Download as pptx, pdf, or txt

You might also like

- Vaidam HealthDocument20 pagesVaidam HealthJai ThakurNo ratings yet

- 1 Economic Influences 2021Document69 pages1 Economic Influences 2021akshatNo ratings yet

- Moriarty Adv-Imc9 Tif ch4Document43 pagesMoriarty Adv-Imc9 Tif ch4devilroksNo ratings yet

- Jasmine Maid Acc 640 Audit Procedures Southern New Hampshire UniversityDocument6 pagesJasmine Maid Acc 640 Audit Procedures Southern New Hampshire UniversityFloyd SeremNo ratings yet

- Single Entry, Cash and Accrual BasisDocument36 pagesSingle Entry, Cash and Accrual BasisAbby Navarro50% (2)

- Cima Edition 13 FullDocument4 pagesCima Edition 13 FullAdil MahmudNo ratings yet

- The Balance Sheet: Task 1Document12 pagesThe Balance Sheet: Task 1Mahmoud EsmaeilNo ratings yet

- 1 D Abmbrc Chap 1 CompressedDocument11 pages1 D Abmbrc Chap 1 CompressedZOEZEL ANNLEIH LAYONGNo ratings yet

- 01.undrstading Financial AccountingDocument27 pages01.undrstading Financial Accountingits4krishna3776No ratings yet

- Session-2 (22-Sep-2013)Document57 pagesSession-2 (22-Sep-2013)Jamal NasirNo ratings yet

- Interview Base - Knowledge & PracticalDocument39 pagesInterview Base - Knowledge & Practicalsonu malikNo ratings yet

- Essentials of Financial Statement AnalysisDocument87 pagesEssentials of Financial Statement AnalysisouzheshiNo ratings yet

- Accounting Analysis FinalDocument10 pagesAccounting Analysis FinalSarwar IqbalNo ratings yet

- 6 THE CHANNEL CONTROL pt2Document2 pages6 THE CHANNEL CONTROL pt2Maverick AlolorNo ratings yet

- Bbap2103 - Management Accounting 2016Document16 pagesBbap2103 - Management Accounting 2016yooheechulNo ratings yet

- Narrative - Assumptions and ISFDocument10 pagesNarrative - Assumptions and ISFKatrizia FauniNo ratings yet

- Financial Reporting Thesis PDFDocument6 pagesFinancial Reporting Thesis PDFUK100% (2)

- Notes On AgribusinessDocument30 pagesNotes On AgribusinessNelgenia Anne GabroninoNo ratings yet

- Similarities Between Management AccountingDocument3 pagesSimilarities Between Management AccountingNurul 'Ain100% (4)

- Chapter 15 Acc Text CasesDocument20 pagesChapter 15 Acc Text CasesHasan PehlivanNo ratings yet

- Introduction To Managerial AccDocument6 pagesIntroduction To Managerial AccNiaz AhmedNo ratings yet

- Financial Statement Analysis: Analysis of The Annual Report of Singapore Airlines For The Year 2020-2021Document11 pagesFinancial Statement Analysis: Analysis of The Annual Report of Singapore Airlines For The Year 2020-2021Pratik GiriNo ratings yet

- Managerial AccountingDocument3 pagesManagerial Accountingujjwal.knsl3803100% (2)

- Cost Management P1Document3 pagesCost Management P1Muzamil LoneNo ratings yet

- MA 6e CH01 WebsiteDocument26 pagesMA 6e CH01 WebsiteSewale AbateNo ratings yet

- Uses of Accounting InformationsDocument2 pagesUses of Accounting InformationsAhmed OusamaNo ratings yet

- Fa - Session 3Document18 pagesFa - Session 3Haroon RasheedNo ratings yet

- HR Score CardDocument12 pagesHR Score CardKAVIVARMA R KNo ratings yet

- Research Paper On Revenue ManagementDocument4 pagesResearch Paper On Revenue Managementafmcueagg100% (1)

- Buy-Side Business Attribution - TABB VersionDocument11 pagesBuy-Side Business Attribution - TABB VersiontabbforumNo ratings yet

- Balanced Scorecard: BY: Purvi Shah (39) (Mms Ii B)Document11 pagesBalanced Scorecard: BY: Purvi Shah (39) (Mms Ii B)purvis15100% (1)

- Gapas, Daniel John L. Financial Management Exercise 1: True or FalseDocument18 pagesGapas, Daniel John L. Financial Management Exercise 1: True or FalseDaniel John GapasNo ratings yet

- Financial Planning PresentationDocument27 pagesFinancial Planning PresentationSeidu AbdullahiNo ratings yet

- Fundamental Accounting Principles: 17 Edition Larson Wild ChiappettaDocument42 pagesFundamental Accounting Principles: 17 Edition Larson Wild ChiappettaAnbuoli ParthasarathyNo ratings yet

- Functions of FinanceDocument4 pagesFunctions of Financemanan mohanNo ratings yet

- Strategy - Chapter 5Document5 pagesStrategy - Chapter 532_one_two_threeNo ratings yet

- ACG3101 Financial Accounting and Reporting 1 Course Study NotesDocument3 pagesACG3101 Financial Accounting and Reporting 1 Course Study NotesJohannes WeinerNo ratings yet

- FDNACCT Reflection Paper PDFDocument4 pagesFDNACCT Reflection Paper PDFCrystal Castor LabragueNo ratings yet

- Submitted by Roshan Shahane (PGPM/0911/029)Document3 pagesSubmitted by Roshan Shahane (PGPM/0911/029)roshanshahaneNo ratings yet

- Strategic Cost Management PrelimDocument6 pagesStrategic Cost Management Prelimailel isagaNo ratings yet

- A Study On Financial Ratio Analysis of Planys Technologies Pvt. LTDDocument24 pagesA Study On Financial Ratio Analysis of Planys Technologies Pvt. LTDshaik.712239No ratings yet

- Accountancy BasicsDocument56 pagesAccountancy BasicsShubham PariharNo ratings yet

- Branch of AccountingDocument33 pagesBranch of AccountingIreneRoseMotasNo ratings yet

- 05 Finance For Strategic Managers V2Document27 pages05 Finance For Strategic Managers V2Renju George100% (1)

- Course: Financial Accounting & AnalysisDocument16 pagesCourse: Financial Accounting & Analysiskarunakar vNo ratings yet

- F5-PM 1Document10 pagesF5-PM 1Amna HussainNo ratings yet

- Group 1 ThesisDocument9 pagesGroup 1 ThesisFallcia B. AranconNo ratings yet

- Sales Management: 1 Compiled by T S Dawar - Sales Management Lecture 7 & 8Document21 pagesSales Management: 1 Compiled by T S Dawar - Sales Management Lecture 7 & 8sagartolaneyNo ratings yet

- MGT. Accounting & Business EnvironmentDocument26 pagesMGT. Accounting & Business Environmentsubu_saxNo ratings yet

- FM Chapter-6Document73 pagesFM Chapter-6Kyla De MesaNo ratings yet

- Difference Between Financial and Managerial AccountingDocument10 pagesDifference Between Financial and Managerial AccountingRahman Sankai KaharuddinNo ratings yet

- Chapter 1Document62 pagesChapter 1Patricia GunawanNo ratings yet

- FC ProjectDocument17 pagesFC Projectutub3abr0No ratings yet

- Assignment On SCMDocument5 pagesAssignment On SCMcattiger123No ratings yet

- FIN Handout BWDocument103 pagesFIN Handout BWnsdchauNo ratings yet

- Leads To Very Poor Manager-Subordinate Relationships Encourages The Manipulation and Misreporting of InformationDocument8 pagesLeads To Very Poor Manager-Subordinate Relationships Encourages The Manipulation and Misreporting of InformationJannatul FerdousyNo ratings yet

- The Balanced Scorecard: A Tool To Implement StrategyDocument39 pagesThe Balanced Scorecard: A Tool To Implement StrategyAilene QuintoNo ratings yet

- The Financial Plan 14 17Document22 pagesThe Financial Plan 14 17Shen AcodesinNo ratings yet

- Components of The Income StatementDocument4 pagesComponents of The Income StatementMel LissaNo ratings yet

- Assignment: Principles of AccountingDocument11 pagesAssignment: Principles of Accountingmudassar saeedNo ratings yet

- The Balanced Scorecard: Turn your data into a roadmap to successFrom EverandThe Balanced Scorecard: Turn your data into a roadmap to successRating: 3.5 out of 5 stars3.5/5 (4)

- Mini Project ReportDocument18 pagesMini Project ReportClash With KAINo ratings yet

- Management Reports Control Reports Performance Evaluation and ManagementDocument43 pagesManagement Reports Control Reports Performance Evaluation and ManagementTricia Marie TumandaNo ratings yet

- Chapter 1: Introduction To Management & OrganizationsDocument15 pagesChapter 1: Introduction To Management & OrganizationsdevilroksNo ratings yet

- Small Business and Entreprenership 1Document11 pagesSmall Business and Entreprenership 1devilroksNo ratings yet

- Small Business and Entreprenership 3Document16 pagesSmall Business and Entreprenership 3devilroksNo ratings yet

- Solomon04 TifDocument19 pagesSolomon04 TifdevilroksNo ratings yet

- Strategies in Action: Strategic Management: Concepts & Cases 12 Edition Fred DavidDocument32 pagesStrategies in Action: Strategic Management: Concepts & Cases 12 Edition Fred DaviddevilroksNo ratings yet

- Solomon01 TifDocument19 pagesSolomon01 TifdevilroksNo ratings yet

- Solomon01 TifDocument19 pagesSolomon01 TifdevilroksNo ratings yet

- Solomon05 TifDocument19 pagesSolomon05 TifdevilroksNo ratings yet

- Solomon04 TifDocument19 pagesSolomon04 TifdevilroksNo ratings yet

- Solomon03 TifDocument18 pagesSolomon03 TifdevilroksNo ratings yet

- Moriarty Adv-Imc9 Tif ch3Document46 pagesMoriarty Adv-Imc9 Tif ch3devilroksNo ratings yet

- Solomon02 TifDocument19 pagesSolomon02 TifdevilroksNo ratings yet

- Tender Document For Purchase Of: Turnkey Project For Supply of STP Tender Number: 6000012984/SAFETY, Dated: 11.05.2019Document51 pagesTender Document For Purchase Of: Turnkey Project For Supply of STP Tender Number: 6000012984/SAFETY, Dated: 11.05.2019aneile liegiseNo ratings yet

- Metro Ridership TrendsDocument10 pagesMetro Ridership TrendsMetro Los AngelesNo ratings yet

- List of Itemized ExpendituresDocument5 pagesList of Itemized ExpendituresRojen YuriNo ratings yet

- Eco QuizDocument5 pagesEco QuizSabbir HassanNo ratings yet

- The Progress To Allow Fully FledgedDocument10 pagesThe Progress To Allow Fully Fledgedtura kedirNo ratings yet

- Unit 3 Capital Structure DecisionsDocument45 pagesUnit 3 Capital Structure DecisionsNaman LadhaNo ratings yet

- List of Headers Associated With PEOn DLTDocument8,197 pagesList of Headers Associated With PEOn DLTLokesh Ranjan KrishNo ratings yet

- The United States Edition of Marketing Management, 14e. 1-1Document133 pagesThe United States Edition of Marketing Management, 14e. 1-1Tauhid Ahmed BappyNo ratings yet

- Midterm - Assignment 1Document2 pagesMidterm - Assignment 1Pearl Dianne PinoteNo ratings yet

- 2 PB 1Document20 pages2 PB 1Ria Idola SurbaktiNo ratings yet

- Political FactorsDocument8 pagesPolitical FactorscebucpatriciaNo ratings yet

- Basic Accounting Lecture 05202018Document188 pagesBasic Accounting Lecture 05202018Rheea de los SantosNo ratings yet

- Invoice 92013866 9100011081 MapalDocument2 pagesInvoice 92013866 9100011081 MapalSaulo TrejoNo ratings yet

- A Synopsis ON "An Analysis of Financial Statements of Icici Bank"Document8 pagesA Synopsis ON "An Analysis of Financial Statements of Icici Bank"tejas0% (1)

- APUSH Industrialization EssayDocument6 pagesAPUSH Industrialization EssayChristopherNo ratings yet

- ORS Making PlantDocument25 pagesORS Making PlantJohn67% (3)

- 183601fb151b9f5741a7fe66505ccc3dDocument35 pages183601fb151b9f5741a7fe66505ccc3dLeonardo BritoNo ratings yet

- Supply Chain Management of Non Perishable GoodsDocument28 pagesSupply Chain Management of Non Perishable GoodsRaj BhalodiaNo ratings yet

- India's IT Infrastructure ServicesDocument27 pagesIndia's IT Infrastructure Servicesmartand86No ratings yet

- Lesson 3 The Firm and Its EnvironmentDocument17 pagesLesson 3 The Firm and Its EnvironmentHeron LacanlaleNo ratings yet

- Cost-Effective Pallet Management StrategiesDocument14 pagesCost-Effective Pallet Management StrategiesSantiago Lara MachadoNo ratings yet

- CPA A 4 Audit EvidenceDocument28 pagesCPA A 4 Audit EvidenceNatasha DeclanNo ratings yet

- Amazon10 09 2022Document7 pagesAmazon10 09 2022ayush bansal100% (1)

- François RufDocument10 pagesFrançois RufJessica AngelinaNo ratings yet

- Amortisations and Sinking FundsDocument7 pagesAmortisations and Sinking FundsChari TawaNo ratings yet

- Acknowledgement of DebtDocument2 pagesAcknowledgement of DebtvernardNo ratings yet

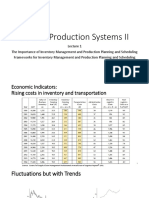

- Chapter 1 Importance of Inventory Management and Production SystemsDocument39 pagesChapter 1 Importance of Inventory Management and Production Systemsjane chahineNo ratings yet