Download as ppt, pdf, or txt

You might also like

- Nilson Report Issue 1182 - 0045Document15 pagesNilson Report Issue 1182 - 0045John MulderNo ratings yet

- Worldpay Global Payment Report 2016Document47 pagesWorldpay Global Payment Report 2016ipsitaNo ratings yet

- Latin America Payments Solution: November 2018Document19 pagesLatin America Payments Solution: November 2018Jairo MartinezNo ratings yet

- Nilson Report Issue 1175 - 0036Document10 pagesNilson Report Issue 1175 - 0036John MulderNo ratings yet

- PWC Payments Handbook 2023Document34 pagesPWC Payments Handbook 2023Koshur KottNo ratings yet

- Swift BCG Swiftfocus White PaperDocument17 pagesSwift BCG Swiftfocus White Paperchi nguyenNo ratings yet

- The Rising Tide of US Electronic Payments: White PaperDocument11 pagesThe Rising Tide of US Electronic Payments: White Papervatimetro2012No ratings yet

- 2014 Worldpay Alternative Payments 2nd Edition ReportDocument36 pages2014 Worldpay Alternative Payments 2nd Edition ReporteffeviNo ratings yet

- Why Software Vendors Should Be PFsDocument11 pagesWhy Software Vendors Should Be PFsLuis F JaureguiNo ratings yet

- Benefits of E-Payment SystemNEWDocument43 pagesBenefits of E-Payment SystemNEWDeepu MssNo ratings yet

- Traditional and Electronic Payment MethodsDocument35 pagesTraditional and Electronic Payment Methodsarshiyashah50% (2)

- Electronic Payment SystemDocument5 pagesElectronic Payment SystemSwati HansNo ratings yet

- Essentials of Online payment Security and Fraud PreventionFrom EverandEssentials of Online payment Security and Fraud PreventionNo ratings yet

- Accenture Digital Payments Survey North America Accenture Executive SummaryDocument20 pagesAccenture Digital Payments Survey North America Accenture Executive SummarySatya PrakashNo ratings yet

- Bnbpay Whitepaper V 1Document25 pagesBnbpay Whitepaper V 1Yudha Sidhikoro AjiNo ratings yet

- Modern Treasury - Setting Up Your Payment Operations ArchitectureDocument15 pagesModern Treasury - Setting Up Your Payment Operations Architecturefelipeap92No ratings yet

- 2checkout SB Payment Method CoverageDocument25 pages2checkout SB Payment Method CoveragePaul MccollicNo ratings yet

- A Vision For The Future of Cross Border Payments Web Final PDFDocument22 pagesA Vision For The Future of Cross Border Payments Web Final PDFFerdian Perdana KusumaNo ratings yet

- Case Study - NPCIDocument2 pagesCase Study - NPCIDens Can't Be PerfectNo ratings yet

- Classification of Electronic PaymentsDocument38 pagesClassification of Electronic PaymentsKenen BhandhaviNo ratings yet

- Accenture Driving The Future of Payments 10 Mega TrendsDocument16 pagesAccenture Driving The Future of Payments 10 Mega TrendsRaj BhatiNo ratings yet

- International Payments Import RequirementsDocument11 pagesInternational Payments Import Requirementsmariejoe.market1No ratings yet

- Dealroom Embedded Finance v2Document32 pagesDealroom Embedded Finance v2Sushma KazaNo ratings yet

- Making Money On Payments A Guide For SaaS CompaniesDocument15 pagesMaking Money On Payments A Guide For SaaS CompaniesManish ModiNo ratings yet

- VISA Dynamic Passcode AuthenticationDocument4 pagesVISA Dynamic Passcode AuthenticationBudi SugiantoNo ratings yet

- Bux - Multi-Wallet OverviewDocument29 pagesBux - Multi-Wallet OverviewEllen BrillantesNo ratings yet

- Global Fraud Report 2023 enDocument37 pagesGlobal Fraud Report 2023 enSiew Meng WongNo ratings yet

- TerraPay Product BrochureDocument35 pagesTerraPay Product BrochureEzeh Tochukwu100% (1)

- Paytm Payment Solutions Feb15 PDFDocument30 pagesPaytm Payment Solutions Feb15 PDFRomeo MalikNo ratings yet

- Intellias' Insights For Fintech Trends 2021Document1 pageIntellias' Insights For Fintech Trends 2021Quỳnh NhưNo ratings yet

- Online Paymet SystemsDocument23 pagesOnline Paymet SystemsPrabhjeet Sumit GoklaneyNo ratings yet

- Digital Payments IndiaDocument17 pagesDigital Payments IndiaPAUL JEFFERSON CLARENCE S PRC17MS1042No ratings yet

- Line of Credit Deposits Credit Card Balance Interest Credit HistoryDocument4 pagesLine of Credit Deposits Credit Card Balance Interest Credit HistoryJyoti JhajhraNo ratings yet

- The Future of PaymentsDocument6 pagesThe Future of Paymentszing65No ratings yet

- BAIN Brief - Five Imperatives For Navigating Turbulence in The Payments EcosystemDocument12 pagesBAIN Brief - Five Imperatives For Navigating Turbulence in The Payments Ecosystemapritul3539No ratings yet

- The Future of Digital Banking PDFDocument27 pagesThe Future of Digital Banking PDFRahmat SyarifNo ratings yet

- Banks Digital Wallet WhitepaperDocument9 pagesBanks Digital Wallet Whitepaperchandro2007No ratings yet

- Middle East/Africa: Purchase Volume 2015 vs. 2014Document11 pagesMiddle East/Africa: Purchase Volume 2015 vs. 2014Charan TejaNo ratings yet

- World Payments Report 2017 - Year - EndDocument52 pagesWorld Payments Report 2017 - Year - Endnvyg123No ratings yet

- Worldpay Alternative Payments 2nd Edition ReportDocument37 pagesWorldpay Alternative Payments 2nd Edition ReportDiablonNo ratings yet

- DefinitionsDocument2 pagesDefinitionskamlesh0608No ratings yet

- What Makes A Good LoaNDocument25 pagesWhat Makes A Good LoaNrajin_rammsteinNo ratings yet

- Alipay Payment Method Guide 2Document8 pagesAlipay Payment Method Guide 2vignesh_march1994100% (1)

- PayflowGateway GuideDocument238 pagesPayflowGateway Guiderobert2370No ratings yet

- Thinkmate ConfDocument1 pageThinkmate ConfAndrew BzikadzeNo ratings yet

- DB Europe - Data Blocks Overview - 28112023Document22 pagesDB Europe - Data Blocks Overview - 28112023Annas ShahNo ratings yet

- Presentation MSME Products 24092018 - Ver 1Document52 pagesPresentation MSME Products 24092018 - Ver 1Murali KrishnanNo ratings yet

- E-Payments, E-Wallet and The Future of Payments: Ho Chi Minh City, 19 April 2019Document24 pagesE-Payments, E-Wallet and The Future of Payments: Ho Chi Minh City, 19 April 2019icemainNo ratings yet

- Capgemini - World Payments Report 2013Document60 pagesCapgemini - World Payments Report 2013Carlo Di Domenico100% (1)

- Banks Thunes-1Document7 pagesBanks Thunes-1Hader Than UthoughtNo ratings yet

- Impact of Digital Wallets On Consumer Behavior in IndiaDocument17 pagesImpact of Digital Wallets On Consumer Behavior in IndiaIJAR JOURNALNo ratings yet

- Real Time PaymentsDocument21 pagesReal Time PaymentsOfelia PalleteNo ratings yet

- The Payment SystemDocument19 pagesThe Payment SystemLoredana IrinaNo ratings yet

- Electronic Retail Payment Systems: User Acceptability and Payment Problems in GhanaDocument66 pagesElectronic Retail Payment Systems: User Acceptability and Payment Problems in Ghanaafnankhan1100% (1)

- Proposal For Online Payment GatewayDocument11 pagesProposal For Online Payment Gatewaynayon khanNo ratings yet

- Givegivegivegivecorpcorpcorpcorp Productsproductsproductsproductsproductsproductsproductsproducts& ServicesservicesservicesservicesservicesservicesservicesservicesDocument17 pagesGivegivegivegivecorpcorpcorpcorp Productsproductsproductsproductsproductsproductsproductsproducts& ServicesservicesservicesservicesservicesservicesservicesservicesAde SulaemanNo ratings yet

- First 7 PagesDocument8 pagesFirst 7 PagesAndali AliNo ratings yet

- FIS CardLifecycleManagement StrategyDocument35 pagesFIS CardLifecycleManagement Strategygautam_hariharanNo ratings yet

- I5310 A2C User ManualDocument52 pagesI5310 A2C User Manualpax37No ratings yet

- The Digital Banking Revolution: How financial technology companies are rapidly transforming the traditional retail banking industry through disruptive innovation.From EverandThe Digital Banking Revolution: How financial technology companies are rapidly transforming the traditional retail banking industry through disruptive innovation.No ratings yet

- Course Title: Digital Electronics Course Code: ECE 205 Credit Units: 4 Level: UG L T P/ S SW/F W Total Credit UnitsDocument4 pagesCourse Title: Digital Electronics Course Code: ECE 205 Credit Units: 4 Level: UG L T P/ S SW/F W Total Credit UnitsPrinceRajDKilerNo ratings yet

- Java Servlets: What Is Server-Side Programming?Document18 pagesJava Servlets: What Is Server-Side Programming?PrinceRajDKilerNo ratings yet

- Installing and Configuring Tomcat: Softsmith InfotechDocument30 pagesInstalling and Configuring Tomcat: Softsmith InfotechPrinceRajDKilerNo ratings yet

- The Physical Layer, Encoding Schemes:: - Physical Transmission of BitsDocument13 pagesThe Physical Layer, Encoding Schemes:: - Physical Transmission of BitsPrinceRajDKilerNo ratings yet

- To Whom It May ConcernDocument1 pageTo Whom It May ConcernPrinceRajDKilerNo ratings yet

- Functions: by Jeannie FrancisDocument5 pagesFunctions: by Jeannie FrancisPrinceRajDKilerNo ratings yet

- Report ExampleDocument413 pagesReport ExamplePrinceRajDKilerNo ratings yet

- 04 - Process Document - S4Document4 pages04 - Process Document - S4Pãśhãh ŠháìkhNo ratings yet

- Itenerary Ms. Nidia Sofa Amsterdam-Rotterdam, Holland 1-3 OKTOBER 2019Document4 pagesItenerary Ms. Nidia Sofa Amsterdam-Rotterdam, Holland 1-3 OKTOBER 2019Zahrah FarhataeniNo ratings yet

- Accounting For Consigned GoodsDocument6 pagesAccounting For Consigned GoodsHumphrey OdchigueNo ratings yet

- Taxation Review Presentation (Philippines)Document49 pagesTaxation Review Presentation (Philippines)Marc ToresNo ratings yet

- The Expenditure Cycle (Latest)Document4 pagesThe Expenditure Cycle (Latest)Ashiqur Ansary100% (1)

- Schedule of Services and Tariffs: HSBC Jade, HSBC Premier, HSBC Advance and Personal BankingDocument18 pagesSchedule of Services and Tariffs: HSBC Jade, HSBC Premier, HSBC Advance and Personal BankingShadab HussainNo ratings yet

- BCA Fee Slip 17530 67151 11012023Document1 pageBCA Fee Slip 17530 67151 11012023Sohail KarimNo ratings yet

- Eross Security Force AgencyDocument2 pagesEross Security Force AgencyJbars Backyard GFNo ratings yet

- RMIT CalendarDocument2 pagesRMIT CalendarIvan NguyenNo ratings yet

- Tax Planning With Example, Compensation MGMTDocument40 pagesTax Planning With Example, Compensation MGMTrashmi_shantikumarNo ratings yet

- ch03 SM Carlon 5eDocument139 pagesch03 SM Carlon 5eKyle0% (1)

- 4th Sem Fee ReceiptDocument5 pages4th Sem Fee ReceiptKuldeepNo ratings yet

- Email Mobile Database of Cfos Finance Heads SampleDocument7 pagesEmail Mobile Database of Cfos Finance Heads SamplevivekinductusNo ratings yet

- Fee VoucherDocument1 pageFee Vouchermuhammad.wajahat194No ratings yet

- Topic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsDocument3 pagesTopic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsMitchell BylartNo ratings yet

- UntitledDocument8 pagesUntitledPreeti SinghNo ratings yet

- 9th Class MathsDocument23 pages9th Class MathsSrinu SehwagNo ratings yet

- Cricket Bill Pay Methods - Cricket WirelessDocument6 pagesCricket Bill Pay Methods - Cricket WirelessJohn Michael Antonio100% (1)

- Internal Control and CashDocument52 pagesInternal Control and CashDang Thanh100% (1)

- Kaasi Annapurna AnnakshetraDocument2 pagesKaasi Annapurna Annakshetramail2cnivasNo ratings yet

- Announcing The FIS Sales and Channel Distribution OrganizationDocument3 pagesAnnouncing The FIS Sales and Channel Distribution OrganizationCameron BallNo ratings yet

- Account STMT XX2427 08052024Document12 pagesAccount STMT XX2427 08052024Shariff MahammadNo ratings yet

- Incoterms - LC & SBLC For Indonesia Power v2Document167 pagesIncoterms - LC & SBLC For Indonesia Power v2Mohamad WahyudiNo ratings yet

- Same-Day Worksheet 1010Document2 pagesSame-Day Worksheet 1010Hans GadamerNo ratings yet

- HISTORYDocument3 pagesHISTORYpenusila6941No ratings yet

- Invoice 1139421221 I0136P2000267596Document1 pageInvoice 1139421221 I0136P2000267596Thanish GattuNo ratings yet

- 20230410-20240411-9128 Eur enDocument14 pages20230410-20240411-9128 Eur enmarsovnaka2016No ratings yet

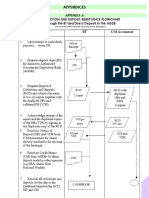

- Appendix A Collection and Deposit/Remittance Flowchart Through The BT and Direct Deposit To The AGDBDocument75 pagesAppendix A Collection and Deposit/Remittance Flowchart Through The BT and Direct Deposit To The AGDBJayNo ratings yet

- Methods of Computing Economic Order QuantityDocument20 pagesMethods of Computing Economic Order QuantityMyrn de AsisNo ratings yet

- Statement For Customer #1046913: NTN# - ATTN:Naveed NazarDocument3 pagesStatement For Customer #1046913: NTN# - ATTN:Naveed NazarHamza NajamNo ratings yet