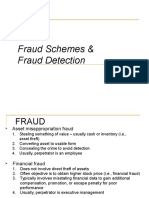

Ethics, Fraud, and Internal Control

Ethics, Fraud, and Internal Control

You might also like

- ERM ChecklistDocument4 pagesERM Checklistaqsa_munir100% (1)

- COunter Affidavit EstafaDocument7 pagesCOunter Affidavit EstafaCheChe89% (19)

- GOVERNANCEDocument2 pagesGOVERNANCENour Aira Nao50% (2)

- Mastering Internal Controls TestbankDocument6 pagesMastering Internal Controls TestbankLade PalkanNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Auditng External Business RelationshipsDocument19 pagesAuditng External Business RelationshipsFernando Ernesto CabralNo ratings yet

- Victor Lustig3 PDFDocument5 pagesVictor Lustig3 PDFShiv Mani NdrNo ratings yet

- Forensic and Investigative AccountingDocument51 pagesForensic and Investigative AccountingNarendra Sengupta100% (5)

- Ethics, Fraud, and Internal Control: Presented byDocument40 pagesEthics, Fraud, and Internal Control: Presented byALMA MORENANo ratings yet

- Internal Control System of A Bank (Dutch Bangla Bank Limited) .Document42 pagesInternal Control System of A Bank (Dutch Bangla Bank Limited) .Tasmia100% (1)

- Ethics Fraud Schemes and Fraud DetectionDocument31 pagesEthics Fraud Schemes and Fraud DetectionJosephine CristajuneNo ratings yet

- Internal Audit Stakeholder Management and The Three Lines of Defense Slide DeckDocument12 pagesInternal Audit Stakeholder Management and The Three Lines of Defense Slide DeckSheyam SelvarajNo ratings yet

- Fraud Examination, 3E: Chapter 1: The Nature of FraudDocument25 pagesFraud Examination, 3E: Chapter 1: The Nature of Fraudpeaceajah100% (1)

- Ethics, Fraud, and Internal ControlDocument22 pagesEthics, Fraud, and Internal ControlsariNo ratings yet

- CH 12 Fraud and ErrorDocument28 pagesCH 12 Fraud and ErrorJoyce Anne GarduqueNo ratings yet

- Impact and Likelihood ScalesDocument3 pagesImpact and Likelihood ScalesRhea SimoneNo ratings yet

- Internal Control-Integrated FrameworkDocument34 pagesInternal Control-Integrated FrameworkInternational Consortium on Governmental Financial Management100% (1)

- Fraud at The Engagement Level: Expositor: Javier BecerraDocument11 pagesFraud at The Engagement Level: Expositor: Javier BecerraWalter Córdova MacedoNo ratings yet

- C Hap Ter 1 3 Overviewof Internal ControlDocument53 pagesC Hap Ter 1 3 Overviewof Internal ControlMariel Rasco100% (1)

- Fraud Position StatementDocument4 pagesFraud Position StatementsenoltoygarNo ratings yet

- FRAUDDocument3 pagesFRAUDprincess manlangitNo ratings yet

- COSO Framework Components and Related Principles: ExhibitDocument1 pageCOSO Framework Components and Related Principles: ExhibitRajat MathurNo ratings yet

- Fraud - Internal Auditing PDFDocument4 pagesFraud - Internal Auditing PDFJaJ08No ratings yet

- The 17 COSO Internal Control PrinciplesDocument7 pagesThe 17 COSO Internal Control Principleseskelapamudah enakNo ratings yet

- Fraud Indicators AuditorsDocument35 pagesFraud Indicators AuditorsMutabarKhanNo ratings yet

- ACC 420 The Fraud Triangle TheoryDocument2 pagesACC 420 The Fraud Triangle TheoryIfemide50% (2)

- Fraud Risk Management ProgramDocument68 pagesFraud Risk Management Programaa yudhoNo ratings yet

- 04 - Fraud Risk Management A Guide To GOOD PRACTICEDocument48 pages04 - Fraud Risk Management A Guide To GOOD PRACTICEEd Gonzales GonzalesNo ratings yet

- COSO FrameworkDocument0 pagesCOSO FrameworkCynthia StoneNo ratings yet

- Checklist For Evaluating Internal Controls ACC 544 Amanda SmithDocument8 pagesChecklist For Evaluating Internal Controls ACC 544 Amanda SmithAmanda GilbertNo ratings yet

- Internal Controls 101Document25 pagesInternal Controls 101Arcee Orcullo100% (1)

- Corporate GovernanceDocument47 pagesCorporate GovernanceShivani100% (1)

- Chapter 1 - CISDocument37 pagesChapter 1 - CISMaeNeth Gullan100% (1)

- Fraud PaperDocument80 pagesFraud Papernasir_m68No ratings yet

- Test of Controls For Some Major ActivitiesDocument22 pagesTest of Controls For Some Major ActivitiesMohsin RazaNo ratings yet

- Internal Control Self Assessment QuestionnaireDocument4 pagesInternal Control Self Assessment QuestionnaireHime Silhouette Gabriel100% (1)

- COSO Fraud Risk Management Guide Executive SummaryDocument13 pagesCOSO Fraud Risk Management Guide Executive SummarymohamedciaNo ratings yet

- PG Engagement Planning Assessing Fraud RisksDocument23 pagesPG Engagement Planning Assessing Fraud RisksRoland Val100% (1)

- Fraud Risk AssessmentDocument32 pagesFraud Risk AssessmentArturoNo ratings yet

- WorldCom Fraud PPT (Accounting Learning)Document12 pagesWorldCom Fraud PPT (Accounting Learning)蒲睿灵No ratings yet

- Fraud Risk Assessment - HandoutsDocument22 pagesFraud Risk Assessment - Handoutsrubel_nsuNo ratings yet

- The Marketing Finance Interface: Cgma ReportDocument48 pagesThe Marketing Finance Interface: Cgma ReportChristie RochaNo ratings yet

- Good AuditorDocument20 pagesGood AuditorBertu NatanaNo ratings yet

- Internal Controls and ERPDocument5 pagesInternal Controls and ERPapi-3748088No ratings yet

- 3 2018 L8 Gov.,Risk Management, ComplianceDocument13 pages3 2018 L8 Gov.,Risk Management, ComplianceTing Phin Yuan100% (1)

- Co So Enterprise Risk Management FrameworkDocument2 pagesCo So Enterprise Risk Management FrameworkasifsubhanNo ratings yet

- Solution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atDocument35 pagesSolution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atmichelle100% (1)

- Fraud-Tree SchemesDocument13 pagesFraud-Tree SchemessulthanhakimNo ratings yet

- Consideration of Internal ControlDocument69 pagesConsideration of Internal Controlmah loveNo ratings yet

- 2015 Leveraging COSO 3LODDocument32 pages2015 Leveraging COSO 3LODalfonsodzibNo ratings yet

- Fraud Risk FormDocument2 pagesFraud Risk FormShelvy SilviaNo ratings yet

- Simplified Sample Entity Level Control Matrices ImpDocument7 pagesSimplified Sample Entity Level Control Matrices ImpAqeelAhmadNo ratings yet

- 3-YR Internal Audit PlanDocument9 pages3-YR Internal Audit PlanJb LavariasNo ratings yet

- Bachelor of Science in Accountancy: GRC 2001: Introduction To Corporate GovernanceDocument2 pagesBachelor of Science in Accountancy: GRC 2001: Introduction To Corporate GovernanceJherryMigLazaroSevilla100% (9)

- Enterprise Risk Management-The COSO Framework: A Primer and Tool For The Audit CommitteeDocument12 pagesEnterprise Risk Management-The COSO Framework: A Primer and Tool For The Audit Committeemlce26No ratings yet

- Internal Control ConceptsDocument14 pagesInternal Control Conceptsmaleenda100% (1)

- Aml Examination Manual PDFDocument170 pagesAml Examination Manual PDFMOKNo ratings yet

- ParmalatDocument60 pagesParmalatAyesha MumtazNo ratings yet

- Fraud RiskDocument56 pagesFraud RiskJoman CorderoNo ratings yet

- Internal Control Policy (1) AustraliaDocument8 pagesInternal Control Policy (1) AustraliabulmezNo ratings yet

- Practice Aid: Enterprise Risk Management: Guidance For Practical Implementation and Assessment, 2018From EverandPractice Aid: Enterprise Risk Management: Guidance For Practical Implementation and Assessment, 2018No ratings yet

- Segregation of FunctionsDocument2 pagesSegregation of FunctionsHelarie RoaringNo ratings yet

- Fraud & MisrepresentationDocument11 pagesFraud & MisrepresentationApoorv SrivastavaNo ratings yet

- Forgery S (463) & S (474) F IPCDocument8 pagesForgery S (463) & S (474) F IPCRajeshwari MgNo ratings yet

- Albrecht 4e Student CH 01Document11 pagesAlbrecht 4e Student CH 01Qorry Aini HaniNo ratings yet

- 2009-01-14Document16 pages2009-01-14Tufts DailyNo ratings yet

- Is Unethical Decision More A Function of Individual Choice or Decision Maker's Work EnvironmentDocument18 pagesIs Unethical Decision More A Function of Individual Choice or Decision Maker's Work Environmentapi-19464015No ratings yet

- Case Study - Fake AccountsDocument1 pageCase Study - Fake Accountsdhruva KumarNo ratings yet

- Yujing ZhangDocument10 pagesYujing Zhangpaulfarrell1895No ratings yet

- FRAUDSDocument8 pagesFRAUDSChitra SalianNo ratings yet

- Free Consent - FRAUD: Under Indian Contract Act 1872Document2 pagesFree Consent - FRAUD: Under Indian Contract Act 1872SEKANISH KALPANA ANo ratings yet

- David Cortez Marshall JR Case SummaryDocument5 pagesDavid Cortez Marshall JR Case SummaryWLTXNo ratings yet

- Government Whore Sheri Polster Chappell On TrialDocument6 pagesGovernment Whore Sheri Polster Chappell On TrialJudicial_FraudNo ratings yet

- Test 7 PDFDocument6 pagesTest 7 PDFShahab ShafiNo ratings yet

- Group 01-Bidding LawDocument5 pagesGroup 01-Bidding Lawlengocanh252002No ratings yet

- Dynamite CatalogDocument11 pagesDynamite CatalogsirneeravNo ratings yet

- Commerce and Agriculture Lien AnnaDocument4 pagesCommerce and Agriculture Lien Annalerosenoir100% (2)

- Identity Theft WebquestDocument2 pagesIdentity Theft Webquestapi-256416574No ratings yet

- Case1 WhodunitDocument5 pagesCase1 WhodunitCj AquinoNo ratings yet

- Sun Life Canada Vs Ma. Daisy Et AlDocument2 pagesSun Life Canada Vs Ma. Daisy Et AlLouie SalazarNo ratings yet

- Bangladesh Heist - Corporate Criminal Liability For The Bank's Money Laundering ActivitiesDocument7 pagesBangladesh Heist - Corporate Criminal Liability For The Bank's Money Laundering ActivitiesMa FajardoNo ratings yet

- Anti-Corruption Compliance DeclarationDocument3 pagesAnti-Corruption Compliance DeclarationUchennaNo ratings yet

- Duane Lilien'Scomplaintfor Breach Ofcontract-Case NoDocument9 pagesDuane Lilien'Scomplaintfor Breach Ofcontract-Case NoADSJDNo ratings yet

- Romary UNC CommunicationDocument7 pagesRomary UNC CommunicationAnonymous jeL70dsNo ratings yet

- 143 Tax - Republic of The Phil v. GMCC United Development Corporation, G.R. No. 191856, 07 December 2016Document1 page143 Tax - Republic of The Phil v. GMCC United Development Corporation, G.R. No. 191856, 07 December 2016Brandon BanasanNo ratings yet

- NOTICE For InfringenmentDocument1 pageNOTICE For Infringenmentniveditafinleaf1No ratings yet

Download as ppt, pdf, or txt

You might also like

- ERM ChecklistDocument4 pagesERM Checklistaqsa_munir100% (1)

- COunter Affidavit EstafaDocument7 pagesCOunter Affidavit EstafaCheChe89% (19)

- GOVERNANCEDocument2 pagesGOVERNANCENour Aira Nao50% (2)

- Mastering Internal Controls TestbankDocument6 pagesMastering Internal Controls TestbankLade PalkanNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Auditng External Business RelationshipsDocument19 pagesAuditng External Business RelationshipsFernando Ernesto CabralNo ratings yet

- Victor Lustig3 PDFDocument5 pagesVictor Lustig3 PDFShiv Mani NdrNo ratings yet

- Forensic and Investigative AccountingDocument51 pagesForensic and Investigative AccountingNarendra Sengupta100% (5)

- Ethics, Fraud, and Internal Control: Presented byDocument40 pagesEthics, Fraud, and Internal Control: Presented byALMA MORENANo ratings yet

- Internal Control System of A Bank (Dutch Bangla Bank Limited) .Document42 pagesInternal Control System of A Bank (Dutch Bangla Bank Limited) .Tasmia100% (1)

- Ethics Fraud Schemes and Fraud DetectionDocument31 pagesEthics Fraud Schemes and Fraud DetectionJosephine CristajuneNo ratings yet

- Internal Audit Stakeholder Management and The Three Lines of Defense Slide DeckDocument12 pagesInternal Audit Stakeholder Management and The Three Lines of Defense Slide DeckSheyam SelvarajNo ratings yet

- Fraud Examination, 3E: Chapter 1: The Nature of FraudDocument25 pagesFraud Examination, 3E: Chapter 1: The Nature of Fraudpeaceajah100% (1)

- Ethics, Fraud, and Internal ControlDocument22 pagesEthics, Fraud, and Internal ControlsariNo ratings yet

- CH 12 Fraud and ErrorDocument28 pagesCH 12 Fraud and ErrorJoyce Anne GarduqueNo ratings yet

- Impact and Likelihood ScalesDocument3 pagesImpact and Likelihood ScalesRhea SimoneNo ratings yet

- Internal Control-Integrated FrameworkDocument34 pagesInternal Control-Integrated FrameworkInternational Consortium on Governmental Financial Management100% (1)

- Fraud at The Engagement Level: Expositor: Javier BecerraDocument11 pagesFraud at The Engagement Level: Expositor: Javier BecerraWalter Córdova MacedoNo ratings yet

- C Hap Ter 1 3 Overviewof Internal ControlDocument53 pagesC Hap Ter 1 3 Overviewof Internal ControlMariel Rasco100% (1)

- Fraud Position StatementDocument4 pagesFraud Position StatementsenoltoygarNo ratings yet

- FRAUDDocument3 pagesFRAUDprincess manlangitNo ratings yet

- COSO Framework Components and Related Principles: ExhibitDocument1 pageCOSO Framework Components and Related Principles: ExhibitRajat MathurNo ratings yet

- Fraud - Internal Auditing PDFDocument4 pagesFraud - Internal Auditing PDFJaJ08No ratings yet

- The 17 COSO Internal Control PrinciplesDocument7 pagesThe 17 COSO Internal Control Principleseskelapamudah enakNo ratings yet

- Fraud Indicators AuditorsDocument35 pagesFraud Indicators AuditorsMutabarKhanNo ratings yet

- ACC 420 The Fraud Triangle TheoryDocument2 pagesACC 420 The Fraud Triangle TheoryIfemide50% (2)

- Fraud Risk Management ProgramDocument68 pagesFraud Risk Management Programaa yudhoNo ratings yet

- 04 - Fraud Risk Management A Guide To GOOD PRACTICEDocument48 pages04 - Fraud Risk Management A Guide To GOOD PRACTICEEd Gonzales GonzalesNo ratings yet

- COSO FrameworkDocument0 pagesCOSO FrameworkCynthia StoneNo ratings yet

- Checklist For Evaluating Internal Controls ACC 544 Amanda SmithDocument8 pagesChecklist For Evaluating Internal Controls ACC 544 Amanda SmithAmanda GilbertNo ratings yet

- Internal Controls 101Document25 pagesInternal Controls 101Arcee Orcullo100% (1)

- Corporate GovernanceDocument47 pagesCorporate GovernanceShivani100% (1)

- Chapter 1 - CISDocument37 pagesChapter 1 - CISMaeNeth Gullan100% (1)

- Fraud PaperDocument80 pagesFraud Papernasir_m68No ratings yet

- Test of Controls For Some Major ActivitiesDocument22 pagesTest of Controls For Some Major ActivitiesMohsin RazaNo ratings yet

- Internal Control Self Assessment QuestionnaireDocument4 pagesInternal Control Self Assessment QuestionnaireHime Silhouette Gabriel100% (1)

- COSO Fraud Risk Management Guide Executive SummaryDocument13 pagesCOSO Fraud Risk Management Guide Executive SummarymohamedciaNo ratings yet

- PG Engagement Planning Assessing Fraud RisksDocument23 pagesPG Engagement Planning Assessing Fraud RisksRoland Val100% (1)

- Fraud Risk AssessmentDocument32 pagesFraud Risk AssessmentArturoNo ratings yet

- WorldCom Fraud PPT (Accounting Learning)Document12 pagesWorldCom Fraud PPT (Accounting Learning)蒲睿灵No ratings yet

- Fraud Risk Assessment - HandoutsDocument22 pagesFraud Risk Assessment - Handoutsrubel_nsuNo ratings yet

- The Marketing Finance Interface: Cgma ReportDocument48 pagesThe Marketing Finance Interface: Cgma ReportChristie RochaNo ratings yet

- Good AuditorDocument20 pagesGood AuditorBertu NatanaNo ratings yet

- Internal Controls and ERPDocument5 pagesInternal Controls and ERPapi-3748088No ratings yet

- 3 2018 L8 Gov.,Risk Management, ComplianceDocument13 pages3 2018 L8 Gov.,Risk Management, ComplianceTing Phin Yuan100% (1)

- Co So Enterprise Risk Management FrameworkDocument2 pagesCo So Enterprise Risk Management FrameworkasifsubhanNo ratings yet

- Solution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atDocument35 pagesSolution Manual For Auditing A Business Risk Approach 8th Edition by Rittenburg Complete Downloadable File atmichelle100% (1)

- Fraud-Tree SchemesDocument13 pagesFraud-Tree SchemessulthanhakimNo ratings yet

- Consideration of Internal ControlDocument69 pagesConsideration of Internal Controlmah loveNo ratings yet

- 2015 Leveraging COSO 3LODDocument32 pages2015 Leveraging COSO 3LODalfonsodzibNo ratings yet

- Fraud Risk FormDocument2 pagesFraud Risk FormShelvy SilviaNo ratings yet

- Simplified Sample Entity Level Control Matrices ImpDocument7 pagesSimplified Sample Entity Level Control Matrices ImpAqeelAhmadNo ratings yet

- 3-YR Internal Audit PlanDocument9 pages3-YR Internal Audit PlanJb LavariasNo ratings yet

- Bachelor of Science in Accountancy: GRC 2001: Introduction To Corporate GovernanceDocument2 pagesBachelor of Science in Accountancy: GRC 2001: Introduction To Corporate GovernanceJherryMigLazaroSevilla100% (9)

- Enterprise Risk Management-The COSO Framework: A Primer and Tool For The Audit CommitteeDocument12 pagesEnterprise Risk Management-The COSO Framework: A Primer and Tool For The Audit Committeemlce26No ratings yet

- Internal Control ConceptsDocument14 pagesInternal Control Conceptsmaleenda100% (1)

- Aml Examination Manual PDFDocument170 pagesAml Examination Manual PDFMOKNo ratings yet

- ParmalatDocument60 pagesParmalatAyesha MumtazNo ratings yet

- Fraud RiskDocument56 pagesFraud RiskJoman CorderoNo ratings yet

- Internal Control Policy (1) AustraliaDocument8 pagesInternal Control Policy (1) AustraliabulmezNo ratings yet

- Practice Aid: Enterprise Risk Management: Guidance For Practical Implementation and Assessment, 2018From EverandPractice Aid: Enterprise Risk Management: Guidance For Practical Implementation and Assessment, 2018No ratings yet

- Segregation of FunctionsDocument2 pagesSegregation of FunctionsHelarie RoaringNo ratings yet

- Fraud & MisrepresentationDocument11 pagesFraud & MisrepresentationApoorv SrivastavaNo ratings yet

- Forgery S (463) & S (474) F IPCDocument8 pagesForgery S (463) & S (474) F IPCRajeshwari MgNo ratings yet

- Albrecht 4e Student CH 01Document11 pagesAlbrecht 4e Student CH 01Qorry Aini HaniNo ratings yet

- 2009-01-14Document16 pages2009-01-14Tufts DailyNo ratings yet

- Is Unethical Decision More A Function of Individual Choice or Decision Maker's Work EnvironmentDocument18 pagesIs Unethical Decision More A Function of Individual Choice or Decision Maker's Work Environmentapi-19464015No ratings yet

- Case Study - Fake AccountsDocument1 pageCase Study - Fake Accountsdhruva KumarNo ratings yet

- Yujing ZhangDocument10 pagesYujing Zhangpaulfarrell1895No ratings yet

- FRAUDSDocument8 pagesFRAUDSChitra SalianNo ratings yet

- Free Consent - FRAUD: Under Indian Contract Act 1872Document2 pagesFree Consent - FRAUD: Under Indian Contract Act 1872SEKANISH KALPANA ANo ratings yet

- David Cortez Marshall JR Case SummaryDocument5 pagesDavid Cortez Marshall JR Case SummaryWLTXNo ratings yet

- Government Whore Sheri Polster Chappell On TrialDocument6 pagesGovernment Whore Sheri Polster Chappell On TrialJudicial_FraudNo ratings yet

- Test 7 PDFDocument6 pagesTest 7 PDFShahab ShafiNo ratings yet

- Group 01-Bidding LawDocument5 pagesGroup 01-Bidding Lawlengocanh252002No ratings yet

- Dynamite CatalogDocument11 pagesDynamite CatalogsirneeravNo ratings yet

- Commerce and Agriculture Lien AnnaDocument4 pagesCommerce and Agriculture Lien Annalerosenoir100% (2)

- Identity Theft WebquestDocument2 pagesIdentity Theft Webquestapi-256416574No ratings yet

- Case1 WhodunitDocument5 pagesCase1 WhodunitCj AquinoNo ratings yet

- Sun Life Canada Vs Ma. Daisy Et AlDocument2 pagesSun Life Canada Vs Ma. Daisy Et AlLouie SalazarNo ratings yet

- Bangladesh Heist - Corporate Criminal Liability For The Bank's Money Laundering ActivitiesDocument7 pagesBangladesh Heist - Corporate Criminal Liability For The Bank's Money Laundering ActivitiesMa FajardoNo ratings yet

- Anti-Corruption Compliance DeclarationDocument3 pagesAnti-Corruption Compliance DeclarationUchennaNo ratings yet

- Duane Lilien'Scomplaintfor Breach Ofcontract-Case NoDocument9 pagesDuane Lilien'Scomplaintfor Breach Ofcontract-Case NoADSJDNo ratings yet

- Romary UNC CommunicationDocument7 pagesRomary UNC CommunicationAnonymous jeL70dsNo ratings yet

- 143 Tax - Republic of The Phil v. GMCC United Development Corporation, G.R. No. 191856, 07 December 2016Document1 page143 Tax - Republic of The Phil v. GMCC United Development Corporation, G.R. No. 191856, 07 December 2016Brandon BanasanNo ratings yet

- NOTICE For InfringenmentDocument1 pageNOTICE For Infringenmentniveditafinleaf1No ratings yet