Introduction To Financial Management: Lecture 2b - Obtaining and Managing Working Capital

Introduction To Financial Management: Lecture 2b - Obtaining and Managing Working Capital

You might also like

- JetBlue IPO Report, Case 28Document10 pagesJetBlue IPO Report, Case 28Adrian Townsend86% (28)

- #Homework Bystra: GOLD Perfect EntryDocument27 pages#Homework Bystra: GOLD Perfect Entrymoitaptrade90% (10)

- Ey Family Office Guide Single FinalDocument64 pagesEy Family Office Guide Single Finalleogonzal100% (3)

- Ratios (Short Interpretations)Document2 pagesRatios (Short Interpretations)iamneonkingNo ratings yet

- Topic 2.0 Evaluation of Financial PerformanceDocument49 pagesTopic 2.0 Evaluation of Financial PerformanceNur ZahirahNo ratings yet

- Types of Securities Equity DebtDocument21 pagesTypes of Securities Equity DebtTeja MullapudiNo ratings yet

- Getting A Grip On Tail SpendDocument12 pagesGetting A Grip On Tail SpendAnamaria Irina Morega100% (1)

- Supply Chain Management Project: Team 1 DMART-Retail Business Analysis Akshaya (08) /ganesh (23) /rengarajanDocument18 pagesSupply Chain Management Project: Team 1 DMART-Retail Business Analysis Akshaya (08) /ganesh (23) /rengarajanAkshaya Lakshminarasimhan80% (5)

- Analyzing AssetsDocument23 pagesAnalyzing AssetsSyed Muhammad Ali OmerNo ratings yet

- Lecture Notes 2 PDFDocument16 pagesLecture Notes 2 PDFRaveesh HurhangeeNo ratings yet

- Short-Term Financial Management: Dr. Del Hawley MBA 622Document27 pagesShort-Term Financial Management: Dr. Del Hawley MBA 622kingleirNo ratings yet

- Week 11-Introduction To Inventory ManagementDocument66 pagesWeek 11-Introduction To Inventory ManagementAdolf AcquayeNo ratings yet

- Strategic Finance Management ppt1Document17 pagesStrategic Finance Management ppt1Ram P100% (1)

- Chapter 2: Securities: Types, Features and ConceptsDocument22 pagesChapter 2: Securities: Types, Features and ConceptsTeja MullapudiNo ratings yet

- Chapter 5 - Purchase - InventoryDocument29 pagesChapter 5 - Purchase - Inventoryhasan jabrNo ratings yet

- R01 The Behavioral Biases of Individuals HY NotesDocument3 pagesR01 The Behavioral Biases of Individuals HY NotesArcadioNo ratings yet

- Analytics Solutions For Retail Banking - MarketelligentDocument25 pagesAnalytics Solutions For Retail Banking - MarketelligentMarketelligentNo ratings yet

- Management of Short Term Assets and Liabilities by P.rai87@gmailDocument22 pagesManagement of Short Term Assets and Liabilities by P.rai87@gmailPRAVEEN RAI100% (4)

- InventoryDocument26 pagesInventoryMayank SharmaNo ratings yet

- L1 R52 HY NotesDocument4 pagesL1 R52 HY Notesayesha ansariNo ratings yet

- What Is Inventory Management?Document31 pagesWhat Is Inventory Management?Naina SobtiNo ratings yet

- Quantitative Models For The Planning and ControlDocument29 pagesQuantitative Models For The Planning and Controlnarandar kumarNo ratings yet

- Sources of Business Finance (Hanith Forman)Document5 pagesSources of Business Finance (Hanith Forman)Hanith Adam FormanNo ratings yet

- S.Chapter 5. WCM and FAMDocument101 pagesS.Chapter 5. WCM and FAMPassionNo ratings yet

- Receivables ManagementDocument37 pagesReceivables Managementchanky_kool8782% (11)

- TFG2971 - 6.15 Transamerica ONE Presentation - DIGITALDocument12 pagesTFG2971 - 6.15 Transamerica ONE Presentation - DIGITALachow04311No ratings yet

- 11 Valuation of Entrepreneurial VenturesDocument15 pages11 Valuation of Entrepreneurial VenturesSatendra JaiswalNo ratings yet

- Cash Receivable and Inventory ManagementDocument39 pagesCash Receivable and Inventory ManagementSophia NicoleNo ratings yet

- Cash Management Problrms SolvedDocument42 pagesCash Management Problrms SolvedKarthikNo ratings yet

- Assignment 2Document8 pagesAssignment 2Shubham RathiNo ratings yet

- BS SCM 7 F23 Procurement Process 10112023 043723pmDocument14 pagesBS SCM 7 F23 Procurement Process 10112023 043723pmAli BajwaNo ratings yet

- Internal - Financing Final MBA 22Document17 pagesInternal - Financing Final MBA 22suparshva99iimNo ratings yet

- BA2088 - Lecture 3 Corporate Credit II - Corporate Credit Analysis Using Financial Statements & RatiosDocument52 pagesBA2088 - Lecture 3 Corporate Credit II - Corporate Credit Analysis Using Financial Statements & RatioskeuqNo ratings yet

- ABL & Factoring Basics 1 PDFDocument146 pagesABL & Factoring Basics 1 PDFDale ChangNo ratings yet

- Borrelli Walsh - 20191111 - Due Diligence For Emerging Markets What WorksDocument3 pagesBorrelli Walsh - 20191111 - Due Diligence For Emerging Markets What WorksImroni PisesaNo ratings yet

- sch1620 - The Capital Structure DecisionDocument145 pagessch1620 - The Capital Structure DecisionApril N. AlfonsoNo ratings yet

- Receivables Management: "Any Fool Can Lend Money, But It TakesDocument37 pagesReceivables Management: "Any Fool Can Lend Money, But It Takesjai262418No ratings yet

- Managing Response To SalesDocument31 pagesManaging Response To SalesAmisha SinghNo ratings yet

- PWC 10minutes DivestituresDocument8 pagesPWC 10minutes DivestituresfuckmegayNo ratings yet

- Working CapitalDocument56 pagesWorking CapitalJuan CarlosNo ratings yet

- 34.scale of OperationsDocument5 pages34.scale of OperationsAndrei PrunilaNo ratings yet

- Workin CapitalDocument17 pagesWorkin CapitalSunnyPawarȜȝNo ratings yet

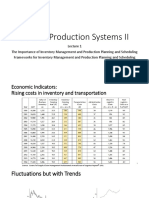

- Chapter 1 Importance of Inventory Management and Production SystemsDocument39 pagesChapter 1 Importance of Inventory Management and Production Systemsjane chahineNo ratings yet

- Summary Chapter 20Document4 pagesSummary Chapter 20Fidelia AgathaNo ratings yet

- Converting Opportunities Into Economic BenefitsDocument10 pagesConverting Opportunities Into Economic BenefitsFlekrer MotaNo ratings yet

- Topic 8 Relevant CostingDocument5 pagesTopic 8 Relevant Costingkimberlyann ongNo ratings yet

- A Project On Supply Chain Management'Document23 pagesA Project On Supply Chain Management'anish_ani777No ratings yet

- Financial Implication of SCM On OrganizationsDocument19 pagesFinancial Implication of SCM On OrganizationsSoorajKrishnanNo ratings yet

- Production PlanningDocument11 pagesProduction PlanningDiana Camily Mesias BahamondeNo ratings yet

- Creating Customer Value and LoyaltyDocument29 pagesCreating Customer Value and LoyaltybakshikamyNo ratings yet

- Nfo Presentation DSP Quant FundDocument26 pagesNfo Presentation DSP Quant FundPrajit NairNo ratings yet

- 29 Business FinanceDocument26 pages29 Business Financeayza.aftab24No ratings yet

- Overtrading Overcapitalization-FinalDocument23 pagesOvertrading Overcapitalization-FinalShsvz SvzuvsvzNo ratings yet

- Receivables Management: "Any Fool Can Lend Money, ButDocument14 pagesReceivables Management: "Any Fool Can Lend Money, ButmanpreetklerNo ratings yet

- Ryanair Company AnalysisDocument12 pagesRyanair Company AnalysisJohn Sebastian Gil (CO)No ratings yet

- PortersDocument1 pagePortersballer0417No ratings yet

- GSLC 8 April LA53Document15 pagesGSLC 8 April LA53dheaNo ratings yet

- Valuation Chapter 3 5 ReviewerDocument4 pagesValuation Chapter 3 5 ReviewerJuday MarquezNo ratings yet

- Far.1 Revision Class Notes 1Document2 pagesFar.1 Revision Class Notes 1Anila NawazNo ratings yet

- Executive's Guide to Fair Value: Profiting from the New Valuation RulesFrom EverandExecutive's Guide to Fair Value: Profiting from the New Valuation RulesNo ratings yet

- Customer Winback: How to Recapture Lost Customers--And Keep Them LoyalFrom EverandCustomer Winback: How to Recapture Lost Customers--And Keep Them LoyalRating: 4 out of 5 stars4/5 (3)

- 2.1 - Definition, Advantages and Functions of Direct MarketingDocument27 pages2.1 - Definition, Advantages and Functions of Direct MarketingMorvinNo ratings yet

- What Does High Net Worth Individual - HNWI Mean?: 51% GowthDocument4 pagesWhat Does High Net Worth Individual - HNWI Mean?: 51% GowthyayhdapuNo ratings yet

- Ctryprem July 21Document176 pagesCtryprem July 21smith100% (1)

- The Dubai International Financial Centre: Databases World Law Multidatabase Search Help FeedbackDocument63 pagesThe Dubai International Financial Centre: Databases World Law Multidatabase Search Help Feedbackabdeali hazariNo ratings yet

- Technopreneurship 10 PDFDocument4 pagesTechnopreneurship 10 PDFjepong100% (1)

- Enron Scandal: About The CompanyDocument5 pagesEnron Scandal: About The Companynidhi nageshNo ratings yet

- Assignment For Week 12 - 2022Document6 pagesAssignment For Week 12 - 2022Rajveer deep100% (1)

- 2007 Resume Book Tuck PDFDocument92 pages2007 Resume Book Tuck PDFpokeefe09No ratings yet

- Maharashtra Tourism 2003Document284 pagesMaharashtra Tourism 2003Mehmood SheikhNo ratings yet

- Armhyla Olivar - Module 6 ActivityDocument3 pagesArmhyla Olivar - Module 6 ActivityGrace Umbaña YangaNo ratings yet

- Are Sellers or Buyers in ControlDocument9 pagesAre Sellers or Buyers in ControlMichael MarioNo ratings yet

- Career in StocksDocument17 pagesCareer in StocksVamsi KrishnaNo ratings yet

- Green Coast DD MOA - FINAL - 09132018Document10 pagesGreen Coast DD MOA - FINAL - 09132018Jerome LeañoNo ratings yet

- Quiz InnovationDocument16 pagesQuiz InnovationMrs Bhawna SinghNo ratings yet

- Double in A Day Forex TechniqueDocument11 pagesDouble in A Day Forex Techniqueabdulrazakyunus75% (4)

- Manager Description PDFDocument3 pagesManager Description PDFyoman777No ratings yet

- Nism Xa Sums and Short Notes 3Document171 pagesNism Xa Sums and Short Notes 3JitendraBhartiNo ratings yet

- Britania ReportDocument26 pagesBritania Reportravi.p23No ratings yet

- Chapter 1 Introduction Pricing As An Element of The Marketing MixDocument6 pagesChapter 1 Introduction Pricing As An Element of The Marketing MixYonneNo ratings yet

- Mgt1022-Lean Startup Management: Project Review 3Document25 pagesMgt1022-Lean Startup Management: Project Review 3Keerthi VasanNo ratings yet

- Arquitos Capital Management - Q3 2014 Investor LetterDocument4 pagesArquitos Capital Management - Q3 2014 Investor LetterCanadianValueNo ratings yet

- Role of Financial IntermediariesDocument5 pagesRole of Financial Intermediarieskevalpatel83No ratings yet

- How To Download Fundamentals of Investing Pearson Series in Finance Ebook PDF Version Ebook PDF Docx Kindle Full ChapterDocument36 pagesHow To Download Fundamentals of Investing Pearson Series in Finance Ebook PDF Version Ebook PDF Docx Kindle Full Chapterannie.root658100% (33)

- State Grid Corporation of ChinaDocument6 pagesState Grid Corporation of Chinasalkaz22432No ratings yet

- Larsen& Toubro LTD Initiating Coverage 15062020Document8 pagesLarsen& Toubro LTD Initiating Coverage 15062020Aparna JRNo ratings yet

- Labour-Based Works Methodology Experiences From ILO: Module 2: Planning, Design, Appraisal and ImplementationDocument46 pagesLabour-Based Works Methodology Experiences From ILO: Module 2: Planning, Design, Appraisal and ImplementationMarvin MessiNo ratings yet

- Investment Attitude QuestionnaireDocument6 pagesInvestment Attitude QuestionnairerakeshmadNo ratings yet

Download as pptx, pdf, or txt

You might also like

- JetBlue IPO Report, Case 28Document10 pagesJetBlue IPO Report, Case 28Adrian Townsend86% (28)

- #Homework Bystra: GOLD Perfect EntryDocument27 pages#Homework Bystra: GOLD Perfect Entrymoitaptrade90% (10)

- Ey Family Office Guide Single FinalDocument64 pagesEy Family Office Guide Single Finalleogonzal100% (3)

- Ratios (Short Interpretations)Document2 pagesRatios (Short Interpretations)iamneonkingNo ratings yet

- Topic 2.0 Evaluation of Financial PerformanceDocument49 pagesTopic 2.0 Evaluation of Financial PerformanceNur ZahirahNo ratings yet

- Types of Securities Equity DebtDocument21 pagesTypes of Securities Equity DebtTeja MullapudiNo ratings yet

- Getting A Grip On Tail SpendDocument12 pagesGetting A Grip On Tail SpendAnamaria Irina Morega100% (1)

- Supply Chain Management Project: Team 1 DMART-Retail Business Analysis Akshaya (08) /ganesh (23) /rengarajanDocument18 pagesSupply Chain Management Project: Team 1 DMART-Retail Business Analysis Akshaya (08) /ganesh (23) /rengarajanAkshaya Lakshminarasimhan80% (5)

- Analyzing AssetsDocument23 pagesAnalyzing AssetsSyed Muhammad Ali OmerNo ratings yet

- Lecture Notes 2 PDFDocument16 pagesLecture Notes 2 PDFRaveesh HurhangeeNo ratings yet

- Short-Term Financial Management: Dr. Del Hawley MBA 622Document27 pagesShort-Term Financial Management: Dr. Del Hawley MBA 622kingleirNo ratings yet

- Week 11-Introduction To Inventory ManagementDocument66 pagesWeek 11-Introduction To Inventory ManagementAdolf AcquayeNo ratings yet

- Strategic Finance Management ppt1Document17 pagesStrategic Finance Management ppt1Ram P100% (1)

- Chapter 2: Securities: Types, Features and ConceptsDocument22 pagesChapter 2: Securities: Types, Features and ConceptsTeja MullapudiNo ratings yet

- Chapter 5 - Purchase - InventoryDocument29 pagesChapter 5 - Purchase - Inventoryhasan jabrNo ratings yet

- R01 The Behavioral Biases of Individuals HY NotesDocument3 pagesR01 The Behavioral Biases of Individuals HY NotesArcadioNo ratings yet

- Analytics Solutions For Retail Banking - MarketelligentDocument25 pagesAnalytics Solutions For Retail Banking - MarketelligentMarketelligentNo ratings yet

- Management of Short Term Assets and Liabilities by P.rai87@gmailDocument22 pagesManagement of Short Term Assets and Liabilities by P.rai87@gmailPRAVEEN RAI100% (4)

- InventoryDocument26 pagesInventoryMayank SharmaNo ratings yet

- L1 R52 HY NotesDocument4 pagesL1 R52 HY Notesayesha ansariNo ratings yet

- What Is Inventory Management?Document31 pagesWhat Is Inventory Management?Naina SobtiNo ratings yet

- Quantitative Models For The Planning and ControlDocument29 pagesQuantitative Models For The Planning and Controlnarandar kumarNo ratings yet

- Sources of Business Finance (Hanith Forman)Document5 pagesSources of Business Finance (Hanith Forman)Hanith Adam FormanNo ratings yet

- S.Chapter 5. WCM and FAMDocument101 pagesS.Chapter 5. WCM and FAMPassionNo ratings yet

- Receivables ManagementDocument37 pagesReceivables Managementchanky_kool8782% (11)

- TFG2971 - 6.15 Transamerica ONE Presentation - DIGITALDocument12 pagesTFG2971 - 6.15 Transamerica ONE Presentation - DIGITALachow04311No ratings yet

- 11 Valuation of Entrepreneurial VenturesDocument15 pages11 Valuation of Entrepreneurial VenturesSatendra JaiswalNo ratings yet

- Cash Receivable and Inventory ManagementDocument39 pagesCash Receivable and Inventory ManagementSophia NicoleNo ratings yet

- Cash Management Problrms SolvedDocument42 pagesCash Management Problrms SolvedKarthikNo ratings yet

- Assignment 2Document8 pagesAssignment 2Shubham RathiNo ratings yet

- BS SCM 7 F23 Procurement Process 10112023 043723pmDocument14 pagesBS SCM 7 F23 Procurement Process 10112023 043723pmAli BajwaNo ratings yet

- Internal - Financing Final MBA 22Document17 pagesInternal - Financing Final MBA 22suparshva99iimNo ratings yet

- BA2088 - Lecture 3 Corporate Credit II - Corporate Credit Analysis Using Financial Statements & RatiosDocument52 pagesBA2088 - Lecture 3 Corporate Credit II - Corporate Credit Analysis Using Financial Statements & RatioskeuqNo ratings yet

- ABL & Factoring Basics 1 PDFDocument146 pagesABL & Factoring Basics 1 PDFDale ChangNo ratings yet

- Borrelli Walsh - 20191111 - Due Diligence For Emerging Markets What WorksDocument3 pagesBorrelli Walsh - 20191111 - Due Diligence For Emerging Markets What WorksImroni PisesaNo ratings yet

- sch1620 - The Capital Structure DecisionDocument145 pagessch1620 - The Capital Structure DecisionApril N. AlfonsoNo ratings yet

- Receivables Management: "Any Fool Can Lend Money, But It TakesDocument37 pagesReceivables Management: "Any Fool Can Lend Money, But It Takesjai262418No ratings yet

- Managing Response To SalesDocument31 pagesManaging Response To SalesAmisha SinghNo ratings yet

- PWC 10minutes DivestituresDocument8 pagesPWC 10minutes DivestituresfuckmegayNo ratings yet

- Working CapitalDocument56 pagesWorking CapitalJuan CarlosNo ratings yet

- 34.scale of OperationsDocument5 pages34.scale of OperationsAndrei PrunilaNo ratings yet

- Workin CapitalDocument17 pagesWorkin CapitalSunnyPawarȜȝNo ratings yet

- Chapter 1 Importance of Inventory Management and Production SystemsDocument39 pagesChapter 1 Importance of Inventory Management and Production Systemsjane chahineNo ratings yet

- Summary Chapter 20Document4 pagesSummary Chapter 20Fidelia AgathaNo ratings yet

- Converting Opportunities Into Economic BenefitsDocument10 pagesConverting Opportunities Into Economic BenefitsFlekrer MotaNo ratings yet

- Topic 8 Relevant CostingDocument5 pagesTopic 8 Relevant Costingkimberlyann ongNo ratings yet

- A Project On Supply Chain Management'Document23 pagesA Project On Supply Chain Management'anish_ani777No ratings yet

- Financial Implication of SCM On OrganizationsDocument19 pagesFinancial Implication of SCM On OrganizationsSoorajKrishnanNo ratings yet

- Production PlanningDocument11 pagesProduction PlanningDiana Camily Mesias BahamondeNo ratings yet

- Creating Customer Value and LoyaltyDocument29 pagesCreating Customer Value and LoyaltybakshikamyNo ratings yet

- Nfo Presentation DSP Quant FundDocument26 pagesNfo Presentation DSP Quant FundPrajit NairNo ratings yet

- 29 Business FinanceDocument26 pages29 Business Financeayza.aftab24No ratings yet

- Overtrading Overcapitalization-FinalDocument23 pagesOvertrading Overcapitalization-FinalShsvz SvzuvsvzNo ratings yet

- Receivables Management: "Any Fool Can Lend Money, ButDocument14 pagesReceivables Management: "Any Fool Can Lend Money, ButmanpreetklerNo ratings yet

- Ryanair Company AnalysisDocument12 pagesRyanair Company AnalysisJohn Sebastian Gil (CO)No ratings yet

- PortersDocument1 pagePortersballer0417No ratings yet

- GSLC 8 April LA53Document15 pagesGSLC 8 April LA53dheaNo ratings yet

- Valuation Chapter 3 5 ReviewerDocument4 pagesValuation Chapter 3 5 ReviewerJuday MarquezNo ratings yet

- Far.1 Revision Class Notes 1Document2 pagesFar.1 Revision Class Notes 1Anila NawazNo ratings yet

- Executive's Guide to Fair Value: Profiting from the New Valuation RulesFrom EverandExecutive's Guide to Fair Value: Profiting from the New Valuation RulesNo ratings yet

- Customer Winback: How to Recapture Lost Customers--And Keep Them LoyalFrom EverandCustomer Winback: How to Recapture Lost Customers--And Keep Them LoyalRating: 4 out of 5 stars4/5 (3)

- 2.1 - Definition, Advantages and Functions of Direct MarketingDocument27 pages2.1 - Definition, Advantages and Functions of Direct MarketingMorvinNo ratings yet

- What Does High Net Worth Individual - HNWI Mean?: 51% GowthDocument4 pagesWhat Does High Net Worth Individual - HNWI Mean?: 51% GowthyayhdapuNo ratings yet

- Ctryprem July 21Document176 pagesCtryprem July 21smith100% (1)

- The Dubai International Financial Centre: Databases World Law Multidatabase Search Help FeedbackDocument63 pagesThe Dubai International Financial Centre: Databases World Law Multidatabase Search Help Feedbackabdeali hazariNo ratings yet

- Technopreneurship 10 PDFDocument4 pagesTechnopreneurship 10 PDFjepong100% (1)

- Enron Scandal: About The CompanyDocument5 pagesEnron Scandal: About The Companynidhi nageshNo ratings yet

- Assignment For Week 12 - 2022Document6 pagesAssignment For Week 12 - 2022Rajveer deep100% (1)

- 2007 Resume Book Tuck PDFDocument92 pages2007 Resume Book Tuck PDFpokeefe09No ratings yet

- Maharashtra Tourism 2003Document284 pagesMaharashtra Tourism 2003Mehmood SheikhNo ratings yet

- Armhyla Olivar - Module 6 ActivityDocument3 pagesArmhyla Olivar - Module 6 ActivityGrace Umbaña YangaNo ratings yet

- Are Sellers or Buyers in ControlDocument9 pagesAre Sellers or Buyers in ControlMichael MarioNo ratings yet

- Career in StocksDocument17 pagesCareer in StocksVamsi KrishnaNo ratings yet

- Green Coast DD MOA - FINAL - 09132018Document10 pagesGreen Coast DD MOA - FINAL - 09132018Jerome LeañoNo ratings yet

- Quiz InnovationDocument16 pagesQuiz InnovationMrs Bhawna SinghNo ratings yet

- Double in A Day Forex TechniqueDocument11 pagesDouble in A Day Forex Techniqueabdulrazakyunus75% (4)

- Manager Description PDFDocument3 pagesManager Description PDFyoman777No ratings yet

- Nism Xa Sums and Short Notes 3Document171 pagesNism Xa Sums and Short Notes 3JitendraBhartiNo ratings yet

- Britania ReportDocument26 pagesBritania Reportravi.p23No ratings yet

- Chapter 1 Introduction Pricing As An Element of The Marketing MixDocument6 pagesChapter 1 Introduction Pricing As An Element of The Marketing MixYonneNo ratings yet

- Mgt1022-Lean Startup Management: Project Review 3Document25 pagesMgt1022-Lean Startup Management: Project Review 3Keerthi VasanNo ratings yet

- Arquitos Capital Management - Q3 2014 Investor LetterDocument4 pagesArquitos Capital Management - Q3 2014 Investor LetterCanadianValueNo ratings yet

- Role of Financial IntermediariesDocument5 pagesRole of Financial Intermediarieskevalpatel83No ratings yet

- How To Download Fundamentals of Investing Pearson Series in Finance Ebook PDF Version Ebook PDF Docx Kindle Full ChapterDocument36 pagesHow To Download Fundamentals of Investing Pearson Series in Finance Ebook PDF Version Ebook PDF Docx Kindle Full Chapterannie.root658100% (33)

- State Grid Corporation of ChinaDocument6 pagesState Grid Corporation of Chinasalkaz22432No ratings yet

- Larsen& Toubro LTD Initiating Coverage 15062020Document8 pagesLarsen& Toubro LTD Initiating Coverage 15062020Aparna JRNo ratings yet

- Labour-Based Works Methodology Experiences From ILO: Module 2: Planning, Design, Appraisal and ImplementationDocument46 pagesLabour-Based Works Methodology Experiences From ILO: Module 2: Planning, Design, Appraisal and ImplementationMarvin MessiNo ratings yet

- Investment Attitude QuestionnaireDocument6 pagesInvestment Attitude QuestionnairerakeshmadNo ratings yet