Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- FocusVu Virtual Empowerment CampaignDocument7 pagesFocusVu Virtual Empowerment CampaignBibekbanCheleNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 306 Homework 4 Answers Winter 2017Document4 pages306 Homework 4 Answers Winter 2017Luke HamiltonNo ratings yet

- Nitesh 123Document7 pagesNitesh 123BibekbanCheleNo ratings yet

- Mooc 3Document2 pagesMooc 3BibekbanCheleNo ratings yet

- Results Presentation TemplateDocument8 pagesResults Presentation TemplateBibekbanCheleNo ratings yet

- Like New Phone Paid-Ad Creative BriefDocument6 pagesLike New Phone Paid-Ad Creative BriefBibekbanCheleNo ratings yet

- 2 Writing Test - Chapter 2 - The Global Economy - Quizlet SolutionDocument2 pages2 Writing Test - Chapter 2 - The Global Economy - Quizlet SolutionMia KulalNo ratings yet

- Cas1 Classification of Cost v1Document5 pagesCas1 Classification of Cost v1rajdeeppawarNo ratings yet

- IGBT Plasma Panasonic Placa Ysus IRG4BC40UDocument8 pagesIGBT Plasma Panasonic Placa Ysus IRG4BC40UAntonio ChavezNo ratings yet

- PDF Paper Erwin Diewert 02 05 Measurement AggregateDocument79 pagesPDF Paper Erwin Diewert 02 05 Measurement AggregatehanwaisettNo ratings yet

- CSEC Tourism QuestionDocument2 pagesCSEC Tourism QuestionJohn-Paul Mollineaux0% (1)

- Smart City Mission: Name-Gaurav Tripathi ROLL NO: - 409 SECTION - G (Omega)Document12 pagesSmart City Mission: Name-Gaurav Tripathi ROLL NO: - 409 SECTION - G (Omega)Gaurav TripathiNo ratings yet

- 5-7 Resolution Filling Vacancy On BoardDocument1 page5-7 Resolution Filling Vacancy On BoardDaniel100% (1)

- Form of Application For Registration-Cum-Membership (RCMC) With EEPC INDIA (Formerly Engineering Export Promotion Council)Document4 pagesForm of Application For Registration-Cum-Membership (RCMC) With EEPC INDIA (Formerly Engineering Export Promotion Council)ramsayliving2No ratings yet

- Kavathekar Scribe PDFDocument10 pagesKavathekar Scribe PDFArdit ZotajNo ratings yet

- Aecom ME Handbook 2015Document55 pagesAecom ME Handbook 2015Le'Novo FernandezNo ratings yet

- Introduction To Entrepreneurship: Prof. Pradip P ChatterjjeeDocument19 pagesIntroduction To Entrepreneurship: Prof. Pradip P ChatterjjeeRohit DhoundiyalNo ratings yet

- HSBC iPad-iPod Touch Application FormDocument1 pageHSBC iPad-iPod Touch Application FormBc CyNo ratings yet

- Stages in Implementing Export TransactionDocument19 pagesStages in Implementing Export TransactionGagan KauraNo ratings yet

- AS 26 - 123 To 138Document16 pagesAS 26 - 123 To 138love chawlaNo ratings yet

- History of TakaDocument11 pagesHistory of TakaAnwar HossainNo ratings yet

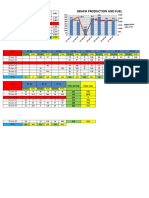

- Production and Fuel Tanggal Produksi Fuel Pagi Malam Total BCMDocument33 pagesProduction and Fuel Tanggal Produksi Fuel Pagi Malam Total BCMPUTRA MAHALONANo ratings yet

- Liquidity As An Investment StyleDocument30 pagesLiquidity As An Investment StyleBurhan SjahNo ratings yet

- Reservations 2Document4 pagesReservations 2Kristina LaovaNo ratings yet

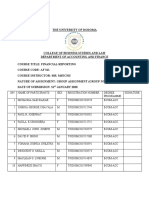

- Financial ReportingDocument7 pagesFinancial ReportingInnocent MollaNo ratings yet

- Tata Corus Case Analysis at GargDocument20 pagesTata Corus Case Analysis at GargNikhil Garg80% (5)

- Soal TOEIC GrammarDocument5 pagesSoal TOEIC GrammarRosman HidayatNo ratings yet

- Krishnaveni Talent School: Ao Visiting ReportDocument4 pagesKrishnaveni Talent School: Ao Visiting ReportgopisrinivasNo ratings yet

- PFMARDocument7 pagesPFMARdonaldhax01100% (1)

- Marketing PlanDocument3 pagesMarketing PlanDENDEN100% (1)

- Afraid To Do Afraid of Doing Afraid To Do Afraid of DoingDocument5 pagesAfraid To Do Afraid of Doing Afraid To Do Afraid of DoingJorge Ponciano AngelesNo ratings yet

- Balance Sheet of Maruti Suzuki IndiaDocument415 pagesBalance Sheet of Maruti Suzuki IndiaMahesh VaiShnavNo ratings yet

- Bid Proposal TemplateDocument3 pagesBid Proposal TemplateGunawan Budi SantosaNo ratings yet

- Network Review: New York City: By: Andrew ThompsonDocument14 pagesNetwork Review: New York City: By: Andrew ThompsonAndrew Thelittleenginethatcould ThompsonNo ratings yet

- Final Presentation: On Comparative Study of Bank's Retail Loan Product at Bank of BarodaDocument11 pagesFinal Presentation: On Comparative Study of Bank's Retail Loan Product at Bank of BarodaPrgya SinghNo ratings yet