

- Financial ManagementDocument50 pagesFinancial ManagementLEO FRAGGERNo ratings yet

- Accounting Principles and Procedures: For Rics ApcDocument20 pagesAccounting Principles and Procedures: For Rics ApcSumayya TariqNo ratings yet

- Basics of Financial AccountingDocument30 pagesBasics of Financial AccountingSAURABH PATELNo ratings yet

- ACCOUNTING TERMS and Their Definitions: AssetsDocument8 pagesACCOUNTING TERMS and Their Definitions: AssetsNoby Ann Vargas LobeteNo ratings yet

- Chapter 06: Understanding Cash Flow StatementsDocument23 pagesChapter 06: Understanding Cash Flow StatementsSadia RahmanNo ratings yet

- 1 - GlossaryDocument2 pages1 - GlossaryTyranid SwarmlordNo ratings yet

- Golis University: Faculty of Business and Economics Chapter Six Balance SheetDocument22 pagesGolis University: Faculty of Business and Economics Chapter Six Balance Sheetsaed cabdiNo ratings yet

- Session 5 - Financial Statement AnalysisDocument42 pagesSession 5 - Financial Statement AnalysisVaibhav JainNo ratings yet

- Finance Ch4Document41 pagesFinance Ch4Tofig HuseynliNo ratings yet

- PC-14 - Day 1 - Session-1 - 22.03.2023Document14 pagesPC-14 - Day 1 - Session-1 - 22.03.2023Ajaya SahooNo ratings yet

- CTRL Vol4Document19 pagesCTRL Vol4Roberto SanchezNo ratings yet

- Untitled PresentationDocument21 pagesUntitled Presentationyhafsa378No ratings yet

- Financial Accounting and Analysis: Internal Assignment Applicable For June 2021examinationDocument10 pagesFinancial Accounting and Analysis: Internal Assignment Applicable For June 2021examinationTeChtroNiCS [AK]No ratings yet

- The Balance SheetDocument101 pagesThe Balance SheethakomoNo ratings yet

- Part 6.a - AccountingDocument38 pagesPart 6.a - AccountingzhengcunzhangNo ratings yet

- Week 4Document36 pagesWeek 4Mariah Cielo DaguroNo ratings yet

- FABM2 - Lesson 1Document27 pagesFABM2 - Lesson 1wendell john mediana100% (1)

- Fabm 2 and FinanceDocument5 pagesFabm 2 and FinanceLenard TaberdoNo ratings yet

- L11 Financial Management 2020Document30 pagesL11 Financial Management 2020NURIN SOFIYA BT ZAKARIA / UPMNo ratings yet

- Cash Flow StatementDocument19 pagesCash Flow StatementGokul KulNo ratings yet

- Unit 2 (Understanding Financial Statements and Cash Flows)Document63 pagesUnit 2 (Understanding Financial Statements and Cash Flows)poohoiying20020524No ratings yet

- Essential Concepts in Managerial Finance: Analysis of Financial Statements (Chapter 2)Document12 pagesEssential Concepts in Managerial Finance: Analysis of Financial Statements (Chapter 2)Allyana Joy NicolasNo ratings yet

- Apuntes AccountingDocument35 pagesApuntes AccountingPatricia Barquin DelgadoNo ratings yet

- Accounting BasicsDocument13 pagesAccounting BasicskameshpatilNo ratings yet

- Balance Sheet Dimasaka & JaranillaDocument56 pagesBalance Sheet Dimasaka & JaranillaShaneBattierNo ratings yet

- Accounting and BookkeepingDocument45 pagesAccounting and BookkeepingMarcel VelascoNo ratings yet

- FINANCIALSTUDYDocument47 pagesFINANCIALSTUDYoliverreromaNo ratings yet

- Lecture 3 - Financial Statements-1Document39 pagesLecture 3 - Financial Statements-1ikhsanNo ratings yet

- Chapter 5 AccountingDocument23 pagesChapter 5 AccountingShania PersaudNo ratings yet

- FABM2 - Statement of Financial PositionDocument36 pagesFABM2 - Statement of Financial PositionVron Blatz100% (6)

- Accounting 101Document25 pagesAccounting 101dalpra.m04No ratings yet

- Bachelor of Business ManagemnetDocument25 pagesBachelor of Business ManagemnetClovey CsyNo ratings yet

- Chapter 12Document8 pagesChapter 12Hareem Zoya WarsiNo ratings yet

- Fundamentals of AccountingDocument5 pagesFundamentals of AccountingawitakintoNo ratings yet

- Financial AppraisalDocument54 pagesFinancial AppraisalAarsh SainiNo ratings yet

- Lecture - 2: Financial Reporting and AccountingDocument41 pagesLecture - 2: Financial Reporting and AccountingMuhammad Waheed SattiNo ratings yet

- Finance ShortcourseDocument46 pagesFinance Shortcoursemahendra ega higuittaNo ratings yet

- Annual ReportDocument5 pagesAnnual Reportmengjun0987654311No ratings yet

- Online Payment SystemDocument1 pageOnline Payment SystemAnonymous 6KWNHZPVINo ratings yet

- 02.03 Letter of RepresenationDocument3 pages02.03 Letter of RepresenationEdison TabakuNo ratings yet

- GRC RulesetDocument6 pagesGRC RulesetDAVIDNo ratings yet

- Basel III Important SectionsDocument22 pagesBasel III Important SectionsGeorge Lekatis100% (1)

- Vision PT 365 Economy 2019Document69 pagesVision PT 365 Economy 2019ajit yashwantraoNo ratings yet

- NonArcaETFs ETNs090808Document5 pagesNonArcaETFs ETNs090808mgarrett00No ratings yet

- LEDGER & Trial BalanceDocument3 pagesLEDGER & Trial BalanceShaba Ponu JacobNo ratings yet

- In The Balance Sheet Above, The Excess Reserve Ratio of ABC Bank Is - and Its Excess Reserves AreDocument5 pagesIn The Balance Sheet Above, The Excess Reserve Ratio of ABC Bank Is - and Its Excess Reserves AreAnnNo ratings yet

- Ratio Analysis of Heidelberg Cement BangladeshDocument15 pagesRatio Analysis of Heidelberg Cement BangladeshMehedi Hasan DurjoyNo ratings yet

- Yeni Microsoft Word BelgesiDocument2 pagesYeni Microsoft Word Belgesibircan basalNo ratings yet

- Negotiable Instruments Case Digests For November 8Document3 pagesNegotiable Instruments Case Digests For November 8Megan MateoNo ratings yet

- Field Report JackyDocument31 pagesField Report JackyGracey KinimoNo ratings yet

- Ac 38644873405Document6 pagesAc 38644873405ajstrading27No ratings yet

- CFAB Accounting Chapter 15. Sole Trader and Partnership Financial Statement Under UK GAAPDocument18 pagesCFAB Accounting Chapter 15. Sole Trader and Partnership Financial Statement Under UK GAAPHuy NguyenNo ratings yet

- Account Statement For Account:0820001500005003: Branch DetailsDocument28 pagesAccount Statement For Account:0820001500005003: Branch DetailsAnmol DeepNo ratings yet

- Aptoinn Nata Coaching Centre - 2013 Application Form 4 PagesDocument4 pagesAptoinn Nata Coaching Centre - 2013 Application Form 4 PagesAniket MahaleNo ratings yet

- Intermediate Accounting 1Document49 pagesIntermediate Accounting 1Harry EvangelistaNo ratings yet

- Credit Management For CooperativesDocument141 pagesCredit Management For CooperativesAndres Lorenzo III75% (16)

- Docs in A Box, Inc.Document6 pagesDocs in A Box, Inc.Leonardo D NinoNo ratings yet

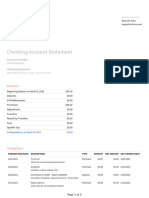

- Checking Account StatementDocument3 pagesChecking Account Statementandyspeers0No ratings yet

- Internet Banking-OOAD PROJECTDocument27 pagesInternet Banking-OOAD PROJECTAbhishek Shah100% (2)

- Ref - No. 2302875-11218095-5: Sakib AkhtarDocument5 pagesRef - No. 2302875-11218095-5: Sakib AkhtarMONISH NAYARNo ratings yet

- Advance Untuk Air GalonDocument3 pagesAdvance Untuk Air Galonslamet supriyadiNo ratings yet

- CIA-1 Sushanth BSDocument5 pagesCIA-1 Sushanth BSKausik BhagatNo ratings yet

- Bsa3b Ia Ipppe BaltazarDocument6 pagesBsa3b Ia Ipppe BaltazarElaine Joyce GarciaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Admission Letter ATUDocument1 pageAdmission Letter ATUIsaac Clarity MensahNo ratings yet

- Name: Ahmed Idris Abaker K Customer No: 2812095 Account Type: Saving Account Currency: SDG Issue Date: 19-03-2023Document17 pagesName: Ahmed Idris Abaker K Customer No: 2812095 Account Type: Saving Account Currency: SDG Issue Date: 19-03-2023Ahmed EdrisNo ratings yet

- NC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerDocument34 pagesNC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerSheila Mae Lira100% (2)

- Financial Accounting Chapter 3Document5 pagesFinancial Accounting Chapter 3NiraniyaNo ratings yet

- Chapter 3: Managerial Accounting - Job Order CostingDocument2 pagesChapter 3: Managerial Accounting - Job Order Costingagm25No ratings yet

- Introducing Financial Statements and Transaction AnalysisDocument64 pagesIntroducing Financial Statements and Transaction AnalysisHazim AbualolaNo ratings yet

- Accounting & FinanceDocument17 pagesAccounting & FinanceInbasaat PirzadaNo ratings yet

- ACM 31 Lec2Document18 pagesACM 31 Lec2Vishal AmbadNo ratings yet

- CH 5Document58 pagesCH 5marwan2004acctNo ratings yet

- Introduction To AccountingDocument15 pagesIntroduction To Accountingluna dupontNo ratings yet

- Accounting and Financial Management in LogisticsDocument23 pagesAccounting and Financial Management in LogisticsWah KhaingNo ratings yet

- Account TitlesDocument4 pagesAccount TitlesChristian VelascoNo ratings yet

- An Introduction To Business and AccountingDocument43 pagesAn Introduction To Business and AccountingKeo VannuthNo ratings yet

- FCFChap002 - Financial StatementsDocument23 pagesFCFChap002 - Financial StatementsSozia TanNo ratings yet

- Financial Accounting - An Introduction: DR Vandana Bhama FORE School of Management, DelhiDocument30 pagesFinancial Accounting - An Introduction: DR Vandana Bhama FORE School of Management, DelhiShavik BaralNo ratings yet

- Balance Sheet: by Dr. ArchanaDocument19 pagesBalance Sheet: by Dr. ArchanaHan JeeNo ratings yet

- 2.2 Financial StatementsDocument38 pages2.2 Financial StatementsNefarioDMNo ratings yet

- Managing The Venture's Financial ResourcesDocument28 pagesManaging The Venture's Financial ResourcesAnto DNo ratings yet

- Analusis of Financial StatementDocument28 pagesAnalusis of Financial StatementAjaykumar MauryaNo ratings yet

- Financial Accounting: Balance SheetDocument53 pagesFinancial Accounting: Balance SheetSNo ratings yet

- Financial Reporting and Analysis - SIGFi - Finance HandbookDocument12 pagesFinancial Reporting and Analysis - SIGFi - Finance HandbookSneha TatiNo ratings yet

- EBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and CoronavirusDocument24 pagesEBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and Coronavirusks frNo ratings yet

- FRA-NewDocument31 pagesFRA-NewAbhishek DograNo ratings yet

- Types of Major AccountsDocument43 pagesTypes of Major AccountsMaeshien Posiquit AboNo ratings yet

- Financial ManagementDocument50 pagesFinancial ManagementLEO FRAGGERNo ratings yet

- Accounting Principles and Procedures: For Rics ApcDocument20 pagesAccounting Principles and Procedures: For Rics ApcSumayya TariqNo ratings yet

- Basics of Financial AccountingDocument30 pagesBasics of Financial AccountingSAURABH PATELNo ratings yet

- ACCOUNTING TERMS and Their Definitions: AssetsDocument8 pagesACCOUNTING TERMS and Their Definitions: AssetsNoby Ann Vargas LobeteNo ratings yet

- Chapter 06: Understanding Cash Flow StatementsDocument23 pagesChapter 06: Understanding Cash Flow StatementsSadia RahmanNo ratings yet

- 1 - GlossaryDocument2 pages1 - GlossaryTyranid SwarmlordNo ratings yet

- Golis University: Faculty of Business and Economics Chapter Six Balance SheetDocument22 pagesGolis University: Faculty of Business and Economics Chapter Six Balance Sheetsaed cabdiNo ratings yet

- Session 5 - Financial Statement AnalysisDocument42 pagesSession 5 - Financial Statement AnalysisVaibhav JainNo ratings yet

- Finance Ch4Document41 pagesFinance Ch4Tofig HuseynliNo ratings yet

- PC-14 - Day 1 - Session-1 - 22.03.2023Document14 pagesPC-14 - Day 1 - Session-1 - 22.03.2023Ajaya SahooNo ratings yet

- CTRL Vol4Document19 pagesCTRL Vol4Roberto SanchezNo ratings yet

- Untitled PresentationDocument21 pagesUntitled Presentationyhafsa378No ratings yet

- Financial Accounting and Analysis: Internal Assignment Applicable For June 2021examinationDocument10 pagesFinancial Accounting and Analysis: Internal Assignment Applicable For June 2021examinationTeChtroNiCS [AK]No ratings yet

- The Balance SheetDocument101 pagesThe Balance SheethakomoNo ratings yet

- Part 6.a - AccountingDocument38 pagesPart 6.a - AccountingzhengcunzhangNo ratings yet

- Week 4Document36 pagesWeek 4Mariah Cielo DaguroNo ratings yet

- FABM2 - Lesson 1Document27 pagesFABM2 - Lesson 1wendell john mediana100% (1)

- Fabm 2 and FinanceDocument5 pagesFabm 2 and FinanceLenard TaberdoNo ratings yet

- L11 Financial Management 2020Document30 pagesL11 Financial Management 2020NURIN SOFIYA BT ZAKARIA / UPMNo ratings yet

- Cash Flow StatementDocument19 pagesCash Flow StatementGokul KulNo ratings yet

- Unit 2 (Understanding Financial Statements and Cash Flows)Document63 pagesUnit 2 (Understanding Financial Statements and Cash Flows)poohoiying20020524No ratings yet

- Essential Concepts in Managerial Finance: Analysis of Financial Statements (Chapter 2)Document12 pagesEssential Concepts in Managerial Finance: Analysis of Financial Statements (Chapter 2)Allyana Joy NicolasNo ratings yet

- Apuntes AccountingDocument35 pagesApuntes AccountingPatricia Barquin DelgadoNo ratings yet

- Accounting BasicsDocument13 pagesAccounting BasicskameshpatilNo ratings yet

- Balance Sheet Dimasaka & JaranillaDocument56 pagesBalance Sheet Dimasaka & JaranillaShaneBattierNo ratings yet

- Accounting and BookkeepingDocument45 pagesAccounting and BookkeepingMarcel VelascoNo ratings yet

- FINANCIALSTUDYDocument47 pagesFINANCIALSTUDYoliverreromaNo ratings yet

- Lecture 3 - Financial Statements-1Document39 pagesLecture 3 - Financial Statements-1ikhsanNo ratings yet

- Chapter 5 AccountingDocument23 pagesChapter 5 AccountingShania PersaudNo ratings yet

- FABM2 - Statement of Financial PositionDocument36 pagesFABM2 - Statement of Financial PositionVron Blatz100% (6)

- Accounting 101Document25 pagesAccounting 101dalpra.m04No ratings yet

- Bachelor of Business ManagemnetDocument25 pagesBachelor of Business ManagemnetClovey CsyNo ratings yet

- Chapter 12Document8 pagesChapter 12Hareem Zoya WarsiNo ratings yet

- Fundamentals of AccountingDocument5 pagesFundamentals of AccountingawitakintoNo ratings yet

- Financial AppraisalDocument54 pagesFinancial AppraisalAarsh SainiNo ratings yet

- Lecture - 2: Financial Reporting and AccountingDocument41 pagesLecture - 2: Financial Reporting and AccountingMuhammad Waheed SattiNo ratings yet

- Finance ShortcourseDocument46 pagesFinance Shortcoursemahendra ega higuittaNo ratings yet

- Annual ReportDocument5 pagesAnnual Reportmengjun0987654311No ratings yet

- Online Payment SystemDocument1 pageOnline Payment SystemAnonymous 6KWNHZPVINo ratings yet

- 02.03 Letter of RepresenationDocument3 pages02.03 Letter of RepresenationEdison TabakuNo ratings yet

- GRC RulesetDocument6 pagesGRC RulesetDAVIDNo ratings yet

- Basel III Important SectionsDocument22 pagesBasel III Important SectionsGeorge Lekatis100% (1)

- Vision PT 365 Economy 2019Document69 pagesVision PT 365 Economy 2019ajit yashwantraoNo ratings yet

- NonArcaETFs ETNs090808Document5 pagesNonArcaETFs ETNs090808mgarrett00No ratings yet

- LEDGER & Trial BalanceDocument3 pagesLEDGER & Trial BalanceShaba Ponu JacobNo ratings yet

- In The Balance Sheet Above, The Excess Reserve Ratio of ABC Bank Is - and Its Excess Reserves AreDocument5 pagesIn The Balance Sheet Above, The Excess Reserve Ratio of ABC Bank Is - and Its Excess Reserves AreAnnNo ratings yet

- Ratio Analysis of Heidelberg Cement BangladeshDocument15 pagesRatio Analysis of Heidelberg Cement BangladeshMehedi Hasan DurjoyNo ratings yet

- Yeni Microsoft Word BelgesiDocument2 pagesYeni Microsoft Word Belgesibircan basalNo ratings yet

- Negotiable Instruments Case Digests For November 8Document3 pagesNegotiable Instruments Case Digests For November 8Megan MateoNo ratings yet

- Field Report JackyDocument31 pagesField Report JackyGracey KinimoNo ratings yet

- Ac 38644873405Document6 pagesAc 38644873405ajstrading27No ratings yet

- CFAB Accounting Chapter 15. Sole Trader and Partnership Financial Statement Under UK GAAPDocument18 pagesCFAB Accounting Chapter 15. Sole Trader and Partnership Financial Statement Under UK GAAPHuy NguyenNo ratings yet

- Account Statement For Account:0820001500005003: Branch DetailsDocument28 pagesAccount Statement For Account:0820001500005003: Branch DetailsAnmol DeepNo ratings yet

- Aptoinn Nata Coaching Centre - 2013 Application Form 4 PagesDocument4 pagesAptoinn Nata Coaching Centre - 2013 Application Form 4 PagesAniket MahaleNo ratings yet

- Intermediate Accounting 1Document49 pagesIntermediate Accounting 1Harry EvangelistaNo ratings yet

- Credit Management For CooperativesDocument141 pagesCredit Management For CooperativesAndres Lorenzo III75% (16)

- Docs in A Box, Inc.Document6 pagesDocs in A Box, Inc.Leonardo D NinoNo ratings yet

- Checking Account StatementDocument3 pagesChecking Account Statementandyspeers0No ratings yet

- Internet Banking-OOAD PROJECTDocument27 pagesInternet Banking-OOAD PROJECTAbhishek Shah100% (2)

- Ref - No. 2302875-11218095-5: Sakib AkhtarDocument5 pagesRef - No. 2302875-11218095-5: Sakib AkhtarMONISH NAYARNo ratings yet

- Advance Untuk Air GalonDocument3 pagesAdvance Untuk Air Galonslamet supriyadiNo ratings yet

- CIA-1 Sushanth BSDocument5 pagesCIA-1 Sushanth BSKausik BhagatNo ratings yet

- Bsa3b Ia Ipppe BaltazarDocument6 pagesBsa3b Ia Ipppe BaltazarElaine Joyce GarciaNo ratings yet