Download as ppt, pdf, or txt

You might also like

- 108 PBM #2 Winter 2015 Part 2Document5 pages108 PBM #2 Winter 2015 Part 2Ray0% (1)

- A Project Report On LLPDocument10 pagesA Project Report On LLPPiyush Saraogi0% (1)

- Contract AssignmentDocument8 pagesContract AssignmentmitaliNo ratings yet

- An Overview of Limited Liability Partnership (LLP) in IndiaDocument4 pagesAn Overview of Limited Liability Partnership (LLP) in IndiaDeevanshu ShrivastavaNo ratings yet

- 5 THE LIMITED LIABILITY PARTNERSHIP ACT 2008 NavkarDocument7 pages5 THE LIMITED LIABILITY PARTNERSHIP ACT 2008 Navkarukka11008No ratings yet

- Accountany and Audit ProjectDocument24 pagesAccountany and Audit ProjectVikram AdityaNo ratings yet

- The Limited Liability Partnership ActDocument4 pagesThe Limited Liability Partnership ActGaurav Sharma100% (2)

- LLPDocument24 pagesLLPPrashant MauryaNo ratings yet

- The Limited LiabilityDocument17 pagesThe Limited LiabilityABINASHNo ratings yet

- Unique Id - Topic-Limited Liability Partnership: Balance Between Partnership and CompanyDocument8 pagesUnique Id - Topic-Limited Liability Partnership: Balance Between Partnership and CompanyUTKARSH MISHRANo ratings yet

- Limited Liability Partnership - Wikipedia PDFDocument51 pagesLimited Liability Partnership - Wikipedia PDFNAVAMY MRNo ratings yet

- Limited Liability PartnershipDocument19 pagesLimited Liability PartnershipKanan JainNo ratings yet

- Vishal, Sai April 17,2010 WWW - Pluggd.in, eHOW Blog: Presented By-Date - SourceDocument11 pagesVishal, Sai April 17,2010 WWW - Pluggd.in, eHOW Blog: Presented By-Date - Sourcewelcome2jungleNo ratings yet

- Limited Liability Partnership Act, (LLP) 2008Document17 pagesLimited Liability Partnership Act, (LLP) 2008shankyagar100% (1)

- The Limited Liability Partnership Act, 2008Document8 pagesThe Limited Liability Partnership Act, 2008Sushant TaleNo ratings yet

- 2 Limited Liability Partnership 2008 Scanner Nitika BachawatDocument16 pages2 Limited Liability Partnership 2008 Scanner Nitika BachawatgayathriNo ratings yet

- LLPARTNERSHIPDocument6 pagesLLPARTNERSHIPAltafMakaiNo ratings yet

- Assigment On LLPDocument50 pagesAssigment On LLPDikshant GopaliaNo ratings yet

- India LLP Taxguru - inDocument7 pagesIndia LLP Taxguru - inJatan HundalNo ratings yet

- Operations Research MCQ PDFDocument17 pagesOperations Research MCQ PDFDipak Mahalik100% (1)

- Limited Liability Partnership Act - 2008 2Document14 pagesLimited Liability Partnership Act - 2008 2Omkar NakasheNo ratings yet

- Limited Liability Partnership Act, 2008: Concept of LLPDocument3 pagesLimited Liability Partnership Act, 2008: Concept of LLPridhi soodNo ratings yet

- Limited Liability Partnership ActDocument45 pagesLimited Liability Partnership Act2022474209.ayushNo ratings yet

- Conversion Partnership PVT LTD LLPDocument60 pagesConversion Partnership PVT LTD LLPAdarsh VermaNo ratings yet

- Law LLPDocument19 pagesLaw LLPOshi KeshariNo ratings yet

- 8850950388/Notes/The Limited Liability Partnership Act and Partnership Act NotesDocument11 pages8850950388/Notes/The Limited Liability Partnership Act and Partnership Act Notesvani14iipsNo ratings yet

- LLP Final Project by Jashan WarraichDocument28 pagesLLP Final Project by Jashan WarraichJashanNo ratings yet

- Law Bachawat Scanner LLPDocument18 pagesLaw Bachawat Scanner LLPgvramani51233No ratings yet

- Business Law ProjectDocument16 pagesBusiness Law Project36 Unzala noorNo ratings yet

- Limited Liability PartnershipDocument18 pagesLimited Liability PartnershipRachit MunjalNo ratings yet

- Unit IVDocument57 pagesUnit IVManisha RaiNo ratings yet

- LLP Group A6Document10 pagesLLP Group A6sayansaha95No ratings yet

- The LLP ActDocument13 pagesThe LLP ActshanumanuranuNo ratings yet

- 1 LLP Darshan Khare QADocument7 pages1 LLP Darshan Khare QANiharika PayasiNo ratings yet

- Module Iv (Special Contracts)Document23 pagesModule Iv (Special Contracts)iamwasim43No ratings yet

- Individual Assignments For EconomicsDocument17 pagesIndividual Assignments For EconomicsGetachew ZelekeNo ratings yet

- LLP ACT New AmendmentsDocument8 pagesLLP ACT New Amendmentsdegevop428No ratings yet

- Esu Business Lawchp 5Document56 pagesEsu Business Lawchp 5newaybeyene5No ratings yet

- Business Law - Module - IVDocument21 pagesBusiness Law - Module - IVdrashti vaishnavNo ratings yet

- Limited Liability Partnership: Overview of LLP in IndiaDocument3 pagesLimited Liability Partnership: Overview of LLP in IndiaIMRAN ALAMNo ratings yet

- Limited Liabality Partnership Act 2017Document8 pagesLimited Liabality Partnership Act 2017Kashir ZamanNo ratings yet

- Scanner For Ca Foundation MAY' 19Document17 pagesScanner For Ca Foundation MAY' 19dbNo ratings yet

- Research PaperDocument9 pagesResearch PaperIsha lohaniNo ratings yet

- Limited Liability Partnership (LLP) & PartnershipDocument9 pagesLimited Liability Partnership (LLP) & PartnershipAnkita SrivastavaNo ratings yet

- School of Law, Narsee Monjee Institute of Management Studies, BangaloreDocument17 pagesSchool of Law, Narsee Monjee Institute of Management Studies, BangaloreSAURABH SINGHNo ratings yet

- LLP or Private Limited CompanyDocument4 pagesLLP or Private Limited CompanyScholarNo ratings yet

- Limited Liability PartnershipDocument5 pagesLimited Liability PartnershipABHIJIT MAZUMDERNo ratings yet

- History of Limited Liability Partnership ActDocument37 pagesHistory of Limited Liability Partnership ActManinder Saini100% (2)

- Limited Liability Partnerships in KenyaDocument5 pagesLimited Liability Partnerships in KenyaStephen Mallowah100% (1)

- Introduction To Limited Liability Partnership (LLP) : - Tushar MittalDocument20 pagesIntroduction To Limited Liability Partnership (LLP) : - Tushar MittalBhavna AroraNo ratings yet

- Limited Liability Partnership - FAQDocument14 pagesLimited Liability Partnership - FAQtarun.mitra1985492350% (2)

- Analysis On LLPDocument25 pagesAnalysis On LLPanjalituli7587No ratings yet

- Law LLP PaperDocument6 pagesLaw LLP PaperGaurav ChopraNo ratings yet

- Handbook On Limited Liability Partnership Bill 2008Document58 pagesHandbook On Limited Liability Partnership Bill 2008shaqueeb nallamanduNo ratings yet

- Business Law PresentaionDocument8 pagesBusiness Law PresentaionSejal NakraNo ratings yet

- The Limited Liability Partnership ActDocument10 pagesThe Limited Liability Partnership ActIshwar MeenaNo ratings yet

- Lecture Topic 2 - (LLPDocument8 pagesLecture Topic 2 - (LLPKERK YONG QIN / UPMNo ratings yet

- Summary European Company LawDocument22 pagesSummary European Company LawAntonio BancicNo ratings yet

- The Limited Liability Partnership Act, 2008: Learning OutcomesDocument26 pagesThe Limited Liability Partnership Act, 2008: Learning OutcomesTechnical Mukul100% (1)

- Business Organizations: Outlines and Case Summaries: Law School Survival Guides, #10From EverandBusiness Organizations: Outlines and Case Summaries: Law School Survival Guides, #10No ratings yet

- Fidic Red Yellow Silver BooksDocument11 pagesFidic Red Yellow Silver Bookssilence_10007No ratings yet

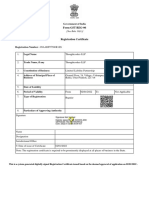

- GST Registration CertificateDocument3 pagesGST Registration Certificatedavid petersonNo ratings yet

- Companies Looking at Llps As New Holding WaysDocument5 pagesCompanies Looking at Llps As New Holding WaysGanesh ChhetriNo ratings yet

- Ede Chapter 1 PDFDocument25 pagesEde Chapter 1 PDFKunal AhiwaleNo ratings yet

- BBA Entrepreneurship DevelopmentDocument128 pagesBBA Entrepreneurship DevelopmentPek yyNo ratings yet

- By Anubha - Assignment of Business LawDocument10 pagesBy Anubha - Assignment of Business LawSubhradeep MajumderNo ratings yet

- R01Document2 pagesR01cutiemocha1100% (1)

- MIA Circular - LLP For Professional ServiceDocument3 pagesMIA Circular - LLP For Professional ServiceLynaNo ratings yet

- Doing - Business - in - India Nithish Desai PDFDocument146 pagesDoing - Business - in - India Nithish Desai PDFappao vidyasagarNo ratings yet

- viewNitPdf 3800015Document15 pagesviewNitPdf 3800015harikrishna007No ratings yet

- Corporate Laws - I (Ma'Am's PPTS)Document280 pagesCorporate Laws - I (Ma'Am's PPTS)Athisaya cgNo ratings yet

- Article - Admission of New Partner in LLPDocument2 pagesArticle - Admission of New Partner in LLPbadarivalivetiNo ratings yet

- In The Following Pages, You Will Find The Sample Chapter From The Book "Tulsian's Business Laws" by P.C. Tulsian & Bharat TulsianDocument13 pagesIn The Following Pages, You Will Find The Sample Chapter From The Book "Tulsian's Business Laws" by P.C. Tulsian & Bharat Tulsianantima shardaNo ratings yet

- TyBCom Unipune SyllabusDocument71 pagesTyBCom Unipune SyllabusSangitaNo ratings yet

- Accounting QuizDocument5 pagesAccounting QuizLloyd Lameon0% (1)

- A Business Organization Is An Individual or Group of People That Collaborate To Achieve Certain Commercial GoalsDocument6 pagesA Business Organization Is An Individual or Group of People That Collaborate To Achieve Certain Commercial GoalsAlexa MañalacNo ratings yet

- Press Release New Associates Wills and Enriquez (00756934)Document2 pagesPress Release New Associates Wills and Enriquez (00756934)Circuit MediaNo ratings yet

- Public Service - No Less A Public Service Because It May Incidentally Be A Means of LivelihoodDocument7 pagesPublic Service - No Less A Public Service Because It May Incidentally Be A Means of LivelihoodMarie Ann JoNo ratings yet

- Partnership in Business LawDocument5 pagesPartnership in Business LawJimmy LevisNo ratings yet

- Audit Committee Institute: Evaluation of Internal AuditorsDocument12 pagesAudit Committee Institute: Evaluation of Internal AuditorsAndre SENo ratings yet

- KPMG Budget - 2011Document102 pagesKPMG Budget - 2011anuragchogtuNo ratings yet

- Concurrent DelayDocument9 pagesConcurrent DelayMdms PayoeNo ratings yet

- Book 1Document140 pagesBook 1R P PrajapatiNo ratings yet

- Disposal Land Rules 1979 PDFDocument207 pagesDisposal Land Rules 1979 PDFKulveer SinghNo ratings yet

- Tender DocumentsDocument101 pagesTender DocumentsSharvari SankheNo ratings yet

- ABE Level 5 Diploma Unit Title: Principles of Business Law Learning OutcomeDocument14 pagesABE Level 5 Diploma Unit Title: Principles of Business Law Learning OutcomehosseinNo ratings yet

- Informatica v. ProtegrityDocument8 pagesInformatica v. ProtegrityPatent LitigationNo ratings yet

- Revenue From Contracts With Customers PDFDocument204 pagesRevenue From Contracts With Customers PDFHafeel MohamedNo ratings yet

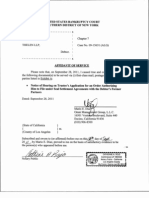

- 10000021260Document23 pages10000021260Chapter 11 DocketsNo ratings yet