Download as pptx, pdf, or txt

You might also like

- Updated To Stop or Pre - Foreclosure of Real Property - Affidavit & InstructionsDocument4 pagesUpdated To Stop or Pre - Foreclosure of Real Property - Affidavit & Instructionsricetech100% (7)

- Guide To Auditing IFRS 9 Expected Credit LossDocument75 pagesGuide To Auditing IFRS 9 Expected Credit LossVikram Oberoi100% (3)

- Accounting Test Bank - Bank ReconciliationDocument2 pagesAccounting Test Bank - Bank ReconciliationAyesha RGNo ratings yet

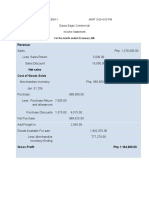

- Cost of Goods Manufactured Income Statement Norton IndustriesDocument2 pagesCost of Goods Manufactured Income Statement Norton IndustriesAmit PandeyNo ratings yet

- Cash Collateral AgreementDocument11 pagesCash Collateral AgreementJudge ReinholdNo ratings yet

- Chapter 11 TestbankDocument34 pagesChapter 11 TestbankFami FamzNo ratings yet

- Sale Deed ProjectDocument5 pagesSale Deed ProjectFaraz Siddiqui100% (1)

- Liabilities: B-ACTG214 SY2019-2020 de La Salle University - DasmariñasDocument158 pagesLiabilities: B-ACTG214 SY2019-2020 de La Salle University - DasmariñasErika Mae LegaspiNo ratings yet

- Conceptual Framework and Accounting Standards - Chapter 2 - NotesDocument5 pagesConceptual Framework and Accounting Standards - Chapter 2 - NotesKhey KheyNo ratings yet

- Intermediate Accounting - Final Output ReceivablesDocument56 pagesIntermediate Accounting - Final Output ReceivablesAnitas LimmaumNo ratings yet

- 03 - Partnership DissolutionDocument38 pages03 - Partnership DissolutionDonise Ronadel SantosNo ratings yet

- 1Document19 pages1Angelica Castillo0% (1)

- Financial Accounting and Reporting ReviewerDocument3 pagesFinancial Accounting and Reporting Reviewercece vergieNo ratings yet

- Chapter4 IA Midterm BuenaventuraDocument10 pagesChapter4 IA Midterm BuenaventuraAnonnNo ratings yet

- Comprehensive ProblemDocument14 pagesComprehensive ProblemMarian Augelio PolancoNo ratings yet

- Quiz No. 1: Intermediate Accounting, Part 4Document3 pagesQuiz No. 1: Intermediate Accounting, Part 4Paula BautistaNo ratings yet

- Accounts Receivable: QuizDocument4 pagesAccounts Receivable: QuizRisa Castillo MiguelNo ratings yet

- Chapter 4 - Accounts ReceivableDocument2 pagesChapter 4 - Accounts ReceivableJerome_JadeNo ratings yet

- Three Methods of Estimating Doubtful AccountsDocument8 pagesThree Methods of Estimating Doubtful AccountsJay Lou PayotNo ratings yet

- Conceptual Framework For Financial ReportingDocument8 pagesConceptual Framework For Financial ReportingsmlingwaNo ratings yet

- First Time Adoption of PFRSDocument5 pagesFirst Time Adoption of PFRSPia ArellanoNo ratings yet

- Finman Test BankDocument3 pagesFinman Test BankATHALIAH LUNA MERCADEJASNo ratings yet

- CF FS and Reporting EntityDocument5 pagesCF FS and Reporting Entitypanda 1No ratings yet

- Midterm Answer KeyDocument6 pagesMidterm Answer Keyazzenethfaye.delacruz.mnlNo ratings yet

- CFAS - Lec. 10 PAS 24 and 26Document13 pagesCFAS - Lec. 10 PAS 24 and 26latte aeriNo ratings yet

- MEDINA - Homework 1 No. 14Document7 pagesMEDINA - Homework 1 No. 14Von Andrei MedinaNo ratings yet

- Exercises On Closing Entries & Reversing EntriesDocument3 pagesExercises On Closing Entries & Reversing EntriesRoy BonitezNo ratings yet

- IntAcc-1 Accounting For ReceivablesDocument13 pagesIntAcc-1 Accounting For ReceivablesShekainah BNo ratings yet

- Merchadising MOCK QUIZDocument5 pagesMerchadising MOCK QUIZCarl Dhaniel Garcia SalenNo ratings yet

- PrelimsDocument24 pagesPrelimsRhea BadanaNo ratings yet

- Cash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsDocument30 pagesCash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsKim Audrey JalalainNo ratings yet

- 8 Inventory EstimationDocument3 pages8 Inventory EstimationJorufel PapasinNo ratings yet

- Substantive Test: Receivables and SalesDocument10 pagesSubstantive Test: Receivables and SalesJoris YapNo ratings yet

- Midterm Exam Parcor 2020Document1 pageMidterm Exam Parcor 2020John Alfred CastinoNo ratings yet

- Chapter 2 Accounting 300 Exam ReviewDocument2 pagesChapter 2 Accounting 300 Exam Reviewagm25No ratings yet

- Chapter 5 (Estimation of Doubtful Accounts)Document8 pagesChapter 5 (Estimation of Doubtful Accounts)Joan LeonorNo ratings yet

- Parcor QuizbowlDocument38 pagesParcor QuizbowlKrestyl Ann GabaldaNo ratings yet

- Financial Management BSATDocument9 pagesFinancial Management BSATEma Dupilas GuianalanNo ratings yet

- Las 6Document4 pagesLas 6Venus Abarico Banque-AbenionNo ratings yet

- Problems 7 10Document19 pagesProblems 7 10Margiery GannabanNo ratings yet

- Finmar Final Quiz Answer KeysDocument15 pagesFinmar Final Quiz Answer KeysGailee VinNo ratings yet

- Property, Plant and EquipmentDocument40 pagesProperty, Plant and EquipmentNatalie SerranoNo ratings yet

- Chapter 6 Cfas ReviewerDocument2 pagesChapter 6 Cfas ReviewerBabeEbab AndreiNo ratings yet

- Finmar 1 5Document11 pagesFinmar 1 5Bhosx KimNo ratings yet

- CF Objective of Financial ReportingDocument6 pagesCF Objective of Financial Reportingpanda 1No ratings yet

- CfasDocument32 pagesCfasLouiseNo ratings yet

- Module 2 ReceivablesDocument43 pagesModule 2 Receivableszarnaih SmithNo ratings yet

- Adjusting ProbsDocument6 pagesAdjusting ProbsKrisha JohnsonNo ratings yet

- CF Qualitative CharacteristicsDocument3 pagesCF Qualitative Characteristicspanda 1No ratings yet

- Conceptual Framework: & Accounting StandardsDocument9 pagesConceptual Framework: & Accounting StandardsBritnys NimNo ratings yet

- AC 3 - Intermediate Acctg' 1 (Ate Jan Ver)Document119 pagesAC 3 - Intermediate Acctg' 1 (Ate Jan Ver)John Renier Bernardo100% (1)

- Partnetship DissolutionDocument45 pagesPartnetship DissolutionDe Gala ShailynNo ratings yet

- Chapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Document1 pageChapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Ianna ManieboNo ratings yet

- This Study Resource Was: (Stale Check)Document2 pagesThis Study Resource Was: (Stale Check)Lyca Mae CubangbangNo ratings yet

- Receivable Financing: Pledge, Assignment and FactoringDocument35 pagesReceivable Financing: Pledge, Assignment and FactoringMARY GRACE VARGASNo ratings yet

- Chapter 26 Land and BuildingDocument17 pagesChapter 26 Land and BuildingKendall JennerNo ratings yet

- Ast-Chapter 1 p3, p5, p6Document8 pagesAst-Chapter 1 p3, p5, p6Geminah BellenNo ratings yet

- Absorption Costing Vs Variable CostingDocument20 pagesAbsorption Costing Vs Variable CostingMa. Alene MagdaraogNo ratings yet

- Davao - Eagle - Com JOSEPHDocument6 pagesDavao - Eagle - Com JOSEPHablay logeneNo ratings yet

- Chapter 24 Government GrantDocument19 pagesChapter 24 Government GrantKendall JennerNo ratings yet

- Cash and Cash Equivalents 1Document15 pagesCash and Cash Equivalents 1Micko LagundinoNo ratings yet

- 6726 Revised Conceptual FrameworkDocument7 pages6726 Revised Conceptual FrameworkJane ValenciaNo ratings yet

- Chapter 7Document39 pagesChapter 7juls100% (1)

- Accounting For Receivables Accounts ReceivableDocument18 pagesAccounting For Receivables Accounts Receivablelocomotingkenya.co.keNo ratings yet

- Computing Loans Involving Partial Payments Before MaturityDocument2 pagesComputing Loans Involving Partial Payments Before MaturityIcekwim05No ratings yet

- Topic 6 - Charges (Part 1)Document16 pagesTopic 6 - Charges (Part 1)J Enn WooNo ratings yet

- GSIS Retirement Form PDFDocument4 pagesGSIS Retirement Form PDFSam ReyesNo ratings yet

- Sec 16Document38 pagesSec 16kristel jane caldozaNo ratings yet

- Ploan 2 PDFDocument2 pagesPloan 2 PDFmahavirNo ratings yet

- AINZA vs. PADUA G.R. No. 165420, June 30, 2005: FactDocument8 pagesAINZA vs. PADUA G.R. No. 165420, June 30, 2005: FactRa QuNo ratings yet

- 1302-19-672-030 SynopsisDocument17 pages1302-19-672-030 SynopsisMohmmedKhayyumNo ratings yet

- Housing Delivery Systems in The Philippines: Faith Caridad I. Hernandez Faculty, College of ArchitectureDocument99 pagesHousing Delivery Systems in The Philippines: Faith Caridad I. Hernandez Faculty, College of ArchitectureJess AndanNo ratings yet

- Bank GuaranteeDocument7 pagesBank GuaranteeDrashti RaichuraNo ratings yet

- SHG Role of Self Help GroupsDocument13 pagesSHG Role of Self Help Groupsapi-372956486% (7)

- Home Building 101Document9 pagesHome Building 101Rajneesh KambojNo ratings yet

- PDFDocument24 pagesPDFBeboy Paylangco EvardoNo ratings yet

- Bachrach Motors V Ledesma Case DigestDocument2 pagesBachrach Motors V Ledesma Case DigestZirk TanNo ratings yet

- Government Assisted HousingDocument2 pagesGovernment Assisted HousingKlent Evran JalecoNo ratings yet

- Tally Notes - Basic Accounting PDFDocument31 pagesTally Notes - Basic Accounting PDFSudhir Kumar100% (1)

- Mba 410: Commercial Banking Credit Units: 03 Course ObjectivesDocument6 pagesMba 410: Commercial Banking Credit Units: 03 Course ObjectivesakmohideenNo ratings yet

- Solved SMU AssignmentDocument4 pagesSolved SMU AssignmentArvind KNo ratings yet

- Specpro Digests Rule 88-90Document18 pagesSpecpro Digests Rule 88-90Jan kristelNo ratings yet

- Case InformationDocument3 pagesCase Informationmglennonexaminer100% (1)

- Here's How I Went From Low Scores and 44%ile in XAT To The XLRI 2015 Batch..Document11 pagesHere's How I Went From Low Scores and 44%ile in XAT To The XLRI 2015 Batch..wolfrum74No ratings yet

- Donor Tax Examples-For DiscussionDocument2 pagesDonor Tax Examples-For DiscussionRey PerosaNo ratings yet

- MBSB Personal Financing-I 2013 (BIRO & NB)Document21 pagesMBSB Personal Financing-I 2013 (BIRO & NB)kamarulabdulNo ratings yet

- Joann Rein Depo Aurora RobosignerDocument113 pagesJoann Rein Depo Aurora RobosignerDinSFLANo ratings yet

- Pradhan Mantri MUDRA YojanaDocument3 pagesPradhan Mantri MUDRA YojanaUjjwal MishraNo ratings yet

- San Miguel Brewery Vs La Union 1361Document4 pagesSan Miguel Brewery Vs La Union 1361Angelic ArcherNo ratings yet