Download as pptx, pdf, or txt

You might also like

- Sample International Arbitration ClaimDocument38 pagesSample International Arbitration ClaimSantiago Cueto100% (2)

- NTC Water Leaks Team 19-20 June2013Document63 pagesNTC Water Leaks Team 19-20 June2013Alick ChipetaNo ratings yet

- Economic Crisis of 1991:: Root Causes, Consequences and Road To RecoveryDocument13 pagesEconomic Crisis of 1991:: Root Causes, Consequences and Road To RecoverymishikaNo ratings yet

- India On The MoveDocument15 pagesIndia On The MoveInsha RahmanNo ratings yet

- Quebrada Blanca Phase 2 - Reporte Tecnico PDFDocument222 pagesQuebrada Blanca Phase 2 - Reporte Tecnico PDFtjuang garces martinezNo ratings yet

- Commodity Prices and FP in LAC, Sinnott 2009Document41 pagesCommodity Prices and FP in LAC, Sinnott 2009Sui-Jade HoNo ratings yet

- Balance of Payment and Balance of Trade of PakistanDocument37 pagesBalance of Payment and Balance of Trade of PakistanAndeela Riaz100% (3)

- Economic Environment in International BusinessDocument26 pagesEconomic Environment in International BusinessAshish kumar ThapaNo ratings yet

- Qatar Business GuideDocument95 pagesQatar Business GuideJessie ColeNo ratings yet

- Balance of PaymentDocument6 pagesBalance of PaymentpalaksfojdarNo ratings yet

- Patterns and Volume of TradeDocument17 pagesPatterns and Volume of TradeqiankeyangNo ratings yet

- Global Financial CrisisDocument31 pagesGlobal Financial CrisisF-10No ratings yet

- The Trade Balance of Pakistan and Its Impact On Exchange Rate of Pakistan: A Research ReportDocument10 pagesThe Trade Balance of Pakistan and Its Impact On Exchange Rate of Pakistan: A Research ReportzainabkhanNo ratings yet

- Nature of Modern Business: Consumer For A Profit. These Activities Satisfy Society's Needs, Desires and BringDocument15 pagesNature of Modern Business: Consumer For A Profit. These Activities Satisfy Society's Needs, Desires and BringAVIJIT SARKARNo ratings yet

- India's Balance of Payments-Areas To ImporveDocument13 pagesIndia's Balance of Payments-Areas To ImporveUtkarsh RajNo ratings yet

- Trade As An Engine For Growth-Developing EconomiesDocument57 pagesTrade As An Engine For Growth-Developing EconomiesAmit BehalNo ratings yet

- 2013 05 Doing Business MineriaDocument0 pages2013 05 Doing Business Mineriaumut2000No ratings yet

- Balance of PaymentsDocument24 pagesBalance of PaymentsHitesh TakhtaniNo ratings yet

- MK006 - Module 2 - PPT 1Document43 pagesMK006 - Module 2 - PPT 1NICOLE YHNA LAGUISMANo ratings yet

- Yeni Microsoft Office Word DocumentDocument2 pagesYeni Microsoft Office Word DocumentzulkadirNo ratings yet

- ED (1) AssignmentDocument21 pagesED (1) AssignmentSalman ZaiNo ratings yet

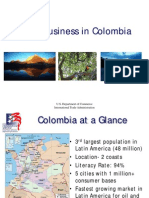

- Doing Business in Colombia September2012Document29 pagesDoing Business in Colombia September2012acmartineziiNo ratings yet

- Global Trade and Its GrowthDocument39 pagesGlobal Trade and Its GrowthKareena Bahl100% (1)

- International Finance: Lectures 4 October 7, 2020Document17 pagesInternational Finance: Lectures 4 October 7, 2020ifrah ahmadNo ratings yet

- External SectorDocument38 pagesExternal SectorSagar DasNo ratings yet

- 108INUNIT5A The Foreign Trade of IndiaDocument55 pages108INUNIT5A The Foreign Trade of IndiaDr. Rakesh BhatiNo ratings yet

- History of Foreign TradeDocument33 pagesHistory of Foreign TradeshantanuNo ratings yet

- Saravanan India's Foreign TradeDocument25 pagesSaravanan India's Foreign TradeSaravanan TkNo ratings yet

- GDB Eco501Document2 pagesGDB Eco501Hina Rashed WaraichNo ratings yet

- Recent Trends in India's Foreign TradeDocument28 pagesRecent Trends in India's Foreign TradeVivek Mishra0% (2)

- 213Document55 pages213Kshipra DhindawNo ratings yet

- India's External SectorDocument22 pagesIndia's External SectorTanisha DhavalpureNo ratings yet

- Relationship Between Pakistan ' S Fiscal & Trade DecifitDocument18 pagesRelationship Between Pakistan ' S Fiscal & Trade Decifitdarky159No ratings yet

- Sustainability of India's Growth RateDocument18 pagesSustainability of India's Growth RateRinky PaulNo ratings yet

- GlobalizationDocument61 pagesGlobalizationKritika MehraNo ratings yet

- GCI-Bulletin - 2020 China LatamDocument20 pagesGCI-Bulletin - 2020 China LatamPablo Fernando Suárez RubioNo ratings yet

- PE CH 5Document12 pagesPE CH 5Annam InayatNo ratings yet

- ECO102Document14 pagesECO102Rashedul RasNo ratings yet

- Effects of India's Growth On The Global Economy and EnvironmentDocument25 pagesEffects of India's Growth On The Global Economy and EnvironmentPankaj YadavNo ratings yet

- By, Neha DokaniaDocument61 pagesBy, Neha DokaniaMatthew FerrellNo ratings yet

- Department of Economics: National University of Modern LanguagesDocument12 pagesDepartment of Economics: National University of Modern LanguagesMaaz SherazNo ratings yet

- Tips To The President Part1Document1 pageTips To The President Part1gmcolinaNo ratings yet

- Report On Risk ProfileDocument16 pagesReport On Risk ProfilehuraldayNo ratings yet

- Trade Theory and DevelopmentDocument28 pagesTrade Theory and Developmentwhatsup_11798No ratings yet

- India's BOP and Foreign ExchangeDocument7 pagesIndia's BOP and Foreign ExchangeSuria UnnikrishnanNo ratings yet

- 1 MainDocument89 pages1 MainSandeep SandyNo ratings yet

- Business Intelligence 20220822Document69 pagesBusiness Intelligence 20220822Alejandro MaguerNo ratings yet

- The Rise of Middle Kingdoms: Emerging Economies in Global TradeDocument25 pagesThe Rise of Middle Kingdoms: Emerging Economies in Global Tradepaul nelsonNo ratings yet

- Jep 26 2 41Document30 pagesJep 26 2 41Ace NebulaNo ratings yet

- Development Unit 3.1Document16 pagesDevelopment Unit 3.1VAIBHAV VERMANo ratings yet

- Overview of Nigerian EconomyDocument9 pagesOverview of Nigerian EconomyGundeep SinghNo ratings yet

- Foreign Trade - BOPDocument54 pagesForeign Trade - BOPDEVANSH KOTHARINo ratings yet

- Bahia Basics Facts: Predictability, Good Regulation and Respect For ContractsDocument38 pagesBahia Basics Facts: Predictability, Good Regulation and Respect For ContractsRomeu TemporalNo ratings yet

- Import - Export Policy of IndiaDocument25 pagesImport - Export Policy of IndiasshreyasNo ratings yet

- China Global PDFDocument16 pagesChina Global PDFUrmi Mehta100% (1)

- Globalization and India: Iipm SMDocument24 pagesGlobalization and India: Iipm SMRAJIV SINGHNo ratings yet

- Colombia's Oil & Gas Update Quarter 1 2011: Gonzalez Consulting International CorporationDocument5 pagesColombia's Oil & Gas Update Quarter 1 2011: Gonzalez Consulting International Corporationpgonzalez171No ratings yet

- BNFN 304 CH 1Document13 pagesBNFN 304 CH 1naqvi1974No ratings yet

- Fundemental AnalysisDocument34 pagesFundemental AnalysisAishwarya SoundaryaNo ratings yet

- What Is International Economics About?Document19 pagesWhat Is International Economics About?Bachuu HossanNo ratings yet

- BRIEF: Gas Sector Investment Policy: The Latin American ExperienceDocument4 pagesBRIEF: Gas Sector Investment Policy: The Latin American ExperienceELLA ProgrammeNo ratings yet

- Role of Remittances and Their Inflow in Pakistan From 1976-2008Document21 pagesRole of Remittances and Their Inflow in Pakistan From 1976-2008Maliha KhanNo ratings yet

- IBF-Week 1-Basics of Business Finance & Importance of Financial DecisionsDocument41 pagesIBF-Week 1-Basics of Business Finance & Importance of Financial DecisionsMohammad MoosaNo ratings yet

- Chapter 1 and 2Document6 pagesChapter 1 and 2Mohammad MoosaNo ratings yet

- IBF Lecture 13-Working Capital-Managing Short-Term AssetsDocument60 pagesIBF Lecture 13-Working Capital-Managing Short-Term AssetsMohammad MoosaNo ratings yet

- Data and Decisions AssignmentDocument7 pagesData and Decisions AssignmentMohammad MoosaNo ratings yet

- Ak PDFDocument2 pagesAk PDFMohammad MoosaNo ratings yet

- Understanding Psychology Chapter 1Document3 pagesUnderstanding Psychology Chapter 1Mohammad MoosaNo ratings yet

- HRM Practices For Employee Retention: An Analysis of Pakistani CompaniesDocument10 pagesHRM Practices For Employee Retention: An Analysis of Pakistani CompaniesMohammad MoosaNo ratings yet

- Chapter 3Document2 pagesChapter 3Mohammad MoosaNo ratings yet

- Health Psychology: StressDocument40 pagesHealth Psychology: StressMohammad MoosaNo ratings yet

- WWW - Studyguide.pk: PhysicsDocument16 pagesWWW - Studyguide.pk: PhysicsMohammad MoosaNo ratings yet

- MKT 301 MBR: ConsolidationDocument28 pagesMKT 301 MBR: ConsolidationMohammad MoosaNo ratings yet

- Assignment 4 International TradeDocument7 pagesAssignment 4 International TradeMohammad MoosaNo ratings yet

- Building Careers and Writing ResumesDocument4 pagesBuilding Careers and Writing ResumesMohammad MoosaNo ratings yet

- 8 Employee Turnover and Retention StrategiesDocument8 pages8 Employee Turnover and Retention StrategiesMohammad MoosaNo ratings yet

- Effective MeetingsDocument3 pagesEffective MeetingsMohammad MoosaNo ratings yet

- The Talent Management Practices For Employee Job Retention - A Phenomenological Investigation of Private Sector Banking Organizations in PakistanDocument22 pagesThe Talent Management Practices For Employee Job Retention - A Phenomenological Investigation of Private Sector Banking Organizations in PakistanMohammad MoosaNo ratings yet

- Sales Management: Session 3 - Organizational Strategy & Sales Role - Sales Planning & Framework Umer UsmaniDocument24 pagesSales Management: Session 3 - Organizational Strategy & Sales Role - Sales Planning & Framework Umer UsmaniMohammad MoosaNo ratings yet

- Process CostingDocument83 pagesProcess CostingMohammad MoosaNo ratings yet

- Business Messages ObDocument5 pagesBusiness Messages ObMohammad MoosaNo ratings yet

- Bop Assignment MIPDocument7 pagesBop Assignment MIPMohammad MoosaNo ratings yet

- Ibf Chapter 6Document2 pagesIbf Chapter 6Mohammad MoosaNo ratings yet

- Dividend PolicyDocument13 pagesDividend PolicyMohammad MoosaNo ratings yet

- Mexico's EconomyDocument8 pagesMexico's EconomyMohammad MoosaNo ratings yet

- Ibf Lecture 3Document3 pagesIbf Lecture 3Mohammad MoosaNo ratings yet

- Exploration Southern - Los ChancasDocument2 pagesExploration Southern - Los ChancasJulio Vento GlaveNo ratings yet

- Radical Innovation Liberating The Potential of TOC in Mining 2019-05-15 Arrie V NiekerkDocument45 pagesRadical Innovation Liberating The Potential of TOC in Mining 2019-05-15 Arrie V NiekerkJelena FedurkoNo ratings yet

- Nagaland (Ownership and Transfer of Land and Its Resources) Act, 1990Document77 pagesNagaland (Ownership and Transfer of Land and Its Resources) Act, 1990Latest Laws TeamNo ratings yet

- Global MinigDocument28 pagesGlobal MinigJOSE0% (1)

- February 2021: The Indian Mining & Engineering JournalDocument36 pagesFebruary 2021: The Indian Mining & Engineering JournalAnurag TripathyNo ratings yet

- ShantaDocument20 pagesShantakisuwahhNo ratings yet

- Ground Vibrations and Fly RocksDocument7 pagesGround Vibrations and Fly Rocksanum razzaqNo ratings yet

- The Extractive Metallurgy of Zinc - by Roderick J. Sinclair: January 2006Document4 pagesThe Extractive Metallurgy of Zinc - by Roderick J. Sinclair: January 2006akshukNo ratings yet

- MBE-CMT Presentation PDFDocument38 pagesMBE-CMT Presentation PDFkselvan_1100% (1)

- Engineering Fundamentals An Introduction To Engineering Chapter 01Document31 pagesEngineering Fundamentals An Introduction To Engineering Chapter 01Ana ChavezNo ratings yet

- Fifth FormDocument46 pagesFifth FormMariah CampbellNo ratings yet

- AccuWeigh FlyerDocument2 pagesAccuWeigh FlyerJuan YdmeNo ratings yet

- CIC Gold ProspectusDocument104 pagesCIC Gold ProspectusFraserNo ratings yet

- MNO Investor Presentation 07 June 2023Document37 pagesMNO Investor Presentation 07 June 2023joseanselmoNo ratings yet

- This Content Downloaded From 13.234.254.191 On Sun, 27 Mar 2022 07:28:07 UTCDocument12 pagesThis Content Downloaded From 13.234.254.191 On Sun, 27 Mar 2022 07:28:07 UTCGunjan ChandavatNo ratings yet

- Means For Improvement of Production and Productivity in Indian Coal Mines - A Case StudyDocument12 pagesMeans For Improvement of Production and Productivity in Indian Coal Mines - A Case StudySatya LearnerNo ratings yet

- A Review of Open Cast Coal Mining in IndiaDocument62 pagesA Review of Open Cast Coal Mining in IndiaAbhiram ReddyNo ratings yet

- Carrying Capacity of Mines in Bellary District EMPRI 2007 09Document304 pagesCarrying Capacity of Mines in Bellary District EMPRI 2007 09Anna Basanth100% (1)

- Intrepid Explorer: Lowell, J. DavidDocument15 pagesIntrepid Explorer: Lowell, J. DavidSGA-UIS BucaramangaNo ratings yet

- Grade Estimation Using SurpacDocument58 pagesGrade Estimation Using SurpacBoukaré OuédraogoNo ratings yet

- CME538 Lecture 1 Slide 1Document122 pagesCME538 Lecture 1 Slide 1Siu Kai CheungNo ratings yet

- $EMTS - Seed Wave Modeling To Natural Caves Protection in Mining Operations - Carajas - ISEEDocument12 pages$EMTS - Seed Wave Modeling To Natural Caves Protection in Mining Operations - Carajas - ISEEJuan Carlos Aburto INo ratings yet

- Analysis of The State and Development of Vehicles Working in The QuarryDocument4 pagesAnalysis of The State and Development of Vehicles Working in The QuarryResearch ParkNo ratings yet

- 605-File Utama Naskah-1304-1-10-20181011Document7 pages605-File Utama Naskah-1304-1-10-20181011abang adekNo ratings yet

- Using Earths Resources Exam Practice GCSEDocument14 pagesUsing Earths Resources Exam Practice GCSEPaul GillNo ratings yet

- ChapterDocument16 pagesChapterSigitNo ratings yet

- L C M C: Epanto Onsolidated Ining OmpanyDocument53 pagesL C M C: Epanto Onsolidated Ining OmpanyPrincess GuiaNo ratings yet