Download as pptx, pdf, or txt

You might also like

- My Revision Notes AQA A-Level AccountingDocument183 pagesMy Revision Notes AQA A-Level AccountingKeshinee Sadasing100% (5)

- Group 2 Sec A PLBsearch Growing With LinkedinDocument3 pagesGroup 2 Sec A PLBsearch Growing With LinkedinSheshadri Bhattacharyya0% (2)

- L&T Mindtree Project PresentationDocument8 pagesL&T Mindtree Project PresentationPuneet Agarwal100% (2)

- Indus Tower & Bharti Infratel FinalDocument17 pagesIndus Tower & Bharti Infratel Finalnikita jadhav67% (3)

- Dr. Narendran's DilemmaDocument9 pagesDr. Narendran's DilemmaIndranil Hansda100% (1)

- A Case Brief Lucy V ZehmerDocument3 pagesA Case Brief Lucy V ZehmerGitichekim100% (2)

- Case Analysis American University of Beirut Medical Centre (AUBMC) PACADI FrameworkDocument7 pagesCase Analysis American University of Beirut Medical Centre (AUBMC) PACADI FrameworkAdarsh Nayan100% (1)

- Mindtree and L&TDocument16 pagesMindtree and L&TRohit Verma100% (2)

- STFC X15Document7 pagesSTFC X15Kajol Keshri100% (1)

- CavinKare Private Limited (B) Entry Into Soaps and Detergents MarketDocument2 pagesCavinKare Private Limited (B) Entry Into Soaps and Detergents MarketRaj Paroha71% (7)

- DG Case StudyDocument9 pagesDG Case StudyRitz Tan CadeliñaNo ratings yet

- L&T: Restructuring The Cement BusinessDocument28 pagesL&T: Restructuring The Cement Businessak123umtNo ratings yet

- Organizational Behavior Personal Learning PaperDocument10 pagesOrganizational Behavior Personal Learning PaperNitin Grover100% (3)

- Maruti Manesar Lockout: The Flip Side of People Management: Case Study by Group 9Document7 pagesMaruti Manesar Lockout: The Flip Side of People Management: Case Study by Group 9manik singh100% (1)

- Case Analysis ReportDocument9 pagesCase Analysis Reportchirag shahNo ratings yet

- P&G Case Solution - VMA SubjectDocument2 pagesP&G Case Solution - VMA SubjectSuryakant Burman100% (2)

- Equity Research Report - Maruti SuzukiDocument13 pagesEquity Research Report - Maruti SuzukiShubhan Khan100% (1)

- Training and Development at RvaDocument2 pagesTraining and Development at RvaDipak Thakur100% (1)

- Hero Honda Motors (India) LTD.: Is It Honda That Made It A Hero?Document7 pagesHero Honda Motors (India) LTD.: Is It Honda That Made It A Hero?Tarun GuptaNo ratings yet

- Shree Cement LimitedDocument3 pagesShree Cement LimitedPurushottamSinhaNo ratings yet

- Ultratech JaypeeDocument8 pagesUltratech JaypeeDeepak Badlani0% (1)

- UltraTech Cements and Jaiprakash AssociatesDocument8 pagesUltraTech Cements and Jaiprakash AssociatesanushaNo ratings yet

- Narayana Health: The Initial Ipo DecisionDocument9 pagesNarayana Health: The Initial Ipo DecisionKANVI KAUSHIKNo ratings yet

- Case Study 2Document5 pagesCase Study 2what_the_fukNo ratings yet

- Assignment On Northern Turkey CaseDocument6 pagesAssignment On Northern Turkey CasepeterNo ratings yet

- Multi Tech Case AnalysisDocument1 pageMulti Tech Case AnalysisRit8No ratings yet

- Phaneesh Murthy Sexual Harassment CaseDocument20 pagesPhaneesh Murthy Sexual Harassment CaseJacob Toms NalleparampilNo ratings yet

- Finlatics Sector Project - 1Document2 pagesFinlatics Sector Project - 1Aditya ChitaliyaNo ratings yet

- Central Equipment CompanyDocument6 pagesCentral Equipment CompanySiddhanth MunjalNo ratings yet

- HPCL - Driving Change Through Internal CommunicationDocument4 pagesHPCL - Driving Change Through Internal Communicationsudipta0% (1)

- Industrial Relations at Asian Paints - ePGPX03 - Group - 9Document13 pagesIndustrial Relations at Asian Paints - ePGPX03 - Group - 9manik singh0% (2)

- HDFC Bank LTD.: Research Insight Banking/ Finance SectorDocument9 pagesHDFC Bank LTD.: Research Insight Banking/ Finance SectorDumb LittyNo ratings yet

- Ramesh and Gargi A Case Solution & AnalysisDocument22 pagesRamesh and Gargi A Case Solution & Analysiscikeron503No ratings yet

- Hostile Takeover of MindtreeDocument4 pagesHostile Takeover of Mindtreeanuj rakheja100% (1)

- Regulatory Framework For Merger and AcquisitionDocument5 pagesRegulatory Framework For Merger and AcquisitionkavitaNo ratings yet

- Fima Assignment PDFDocument6 pagesFima Assignment PDFRomi BaaNo ratings yet

- DMart Case Study - Group 06Document3 pagesDMart Case Study - Group 06Siddhi GodeNo ratings yet

- Capital Structure of NTPCDocument49 pagesCapital Structure of NTPCArunKumar100% (1)

- L&T DemergerDocument28 pagesL&T DemergerAmit MehraNo ratings yet

- Growing Financial Services in IndiaDocument9 pagesGrowing Financial Services in Indiaranjeetk_98No ratings yet

- Right Man Wrong JobDocument11 pagesRight Man Wrong JobDharm Pal YadavNo ratings yet

- Ultratech Acquisition of Jaypee CementDocument9 pagesUltratech Acquisition of Jaypee CementAakashNo ratings yet

- 6 Habits of Merely Effective NegotiatorsDocument3 pages6 Habits of Merely Effective NegotiatorsAAMOD KHARB PGP 2018-20 BatchNo ratings yet

- Case US-64 ControversyDocument4 pagesCase US-64 ControversyBiweshNo ratings yet

- Sales and Distribution Management: Project Report On Bajaj Electrical Appliances - FansDocument14 pagesSales and Distribution Management: Project Report On Bajaj Electrical Appliances - Fanssiddhant hingoraniNo ratings yet

- MACR L&T Takeover of MindtreeDocument24 pagesMACR L&T Takeover of Mindtreeswapnil tyagi50% (2)

- Maruti Manesar Lockout: The Flip Side of People Management: Case AnalysisDocument16 pagesMaruti Manesar Lockout: The Flip Side of People Management: Case AnalysisDikshaNo ratings yet

- HDFC-HDFC Bank MergerDocument18 pagesHDFC-HDFC Bank Mergershriramdeshpande431100% (1)

- All You Need To Know About India'S First It Hostile TakeoverintroductionDocument7 pagesAll You Need To Know About India'S First It Hostile TakeoverintroductionKrishna Kant KumarNo ratings yet

- Reliance Merger Case AnalysisDocument3 pagesReliance Merger Case AnalysisCHAITANYA KNo ratings yet

- Group 8 - Case Analysis of Singhania & PartnersDocument8 pagesGroup 8 - Case Analysis of Singhania & PartnersDhawal MamtoraNo ratings yet

- Market Structure of Indian IT Industry-InFOSYSDocument20 pagesMarket Structure of Indian IT Industry-InFOSYSNitin ChidarNo ratings yet

- Tata Motors Cost of CapitalDocument10 pagesTata Motors Cost of CapitalMia KhalifaNo ratings yet

- HULDocument10 pagesHULSALONI GOYALNo ratings yet

- An Irate Distributor: The Question of Profitability: Presented By: Group 10Document13 pagesAn Irate Distributor: The Question of Profitability: Presented By: Group 10Surbhi SabharwalNo ratings yet

- To Study The Capital Structure of Wipro in Comparison To Industry Standard SynopsisDocument4 pagesTo Study The Capital Structure of Wipro in Comparison To Industry Standard SynopsisAssise ThankappanNo ratings yet

- End Point Model CaseDocument8 pagesEnd Point Model CaseSAURAV KUMAR GUPTANo ratings yet

- (EXPLAINED) Larsen & Toubro's Hostile Takeover of Mindtree - Business NewsDocument3 pages(EXPLAINED) Larsen & Toubro's Hostile Takeover of Mindtree - Business NewsSam vermNo ratings yet

- Zee and Sony MergerDocument12 pagesZee and Sony MergerrashmiNo ratings yet

- Expenses Amount: Shashaank Industries Ltd. Profit and Loss Account For The Year Ended 31st March 2006Document6 pagesExpenses Amount: Shashaank Industries Ltd. Profit and Loss Account For The Year Ended 31st March 2006Srijan SaxenaNo ratings yet

- Financial Accounting: Group-1 Industry - Cement Lead Company-Ultratech Cement LTDDocument19 pagesFinancial Accounting: Group-1 Industry - Cement Lead Company-Ultratech Cement LTDArpita GuptaNo ratings yet

- Beml Limited: Annual Report 2012-2013Document162 pagesBeml Limited: Annual Report 2012-2013Nihit SandNo ratings yet

- Khushi - 10.06.22Document3 pagesKhushi - 10.06.22SnehalNo ratings yet

- Site HisabDocument17 pagesSite HisabSnehalNo ratings yet

- Shree Sava Ventures: Particulars Credit Debit Opening Balance 19,225.80Document2 pagesShree Sava Ventures: Particulars Credit Debit Opening Balance 19,225.80SnehalNo ratings yet

- Thakur Institute of Management Studies and Research: A Project Report On Analysis of Financial AnstrunmentsDocument61 pagesThakur Institute of Management Studies and Research: A Project Report On Analysis of Financial AnstrunmentsSnehalNo ratings yet

- Management of Banks & Financial ServicesDocument22 pagesManagement of Banks & Financial ServicesSnehalNo ratings yet

- Modern Corporate Risk Management-WIP 3Document15 pagesModern Corporate Risk Management-WIP 3SnehalNo ratings yet

- Arcelormittal MergerDocument18 pagesArcelormittal MergerSnehalNo ratings yet

- Presented By:: Group No. 6 Name of Student Roll No. TopicDocument18 pagesPresented By:: Group No. 6 Name of Student Roll No. TopicSnehalNo ratings yet

- Chapter 1 - VLE Part 1Document36 pagesChapter 1 - VLE Part 1Roger FernandezNo ratings yet

- TN 44177 - FactoryTalk Alarms & Events Configuration GuideDocument3 pagesTN 44177 - FactoryTalk Alarms & Events Configuration GuideIsaac MendibleNo ratings yet

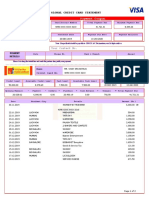

- Credit Card Statement Dated 20122019 PDFDocument3 pagesCredit Card Statement Dated 20122019 PDFvivek srivastavaNo ratings yet

- Motor Vehicle Registration Schedule Based On The Plate NumberDocument2 pagesMotor Vehicle Registration Schedule Based On The Plate NumberJessie Marie dela Peña0% (1)

- Business Ethics 1Document3 pagesBusiness Ethics 1Aravind 9901366442 - 99027872240% (2)

- Sarathi - PCMC Pune EnglishDocument172 pagesSarathi - PCMC Pune EnglishRohan Malik0% (1)

- SIA v. CADocument2 pagesSIA v. CAEmmanuel Princess Zia SalomonNo ratings yet

- EUR Relevé de CompteDocument7 pagesEUR Relevé de Compteandersoneva2003No ratings yet

- @25are Catholic Beliefs and Practices BiblicalDocument3 pages@25are Catholic Beliefs and Practices BiblicalJessie BechaydaNo ratings yet

- FRS 15, Tangible Fixed Assets - Technical Articles - ACCADocument7 pagesFRS 15, Tangible Fixed Assets - Technical Articles - ACCARamen PandeyNo ratings yet

- 32 Garcia Vs Faculty Admission Committee Loyola School of Theology 68 Scra 277Document25 pages32 Garcia Vs Faculty Admission Committee Loyola School of Theology 68 Scra 277LalaLanibaNo ratings yet

- TimkenDocument258 pagesTimkenLuís FerreiraNo ratings yet

- UntitledDocument259 pagesUntitledAnurag KandariNo ratings yet

- Ex 5484Document2 pagesEx 5484Hari Krishnan RNo ratings yet

- Sangeetaben Mahendrabhai Patel v. State of GujaratDocument15 pagesSangeetaben Mahendrabhai Patel v. State of GujaratManushi SaxenaNo ratings yet

- Ownership Structure and Accounting Conservatism ADocument6 pagesOwnership Structure and Accounting Conservatism AFluffy SkinNo ratings yet

- Innocent Mbilinyi, Deceased (1969) HCD 283: HUSTIENE or by Any of The Brothers and SistersDocument2 pagesInnocent Mbilinyi, Deceased (1969) HCD 283: HUSTIENE or by Any of The Brothers and SistersMkushi Fedarh50% (2)

- 602363314Document332 pages602363314chico-tNo ratings yet

- Deed of Absolute Sale 2023Document2 pagesDeed of Absolute Sale 2023John Edward Kenneth Macawili RagazaNo ratings yet

- Appellant's BriefDocument13 pagesAppellant's BriefJojo Navarro100% (1)

- Landlord Tenant Law OutlineDocument6 pagesLandlord Tenant Law OutlineSarah McPherson100% (1)

- Electric Charges and Fields Sub. Test 30th April 2023Document4 pagesElectric Charges and Fields Sub. Test 30th April 2023Rahul pandeyNo ratings yet

- Anatomy of A Market Bottom - CLSADocument21 pagesAnatomy of A Market Bottom - CLSASaeed JafferyNo ratings yet

- Breaking and EnteringDocument1 pageBreaking and EnteringTianaNo ratings yet

- 21 Nigerian LJ308Document24 pages21 Nigerian LJ308Vinay YerubandiNo ratings yet

- Bangladesh Telecommunication Industry-A Comprehensive Review 2019Document14 pagesBangladesh Telecommunication Industry-A Comprehensive Review 2019fullerineNo ratings yet

- Deed of Absolute Sale A SampleDocument4 pagesDeed of Absolute Sale A SampleChrise TalensNo ratings yet

- Rodolfo Abenes Y Gacutan, Petitioner, He Hon. Court of Appeals and People of The Philippines, RespondentsDocument9 pagesRodolfo Abenes Y Gacutan, Petitioner, He Hon. Court of Appeals and People of The Philippines, RespondentsMyka LlagunoNo ratings yet