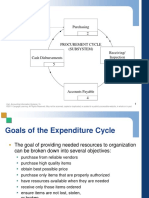

The Expenditure Cycle Part 1: Purchases and Cash Disbursements Procedures

The Expenditure Cycle Part 1: Purchases and Cash Disbursements Procedures

You might also like

- Microeconomics WorkbookDocument46 pagesMicroeconomics Workbookattaullah100% (1)

- Chapter 8Document8 pagesChapter 8Shenne Minglana50% (4)

- Section 2 From Idea To The Opportunity Section 2 From Idea To The OpportunityDocument12 pagesSection 2 From Idea To The Opportunity Section 2 From Idea To The OpportunityJAYANT MAHAJANNo ratings yet

- Question 1 SDocument2 pagesQuestion 1 Sapi-3723783No ratings yet

- Apics CPIM ModuleDocument2 pagesApics CPIM ModuleAvinash DhoneNo ratings yet

- Resource Estimation GuideDocument68 pagesResource Estimation Guideminitaur8No ratings yet

- The Conversion Cycle: Introduction To Accounting Information Systems, 7eDocument44 pagesThe Conversion Cycle: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument38 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresontykerlsNo ratings yet

- Financial Reporting and Management Reporting Systems: Introduction To Accounting Information Systems, 7eDocument14 pagesFinancial Reporting and Management Reporting Systems: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresDocument33 pagesThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresontykerlsNo ratings yet

- The Revenue Cycle: James A. HallDocument91 pagesThe Revenue Cycle: James A. HallAira Rhialyn MangubatNo ratings yet

- Hall Asia Edition PP - ch01Document41 pagesHall Asia Edition PP - ch01Vince Paolo Alicaya AcidoNo ratings yet

- Auditing The Revenue Cycle: Gifari Ahmad Fadhila Jhonysar Akbar Laode M. IkhsanDocument29 pagesAuditing The Revenue Cycle: Gifari Ahmad Fadhila Jhonysar Akbar Laode M. IkhsanHasim kunNo ratings yet

- Ch07 The Conversion Cycle PDFDocument50 pagesCh07 The Conversion Cycle PDFVRNo ratings yet

- Chapter 5 Expenditure Cycle Part 1Document33 pagesChapter 5 Expenditure Cycle Part 1KRIS ANNE SAMUDIO100% (1)

- Fundamentals of Assurance ServicesDocument32 pagesFundamentals of Assurance ServicesDavid alfonsoNo ratings yet

- Chapter 9 Audit of Investing CycleDocument11 pagesChapter 9 Audit of Investing CycleconsulivyNo ratings yet

- AIS Chapter 2Document69 pagesAIS Chapter 2Loren Jel HallareNo ratings yet

- Chapter 4-Auditing Database SystemsDocument37 pagesChapter 4-Auditing Database SystemsMai Thị Ngọc Ánh100% (1)

- Security Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4eDocument34 pagesSecurity Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4eDanna Claire100% (1)

- Gelinas-Dull 8e Chapter 11 Billing & ReceivableDocument30 pagesGelinas-Dull 8e Chapter 11 Billing & Receivableleen mercado100% (1)

- Audit of General Insurance CompaniesDocument16 pagesAudit of General Insurance CompaniesTACS & CO.No ratings yet

- Auditing Inventory, Goods and Services, and Accounts Payable - The Acquisition and Payment CycleDocument64 pagesAuditing Inventory, Goods and Services, and Accounts Payable - The Acquisition and Payment CycleAuliya HafizNo ratings yet

- Us-Conversion CycleDocument3 pagesUs-Conversion CycleThessaloe B. FernandezNo ratings yet

- Chapter 13 Test Bank Romney AisDocument35 pagesChapter 13 Test Bank Romney AisMan Tran Y NhiNo ratings yet

- MAC Material 2Document33 pagesMAC Material 2Blessy Zedlav LacbainNo ratings yet

- Chapter 5 The Expenditure Cycle Part I Purchases and Cash Disbursements Procedures Compiled Detailed ReportDocument23 pagesChapter 5 The Expenditure Cycle Part I Purchases and Cash Disbursements Procedures Compiled Detailed ReportHera Aster LudwigNo ratings yet

- Investment Property Owner Occupied: Theory of Accounts Practical Accounting 1Document4 pagesInvestment Property Owner Occupied: Theory of Accounts Practical Accounting 1hanie lalaNo ratings yet

- Security Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4eDocument63 pagesSecurity Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4ejeanette lampitoc100% (1)

- Hall SM-CH05Document20 pagesHall SM-CH05hassan nassereddineNo ratings yet

- ACP 314 Answer KeyDocument3 pagesACP 314 Answer KeyJastine Rose CañeteNo ratings yet

- Lecture 5 - Computer-Assisted Audit Tools and TechniquesDocument6 pagesLecture 5 - Computer-Assisted Audit Tools and TechniquesViviene Madriaga100% (1)

- c2 Introduction To Transaction ProcessingDocument14 pagesc2 Introduction To Transaction ProcessingLee SuarezNo ratings yet

- Pfrs 2 Share-Based PaymentsDocument3 pagesPfrs 2 Share-Based PaymentsR.A.No ratings yet

- 12 Transaction Processing PDFDocument50 pages12 Transaction Processing PDFkdgNo ratings yet

- 2 Lecture Notes Chapter8 CAATTS Data Extraction AnalysisDocument34 pages2 Lecture Notes Chapter8 CAATTS Data Extraction AnalysisLuka CrosszeriaNo ratings yet

- Auditing IT Governance ControlsDocument31 pagesAuditing IT Governance ControlsAira Belle100% (1)

- AisDocument72 pagesAisShannon MojicaNo ratings yet

- Audit of LiabilitiesDocument12 pagesAudit of LiabilitiesAcier KozukiNo ratings yet

- The Conversion Cycle: Accounting Information Systems, 7eDocument51 pagesThe Conversion Cycle: Accounting Information Systems, 7ebrookeNo ratings yet

- Psa 600Document9 pagesPsa 600Bhebi Dela CruzNo ratings yet

- Accounting Information System - Chapter 5 - ReviewerDocument8 pagesAccounting Information System - Chapter 5 - ReviewerSecret LangNo ratings yet

- Sample Articles of PartnershipDocument57 pagesSample Articles of PartnershipClint Jan SalvañaNo ratings yet

- FM Unit 7 Lecture Notes - Cost of CapitalDocument2 pagesFM Unit 7 Lecture Notes - Cost of CapitalDebbie DebzNo ratings yet

- Credit Managers. Lesson 3Document40 pagesCredit Managers. Lesson 3Joseph PoNo ratings yet

- Ais Chapter 1 and 2 QuizletDocument63 pagesAis Chapter 1 and 2 QuizletVenice Espinoza100% (1)

- Payback Period Method For Capital Budgeting DecisionsDocument5 pagesPayback Period Method For Capital Budgeting DecisionsAmit Kainth100% (1)

- Reviewer Intangible AssetsDocument10 pagesReviewer Intangible AssetsMay100% (1)

- Chapter 14:construct, Deliver, and Maintain Systems ProjectsDocument5 pagesChapter 14:construct, Deliver, and Maintain Systems ProjectsSkyeGalNo ratings yet

- Romney Ais13 PPT 08Document14 pagesRomney Ais13 PPT 08Tamara SaraswatiNo ratings yet

- Internal Control WeaknessesDocument3 pagesInternal Control WeaknessesRosaly JadraqueNo ratings yet

- Internal Control in ActionDocument26 pagesInternal Control in ActionAngel PascuhinNo ratings yet

- Welcome To The Presentation of The: Group 4Document126 pagesWelcome To The Presentation of The: Group 4Ronald Jason RomeroNo ratings yet

- Chapter7 The Conversion CycleDocument15 pagesChapter7 The Conversion CycleAnthonyNo ratings yet

- Philippine Deposit Insurance Corporation (PDIC)Document4 pagesPhilippine Deposit Insurance Corporation (PDIC)Ria Evita RevitaNo ratings yet

- CorporationDocument18 pagesCorporationSarah GoNo ratings yet

- Gramling 9e Auditing Solman Audit SamplingDocument29 pagesGramling 9e Auditing Solman Audit Samplingkimjoonmyeon22100% (1)

- Audit 2 - TheoriesDocument2 pagesAudit 2 - TheoriesJoy ConsigeneNo ratings yet

- Study Notes 4 PAPS 1013Document6 pagesStudy Notes 4 PAPS 1013Francis Ysabella BalagtasNo ratings yet

- Romney Ais13 PPT 13Document11 pagesRomney Ais13 PPT 13Aj PotXzs ÜNo ratings yet

- Ais MidtermDocument5 pagesAis MidtermMosabAbuKhaterNo ratings yet

- CH 05Document27 pagesCH 05Zac VanessaNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument38 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresontykerlsNo ratings yet

- Chapter 5Document41 pagesChapter 5TERRIUS AceNo ratings yet

- Table of ContentDocument15 pagesTable of ContentNarinderjeet KaurNo ratings yet

- Transaction Codes SAP FI BeginnersDocument9 pagesTransaction Codes SAP FI BeginnersWayne WilliamNo ratings yet

- Tax Hand Book - BODocument2 pagesTax Hand Book - BOnmshamim7750No ratings yet

- Initial ResolutionsDocument2 pagesInitial ResolutionsAmitNo ratings yet

- Animation December 2017Document2 pagesAnimation December 2017clay adrianNo ratings yet

- Iso QM Issue IV Rev 04 Dec 21Document105 pagesIso QM Issue IV Rev 04 Dec 21repair sectionNo ratings yet

- Company Profile MPCDocument19 pagesCompany Profile MPCRivki SatriaNo ratings yet

- Case Study Operations Management: NAME: - DateDocument2 pagesCase Study Operations Management: NAME: - DateJohn Delos SantosNo ratings yet

- Principles of Accounts Grade 12 Final BookletDocument24 pagesPrinciples of Accounts Grade 12 Final BookletWisdom Sikanyika100% (2)

- Scrisoare de Intentie EnglezaDocument3 pagesScrisoare de Intentie EnglezaAdrian VasileNo ratings yet

- CV - Ayman Sadiq - 10MSDocument2 pagesCV - Ayman Sadiq - 10MSRaihan Pervez50% (6)

- IC - Pricing Strategy in The Fast Food IndustryDocument27 pagesIC - Pricing Strategy in The Fast Food IndustryRadoslav RobertNo ratings yet

- KPIsDocument15 pagesKPIsShadai RodríguezNo ratings yet

- Ajman Gate BrochureDocument27 pagesAjman Gate BrochureBrand ImpaktNo ratings yet

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocument1 pageOriginal For Recipient Duplicate For Transporter Triplicate For Suppliernitin agrawalNo ratings yet

- Corporate Presentation 2013 Happy Bar & Grill PDFDocument33 pagesCorporate Presentation 2013 Happy Bar & Grill PDFmasterfabbbNo ratings yet

- Contract Period of PKS POLAND 2022 LP Calang PortDocument22 pagesContract Period of PKS POLAND 2022 LP Calang PortDisdikbun acehjaya22No ratings yet

- Icon SCP 11.0 User GuideDocument756 pagesIcon SCP 11.0 User GuideAgnihotri VikasNo ratings yet

- Dubailand Final Case StudyDocument8 pagesDubailand Final Case StudyShubhangMattooNo ratings yet

- Hjalager, A.-M. (2002) - Repairing Innovation Defectiveness in TourismDocument10 pagesHjalager, A.-M. (2002) - Repairing Innovation Defectiveness in TourismthibaultNo ratings yet

- GST-"One Nation, One Market and One Tax" - SWOT ANALYSISDocument7 pagesGST-"One Nation, One Market and One Tax" - SWOT ANALYSISarcherselevatorsNo ratings yet

- Honda Siel Cars India Ltd. ..... PETITIONER (S) Appellant (S) Versus Commissioner of Income Tax, Ghaziabad ..... RESPONDENT (S)Document34 pagesHonda Siel Cars India Ltd. ..... PETITIONER (S) Appellant (S) Versus Commissioner of Income Tax, Ghaziabad ..... RESPONDENT (S)sachinvoraNo ratings yet

- Victoria Vs Inciong Case DigestDocument1 pageVictoria Vs Inciong Case DigestMelody Lim DayagNo ratings yet

- Chapter 5 Legal LiabilityDocument40 pagesChapter 5 Legal LiabilitymperezNo ratings yet

- Format For Send To KCGDocument6 pagesFormat For Send To KCGMayank GandhiNo ratings yet

- 10000016084Document150 pages10000016084Chapter 11 DocketsNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Microeconomics WorkbookDocument46 pagesMicroeconomics Workbookattaullah100% (1)

- Chapter 8Document8 pagesChapter 8Shenne Minglana50% (4)

- Section 2 From Idea To The Opportunity Section 2 From Idea To The OpportunityDocument12 pagesSection 2 From Idea To The Opportunity Section 2 From Idea To The OpportunityJAYANT MAHAJANNo ratings yet

- Question 1 SDocument2 pagesQuestion 1 Sapi-3723783No ratings yet

- Apics CPIM ModuleDocument2 pagesApics CPIM ModuleAvinash DhoneNo ratings yet

- Resource Estimation GuideDocument68 pagesResource Estimation Guideminitaur8No ratings yet

- The Conversion Cycle: Introduction To Accounting Information Systems, 7eDocument44 pagesThe Conversion Cycle: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument38 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresontykerlsNo ratings yet

- Financial Reporting and Management Reporting Systems: Introduction To Accounting Information Systems, 7eDocument14 pagesFinancial Reporting and Management Reporting Systems: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresDocument33 pagesThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresontykerlsNo ratings yet

- The Revenue Cycle: James A. HallDocument91 pagesThe Revenue Cycle: James A. HallAira Rhialyn MangubatNo ratings yet

- Hall Asia Edition PP - ch01Document41 pagesHall Asia Edition PP - ch01Vince Paolo Alicaya AcidoNo ratings yet

- Auditing The Revenue Cycle: Gifari Ahmad Fadhila Jhonysar Akbar Laode M. IkhsanDocument29 pagesAuditing The Revenue Cycle: Gifari Ahmad Fadhila Jhonysar Akbar Laode M. IkhsanHasim kunNo ratings yet

- Ch07 The Conversion Cycle PDFDocument50 pagesCh07 The Conversion Cycle PDFVRNo ratings yet

- Chapter 5 Expenditure Cycle Part 1Document33 pagesChapter 5 Expenditure Cycle Part 1KRIS ANNE SAMUDIO100% (1)

- Fundamentals of Assurance ServicesDocument32 pagesFundamentals of Assurance ServicesDavid alfonsoNo ratings yet

- Chapter 9 Audit of Investing CycleDocument11 pagesChapter 9 Audit of Investing CycleconsulivyNo ratings yet

- AIS Chapter 2Document69 pagesAIS Chapter 2Loren Jel HallareNo ratings yet

- Chapter 4-Auditing Database SystemsDocument37 pagesChapter 4-Auditing Database SystemsMai Thị Ngọc Ánh100% (1)

- Security Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4eDocument34 pagesSecurity Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4eDanna Claire100% (1)

- Gelinas-Dull 8e Chapter 11 Billing & ReceivableDocument30 pagesGelinas-Dull 8e Chapter 11 Billing & Receivableleen mercado100% (1)

- Audit of General Insurance CompaniesDocument16 pagesAudit of General Insurance CompaniesTACS & CO.No ratings yet

- Auditing Inventory, Goods and Services, and Accounts Payable - The Acquisition and Payment CycleDocument64 pagesAuditing Inventory, Goods and Services, and Accounts Payable - The Acquisition and Payment CycleAuliya HafizNo ratings yet

- Us-Conversion CycleDocument3 pagesUs-Conversion CycleThessaloe B. FernandezNo ratings yet

- Chapter 13 Test Bank Romney AisDocument35 pagesChapter 13 Test Bank Romney AisMan Tran Y NhiNo ratings yet

- MAC Material 2Document33 pagesMAC Material 2Blessy Zedlav LacbainNo ratings yet

- Chapter 5 The Expenditure Cycle Part I Purchases and Cash Disbursements Procedures Compiled Detailed ReportDocument23 pagesChapter 5 The Expenditure Cycle Part I Purchases and Cash Disbursements Procedures Compiled Detailed ReportHera Aster LudwigNo ratings yet

- Investment Property Owner Occupied: Theory of Accounts Practical Accounting 1Document4 pagesInvestment Property Owner Occupied: Theory of Accounts Practical Accounting 1hanie lalaNo ratings yet

- Security Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4eDocument63 pagesSecurity Part I: Auditing Operating Systems and Networks: IT Auditing, Hall, 4ejeanette lampitoc100% (1)

- Hall SM-CH05Document20 pagesHall SM-CH05hassan nassereddineNo ratings yet

- ACP 314 Answer KeyDocument3 pagesACP 314 Answer KeyJastine Rose CañeteNo ratings yet

- Lecture 5 - Computer-Assisted Audit Tools and TechniquesDocument6 pagesLecture 5 - Computer-Assisted Audit Tools and TechniquesViviene Madriaga100% (1)

- c2 Introduction To Transaction ProcessingDocument14 pagesc2 Introduction To Transaction ProcessingLee SuarezNo ratings yet

- Pfrs 2 Share-Based PaymentsDocument3 pagesPfrs 2 Share-Based PaymentsR.A.No ratings yet

- 12 Transaction Processing PDFDocument50 pages12 Transaction Processing PDFkdgNo ratings yet

- 2 Lecture Notes Chapter8 CAATTS Data Extraction AnalysisDocument34 pages2 Lecture Notes Chapter8 CAATTS Data Extraction AnalysisLuka CrosszeriaNo ratings yet

- Auditing IT Governance ControlsDocument31 pagesAuditing IT Governance ControlsAira Belle100% (1)

- AisDocument72 pagesAisShannon MojicaNo ratings yet

- Audit of LiabilitiesDocument12 pagesAudit of LiabilitiesAcier KozukiNo ratings yet

- The Conversion Cycle: Accounting Information Systems, 7eDocument51 pagesThe Conversion Cycle: Accounting Information Systems, 7ebrookeNo ratings yet

- Psa 600Document9 pagesPsa 600Bhebi Dela CruzNo ratings yet

- Accounting Information System - Chapter 5 - ReviewerDocument8 pagesAccounting Information System - Chapter 5 - ReviewerSecret LangNo ratings yet

- Sample Articles of PartnershipDocument57 pagesSample Articles of PartnershipClint Jan SalvañaNo ratings yet

- FM Unit 7 Lecture Notes - Cost of CapitalDocument2 pagesFM Unit 7 Lecture Notes - Cost of CapitalDebbie DebzNo ratings yet

- Credit Managers. Lesson 3Document40 pagesCredit Managers. Lesson 3Joseph PoNo ratings yet

- Ais Chapter 1 and 2 QuizletDocument63 pagesAis Chapter 1 and 2 QuizletVenice Espinoza100% (1)

- Payback Period Method For Capital Budgeting DecisionsDocument5 pagesPayback Period Method For Capital Budgeting DecisionsAmit Kainth100% (1)

- Reviewer Intangible AssetsDocument10 pagesReviewer Intangible AssetsMay100% (1)

- Chapter 14:construct, Deliver, and Maintain Systems ProjectsDocument5 pagesChapter 14:construct, Deliver, and Maintain Systems ProjectsSkyeGalNo ratings yet

- Romney Ais13 PPT 08Document14 pagesRomney Ais13 PPT 08Tamara SaraswatiNo ratings yet

- Internal Control WeaknessesDocument3 pagesInternal Control WeaknessesRosaly JadraqueNo ratings yet

- Internal Control in ActionDocument26 pagesInternal Control in ActionAngel PascuhinNo ratings yet

- Welcome To The Presentation of The: Group 4Document126 pagesWelcome To The Presentation of The: Group 4Ronald Jason RomeroNo ratings yet

- Chapter7 The Conversion CycleDocument15 pagesChapter7 The Conversion CycleAnthonyNo ratings yet

- Philippine Deposit Insurance Corporation (PDIC)Document4 pagesPhilippine Deposit Insurance Corporation (PDIC)Ria Evita RevitaNo ratings yet

- CorporationDocument18 pagesCorporationSarah GoNo ratings yet

- Gramling 9e Auditing Solman Audit SamplingDocument29 pagesGramling 9e Auditing Solman Audit Samplingkimjoonmyeon22100% (1)

- Audit 2 - TheoriesDocument2 pagesAudit 2 - TheoriesJoy ConsigeneNo ratings yet

- Study Notes 4 PAPS 1013Document6 pagesStudy Notes 4 PAPS 1013Francis Ysabella BalagtasNo ratings yet

- Romney Ais13 PPT 13Document11 pagesRomney Ais13 PPT 13Aj PotXzs ÜNo ratings yet

- Ais MidtermDocument5 pagesAis MidtermMosabAbuKhaterNo ratings yet

- CH 05Document27 pagesCH 05Zac VanessaNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument38 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresontykerlsNo ratings yet

- Chapter 5Document41 pagesChapter 5TERRIUS AceNo ratings yet

- Table of ContentDocument15 pagesTable of ContentNarinderjeet KaurNo ratings yet

- Transaction Codes SAP FI BeginnersDocument9 pagesTransaction Codes SAP FI BeginnersWayne WilliamNo ratings yet

- Tax Hand Book - BODocument2 pagesTax Hand Book - BOnmshamim7750No ratings yet

- Initial ResolutionsDocument2 pagesInitial ResolutionsAmitNo ratings yet

- Animation December 2017Document2 pagesAnimation December 2017clay adrianNo ratings yet

- Iso QM Issue IV Rev 04 Dec 21Document105 pagesIso QM Issue IV Rev 04 Dec 21repair sectionNo ratings yet

- Company Profile MPCDocument19 pagesCompany Profile MPCRivki SatriaNo ratings yet

- Case Study Operations Management: NAME: - DateDocument2 pagesCase Study Operations Management: NAME: - DateJohn Delos SantosNo ratings yet

- Principles of Accounts Grade 12 Final BookletDocument24 pagesPrinciples of Accounts Grade 12 Final BookletWisdom Sikanyika100% (2)

- Scrisoare de Intentie EnglezaDocument3 pagesScrisoare de Intentie EnglezaAdrian VasileNo ratings yet

- CV - Ayman Sadiq - 10MSDocument2 pagesCV - Ayman Sadiq - 10MSRaihan Pervez50% (6)

- IC - Pricing Strategy in The Fast Food IndustryDocument27 pagesIC - Pricing Strategy in The Fast Food IndustryRadoslav RobertNo ratings yet

- KPIsDocument15 pagesKPIsShadai RodríguezNo ratings yet

- Ajman Gate BrochureDocument27 pagesAjman Gate BrochureBrand ImpaktNo ratings yet

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocument1 pageOriginal For Recipient Duplicate For Transporter Triplicate For Suppliernitin agrawalNo ratings yet

- Corporate Presentation 2013 Happy Bar & Grill PDFDocument33 pagesCorporate Presentation 2013 Happy Bar & Grill PDFmasterfabbbNo ratings yet

- Contract Period of PKS POLAND 2022 LP Calang PortDocument22 pagesContract Period of PKS POLAND 2022 LP Calang PortDisdikbun acehjaya22No ratings yet

- Icon SCP 11.0 User GuideDocument756 pagesIcon SCP 11.0 User GuideAgnihotri VikasNo ratings yet

- Dubailand Final Case StudyDocument8 pagesDubailand Final Case StudyShubhangMattooNo ratings yet

- Hjalager, A.-M. (2002) - Repairing Innovation Defectiveness in TourismDocument10 pagesHjalager, A.-M. (2002) - Repairing Innovation Defectiveness in TourismthibaultNo ratings yet

- GST-"One Nation, One Market and One Tax" - SWOT ANALYSISDocument7 pagesGST-"One Nation, One Market and One Tax" - SWOT ANALYSISarcherselevatorsNo ratings yet

- Honda Siel Cars India Ltd. ..... PETITIONER (S) Appellant (S) Versus Commissioner of Income Tax, Ghaziabad ..... RESPONDENT (S)Document34 pagesHonda Siel Cars India Ltd. ..... PETITIONER (S) Appellant (S) Versus Commissioner of Income Tax, Ghaziabad ..... RESPONDENT (S)sachinvoraNo ratings yet

- Victoria Vs Inciong Case DigestDocument1 pageVictoria Vs Inciong Case DigestMelody Lim DayagNo ratings yet

- Chapter 5 Legal LiabilityDocument40 pagesChapter 5 Legal LiabilitymperezNo ratings yet

- Format For Send To KCGDocument6 pagesFormat For Send To KCGMayank GandhiNo ratings yet

- 10000016084Document150 pages10000016084Chapter 11 DocketsNo ratings yet