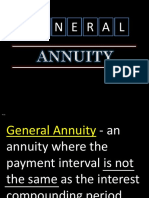

Annuity

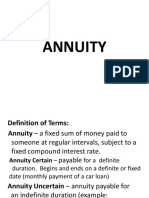

Annuity

You might also like

- 3-10-2021 Receipt Notice I-765 HildaDocument110 pages3-10-2021 Receipt Notice I-765 Hildaeliseo abreuNo ratings yet

- General AnnuitiesDocument141 pagesGeneral AnnuitiesJuanito71% (7)

- MATH 01 Lesson 7 Simple and Compound InterestsDocument34 pagesMATH 01 Lesson 7 Simple and Compound InterestsKen Aguila86% (7)

- Bus. Math Essay Decimal Fraction PercentageDocument1 pageBus. Math Essay Decimal Fraction PercentageLe Gumi100% (2)

- GenMath11 Q2 Mod1 Simple-And-Compound-Interest Ce1ce2Document30 pagesGenMath11 Q2 Mod1 Simple-And-Compound-Interest Ce1ce2Joan Balmes83% (6)

- Chapter 1 - Lesson 1 - Functions As ModelsDocument39 pagesChapter 1 - Lesson 1 - Functions As ModelsMarvin Bustamante100% (3)

- Simple InterestDocument25 pagesSimple InterestRJRegio25% (4)

- Simple InterestDocument95 pagesSimple Interestmaria100% (2)

- GM-Q2-Module 2aDocument19 pagesGM-Q2-Module 2aZandria Camille Delos Santos67% (3)

- Chapter 2 Compound InterestDocument61 pagesChapter 2 Compound InterestSharryne Pador ManabatNo ratings yet

- General Mathematics - Module 6 - Math of InvestmentDocument52 pagesGeneral Mathematics - Module 6 - Math of InvestmentReaper Unseen100% (4)

- GenMath11 - Q2 - Mod5 - Demesa CE 1 Ce 2 EDITEDDocument31 pagesGenMath11 - Q2 - Mod5 - Demesa CE 1 Ce 2 EDITEDAngel Lou Datu50% (6)

- Jan Albert Baluyot Grade 11-St. Andrew: Biogeochemical CycleDocument2 pagesJan Albert Baluyot Grade 11-St. Andrew: Biogeochemical CycleJeffreyMitraNo ratings yet

- Event ProposalDocument30 pagesEvent ProposalDianne Gidayao DacanayNo ratings yet

- AnnuityDocument24 pagesAnnuityMelvel John Nobleza Amarillo100% (2)

- GENMATH - Simple and General AnnuitiesDocument2 pagesGENMATH - Simple and General AnnuitiesBern Balingit-Arnaiz100% (5)

- Compound Interest Rate and TimeDocument18 pagesCompound Interest Rate and TimeRJRegio50% (2)

- Gen Math FinalsDocument48 pagesGen Math Finalsjohn christian de leonNo ratings yet

- #NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToDocument1 page#NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToMikko PerezNo ratings yet

- General Annuity: Future Value Present Value Cash Flow Fair Market ValueDocument7 pagesGeneral Annuity: Future Value Present Value Cash Flow Fair Market ValueReyes C. Ervin0% (1)

- Simple Annuities FinalDocument95 pagesSimple Annuities FinalMae Ann KongNo ratings yet

- GeneralMathematics (SHS) Q2 Mod10 MarketIndicesForStocksAndBonds V1Document26 pagesGeneralMathematics (SHS) Q2 Mod10 MarketIndicesForStocksAndBonds V1Rachael OrtizNo ratings yet

- Compound InterestDocument25 pagesCompound InterestCharlie Anne Padayao0% (2)

- SIMPLE DEFERRED ANNUITY (For DEMO)Document86 pagesSIMPLE DEFERRED ANNUITY (For DEMO)JuanitoNo ratings yet

- The Basic Concepts of LoansDocument27 pagesThe Basic Concepts of LoansAshie-chewNo ratings yet

- 2ND Quarter Modules Gen MathDocument159 pages2ND Quarter Modules Gen MathJester Guballa de LeonNo ratings yet

- GENMATH - Business and Consumer LoansDocument1 pageGENMATH - Business and Consumer LoansBern Balingit-ArnaizNo ratings yet

- SHS General Mathematics Q2 M5Document16 pagesSHS General Mathematics Q2 M5Christian Leimer Gahisan100% (1)

- AnnuityDocument3 pagesAnnuityJeffrey Del Mundo50% (2)

- GM 016 344575 PDFDocument15 pagesGM 016 344575 PDFeunha allaybanNo ratings yet

- General Mathematics: Quarter 2 - Module 7 AnnuitiesDocument40 pagesGeneral Mathematics: Quarter 2 - Module 7 AnnuitiesBreanna CIel E. Cabahit100% (1)

- General Mathematics 2Document11 pagesGeneral Mathematics 2Ryzel Vonne DantesNo ratings yet

- GenMathG11 Q2 Mod8 Basic Concepts of Stocks and Bonds Version2Document25 pagesGenMathG11 Q2 Mod8 Basic Concepts of Stocks and Bonds Version2Glaiza Dalayoan Flores100% (12)

- Simple Annuity 1Document13 pagesSimple Annuity 1Kelvin BarceLon0% (1)

- Simple InterestDocument19 pagesSimple InterestHJNo ratings yet

- Lesson 23 Illustrating Simple and Compound InterestDocument12 pagesLesson 23 Illustrating Simple and Compound InterestANGELIE FERNANDEZNo ratings yet

- Simple Interest ReviewDocument12 pagesSimple Interest ReviewLeciram Santiago MasikipNo ratings yet

- Amortization & Sinking FundDocument27 pagesAmortization & Sinking FundkimNo ratings yet

- Exponential Models: General MathematicsDocument33 pagesExponential Models: General MathematicsJulie Ann Barba TayasNo ratings yet

- General Mathematics 2nd Quarter Module #2Document32 pagesGeneral Mathematics 2nd Quarter Module #2John Lloyd RegalaNo ratings yet

- Module1 - Exponential FunctionsDocument28 pagesModule1 - Exponential Functionsstepharry08No ratings yet

- Grade: Department of Education - Republic of The PhilippinesDocument16 pagesGrade: Department of Education - Republic of The PhilippinesGeraldine Gementiza Poliquit100% (4)

- Chapter 2 Part 1Document42 pagesChapter 2 Part 1Raphael RazonNo ratings yet

- Lesson 1: Fair Market Value of An AnnuityDocument7 pagesLesson 1: Fair Market Value of An AnnuityAlex Albarando SaraososNo ratings yet

- Probability-Chapter 1 Random VariablesDocument92 pagesProbability-Chapter 1 Random VariablesEr Baer80% (5)

- Deferred AnnuityDocument13 pagesDeferred AnnuitySteven Baculanta100% (2)

- Review On Piecewise FunctionsDocument46 pagesReview On Piecewise FunctionsNeil Janas100% (1)

- Pre-Calculus Q2 Module 9Document7 pagesPre-Calculus Q2 Module 9Prince Reinier JonNo ratings yet

- 13 Compound Interest LectureDocument41 pages13 Compound Interest LectureMr.Clown 107No ratings yet

- GM 014 344573 PDFDocument13 pagesGM 014 344573 PDFItsRenz YTNo ratings yet

- General Mathematics: Quarter 2 - Module 14: Simple and Compound PropositionsDocument20 pagesGeneral Mathematics: Quarter 2 - Module 14: Simple and Compound PropositionscsolutionNo ratings yet

- Solving Problems Involving Simple InterestDocument28 pagesSolving Problems Involving Simple InterestCarbon Copy67% (3)

- Simple and Compound InterestDocument47 pagesSimple and Compound InterestCLARENCE AGUDONo ratings yet

- Abm 11 Business Mathematics q1 w3 Mod3Document11 pagesAbm 11 Business Mathematics q1 w3 Mod3Angelica perez100% (1)

- 2nd Quarter Week 3-4Document7 pages2nd Quarter Week 3-4John Clarence89% (9)

- Basic Concepts of Stocks and BondsDocument10 pagesBasic Concepts of Stocks and BondsDaniel De Guzman100% (1)

- Lesson 12 Exponential FunctionDocument34 pagesLesson 12 Exponential FunctionFretchie Anne C. LauroNo ratings yet

- Module 9 - COMPOUND INTERESTDocument15 pagesModule 9 - COMPOUND INTERESTFrancine Yzabelle FugosoNo ratings yet

- GenMath11 Q2 Mod4 Simple and General Annuities Version 1 From CE1 Ce2 EvaluatedDocument28 pagesGenMath11 Q2 Mod4 Simple and General Annuities Version 1 From CE1 Ce2 EvaluatedLorielNo ratings yet

- Simple Annuities PDFDocument6 pagesSimple Annuities PDFNhel AlvaroNo ratings yet

- Time Value of Money 1-1!1!044649Document67 pagesTime Value of Money 1-1!1!044649Yusuph HajiNo ratings yet

- Potato 2Document2 pagesPotato 2JeffreyMitraNo ratings yet

- Personal Development QUARTER 2-Module 17: Teen-Age Relationships Including The Acceptable and Unacceptable Expressions of AttractionsDocument8 pagesPersonal Development QUARTER 2-Module 17: Teen-Age Relationships Including The Acceptable and Unacceptable Expressions of AttractionsJeffreyMitra50% (2)

- 1 WRBSDocument13 pages1 WRBSJeffreyMitraNo ratings yet

- Promotion: Group 2 Jamais Vu EntDocument24 pagesPromotion: Group 2 Jamais Vu EntJeffreyMitraNo ratings yet

- Deformation of The Crust: Sean Gabriel D. Tan Grade 11-STEM St. AndrewDocument2 pagesDeformation of The Crust: Sean Gabriel D. Tan Grade 11-STEM St. AndrewJeffreyMitraNo ratings yet

- All About Climate Change: Group 1 Grade 9 St. ThomasDocument2 pagesAll About Climate Change: Group 1 Grade 9 St. ThomasJeffreyMitraNo ratings yet

- AUTOMATIC TRANSMISSION 6T70 (M7W) - REPAIR INSTRUCTION - OFF VEHICLE-unlockedDocument109 pagesAUTOMATIC TRANSMISSION 6T70 (M7W) - REPAIR INSTRUCTION - OFF VEHICLE-unlockedMarco MeloncelliNo ratings yet

- Big Data and E-Government A ReviewDocument8 pagesBig Data and E-Government A ReviewHelmi ImaduddinNo ratings yet

- Presentation On Institutional Investors Roadshow (Company Update)Document30 pagesPresentation On Institutional Investors Roadshow (Company Update)Shyam SunderNo ratings yet

- Open Sesame: The Rise of Alibaba: After HoursDocument2 pagesOpen Sesame: The Rise of Alibaba: After Hoursa luNo ratings yet

- Q & A ReliablityDocument6 pagesQ & A ReliablitypkcdubNo ratings yet

- Qdoc - Tips - Volvo Penta Installation ManualDocument53 pagesQdoc - Tips - Volvo Penta Installation ManualJorge GomezNo ratings yet

- Environment Management PlanDocument22 pagesEnvironment Management PlanAbir Sengupta100% (2)

- List of Barricades:: Sr. No. Section Line No DescriptionDocument4 pagesList of Barricades:: Sr. No. Section Line No DescriptionSafety DeptNo ratings yet

- VIII Evaluation and ControlDocument2 pagesVIII Evaluation and ControlMadduma, Jeromie G.No ratings yet

- An Overview of Multi-Cloud ComputingDocument12 pagesAn Overview of Multi-Cloud ComputingapesssNo ratings yet

- Practice Manager Job Description - Oct 2019Document3 pagesPractice Manager Job Description - Oct 2019M LubisNo ratings yet

- Phpwyt 7 NaDocument170 pagesPhpwyt 7 Na0176rahulsharmaNo ratings yet

- Pengenalan Safety N Health PDFDocument48 pagesPengenalan Safety N Health PDFwsuzana0% (1)

- Queensland CaseDocument24 pagesQueensland CaseCharlene MiraNo ratings yet

- Day 3Document62 pagesDay 3abdo kasebNo ratings yet

- Hci (Midterm Exam) - Lovely Sarce - BSCS 3a - Naay Watermark Sorry HeheDocument7 pagesHci (Midterm Exam) - Lovely Sarce - BSCS 3a - Naay Watermark Sorry HehePark JiminNo ratings yet

- Project Report GuidelinesDocument8 pagesProject Report GuidelinesHarshil TejaniNo ratings yet

- Akta Koperasi EnglishDocument57 pagesAkta Koperasi EnglishSuraiya Abd RahmanNo ratings yet

- Oracle Golden Gate 11g SyllabusDocument4 pagesOracle Golden Gate 11g SyllabusksknrindianNo ratings yet

- Acctg ResearchDocument38 pagesAcctg ResearchDebbie Grace Latiban LinazaNo ratings yet

- Gr10 Math P1 Nov 2022Document20 pagesGr10 Math P1 Nov 2022samcuthbert4No ratings yet

- Annexure-1 NCR FormDocument1 pageAnnexure-1 NCR FormwaseemhengtongNo ratings yet

- "Pab Rules": Denr - Emb XiDocument38 pages"Pab Rules": Denr - Emb XiLeslie Balneg RubinNo ratings yet

- The Stony Brook Press - Volume 7, Issue 12Document12 pagesThe Stony Brook Press - Volume 7, Issue 12The Stony Brook PressNo ratings yet

- Nagothane Manufacturing Division Summer Internship ReportDocument5 pagesNagothane Manufacturing Division Summer Internship ReportMrudu PadteNo ratings yet

- Nationalism in IndiaDocument9 pagesNationalism in Indiathinkiit0% (1)

- LML 6002 Task 2Document9 pagesLML 6002 Task 2hind.ausNo ratings yet

- 1 Crypt Mausoleum Foundation Plan Rev - New - SanitizedDocument1 page1 Crypt Mausoleum Foundation Plan Rev - New - SanitizedWinmentolMalisa100% (1)

Download as pptx, pdf, or txt

You might also like

- 3-10-2021 Receipt Notice I-765 HildaDocument110 pages3-10-2021 Receipt Notice I-765 Hildaeliseo abreuNo ratings yet

- General AnnuitiesDocument141 pagesGeneral AnnuitiesJuanito71% (7)

- MATH 01 Lesson 7 Simple and Compound InterestsDocument34 pagesMATH 01 Lesson 7 Simple and Compound InterestsKen Aguila86% (7)

- Bus. Math Essay Decimal Fraction PercentageDocument1 pageBus. Math Essay Decimal Fraction PercentageLe Gumi100% (2)

- GenMath11 Q2 Mod1 Simple-And-Compound-Interest Ce1ce2Document30 pagesGenMath11 Q2 Mod1 Simple-And-Compound-Interest Ce1ce2Joan Balmes83% (6)

- Chapter 1 - Lesson 1 - Functions As ModelsDocument39 pagesChapter 1 - Lesson 1 - Functions As ModelsMarvin Bustamante100% (3)

- Simple InterestDocument25 pagesSimple InterestRJRegio25% (4)

- Simple InterestDocument95 pagesSimple Interestmaria100% (2)

- GM-Q2-Module 2aDocument19 pagesGM-Q2-Module 2aZandria Camille Delos Santos67% (3)

- Chapter 2 Compound InterestDocument61 pagesChapter 2 Compound InterestSharryne Pador ManabatNo ratings yet

- General Mathematics - Module 6 - Math of InvestmentDocument52 pagesGeneral Mathematics - Module 6 - Math of InvestmentReaper Unseen100% (4)

- GenMath11 - Q2 - Mod5 - Demesa CE 1 Ce 2 EDITEDDocument31 pagesGenMath11 - Q2 - Mod5 - Demesa CE 1 Ce 2 EDITEDAngel Lou Datu50% (6)

- Jan Albert Baluyot Grade 11-St. Andrew: Biogeochemical CycleDocument2 pagesJan Albert Baluyot Grade 11-St. Andrew: Biogeochemical CycleJeffreyMitraNo ratings yet

- Event ProposalDocument30 pagesEvent ProposalDianne Gidayao DacanayNo ratings yet

- AnnuityDocument24 pagesAnnuityMelvel John Nobleza Amarillo100% (2)

- GENMATH - Simple and General AnnuitiesDocument2 pagesGENMATH - Simple and General AnnuitiesBern Balingit-Arnaiz100% (5)

- Compound Interest Rate and TimeDocument18 pagesCompound Interest Rate and TimeRJRegio50% (2)

- Gen Math FinalsDocument48 pagesGen Math Finalsjohn christian de leonNo ratings yet

- #NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToDocument1 page#NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToMikko PerezNo ratings yet

- General Annuity: Future Value Present Value Cash Flow Fair Market ValueDocument7 pagesGeneral Annuity: Future Value Present Value Cash Flow Fair Market ValueReyes C. Ervin0% (1)

- Simple Annuities FinalDocument95 pagesSimple Annuities FinalMae Ann KongNo ratings yet

- GeneralMathematics (SHS) Q2 Mod10 MarketIndicesForStocksAndBonds V1Document26 pagesGeneralMathematics (SHS) Q2 Mod10 MarketIndicesForStocksAndBonds V1Rachael OrtizNo ratings yet

- Compound InterestDocument25 pagesCompound InterestCharlie Anne Padayao0% (2)

- SIMPLE DEFERRED ANNUITY (For DEMO)Document86 pagesSIMPLE DEFERRED ANNUITY (For DEMO)JuanitoNo ratings yet

- The Basic Concepts of LoansDocument27 pagesThe Basic Concepts of LoansAshie-chewNo ratings yet

- 2ND Quarter Modules Gen MathDocument159 pages2ND Quarter Modules Gen MathJester Guballa de LeonNo ratings yet

- GENMATH - Business and Consumer LoansDocument1 pageGENMATH - Business and Consumer LoansBern Balingit-ArnaizNo ratings yet

- SHS General Mathematics Q2 M5Document16 pagesSHS General Mathematics Q2 M5Christian Leimer Gahisan100% (1)

- AnnuityDocument3 pagesAnnuityJeffrey Del Mundo50% (2)

- GM 016 344575 PDFDocument15 pagesGM 016 344575 PDFeunha allaybanNo ratings yet

- General Mathematics: Quarter 2 - Module 7 AnnuitiesDocument40 pagesGeneral Mathematics: Quarter 2 - Module 7 AnnuitiesBreanna CIel E. Cabahit100% (1)

- General Mathematics 2Document11 pagesGeneral Mathematics 2Ryzel Vonne DantesNo ratings yet

- GenMathG11 Q2 Mod8 Basic Concepts of Stocks and Bonds Version2Document25 pagesGenMathG11 Q2 Mod8 Basic Concepts of Stocks and Bonds Version2Glaiza Dalayoan Flores100% (12)

- Simple Annuity 1Document13 pagesSimple Annuity 1Kelvin BarceLon0% (1)

- Simple InterestDocument19 pagesSimple InterestHJNo ratings yet

- Lesson 23 Illustrating Simple and Compound InterestDocument12 pagesLesson 23 Illustrating Simple and Compound InterestANGELIE FERNANDEZNo ratings yet

- Simple Interest ReviewDocument12 pagesSimple Interest ReviewLeciram Santiago MasikipNo ratings yet

- Amortization & Sinking FundDocument27 pagesAmortization & Sinking FundkimNo ratings yet

- Exponential Models: General MathematicsDocument33 pagesExponential Models: General MathematicsJulie Ann Barba TayasNo ratings yet

- General Mathematics 2nd Quarter Module #2Document32 pagesGeneral Mathematics 2nd Quarter Module #2John Lloyd RegalaNo ratings yet

- Module1 - Exponential FunctionsDocument28 pagesModule1 - Exponential Functionsstepharry08No ratings yet

- Grade: Department of Education - Republic of The PhilippinesDocument16 pagesGrade: Department of Education - Republic of The PhilippinesGeraldine Gementiza Poliquit100% (4)

- Chapter 2 Part 1Document42 pagesChapter 2 Part 1Raphael RazonNo ratings yet

- Lesson 1: Fair Market Value of An AnnuityDocument7 pagesLesson 1: Fair Market Value of An AnnuityAlex Albarando SaraososNo ratings yet

- Probability-Chapter 1 Random VariablesDocument92 pagesProbability-Chapter 1 Random VariablesEr Baer80% (5)

- Deferred AnnuityDocument13 pagesDeferred AnnuitySteven Baculanta100% (2)

- Review On Piecewise FunctionsDocument46 pagesReview On Piecewise FunctionsNeil Janas100% (1)

- Pre-Calculus Q2 Module 9Document7 pagesPre-Calculus Q2 Module 9Prince Reinier JonNo ratings yet

- 13 Compound Interest LectureDocument41 pages13 Compound Interest LectureMr.Clown 107No ratings yet

- GM 014 344573 PDFDocument13 pagesGM 014 344573 PDFItsRenz YTNo ratings yet

- General Mathematics: Quarter 2 - Module 14: Simple and Compound PropositionsDocument20 pagesGeneral Mathematics: Quarter 2 - Module 14: Simple and Compound PropositionscsolutionNo ratings yet

- Solving Problems Involving Simple InterestDocument28 pagesSolving Problems Involving Simple InterestCarbon Copy67% (3)

- Simple and Compound InterestDocument47 pagesSimple and Compound InterestCLARENCE AGUDONo ratings yet

- Abm 11 Business Mathematics q1 w3 Mod3Document11 pagesAbm 11 Business Mathematics q1 w3 Mod3Angelica perez100% (1)

- 2nd Quarter Week 3-4Document7 pages2nd Quarter Week 3-4John Clarence89% (9)

- Basic Concepts of Stocks and BondsDocument10 pagesBasic Concepts of Stocks and BondsDaniel De Guzman100% (1)

- Lesson 12 Exponential FunctionDocument34 pagesLesson 12 Exponential FunctionFretchie Anne C. LauroNo ratings yet

- Module 9 - COMPOUND INTERESTDocument15 pagesModule 9 - COMPOUND INTERESTFrancine Yzabelle FugosoNo ratings yet

- GenMath11 Q2 Mod4 Simple and General Annuities Version 1 From CE1 Ce2 EvaluatedDocument28 pagesGenMath11 Q2 Mod4 Simple and General Annuities Version 1 From CE1 Ce2 EvaluatedLorielNo ratings yet

- Simple Annuities PDFDocument6 pagesSimple Annuities PDFNhel AlvaroNo ratings yet

- Time Value of Money 1-1!1!044649Document67 pagesTime Value of Money 1-1!1!044649Yusuph HajiNo ratings yet

- Potato 2Document2 pagesPotato 2JeffreyMitraNo ratings yet

- Personal Development QUARTER 2-Module 17: Teen-Age Relationships Including The Acceptable and Unacceptable Expressions of AttractionsDocument8 pagesPersonal Development QUARTER 2-Module 17: Teen-Age Relationships Including The Acceptable and Unacceptable Expressions of AttractionsJeffreyMitra50% (2)

- 1 WRBSDocument13 pages1 WRBSJeffreyMitraNo ratings yet

- Promotion: Group 2 Jamais Vu EntDocument24 pagesPromotion: Group 2 Jamais Vu EntJeffreyMitraNo ratings yet

- Deformation of The Crust: Sean Gabriel D. Tan Grade 11-STEM St. AndrewDocument2 pagesDeformation of The Crust: Sean Gabriel D. Tan Grade 11-STEM St. AndrewJeffreyMitraNo ratings yet

- All About Climate Change: Group 1 Grade 9 St. ThomasDocument2 pagesAll About Climate Change: Group 1 Grade 9 St. ThomasJeffreyMitraNo ratings yet

- AUTOMATIC TRANSMISSION 6T70 (M7W) - REPAIR INSTRUCTION - OFF VEHICLE-unlockedDocument109 pagesAUTOMATIC TRANSMISSION 6T70 (M7W) - REPAIR INSTRUCTION - OFF VEHICLE-unlockedMarco MeloncelliNo ratings yet

- Big Data and E-Government A ReviewDocument8 pagesBig Data and E-Government A ReviewHelmi ImaduddinNo ratings yet

- Presentation On Institutional Investors Roadshow (Company Update)Document30 pagesPresentation On Institutional Investors Roadshow (Company Update)Shyam SunderNo ratings yet

- Open Sesame: The Rise of Alibaba: After HoursDocument2 pagesOpen Sesame: The Rise of Alibaba: After Hoursa luNo ratings yet

- Q & A ReliablityDocument6 pagesQ & A ReliablitypkcdubNo ratings yet

- Qdoc - Tips - Volvo Penta Installation ManualDocument53 pagesQdoc - Tips - Volvo Penta Installation ManualJorge GomezNo ratings yet

- Environment Management PlanDocument22 pagesEnvironment Management PlanAbir Sengupta100% (2)

- List of Barricades:: Sr. No. Section Line No DescriptionDocument4 pagesList of Barricades:: Sr. No. Section Line No DescriptionSafety DeptNo ratings yet

- VIII Evaluation and ControlDocument2 pagesVIII Evaluation and ControlMadduma, Jeromie G.No ratings yet

- An Overview of Multi-Cloud ComputingDocument12 pagesAn Overview of Multi-Cloud ComputingapesssNo ratings yet

- Practice Manager Job Description - Oct 2019Document3 pagesPractice Manager Job Description - Oct 2019M LubisNo ratings yet

- Phpwyt 7 NaDocument170 pagesPhpwyt 7 Na0176rahulsharmaNo ratings yet

- Pengenalan Safety N Health PDFDocument48 pagesPengenalan Safety N Health PDFwsuzana0% (1)

- Queensland CaseDocument24 pagesQueensland CaseCharlene MiraNo ratings yet

- Day 3Document62 pagesDay 3abdo kasebNo ratings yet

- Hci (Midterm Exam) - Lovely Sarce - BSCS 3a - Naay Watermark Sorry HeheDocument7 pagesHci (Midterm Exam) - Lovely Sarce - BSCS 3a - Naay Watermark Sorry HehePark JiminNo ratings yet

- Project Report GuidelinesDocument8 pagesProject Report GuidelinesHarshil TejaniNo ratings yet

- Akta Koperasi EnglishDocument57 pagesAkta Koperasi EnglishSuraiya Abd RahmanNo ratings yet

- Oracle Golden Gate 11g SyllabusDocument4 pagesOracle Golden Gate 11g SyllabusksknrindianNo ratings yet

- Acctg ResearchDocument38 pagesAcctg ResearchDebbie Grace Latiban LinazaNo ratings yet

- Gr10 Math P1 Nov 2022Document20 pagesGr10 Math P1 Nov 2022samcuthbert4No ratings yet

- Annexure-1 NCR FormDocument1 pageAnnexure-1 NCR FormwaseemhengtongNo ratings yet

- "Pab Rules": Denr - Emb XiDocument38 pages"Pab Rules": Denr - Emb XiLeslie Balneg RubinNo ratings yet

- The Stony Brook Press - Volume 7, Issue 12Document12 pagesThe Stony Brook Press - Volume 7, Issue 12The Stony Brook PressNo ratings yet

- Nagothane Manufacturing Division Summer Internship ReportDocument5 pagesNagothane Manufacturing Division Summer Internship ReportMrudu PadteNo ratings yet

- Nationalism in IndiaDocument9 pagesNationalism in Indiathinkiit0% (1)

- LML 6002 Task 2Document9 pagesLML 6002 Task 2hind.ausNo ratings yet

- 1 Crypt Mausoleum Foundation Plan Rev - New - SanitizedDocument1 page1 Crypt Mausoleum Foundation Plan Rev - New - SanitizedWinmentolMalisa100% (1)