Retail Banking: by Prof Santosh Kumar

Retail Banking: by Prof Santosh Kumar

You might also like

- Motilal Oswal Financial Services LTDDocument5 pagesMotilal Oswal Financial Services LTDseawoodsNo ratings yet

- Loi Buy Buyer MTN Mid Medium Term Notes 2012Document13 pagesLoi Buy Buyer MTN Mid Medium Term Notes 2012Max de Espacan83% (6)

- Consumerism and Prestige: The Materiality of Literature in the Modern AgeFrom EverandConsumerism and Prestige: The Materiality of Literature in the Modern AgeAnthony EnnsNo ratings yet

- Case Analysis BigBAzaarDocument6 pagesCase Analysis BigBAzaarArka MitraNo ratings yet

- Ch04 Capm and AptDocument167 pagesCh04 Capm and AptAmit PandeyNo ratings yet

- Ebook - The Economics of Corporate Information Systems Measuring Information Payoffs - Paul A. StrassmannDocument224 pagesEbook - The Economics of Corporate Information Systems Measuring Information Payoffs - Paul A. StrassmannGraciela GourethNo ratings yet

- BUAd 801Document47 pagesBUAd 801Adetunji Taiwo100% (1)

- Capital First Limited ProjectDocument74 pagesCapital First Limited Projectbiranchi behera100% (1)

- What Is Wholesale Banking ?Document10 pagesWhat Is Wholesale Banking ?Anonymous So5qPSnNo ratings yet

- Bharti Minor Project ReportDocument42 pagesBharti Minor Project ReportHatsh kumarNo ratings yet

- Process of Issue of Commercial PapersDocument14 pagesProcess of Issue of Commercial PapersApoorv Gupta100% (1)

- Financial Analysis of HDFC LifeDocument77 pagesFinancial Analysis of HDFC LifeSankalp SamantNo ratings yet

- Demand EstimationDocument84 pagesDemand EstimationMuhammad AjmalNo ratings yet

- Bandhan Case Study: Prepared By: Bakshi Satpreet Singh (10MBI1005)Document17 pagesBandhan Case Study: Prepared By: Bakshi Satpreet Singh (10MBI1005)Sachit MalikNo ratings yet

- SBI Plans 'By-Invitation-Only' Branches in 20 CitiesDocument1 pageSBI Plans 'By-Invitation-Only' Branches in 20 CitiesSanjay Sinha0% (1)

- SportkingDocument11 pagesSportkinggurkirat singhNo ratings yet

- HDFCDocument1 pageHDFCArun SomanNo ratings yet

- ICICI Case StudiesDocument4 pagesICICI Case StudiesSupriyo Sen100% (1)

- 26.inward RemittancesDocument4 pages26.inward RemittancesanilkumarosmeNo ratings yet

- Faircent P2P Case AnalysisDocument5 pagesFaircent P2P Case AnalysisSiddharth KashyapNo ratings yet

- Risk Management With A Duration Gap ApproachDocument44 pagesRisk Management With A Duration Gap ApproachDicto RockyNo ratings yet

- Case# Bandhan (A) : Advancing Financial Inclusion in IndiaDocument3 pagesCase# Bandhan (A) : Advancing Financial Inclusion in IndiaLavanya KashyapNo ratings yet

- A Study of Dematerialisation in Banking SectorDocument65 pagesA Study of Dematerialisation in Banking SectorUmesh SoniNo ratings yet

- Boosting Boost: Section C Group C 10Document6 pagesBoosting Boost: Section C Group C 10Ishaan VatsNo ratings yet

- Prof.. Anju Dusseja: Name Roll - NoDocument18 pagesProf.. Anju Dusseja: Name Roll - NoOmkar PandeyNo ratings yet

- SidbiDocument26 pagesSidbiAnand JoshiNo ratings yet

- Cashing Out The Future of Cash in Israel - Group12Document7 pagesCashing Out The Future of Cash in Israel - Group12Vimal JephNo ratings yet

- Case Study ON State Bank of India: VRS StoryDocument9 pagesCase Study ON State Bank of India: VRS StoryKapil SoniNo ratings yet

- A Study On Comparative Analysis of HDFC Bank and Icici Bank On The Basis of Capital Market PerformanceDocument11 pagesA Study On Comparative Analysis of HDFC Bank and Icici Bank On The Basis of Capital Market PerformanceSahil BansalNo ratings yet

- Icici BankDocument59 pagesIcici BankChetan JanardhanaNo ratings yet

- FCCBDocument14 pagesFCCBVanessa DavisNo ratings yet

- Financial CrisisDocument40 pagesFinancial CrisisShahidAthaniNo ratings yet

- Payment and Small BanksDocument27 pagesPayment and Small BanksDr.Satish RadhakrishnanNo ratings yet

- Aditya Birla Financial Services Group (ABFSG)Document12 pagesAditya Birla Financial Services Group (ABFSG)yoper18No ratings yet

- Consumer FinanceDocument15 pagesConsumer FinanceforamnshahNo ratings yet

- Industry Life Cycle of Banking IndustryDocument1 pageIndustry Life Cycle of Banking IndustryShariq Siddiqui0% (2)

- Porter'S Five Forces Analysis: Banking IndustryDocument5 pagesPorter'S Five Forces Analysis: Banking Industryshraddha anandNo ratings yet

- Behavioral FinanceDocument5 pagesBehavioral FinancemanojeethNo ratings yet

- Swot AnalysisDocument4 pagesSwot AnalysisShubhamSoodNo ratings yet

- 7 P's of ICICI BANKDocument13 pages7 P's of ICICI BANKSumit VishwakarmaNo ratings yet

- Ques TestDocument3 pagesQues Testaastha124892823No ratings yet

- HSBC Bank Bangladesh Powervantage Account (Pva)Document7 pagesHSBC Bank Bangladesh Powervantage Account (Pva)carinagtNo ratings yet

- Presented By: Himanshu Gurani Roll No. 33Document27 pagesPresented By: Himanshu Gurani Roll No. 33AshishBhardwajNo ratings yet

- Assessment of Service Quality in Indian Retailbanks For Icici Bank, HDFC Bank, Sbi and PNBDocument76 pagesAssessment of Service Quality in Indian Retailbanks For Icici Bank, HDFC Bank, Sbi and PNBParthesh Pandey100% (1)

- Reaction Paper To Abraham Zaleznik's Managers & Leaders - Are They DifferentDocument4 pagesReaction Paper To Abraham Zaleznik's Managers & Leaders - Are They DifferentElizier 'Barlee' B. Lazo50% (2)

- Case 1 - Term Sheet Negotiations For Trendsetter Inc. Group 3Document10 pagesCase 1 - Term Sheet Negotiations For Trendsetter Inc. Group 3Avanish Nagar 23No ratings yet

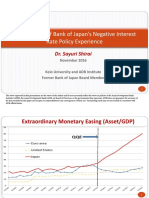

- An Overview of Bank of Japan Negative Interest Rate Policy ExperienceDocument12 pagesAn Overview of Bank of Japan Negative Interest Rate Policy ExperienceADBI Events100% (1)

- Evolution & Growth of Investment Banking in India - grp6 - SecannnnDocument13 pagesEvolution & Growth of Investment Banking in India - grp6 - SecannnnNaveen KeswaniNo ratings yet

- AssignmentDocument10 pagesAssignmentaruakshNo ratings yet

- Derivative Market in IndiaDocument19 pagesDerivative Market in IndiaMunmun Das JenaNo ratings yet

- CG IntroDocument15 pagesCG IntroMohit SonyNo ratings yet

- M&ADocument8 pagesM&ARituparna BhattacharjeeNo ratings yet

- OverviewDocument18 pagesOverviewGaurav SinghNo ratings yet

- Consumer Finance PDFDocument27 pagesConsumer Finance PDFumair100% (4)

- Retail Management: Case AnalysisDocument7 pagesRetail Management: Case Analysisakshaysingh211No ratings yet

- Indian Financial SystemDocument163 pagesIndian Financial SystemrohitravaliyaNo ratings yet

- Case Study Barclays FinalDocument13 pagesCase Study Barclays FinalShalini Senglo RajaNo ratings yet

- Sujit Balbirpasha CaseananalysisDocument6 pagesSujit Balbirpasha CaseananalysisMukilPillaiNo ratings yet

- "Retail Banking": A Project ReportDocument72 pages"Retail Banking": A Project ReportneanaoNo ratings yet

- Marketing Mix in ICICI BankDocument24 pagesMarketing Mix in ICICI BankAzim SamnaniNo ratings yet

- Starbucks Market Entry and Expansion STR PDFDocument19 pagesStarbucks Market Entry and Expansion STR PDFKushagra Hansrani100% (1)

- Behavioral Finance: Jay R. RitterDocument9 pagesBehavioral Finance: Jay R. RitterTehreema KazmiNo ratings yet

- Osp AakashDocument6 pagesOsp AakashSuraj KumarNo ratings yet

- Organizational Structure and Its Various CorrelatesDocument3 pagesOrganizational Structure and Its Various CorrelatesSuraj KumarNo ratings yet

- Chap006 PPT 8eDocument14 pagesChap006 PPT 8eSuraj KumarNo ratings yet

- Drivers & Metrics: of Supply Chain PerformanceDocument51 pagesDrivers & Metrics: of Supply Chain PerformanceSuraj KumarNo ratings yet

- Leo Negotiation StyleDocument1 pageLeo Negotiation StyleSuraj KumarNo ratings yet

- Traits of Jack MaDocument2 pagesTraits of Jack MaSuraj Kumar100% (1)

- Structuring of InnovationDocument1 pageStructuring of InnovationSuraj KumarNo ratings yet

- Osp AakashDocument20 pagesOsp AakashSuraj KumarNo ratings yet

- Insolvency ProceedingsDocument3 pagesInsolvency ProceedingsSuraj KumarNo ratings yet

- A Brief Study On Alibaba Group and Jack Ma: Chandragupt Institute of Management PatnaDocument16 pagesA Brief Study On Alibaba Group and Jack Ma: Chandragupt Institute of Management PatnaSuraj KumarNo ratings yet

- Financial Modeling: Financial Planning and InvestmentsDocument1 pageFinancial Modeling: Financial Planning and InvestmentsSuraj KumarNo ratings yet

- UdbhavDocument1 pageUdbhavSuraj KumarNo ratings yet

- Q:-Define Hypothesis and Explain The Different Functions They Perform in A Research ProcessDocument3 pagesQ:-Define Hypothesis and Explain The Different Functions They Perform in A Research ProcessSuraj KumarNo ratings yet

- Q:-Discuss The Stages in Product Design Process: 1. Idea GenerationDocument7 pagesQ:-Discuss The Stages in Product Design Process: 1. Idea GenerationSuraj KumarNo ratings yet

- Q:-Explain The Probability and Nonprobability Sampling TechniquesDocument3 pagesQ:-Explain The Probability and Nonprobability Sampling TechniquesSuraj KumarNo ratings yet

- Research Can Be Classified in Many Different Ways On The Basis of The Methodology of Research, The Knowledge It Creates, The User Group, The Research Problem It Investigates EtcDocument2 pagesResearch Can Be Classified in Many Different Ways On The Basis of The Methodology of Research, The Knowledge It Creates, The User Group, The Research Problem It Investigates EtcSuraj KumarNo ratings yet

- Lecture Notes For IAS 36Document9 pagesLecture Notes For IAS 36dương nguyễn vũ thùyNo ratings yet

- Calimanesti - English PresentationDocument23 pagesCalimanesti - English Presentationada1808No ratings yet

- P2 RevisionDocument16 pagesP2 RevisionfirefxyNo ratings yet

- ITC Company AnalysisDocument16 pagesITC Company AnalysisAaron RodriguesNo ratings yet

- Client Acceptance and Continuance: Good Practice GuidanceDocument42 pagesClient Acceptance and Continuance: Good Practice GuidanceJoHn CarLoNo ratings yet

- Fsa 2010 14 PDFDocument257 pagesFsa 2010 14 PDFsarapariNo ratings yet

- Assignment DigestsDocument8 pagesAssignment Digestsmelaniem_1No ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasReznakNo ratings yet

- Risk Chapter 7Document15 pagesRisk Chapter 7Wonde Biru100% (1)

- Annie MaidhDocument11 pagesAnnie MaidhMadhurendra SinghNo ratings yet

- ValCom Syllabus BSMADocument14 pagesValCom Syllabus BSMAMerel Rose FloresNo ratings yet

- StarbucksDocument9 pagesStarbucksallen1191919No ratings yet

- AbhayaHastam Note 200209Document4 pagesAbhayaHastam Note 200209Vijay Kumar BNo ratings yet

- Tutorial 1 (For Student)Document2 pagesTutorial 1 (For Student)dee davyanNo ratings yet

- JAIIB Paper 1 CAPSULE PDF Principles Practices of Banking PDFDocument269 pagesJAIIB Paper 1 CAPSULE PDF Principles Practices of Banking PDFLatha Mypati100% (1)

- Sbi Focused Equity Fund Factsheet (May-2019!25!1)Document1 pageSbi Focused Equity Fund Factsheet (May-2019!25!1)Chandrasekar Attayampatty TamilarasanNo ratings yet

- (Strategy) Indian Diaspora For General Studies Mains Paper 2 Free Study Material, Previous Questions For UPSC Civil Service IAS IPS ExamDocument9 pages(Strategy) Indian Diaspora For General Studies Mains Paper 2 Free Study Material, Previous Questions For UPSC Civil Service IAS IPS ExambhavyaNo ratings yet

- The Forum: Our New Comment SectionDocument36 pagesThe Forum: Our New Comment SectionCity A.M.No ratings yet

- Accounting Adjustment-Accrued & PrepaidDocument30 pagesAccounting Adjustment-Accrued & PrepaidEida HidayahNo ratings yet

- ValuEngine Weekly Newsletter September 30, 2011Document12 pagesValuEngine Weekly Newsletter September 30, 2011ValuEngine.comNo ratings yet

- Private Equity and Venture CapitalDocument21 pagesPrivate Equity and Venture CapitalRahul LakhaniNo ratings yet

- Mergers and ConsolidationDocument2 pagesMergers and ConsolidationCarlo Columna100% (1)

- F No - 135Document3 pagesF No - 135Treena Majumder SarkarNo ratings yet

- GLobal Financial Stability April 2023 IMFDocument126 pagesGLobal Financial Stability April 2023 IMFZeid comline2020No ratings yet

- Project ReportDocument60 pagesProject ReportItronix Mohali75% (4)

- FbvarDocument4 pagesFbvarSRGVPNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Motilal Oswal Financial Services LTDDocument5 pagesMotilal Oswal Financial Services LTDseawoodsNo ratings yet

- Loi Buy Buyer MTN Mid Medium Term Notes 2012Document13 pagesLoi Buy Buyer MTN Mid Medium Term Notes 2012Max de Espacan83% (6)

- Consumerism and Prestige: The Materiality of Literature in the Modern AgeFrom EverandConsumerism and Prestige: The Materiality of Literature in the Modern AgeAnthony EnnsNo ratings yet

- Case Analysis BigBAzaarDocument6 pagesCase Analysis BigBAzaarArka MitraNo ratings yet

- Ch04 Capm and AptDocument167 pagesCh04 Capm and AptAmit PandeyNo ratings yet

- Ebook - The Economics of Corporate Information Systems Measuring Information Payoffs - Paul A. StrassmannDocument224 pagesEbook - The Economics of Corporate Information Systems Measuring Information Payoffs - Paul A. StrassmannGraciela GourethNo ratings yet

- BUAd 801Document47 pagesBUAd 801Adetunji Taiwo100% (1)

- Capital First Limited ProjectDocument74 pagesCapital First Limited Projectbiranchi behera100% (1)

- What Is Wholesale Banking ?Document10 pagesWhat Is Wholesale Banking ?Anonymous So5qPSnNo ratings yet

- Bharti Minor Project ReportDocument42 pagesBharti Minor Project ReportHatsh kumarNo ratings yet

- Process of Issue of Commercial PapersDocument14 pagesProcess of Issue of Commercial PapersApoorv Gupta100% (1)

- Financial Analysis of HDFC LifeDocument77 pagesFinancial Analysis of HDFC LifeSankalp SamantNo ratings yet

- Demand EstimationDocument84 pagesDemand EstimationMuhammad AjmalNo ratings yet

- Bandhan Case Study: Prepared By: Bakshi Satpreet Singh (10MBI1005)Document17 pagesBandhan Case Study: Prepared By: Bakshi Satpreet Singh (10MBI1005)Sachit MalikNo ratings yet

- SBI Plans 'By-Invitation-Only' Branches in 20 CitiesDocument1 pageSBI Plans 'By-Invitation-Only' Branches in 20 CitiesSanjay Sinha0% (1)

- SportkingDocument11 pagesSportkinggurkirat singhNo ratings yet

- HDFCDocument1 pageHDFCArun SomanNo ratings yet

- ICICI Case StudiesDocument4 pagesICICI Case StudiesSupriyo Sen100% (1)

- 26.inward RemittancesDocument4 pages26.inward RemittancesanilkumarosmeNo ratings yet

- Faircent P2P Case AnalysisDocument5 pagesFaircent P2P Case AnalysisSiddharth KashyapNo ratings yet

- Risk Management With A Duration Gap ApproachDocument44 pagesRisk Management With A Duration Gap ApproachDicto RockyNo ratings yet

- Case# Bandhan (A) : Advancing Financial Inclusion in IndiaDocument3 pagesCase# Bandhan (A) : Advancing Financial Inclusion in IndiaLavanya KashyapNo ratings yet

- A Study of Dematerialisation in Banking SectorDocument65 pagesA Study of Dematerialisation in Banking SectorUmesh SoniNo ratings yet

- Boosting Boost: Section C Group C 10Document6 pagesBoosting Boost: Section C Group C 10Ishaan VatsNo ratings yet

- Prof.. Anju Dusseja: Name Roll - NoDocument18 pagesProf.. Anju Dusseja: Name Roll - NoOmkar PandeyNo ratings yet

- SidbiDocument26 pagesSidbiAnand JoshiNo ratings yet

- Cashing Out The Future of Cash in Israel - Group12Document7 pagesCashing Out The Future of Cash in Israel - Group12Vimal JephNo ratings yet

- Case Study ON State Bank of India: VRS StoryDocument9 pagesCase Study ON State Bank of India: VRS StoryKapil SoniNo ratings yet

- A Study On Comparative Analysis of HDFC Bank and Icici Bank On The Basis of Capital Market PerformanceDocument11 pagesA Study On Comparative Analysis of HDFC Bank and Icici Bank On The Basis of Capital Market PerformanceSahil BansalNo ratings yet

- Icici BankDocument59 pagesIcici BankChetan JanardhanaNo ratings yet

- FCCBDocument14 pagesFCCBVanessa DavisNo ratings yet

- Financial CrisisDocument40 pagesFinancial CrisisShahidAthaniNo ratings yet

- Payment and Small BanksDocument27 pagesPayment and Small BanksDr.Satish RadhakrishnanNo ratings yet

- Aditya Birla Financial Services Group (ABFSG)Document12 pagesAditya Birla Financial Services Group (ABFSG)yoper18No ratings yet

- Consumer FinanceDocument15 pagesConsumer FinanceforamnshahNo ratings yet

- Industry Life Cycle of Banking IndustryDocument1 pageIndustry Life Cycle of Banking IndustryShariq Siddiqui0% (2)

- Porter'S Five Forces Analysis: Banking IndustryDocument5 pagesPorter'S Five Forces Analysis: Banking Industryshraddha anandNo ratings yet

- Behavioral FinanceDocument5 pagesBehavioral FinancemanojeethNo ratings yet

- Swot AnalysisDocument4 pagesSwot AnalysisShubhamSoodNo ratings yet

- 7 P's of ICICI BANKDocument13 pages7 P's of ICICI BANKSumit VishwakarmaNo ratings yet

- Ques TestDocument3 pagesQues Testaastha124892823No ratings yet

- HSBC Bank Bangladesh Powervantage Account (Pva)Document7 pagesHSBC Bank Bangladesh Powervantage Account (Pva)carinagtNo ratings yet

- Presented By: Himanshu Gurani Roll No. 33Document27 pagesPresented By: Himanshu Gurani Roll No. 33AshishBhardwajNo ratings yet

- Assessment of Service Quality in Indian Retailbanks For Icici Bank, HDFC Bank, Sbi and PNBDocument76 pagesAssessment of Service Quality in Indian Retailbanks For Icici Bank, HDFC Bank, Sbi and PNBParthesh Pandey100% (1)

- Reaction Paper To Abraham Zaleznik's Managers & Leaders - Are They DifferentDocument4 pagesReaction Paper To Abraham Zaleznik's Managers & Leaders - Are They DifferentElizier 'Barlee' B. Lazo50% (2)

- Case 1 - Term Sheet Negotiations For Trendsetter Inc. Group 3Document10 pagesCase 1 - Term Sheet Negotiations For Trendsetter Inc. Group 3Avanish Nagar 23No ratings yet

- An Overview of Bank of Japan Negative Interest Rate Policy ExperienceDocument12 pagesAn Overview of Bank of Japan Negative Interest Rate Policy ExperienceADBI Events100% (1)

- Evolution & Growth of Investment Banking in India - grp6 - SecannnnDocument13 pagesEvolution & Growth of Investment Banking in India - grp6 - SecannnnNaveen KeswaniNo ratings yet

- AssignmentDocument10 pagesAssignmentaruakshNo ratings yet

- Derivative Market in IndiaDocument19 pagesDerivative Market in IndiaMunmun Das JenaNo ratings yet

- CG IntroDocument15 pagesCG IntroMohit SonyNo ratings yet

- M&ADocument8 pagesM&ARituparna BhattacharjeeNo ratings yet

- OverviewDocument18 pagesOverviewGaurav SinghNo ratings yet

- Consumer Finance PDFDocument27 pagesConsumer Finance PDFumair100% (4)

- Retail Management: Case AnalysisDocument7 pagesRetail Management: Case Analysisakshaysingh211No ratings yet

- Indian Financial SystemDocument163 pagesIndian Financial SystemrohitravaliyaNo ratings yet

- Case Study Barclays FinalDocument13 pagesCase Study Barclays FinalShalini Senglo RajaNo ratings yet

- Sujit Balbirpasha CaseananalysisDocument6 pagesSujit Balbirpasha CaseananalysisMukilPillaiNo ratings yet

- "Retail Banking": A Project ReportDocument72 pages"Retail Banking": A Project ReportneanaoNo ratings yet

- Marketing Mix in ICICI BankDocument24 pagesMarketing Mix in ICICI BankAzim SamnaniNo ratings yet

- Starbucks Market Entry and Expansion STR PDFDocument19 pagesStarbucks Market Entry and Expansion STR PDFKushagra Hansrani100% (1)

- Behavioral Finance: Jay R. RitterDocument9 pagesBehavioral Finance: Jay R. RitterTehreema KazmiNo ratings yet

- Osp AakashDocument6 pagesOsp AakashSuraj KumarNo ratings yet

- Organizational Structure and Its Various CorrelatesDocument3 pagesOrganizational Structure and Its Various CorrelatesSuraj KumarNo ratings yet

- Chap006 PPT 8eDocument14 pagesChap006 PPT 8eSuraj KumarNo ratings yet

- Drivers & Metrics: of Supply Chain PerformanceDocument51 pagesDrivers & Metrics: of Supply Chain PerformanceSuraj KumarNo ratings yet

- Leo Negotiation StyleDocument1 pageLeo Negotiation StyleSuraj KumarNo ratings yet

- Traits of Jack MaDocument2 pagesTraits of Jack MaSuraj Kumar100% (1)

- Structuring of InnovationDocument1 pageStructuring of InnovationSuraj KumarNo ratings yet

- Osp AakashDocument20 pagesOsp AakashSuraj KumarNo ratings yet

- Insolvency ProceedingsDocument3 pagesInsolvency ProceedingsSuraj KumarNo ratings yet

- A Brief Study On Alibaba Group and Jack Ma: Chandragupt Institute of Management PatnaDocument16 pagesA Brief Study On Alibaba Group and Jack Ma: Chandragupt Institute of Management PatnaSuraj KumarNo ratings yet

- Financial Modeling: Financial Planning and InvestmentsDocument1 pageFinancial Modeling: Financial Planning and InvestmentsSuraj KumarNo ratings yet

- UdbhavDocument1 pageUdbhavSuraj KumarNo ratings yet

- Q:-Define Hypothesis and Explain The Different Functions They Perform in A Research ProcessDocument3 pagesQ:-Define Hypothesis and Explain The Different Functions They Perform in A Research ProcessSuraj KumarNo ratings yet

- Q:-Discuss The Stages in Product Design Process: 1. Idea GenerationDocument7 pagesQ:-Discuss The Stages in Product Design Process: 1. Idea GenerationSuraj KumarNo ratings yet

- Q:-Explain The Probability and Nonprobability Sampling TechniquesDocument3 pagesQ:-Explain The Probability and Nonprobability Sampling TechniquesSuraj KumarNo ratings yet

- Research Can Be Classified in Many Different Ways On The Basis of The Methodology of Research, The Knowledge It Creates, The User Group, The Research Problem It Investigates EtcDocument2 pagesResearch Can Be Classified in Many Different Ways On The Basis of The Methodology of Research, The Knowledge It Creates, The User Group, The Research Problem It Investigates EtcSuraj KumarNo ratings yet

- Lecture Notes For IAS 36Document9 pagesLecture Notes For IAS 36dương nguyễn vũ thùyNo ratings yet

- Calimanesti - English PresentationDocument23 pagesCalimanesti - English Presentationada1808No ratings yet

- P2 RevisionDocument16 pagesP2 RevisionfirefxyNo ratings yet

- ITC Company AnalysisDocument16 pagesITC Company AnalysisAaron RodriguesNo ratings yet

- Client Acceptance and Continuance: Good Practice GuidanceDocument42 pagesClient Acceptance and Continuance: Good Practice GuidanceJoHn CarLoNo ratings yet

- Fsa 2010 14 PDFDocument257 pagesFsa 2010 14 PDFsarapariNo ratings yet

- Assignment DigestsDocument8 pagesAssignment Digestsmelaniem_1No ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasReznakNo ratings yet

- Risk Chapter 7Document15 pagesRisk Chapter 7Wonde Biru100% (1)

- Annie MaidhDocument11 pagesAnnie MaidhMadhurendra SinghNo ratings yet

- ValCom Syllabus BSMADocument14 pagesValCom Syllabus BSMAMerel Rose FloresNo ratings yet

- StarbucksDocument9 pagesStarbucksallen1191919No ratings yet

- AbhayaHastam Note 200209Document4 pagesAbhayaHastam Note 200209Vijay Kumar BNo ratings yet

- Tutorial 1 (For Student)Document2 pagesTutorial 1 (For Student)dee davyanNo ratings yet

- JAIIB Paper 1 CAPSULE PDF Principles Practices of Banking PDFDocument269 pagesJAIIB Paper 1 CAPSULE PDF Principles Practices of Banking PDFLatha Mypati100% (1)

- Sbi Focused Equity Fund Factsheet (May-2019!25!1)Document1 pageSbi Focused Equity Fund Factsheet (May-2019!25!1)Chandrasekar Attayampatty TamilarasanNo ratings yet

- (Strategy) Indian Diaspora For General Studies Mains Paper 2 Free Study Material, Previous Questions For UPSC Civil Service IAS IPS ExamDocument9 pages(Strategy) Indian Diaspora For General Studies Mains Paper 2 Free Study Material, Previous Questions For UPSC Civil Service IAS IPS ExambhavyaNo ratings yet

- The Forum: Our New Comment SectionDocument36 pagesThe Forum: Our New Comment SectionCity A.M.No ratings yet

- Accounting Adjustment-Accrued & PrepaidDocument30 pagesAccounting Adjustment-Accrued & PrepaidEida HidayahNo ratings yet

- ValuEngine Weekly Newsletter September 30, 2011Document12 pagesValuEngine Weekly Newsletter September 30, 2011ValuEngine.comNo ratings yet

- Private Equity and Venture CapitalDocument21 pagesPrivate Equity and Venture CapitalRahul LakhaniNo ratings yet

- Mergers and ConsolidationDocument2 pagesMergers and ConsolidationCarlo Columna100% (1)

- F No - 135Document3 pagesF No - 135Treena Majumder SarkarNo ratings yet

- GLobal Financial Stability April 2023 IMFDocument126 pagesGLobal Financial Stability April 2023 IMFZeid comline2020No ratings yet

- Project ReportDocument60 pagesProject ReportItronix Mohali75% (4)

- FbvarDocument4 pagesFbvarSRGVPNo ratings yet