Download as ppt, pdf, or txt

You might also like

- NSE Equity Research Module 1 PDFDocument143 pagesNSE Equity Research Module 1 PDFBaneNo ratings yet

- Designing and Managing Integrated Marketing Communications Chapter 17Document14 pagesDesigning and Managing Integrated Marketing Communications Chapter 17Subhajit KarmakarNo ratings yet

- Ag Settlement Docs Filed in Federal Court-Complaint + Boa and Chase Proposed Consent JudgementsDocument707 pagesAg Settlement Docs Filed in Federal Court-Complaint + Boa and Chase Proposed Consent Judgements83jjmackNo ratings yet

- Problem 2Document4 pagesProblem 2redassdawn100% (1)

- Sample Report II - Card System Forensic Audit ReportDocument24 pagesSample Report II - Card System Forensic Audit ReportArif AhmedNo ratings yet

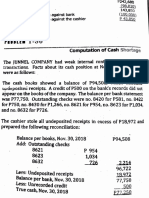

- T N e M e T A T S R e M o T S U CDocument2 pagesT N e M e T A T S R e M o T S U Czubair ahmad100% (1)

- L8 Raising CapitalDocument26 pagesL8 Raising CapitalKranthi ManthriNo ratings yet

- Company Profile: Kalikasthan, Dillibazar, Kathmandu, Nepal Tel: +977 - 1 - 4442435, 4424743 EmailDocument13 pagesCompany Profile: Kalikasthan, Dillibazar, Kathmandu, Nepal Tel: +977 - 1 - 4442435, 4424743 EmailSaahil GoyalNo ratings yet

- ARNDTECH Solutions Inc ARNDTECH Solutions IncDocument17 pagesARNDTECH Solutions Inc ARNDTECH Solutions IncAmer AliNo ratings yet

- Aicpa Accounting GlossaryDocument24 pagesAicpa Accounting GlossaryRafael AlemanNo ratings yet

- Valuing Private Companies:: Factors and Approaches To ConsiderDocument35 pagesValuing Private Companies:: Factors and Approaches To ConsiderAvinash DasNo ratings yet

- The Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinDocument45 pagesThe Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinSobia NasreenNo ratings yet

- The Time Value of MoneyDocument66 pagesThe Time Value of MoneyrachealllNo ratings yet

- Pre-Money Valuation: Multiple ApproachDocument16 pagesPre-Money Valuation: Multiple ApproachDavid ChikhladzeNo ratings yet

- Pricing Strategy and ManagementDocument15 pagesPricing Strategy and Managementadibhai06No ratings yet

- Discounted Cash Flow ApplicationsDocument27 pagesDiscounted Cash Flow ApplicationsAvinash DasNo ratings yet

- CVP Analysis - 2018Document23 pagesCVP Analysis - 2018Ali KhanNo ratings yet

- Pricing StrategyDocument19 pagesPricing StrategyKamal SinghNo ratings yet

- Module 5 - Game TheoryDocument14 pagesModule 5 - Game Theorychandni_murthy_46404No ratings yet

- Report On New Business Plan: (Mr. Fast Food)Document24 pagesReport On New Business Plan: (Mr. Fast Food)shahidul0No ratings yet

- Workbook On Ratio AnalysisDocument9 pagesWorkbook On Ratio AnalysisZahid HassanNo ratings yet

- HDFC BankDocument39 pagesHDFC BankDurgaprasad VelamalaNo ratings yet

- Financial Desion MakingDocument35 pagesFinancial Desion MakingFrancisca LotraNo ratings yet

- PRAN RFL Ratio AnalysisDocument5 pagesPRAN RFL Ratio AnalysisMasud RanaNo ratings yet

- Master in Business Finance: Praloy Majumder Icai Mumbai May 2010Document38 pagesMaster in Business Finance: Praloy Majumder Icai Mumbai May 2010praloy66No ratings yet

- FCFEDocument7 pagesFCFEbang bebetNo ratings yet

- S12 Retail PricingDocument66 pagesS12 Retail PricingVishnuvardhan Ravichandran0% (1)

- Value Chain Analysis of Banana in Bardiya District, NepalDocument1 pageValue Chain Analysis of Banana in Bardiya District, Nepalsachchida sharma0% (1)

- Attitude On Sanitary NapkinsDocument15 pagesAttitude On Sanitary NapkinsMeetika Malhotra100% (2)

- Auditing CA Final Investigation and Due DiligenceDocument26 pagesAuditing CA Final Investigation and Due Diligencevarunmonga90No ratings yet

- Project TimelineDocument4 pagesProject TimelineAnonymous Rr4x3z46JNo ratings yet

- Glossary: Edit Ok: D: K03 Edit Pass SRL/TKB 102 Score 13 CDSDocument11 pagesGlossary: Edit Ok: D: K03 Edit Pass SRL/TKB 102 Score 13 CDSFUCKYOU21170% (1)

- DAIBB Lending - 2 - 0Document8 pagesDAIBB Lending - 2 - 0ashraf294No ratings yet

- Accounting I N ActionDocument38 pagesAccounting I N ActionJr RoqueNo ratings yet

- Fraud Risk FactorsDocument7 pagesFraud Risk FactorsFrancis Azul SimalongNo ratings yet

- Pestle Analysis - Alesh and GroupDocument18 pagesPestle Analysis - Alesh and GroupJay KapoorNo ratings yet

- Fundamental Equity Analysis & Analyst Recommendations - SX5E Eurostoxx 50 Index ComponentsDocument103 pagesFundamental Equity Analysis & Analyst Recommendations - SX5E Eurostoxx 50 Index ComponentsQ.M.S Advisors LLCNo ratings yet

- SMA - Chapter Seven - Cost-Volume-Profit AnalysisDocument35 pagesSMA - Chapter Seven - Cost-Volume-Profit Analysisngandu0% (1)

- NabkisanDocument24 pagesNabkisanDnyaneshwar Dattatraya PhadatareNo ratings yet

- Investor Guide BookDocument169 pagesInvestor Guide BooktonyvinayakNo ratings yet

- Days-Sales-Outstanding-TemplateDocument3 pagesDays-Sales-Outstanding-TemplateKaren Anne Pineda IngenteNo ratings yet

- 6W2X - Business Model Canvas With ExplanationsDocument2 pages6W2X - Business Model Canvas With ExplanationstorqtechNo ratings yet

- Fauji Fertilizer Company Vs Engro Fertilizer CompanyDocument14 pagesFauji Fertilizer Company Vs Engro Fertilizer CompanyArslan Ali Butt100% (1)

- Pricing StrategiesDocument4 pagesPricing StrategiesvinniieeNo ratings yet

- Presentation - On - Companies - Act2013 - K C MehtaDocument116 pagesPresentation - On - Companies - Act2013 - K C MehtasarashviNo ratings yet

- Ration Analysis of M&SDocument72 pagesRation Analysis of M&SRashid JalalNo ratings yet

- Credit RatingDocument28 pagesCredit Ratingak5775No ratings yet

- Pricing StrategiesDocument34 pagesPricing StrategiesshwetambarirupeshNo ratings yet

- CH - 4 - Time Value of MoneyDocument49 pagesCH - 4 - Time Value of Moneyak sNo ratings yet

- Goal Seek in ExcelDocument2 pagesGoal Seek in ExcelsauravnarukaNo ratings yet

- Feasibility Study On New BusinessDocument8 pagesFeasibility Study On New BusinessWyn OkpapiNo ratings yet

- MUG Business Models UplDocument23 pagesMUG Business Models UplChristoph MagistraNo ratings yet

- Cash Flow Forecast, Cost-Benefit Evaluation TechniquesDocument15 pagesCash Flow Forecast, Cost-Benefit Evaluation Techniqueswaqar chNo ratings yet

- Hindustan TimesDocument1 pageHindustan TimesRaviraj0% (1)

- RCF Ratio AnlysisDocument46 pagesRCF Ratio AnlysisAnil KoliNo ratings yet

- Indian Biodegradable Sanitary Napkin Market Price Trends, Demand and Business Opportunities 2024Document3 pagesIndian Biodegradable Sanitary Napkin Market Price Trends, Demand and Business Opportunities 2024anand sahuNo ratings yet

- Val PacketDocument157 pagesVal PacketKumar PrashantNo ratings yet

- FM Assignment - EVA and DuPont Analysis For CompaniesDocument10 pagesFM Assignment - EVA and DuPont Analysis For Companiesamitbharadwaj7No ratings yet

- Sensitivity AnalysisDocument13 pagesSensitivity Analysisrastogi paragNo ratings yet

- Traditional Credit AnalysisDocument1 pageTraditional Credit AnalysisAnkita DasNo ratings yet

- IBDRoadmap PDFDocument7 pagesIBDRoadmap PDFPavitraNo ratings yet

- Corporate BankingDocument57 pagesCorporate BankingSoumya TiwaryNo ratings yet

- Types of Risks in Banking Sector: DR - SMDocument30 pagesTypes of Risks in Banking Sector: DR - SMPriya DharshiniNo ratings yet

- Corporate Banking: by Prof. Santosh KumarDocument58 pagesCorporate Banking: by Prof. Santosh KumarSuraj KumarNo ratings yet

- Corporate Banking: by Prof. Santosh KumarDocument60 pagesCorporate Banking: by Prof. Santosh KumarAditya RajNo ratings yet

- TNB7: Human Resources: Period: 0 TOPSIM - Production & Services Company 1Document1 pageTNB7: Human Resources: Period: 0 TOPSIM - Production & Services Company 1Subhajit KarmakarNo ratings yet

- Kellogg: Balance SheetDocument14 pagesKellogg: Balance SheetSubhajit KarmakarNo ratings yet

- Kellogg PIB 2016Document264 pagesKellogg PIB 2016Subhajit KarmakarNo ratings yet

- The Cost Leadership Strategy: It Is All About Minimizing The Cost of Delivering Products orDocument2 pagesThe Cost Leadership Strategy: It Is All About Minimizing The Cost of Delivering Products orSubhajit KarmakarNo ratings yet

- Gathering and Synthesising Financial and Operating Information About Companies, Industries and GovernmentsDocument1 pageGathering and Synthesising Financial and Operating Information About Companies, Industries and GovernmentsSubhajit KarmakarNo ratings yet

- 07 - Petty Cash Fund and Bank ReconciliationDocument2 pages07 - Petty Cash Fund and Bank ReconciliationCy Miolata100% (2)

- ListDocument6 pagesListkoose340No ratings yet

- USFB Annual ReportDocument149 pagesUSFB Annual Reportvanitha vemulaNo ratings yet

- Terms and Conditions - UCPB Debit CardDocument2 pagesTerms and Conditions - UCPB Debit Cardsky9213100% (2)

- Core Banking PDFDocument2 pagesCore Banking PDFsrimkbNo ratings yet

- Revision Notes For Class 12 Macro Economics Chapter 3 - Free PDF DownloadDocument7 pagesRevision Notes For Class 12 Macro Economics Chapter 3 - Free PDF DownloadVibhuti BatraNo ratings yet

- BZ Maths CHAPTER 1 - Simple Interest IuklDocument25 pagesBZ Maths CHAPTER 1 - Simple Interest Iuklwong peterNo ratings yet

- Central Banking in Pakistan: State Bank of PakistanDocument59 pagesCentral Banking in Pakistan: State Bank of PakistanMuhammad Iqrash Awan87% (15)

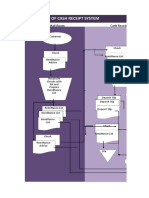

- Flowchart of Cash Receipt System: Mail Room Cash ReceiptsDocument17 pagesFlowchart of Cash Receipt System: Mail Room Cash ReceiptsStephanie Diane SabadoNo ratings yet

- A533XXXXXXXXXXXXX8638 2074324115-UnlockedDocument12 pagesA533XXXXXXXXXXXXX8638 2074324115-Unlockedm3788999No ratings yet

- XboxDocument6 pagesXboxvenipaz63No ratings yet

- PAYROLL PAY N SAVE-i 082020Document1 pagePAYROLL PAY N SAVE-i 082020Nick Ren MicNo ratings yet

- Inflation Targeting Framework: Indonesia in ComparisonDocument25 pagesInflation Targeting Framework: Indonesia in ComparisonPrasya AnindityaNo ratings yet

- Business RegulatoryframeworkDocument28 pagesBusiness Regulatoryframeworknidhi boranaNo ratings yet

- ALW Bank Loan With Real Estate Mortgage TemplateDocument3 pagesALW Bank Loan With Real Estate Mortgage TemplateKikoy IlaganNo ratings yet

- Advance Clearance-Form f00254Document4 pagesAdvance Clearance-Form f00254purnaz100% (2)

- Chennai Metro WaterDocument1 pageChennai Metro WaterlkjdfkallNo ratings yet

- Sanima Bank Intern ReportDocument38 pagesSanima Bank Intern ReportLokesh Bhatta100% (1)

- Maddi Abhilash: Account StatementDocument6 pagesMaddi Abhilash: Account StatementAbhi0% (1)

- International Cash ManagementDocument20 pagesInternational Cash Managementmary aligmayoNo ratings yet

- Demand Letter - QWRDocument3 pagesDemand Letter - QWRj_west30No ratings yet

- Phillipine Banking SystemDocument2 pagesPhillipine Banking SystemPete BasNo ratings yet

- SRF2324 00772454Document1 pageSRF2324 00772454Aman PathakNo ratings yet

- 2021 - Direct Deposit Form - StudentsDocument1 page2021 - Direct Deposit Form - StudentsArmando MaldonadoNo ratings yet

- Swift CodeDocument2 pagesSwift CodeEmmarold OdwongosNo ratings yet

- Mmm-List of DocsDocument8 pagesMmm-List of Docsmadhukar sahayNo ratings yet