Download as pptx, pdf, or txt

You might also like

- Module Assessment Answers - Group Accounts 2Document11 pagesModule Assessment Answers - Group Accounts 2John Philip L Concepcion100% (1)

- BSA2BQuiz 3Document19 pagesBSA2BQuiz 3Monica Enrico0% (1)

- Intro To Financial Accounting Horngen 11e Chapter2 SolutionsDocument41 pagesIntro To Financial Accounting Horngen 11e Chapter2 SolutionsArena Arena100% (7)

- Cash and Cash Equivalents - ExampleDocument1 pageCash and Cash Equivalents - ExampleMark Domingo MendozaNo ratings yet

- Assessing Earnings Quality at NuwareDocument7 pagesAssessing Earnings Quality at Nuwaresatherbd21100% (4)

- CORPORATIONEXERCISES28PROBLEMS29ONORGANIZATION21FEB21Document9 pagesCORPORATIONEXERCISES28PROBLEMS29ONORGANIZATION21FEB21Jasmine ActaNo ratings yet

- Consolidation Review QuestionsDocument9 pagesConsolidation Review QuestionsErnest100% (1)

- Consolidated FS QuizDocument4 pagesConsolidated FS QuizCattleya0% (2)

- Chapter 11 - She Part 2Document4 pagesChapter 11 - She Part 2XienaNo ratings yet

- Account P S at Book Value S at Fair ValueDocument7 pagesAccount P S at Book Value S at Fair ValueAditya Agung SatrioNo ratings yet

- AFR - Question BankDocument31 pagesAFR - Question BankDownloder UwambajimanaNo ratings yet

- ABC Park&Strand CorporationDocument1 pageABC Park&Strand CorporationAlyzaNo ratings yet

- Business Combination Q4Document2 pagesBusiness Combination Q4Sweet EmmeNo ratings yet

- Module 2 Business Combination ProportionateDocument3 pagesModule 2 Business Combination ProportionateasdasdaNo ratings yet

- ASSIGNMENT CH 23 PROB 9 To 24Document5 pagesASSIGNMENT CH 23 PROB 9 To 24Georgina Francheska RamirezNo ratings yet

- BS 420 Exam QuestionsDocument17 pagesBS 420 Exam QuestionsPrince Daniels TutorNo ratings yet

- Finman 108 (Quiz 4) ...Document6 pagesFinman 108 (Quiz 4) ...CHARRYSAH TABAOSARESNo ratings yet

- Latihan Soal Advanced Accounting Chapter 3Document18 pagesLatihan Soal Advanced Accounting Chapter 3JulyaniNo ratings yet

- Kunci Jawaban Soal Latihan Pertemuan 6Document6 pagesKunci Jawaban Soal Latihan Pertemuan 6aprian caesarioNo ratings yet

- Chapter+3+Consolidation+at+aquisition+date+ PART+2Document16 pagesChapter+3+Consolidation+at+aquisition+date+ PART+2Christi ClarkNo ratings yet

- Preparation of FS To Post-Closing TB - Marge Orie Problem SolutionDocument32 pagesPreparation of FS To Post-Closing TB - Marge Orie Problem SolutionAngel Yohaiña Ramos SantiagoNo ratings yet

- balancesheet (16)Document5 pagesbalancesheet (16)abhisekNo ratings yet

- Advanced FR-Review Questions-Complex GroupsDocument5 pagesAdvanced FR-Review Questions-Complex GroupsBilliee ButccherNo ratings yet

- Partnership Operations Part 2Document14 pagesPartnership Operations Part 2Nerish PlazaNo ratings yet

- Bus - Com - 1Document2 pagesBus - Com - 1Blythe AzodnemNo ratings yet

- Session 7 and 7a SupplemenDocument10 pagesSession 7 and 7a Supplemenkhadija arifNo ratings yet

- BS 420 - 16TH MayDocument5 pagesBS 420 - 16TH MayPrince Daniels TutorNo ratings yet

- Investment in Associate and Joint VentureDocument5 pagesInvestment in Associate and Joint VenturedumpyforhimNo ratings yet

- Partnership OperationsDocument8 pagesPartnership OperationsNerish PlazaNo ratings yet

- Contoh Soal Mutual Holding Pendekatan KonvensionalDocument10 pagesContoh Soal Mutual Holding Pendekatan KonvensionalPutri ShaniaNo ratings yet

- ShortproblemDocument2 pagesShortproblemLabLab ChattoNo ratings yet

- WEEK 6-7 ULO A, B, C Answer KeyDocument4 pagesWEEK 6-7 ULO A, B, C Answer Keyzee abadilla100% (1)

- Past Paper Question 1 With AnswerDocument6 pagesPast Paper Question 1 With AnswerChitradevi RamooNo ratings yet

- WP CHP 6Document11 pagesWP CHP 6chrisdtfsNo ratings yet

- BSA 315 Accounting For Business CombinationDocument5 pagesBSA 315 Accounting For Business CombinationJeth MahusayNo ratings yet

- Name: DEC. 17, 2020 Buscom ScoreDocument4 pagesName: DEC. 17, 2020 Buscom ScoreErica DaprosaNo ratings yet

- Chapter FIVEDocument14 pagesChapter FIVEannisaNo ratings yet

- Worksheet Master BudgetDocument6 pagesWorksheet Master BudgetRUPIKA R GNo ratings yet

- Review Midterm (MyAnswers)Document30 pagesReview Midterm (MyAnswers)Jester SarabiaNo ratings yet

- Multiple Choices - Computational Answer KeyDocument4 pagesMultiple Choices - Computational Answer KeyAleah kay BalontongNo ratings yet

- Consolidation of Financial Statements at Acquisition DateDocument4 pagesConsolidation of Financial Statements at Acquisition DateShiela Mae RedobleNo ratings yet

- CFASDocument3 pagesCFASataydeyessaNo ratings yet

- BBA Program Spring 2022 ACT301: Intermediate Accounting Assignment 2Document2 pagesBBA Program Spring 2022 ACT301: Intermediate Accounting Assignment 2মাহিদ হাসানNo ratings yet

- Kunci AKL 2Document10 pagesKunci AKL 2Brenda BeatrikNo ratings yet

- Q1 From The Following Particulars of XYZ Ltd. Prepare The Cash Flow StatementDocument2 pagesQ1 From The Following Particulars of XYZ Ltd. Prepare The Cash Flow StatementSuvam PatelNo ratings yet

- P S T Total: PT PapanDocument20 pagesP S T Total: PT Papansean franciscusNo ratings yet

- Suria BHD Income Statement For The Year Ended (RM'000) SalesDocument3 pagesSuria BHD Income Statement For The Year Ended (RM'000) SalesAzzurin ArissaNo ratings yet

- Cash Flow Statement QuestionDocument1 pageCash Flow Statement QuestionVarunNo ratings yet

- Refresher Partnership Formation Problems SolutionsDocument11 pagesRefresher Partnership Formation Problems SolutionsbiadnescydcharyNo ratings yet

- Extra Session 2 (30 Sept 2022) Spreadsheet (CH 3)Document2 pagesExtra Session 2 (30 Sept 2022) Spreadsheet (CH 3)georgius gabrielNo ratings yet

- Shareholders EquityDocument6 pagesShareholders EquityDe Guzman Olchondra Kimberly100% (1)

- Bab 2 MateriDocument4 pagesBab 2 MateriAndikaNo ratings yet

- Buscom Subsequent MeasurementDocument6 pagesBuscom Subsequent MeasurementCarmela BautistaNo ratings yet

- Week 2 Requirement: Name: Puray, Ma. Lorraine M - Course: BSA-1 Class Schedule: M-F (7:00-8:50 Am)Document10 pagesWeek 2 Requirement: Name: Puray, Ma. Lorraine M - Course: BSA-1 Class Schedule: M-F (7:00-8:50 Am)Lorraine Millama PurayNo ratings yet

- Contoh Soal Mutual Holding Pendekatan Saham TreasuryDocument10 pagesContoh Soal Mutual Holding Pendekatan Saham TreasuryPutri ShaniaNo ratings yet

- CHP 2AnalysisInterpretationofAccountsDocument5 pagesCHP 2AnalysisInterpretationofAccountsalpeshmahto2004No ratings yet

- 10.3.2.5 Elaborate 10.3 Treasury Stock TransactionDocument8 pages10.3.2.5 Elaborate 10.3 Treasury Stock TransactionMARY ROSENo ratings yet

- Afar. Diagnostic: Response: Correct Answer: Score: 1 Out of 1 YesDocument31 pagesAfar. Diagnostic: Response: Correct Answer: Score: 1 Out of 1 YesMitch MinglanaNo ratings yet

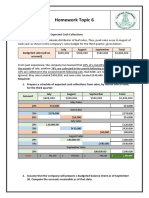

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Learning Task 2 Financial Statements of Rosalina Besario SurveyorsDocument6 pagesLearning Task 2 Financial Statements of Rosalina Besario SurveyorsNeil Matundan100% (1)

- Entry For The AcquisitionDocument5 pagesEntry For The AcquisitionEnalem OtsuepmeNo ratings yet

- BSA32 (Team 5) Team Task - University of San Jose RecoletosDocument11 pagesBSA32 (Team 5) Team Task - University of San Jose RecoletosVon Andrei MedinaNo ratings yet

- Solution For Activity On Consolidation at The Date of AcquisitionDocument4 pagesSolution For Activity On Consolidation at The Date of AcquisitionRea June SumatraNo ratings yet

- The Accounting Process 7th EditionDocument9 pagesThe Accounting Process 7th EditionPaula Anyssa Tobias BerbaNo ratings yet

- Multiple Choice Problems Chapter 8Document12 pagesMultiple Choice Problems Chapter 8Dieter LudwigNo ratings yet

- Solution Chapter 17Document87 pagesSolution Chapter 17Sy Him88% (8)

- Illustration On AFN (FE 12)Document39 pagesIllustration On AFN (FE 12)Jessica Adharana KurniaNo ratings yet

- Final Reviewer For ACC221Document91 pagesFinal Reviewer For ACC221ZalaR0cksNo ratings yet

- Consolidated Income Statement or Statement of Profit or Loss and Other Comprehensive IncomeDocument4 pagesConsolidated Income Statement or Statement of Profit or Loss and Other Comprehensive IncomeOmolaja IbukunNo ratings yet

- Foreign Currency Transactions2019Document6 pagesForeign Currency Transactions2019Jeann MuycoNo ratings yet

- Enero - ACC 222 Exercise - FS AnalysisDocument4 pagesEnero - ACC 222 Exercise - FS AnalysisregineNo ratings yet

- Excercise Chapter 2Document2 pagesExcercise Chapter 2Loan VũNo ratings yet

- Review Sw4tgession 5 TEXTDocument9 pagesReview Sw4tgession 5 TEXTMelissa WhiteNo ratings yet

- A Refresher in Financial AccountingDocument115 pagesA Refresher in Financial AccountingWang Hon Yuen100% (1)

- Chap 006Document71 pagesChap 006Aufa RadityatamaNo ratings yet

- Introducing Financial Statements and Transaction AnalysisDocument64 pagesIntroducing Financial Statements and Transaction AnalysisHazim AbualolaNo ratings yet

- Audit of Financial StatementsDocument8 pagesAudit of Financial Statementsd.pagkatoytoyNo ratings yet

- Answers - V2Chapter 3 2012 PDFDocument17 pagesAnswers - V2Chapter 3 2012 PDFkea paduaNo ratings yet

- C7 Gramado Đáp Án 1Document2 pagesC7 Gramado Đáp Án 1An TrịnhNo ratings yet

- AFAR Summary Lecture (10 May 2021)Document30 pagesAFAR Summary Lecture (10 May 2021)Joanna MalubayNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- Abc Chapter 2Document22 pagesAbc Chapter 2ZNo ratings yet

- IAII FINAL EXAM Maual SET BDocument9 pagesIAII FINAL EXAM Maual SET BClara MacallingNo ratings yet

- NN5 Chap 5Document41 pagesNN5 Chap 5Nguyet NguyenNo ratings yet

- Accounting For Business Combinations Pre 7 - SeatworksDocument4 pagesAccounting For Business Combinations Pre 7 - SeatworksJalyn Jalando-on50% (2)

- ACC 1701X Mock Exam #1 SolutionDocument13 pagesACC 1701X Mock Exam #1 SolutionShaunny BravoNo ratings yet

- 613659759Document11 pages613659759DJVillafuerteNo ratings yet

- Review of AccountingDocument31 pagesReview of AccountingDylan LoweNo ratings yet