Download as ppt, pdf, or txt

You might also like

- Integrated Siting SystemDocument8 pagesIntegrated Siting SystemSahrish Jaleel Shaikh100% (4)

- Dansk Minox Write UpDocument2 pagesDansk Minox Write Upsathwik_mohanNo ratings yet

- Exercises On Tradeoffs and Conflicting ObjectivesDocument9 pagesExercises On Tradeoffs and Conflicting ObjectivesJoel SamuelNo ratings yet

- CLV SonanceDocument5 pagesCLV Sonancegrover.ankush8879No ratings yet

- Cafés Monte Bianco - Questions and Additional DataDocument1 pageCafés Monte Bianco - Questions and Additional DataMarco BolzonelloNo ratings yet

- AJAX OriginalDocument7 pagesAJAX Originalreva_radhakrish1834No ratings yet

- Dansk MinoxDocument1 pageDansk MinoxAksha Anand100% (2)

- Hilton Manufacturing Company 1201326783827489 2Document6 pagesHilton Manufacturing Company 1201326783827489 2Bilal Asim0% (1)

- Case ReichardDocument23 pagesCase ReichardDesiSelviaNo ratings yet

- Balakrishnan MGRL Solutions Ch14Document36 pagesBalakrishnan MGRL Solutions Ch14Aditya Krishna100% (1)

- Natureview Farm Case StudyDocument6 pagesNatureview Farm Case StudysshilawatNo ratings yet

- Reliance Baking Soda - Case ExhibitsDocument5 pagesReliance Baking Soda - Case ExhibitsAnonymous FUZw6z6JN8No ratings yet

- Kodak Funtime MarginsDocument1 pageKodak Funtime Marginsan052091No ratings yet

- Dansk Minox CaseDocument5 pagesDansk Minox CaseGunjan Vishal Tyagi100% (1)

- Soga For Iba Complete NotesDocument12 pagesSoga For Iba Complete Noteshsha mo100% (2)

- A Call For Unity, A Call To Collective ActionDocument3 pagesA Call For Unity, A Call To Collective ActionVen DeeNo ratings yet

- 14 Assignment4Document5 pages14 Assignment4SasisomWilaiwanNo ratings yet

- Becker Textilwerk: Preparation SheetDocument2 pagesBecker Textilwerk: Preparation Sheetabeer fatimaNo ratings yet

- Decision Models and Optimization: Indian School of Business Assignment 4Document8 pagesDecision Models and Optimization: Indian School of Business Assignment 4NANo ratings yet

- Idwest ICE Cream Company: A Case StudyDocument10 pagesIdwest ICE Cream Company: A Case StudyDixie Diana Viquiera FernandezNo ratings yet

- Forner Carpet CompanyDocument7 pagesForner Carpet CompanySimranjeet KaurNo ratings yet

- Hilton Case1Document2 pagesHilton Case1Ana Fernanda Gonzales CaveroNo ratings yet

- Sec A - Group 14 - Migros Turkey - Scaling Online OperationsDocument6 pagesSec A - Group 14 - Migros Turkey - Scaling Online OperationsSrishti JainNo ratings yet

- Case - SunAir Boat Builders Part - 2Document3 pagesCase - SunAir Boat Builders Part - 2dhakar_ravi1No ratings yet

- TAM Analysis of Business ProblemsDocument2 pagesTAM Analysis of Business Problemsgeraldine sandovalNo ratings yet

- Sherman Motor Compant Case Analysis Sherman Motor Compant Case AnalysisDocument5 pagesSherman Motor Compant Case Analysis Sherman Motor Compant Case AnalysisChristian CabariqueNo ratings yet

- Baguette Galore International Ppts FinalDocument23 pagesBaguette Galore International Ppts FinalSadaf KazmiNo ratings yet

- Case Study Synthite Syndicate 5Document1 pageCase Study Synthite Syndicate 5okki hamdaniNo ratings yet

- Natureview Farm - ExcelDocument35 pagesNatureview Farm - ExcelGaurav Suresh YadavNo ratings yet

- DhahranDocument4 pagesDhahranTalha ZubairNo ratings yet

- A Case Analysis: Baldwin Bicycle CompanyDocument12 pagesA Case Analysis: Baldwin Bicycle CompanySamrat KaushikNo ratings yet

- Lehigh Steel Final DocumentDocument6 pagesLehigh Steel Final DocumentSavita SoniNo ratings yet

- Group 7 - Morrissey ForgingsDocument10 pagesGroup 7 - Morrissey ForgingsVishal AgarwalNo ratings yet

- Darby Case ReportDocument23 pagesDarby Case Reportrichiedevil666s100% (1)

- Arkaylite LP02 Wef 09.09.21-1Document2 pagesArkaylite LP02 Wef 09.09.21-1Prateek Agarwal0% (1)

- Blanchard Importing and Distributing Co., Inc.: Setup Cost ErrorDocument3 pagesBlanchard Importing and Distributing Co., Inc.: Setup Cost ErroranushaNo ratings yet

- Case - Demand For Toffe IncDocument16 pagesCase - Demand For Toffe IncSaikat MukherjeeeNo ratings yet

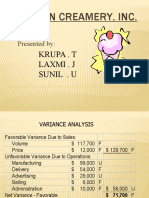

- Boston CreameryDocument11 pagesBoston CreameryJelline Gaza100% (3)

- Group 7 Epgp 28sep PDocument8 pagesGroup 7 Epgp 28sep PPuneet AgarwalNo ratings yet

- EC2101 Practice Problems 8 SolutionDocument3 pagesEC2101 Practice Problems 8 Solutiongravity_coreNo ratings yet

- Case Write-Up: Grocery Gateway: Customer Delivery OperationsDocument4 pagesCase Write-Up: Grocery Gateway: Customer Delivery OperationsCHARANJEET SINGHNo ratings yet

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Worldwide Paper Company: Case Solution Company BackgroundDocument4 pagesWorldwide Paper Company: Case Solution Company BackgroundJauhari WicaksonoNo ratings yet

- Exercise 1 SolnDocument2 pagesExercise 1 Solndarinjohson0% (2)

- Pirelli Supplements TO DODocument8 pagesPirelli Supplements TO DOangie.lopezNo ratings yet

- Baldwin Bicycle CompanyDocument5 pagesBaldwin Bicycle CompanyPremal Gangar0% (1)

- M&A - Valuation - Expanded - BV - SS EQUIPODocument3 pagesM&A - Valuation - Expanded - BV - SS EQUIPOGianina Mendoza NestaresNo ratings yet

- Baria Planning Solutions CaseDocument18 pagesBaria Planning Solutions CaseScribdTranslationsNo ratings yet

- Markstrat Report Round 0-3 Rubicon BravoDocument4 pagesMarkstrat Report Round 0-3 Rubicon BravoDebadatta RathaNo ratings yet

- Group 7 - Excel - Destin BrassDocument9 pagesGroup 7 - Excel - Destin BrassSaumya SahaNo ratings yet

- Case Analysis On Huron Automotive CompanyDocument12 pagesCase Analysis On Huron Automotive CompanyAce ConcepcionNo ratings yet

- Midwest Office Products - AHMDocument4 pagesMidwest Office Products - AHMMSINS SDEDNo ratings yet

- Wilkerson Company Case Numerical Approach SolutionDocument3 pagesWilkerson Company Case Numerical Approach SolutionAbdul Rauf JamroNo ratings yet

- Baldwin Bicycle Company - Group8Document8 pagesBaldwin Bicycle Company - Group8Satyendra ShuklaNo ratings yet

- Bridgeton HWDocument3 pagesBridgeton HWravNo ratings yet

- Krugman2e Solutions CH15Document12 pagesKrugman2e Solutions CH15Joel OettingNo ratings yet

- Price Elasticity of Demand (PED) : The Responsiveness of Quantity Demanded To ChangesDocument5 pagesPrice Elasticity of Demand (PED) : The Responsiveness of Quantity Demanded To Changes7472 VITHALAPARANo ratings yet

- Ped Elasticity ActivitiesDocument5 pagesPed Elasticity ActivitiesSonia HajiyaniNo ratings yet

- Economics Assigment: (Type The Company Name) AcerDocument17 pagesEconomics Assigment: (Type The Company Name) AcerMonty WankharNo ratings yet

- CVP 3 TOM ElpinikiDocument17 pagesCVP 3 TOM ElpinikiPetra SánchezNo ratings yet

- H4Document3 pagesH4Росим ЁдалиNo ratings yet

- Q1 AND Q4 (MCQS)Document3 pagesQ1 AND Q4 (MCQS)Maarij KhanNo ratings yet

- Quiz2 With AnswersDocument9 pagesQuiz2 With Answersprsa2017No ratings yet

- Business Ethics and Relevance in Modern TimesDocument21 pagesBusiness Ethics and Relevance in Modern TimesPooja DaxiniNo ratings yet

- Tendernotice 1Document82 pagesTendernotice 1N5207ACCESSORIES MGRNo ratings yet

- M13 Gitman50803X 14 MF C13Document92 pagesM13 Gitman50803X 14 MF C13sita deliyana FirmialyNo ratings yet

- 2.history and Theories of EntrepreneurshipDocument65 pages2.history and Theories of Entrepreneurshipdeus nyangokoNo ratings yet

- Cash Forcasting GreenhouseDocument1 pageCash Forcasting GreenhouseAdam MirzaNo ratings yet

- PWC The Audit Committees Role in Sustainability Esg OversightDocument10 pagesPWC The Audit Committees Role in Sustainability Esg OversightISabella ARndorferNo ratings yet

- Company Profile of Bank JatimDocument3 pagesCompany Profile of Bank JatimRecette TouileNo ratings yet

- Example Calculation - Import Taxes For A Laptop, Iphone and CameraDocument4 pagesExample Calculation - Import Taxes For A Laptop, Iphone and CameraLalit ChoudharyNo ratings yet

- FINANCIAL MANAGEMENT MODULE 1 6 Capital BudgetingDocument49 pagesFINANCIAL MANAGEMENT MODULE 1 6 Capital BudgetingMarriel Fate CullanoNo ratings yet

- Rrs Local RevisedDocument6 pagesRrs Local RevisedMaria Sienna QassimNo ratings yet

- Money Habits Cheat SheetDocument9 pagesMoney Habits Cheat Sheetned100% (1)

- Management by Objectives (MBO)Document25 pagesManagement by Objectives (MBO)John BerkmansNo ratings yet

- Sub Order LabelsDocument2 pagesSub Order LabelsZeeshan naseemNo ratings yet

- CTT - Donor's TaxDocument8 pagesCTT - Donor's TaxMary Ann GalinatoNo ratings yet

- Quiz 2Document3 pagesQuiz 2Alyssa GervacioNo ratings yet

- Biocon India Case StudyDocument7 pagesBiocon India Case StudyAmit Jha100% (1)

- TD - pwd186928 - Form Karaikudi Testing Track Oct 2021Document57 pagesTD - pwd186928 - Form Karaikudi Testing Track Oct 2021Rishi keshNo ratings yet

- Microeconomics, Module 11: "Monopoly" (Chapter 10) Homework Assignment (The AttachedDocument3 pagesMicroeconomics, Module 11: "Monopoly" (Chapter 10) Homework Assignment (The Attached03137622424No ratings yet

- Act de INFIINTARE (ESTABLISH) Banca Centrala in UGANDA - ROMANIA NU A INFIINTAT BNR (NOT ESTABLISHED)Document26 pagesAct de INFIINTARE (ESTABLISH) Banca Centrala in UGANDA - ROMANIA NU A INFIINTAT BNR (NOT ESTABLISHED)Nicusor TeodorescuNo ratings yet

- Child LabourDocument2 pagesChild LabourAmy JonesNo ratings yet

- Zomato - Market and Consumer Analysis: Aniruddha DeshpandeDocument7 pagesZomato - Market and Consumer Analysis: Aniruddha DeshpandeMonika VermaNo ratings yet

- Audit 2 l2 Test of ControlsDocument45 pagesAudit 2 l2 Test of ControlsGen AbulkhairNo ratings yet

- CommissionDocument4 pagesCommissionArnelson DerechoNo ratings yet

- Year Ended (Audited) Quarter Ended (Unaudited) Nine Months Ended (Unaudited)Document1 pageYear Ended (Audited) Quarter Ended (Unaudited) Nine Months Ended (Unaudited)Jatin GuptaNo ratings yet

- ch14-Off-Balance Sheet ActivitiesDocument15 pagesch14-Off-Balance Sheet ActivitiesYousif Agha100% (3)

- Financial Times UK 2018-05-16Document26 pagesFinancial Times UK 2018-05-16RaycharlesNo ratings yet

- Circular Economy and Innovation Ecosystems The Case of The Italian Circular Economy Stakeholder PlatformDocument17 pagesCircular Economy and Innovation Ecosystems The Case of The Italian Circular Economy Stakeholder Platformms luong mai uyenNo ratings yet