Download as pptx, pdf, or txt

You might also like

- Easy Drive GT20manualV1.1Document102 pagesEasy Drive GT20manualV1.1Musa inverter HouseNo ratings yet

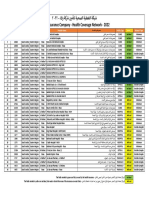

- Walaa Network 2022 شبكة التغطية الصحية-تامين شركة ولاءDocument1 pageWalaa Network 2022 شبكة التغطية الصحية-تامين شركة ولاءMohammed SulimanNo ratings yet

- Finance1 LectureDocument16 pagesFinance1 LectureRegimhel Dalisay75% (4)

- Design Solutions and Innovations in Temporary Structures Robert BealeDocument518 pagesDesign Solutions and Innovations in Temporary Structures Robert Bealerenzo divendra100% (1)

- Federal Reserve Bank - Two Faces of DebtDocument28 pagesFederal Reserve Bank - Two Faces of Debtpwilkers36100% (1)

- MGT 201-Business Communication (SUN 1:30-4:30)Document5 pagesMGT 201-Business Communication (SUN 1:30-4:30)AndreaNicoleAurelioNo ratings yet

- DASA - DevOps Fundamentals Mock ExamDocument22 pagesDASA - DevOps Fundamentals Mock ExamUnes WachaouNo ratings yet

- FM 303 Chapter 1Document9 pagesFM 303 Chapter 1Eve HittyNo ratings yet

- 1.a. PPT1 CR COLL Nature and Functions of CreditDocument41 pages1.a. PPT1 CR COLL Nature and Functions of CreditRoi Martin A. De VeyraNo ratings yet

- Financial Markets Chapter 4 CreditsDocument4 pagesFinancial Markets Chapter 4 CreditsJireh Albay100% (1)

- Uses, Classification of CreditDocument29 pagesUses, Classification of CreditEi-Ei EsguerraNo ratings yet

- Overview of CreditDocument15 pagesOverview of CreditJohn Daniel BerdosNo ratings yet

- Module 4 - Credit, Its Uses, Classifications and Risks PDFDocument17 pagesModule 4 - Credit, Its Uses, Classifications and Risks PDFRodel Novesteras Claus0% (1)

- Canilang, Julius Ceasar Duarte, Mary Lyn Flores, John Robin: Name: Betiola, Rachelle AnnDocument8 pagesCanilang, Julius Ceasar Duarte, Mary Lyn Flores, John Robin: Name: Betiola, Rachelle AnnMary Lyn DuarteNo ratings yet

- Classification of CreditDocument25 pagesClassification of CreditJohn Nikko LlaneraNo ratings yet

- Classess and Kinds of CreditDocument4 pagesClassess and Kinds of CreditJimuel FaigaoNo ratings yet

- Credit ManagementDocument9 pagesCredit ManagementMorris MusvavairiNo ratings yet

- Loans& AdvancesDocument80 pagesLoans& AdvancesSatyajit Naik100% (2)

- Overview of CreditDocument24 pagesOverview of CreditJanell AgananNo ratings yet

- The Need For A System of Credit: People Buy Things That They Cannot Afford To Pay For at The Moment, But Probably Can Pay For in The Long RunDocument63 pagesThe Need For A System of Credit: People Buy Things That They Cannot Afford To Pay For at The Moment, But Probably Can Pay For in The Long RunjaneNo ratings yet

- BANKING Philippine Credit SystemDocument13 pagesBANKING Philippine Credit SystemTim MagalingNo ratings yet

- Bank Credit Loans TrustDocument8 pagesBank Credit Loans TrustN.O. Vista100% (1)

- Chapter Vi - Classification of Credit & Their SourcerDocument4 pagesChapter Vi - Classification of Credit & Their Sourcermark_torreonNo ratings yet

- Credit InstrumentsDocument21 pagesCredit InstrumentsJoann Sacol100% (1)

- Credit SystemDocument57 pagesCredit SystemHakdog CheeseNo ratings yet

- Developing Understanding of Debt and Consumer CreditDocument42 pagesDeveloping Understanding of Debt and Consumer CreditMelkamu EndaleNo ratings yet

- The Credit SystemDocument6 pagesThe Credit SystemJamil MacabandingNo ratings yet

- Business and Consumer Loan: What Is The Difference Between Bonds and Loans?Document10 pagesBusiness and Consumer Loan: What Is The Difference Between Bonds and Loans?Dandreb SardanNo ratings yet

- Final Project Thanuja Vehicle LoanDocument88 pagesFinal Project Thanuja Vehicle LoanRakeshNo ratings yet

- TYPES OF CREDIT Week13Document61 pagesTYPES OF CREDIT Week13Richard Santiago JimenezNo ratings yet

- CBM AssignmentDocument6 pagesCBM AssignmentNimit BhatiaNo ratings yet

- UNIT 2 Process and DocumentationDocument27 pagesUNIT 2 Process and DocumentationAroop PalNo ratings yet

- Bank CreditDocument5 pagesBank Creditnhan thanhNo ratings yet

- Propos LDocument19 pagesPropos LEyerus MulugetaNo ratings yet

- Chapter Vi: Classification of Credit and Their ResourcesDocument5 pagesChapter Vi: Classification of Credit and Their Resourcesfsfsfsfs asdfsfsNo ratings yet

- Introduction:-: Establishment For Custody of Money, Which It Pays Out On Customer's Order."Document12 pagesIntroduction:-: Establishment For Custody of Money, Which It Pays Out On Customer's Order."varunNo ratings yet

- Different Types OF: Loans and AdvancesDocument19 pagesDifferent Types OF: Loans and Advancesharesh KNo ratings yet

- Credit and Collection Week 4Document69 pagesCredit and Collection Week 4ephesians320laiNo ratings yet

- Credit and Collection ActivityDocument4 pagesCredit and Collection ActivityAngelouNo ratings yet

- CreditDocument31 pagesCreditErnelyn Fe T. TuseNo ratings yet

- Types of Credit BSBA 3B, GROUP 2Document20 pagesTypes of Credit BSBA 3B, GROUP 2Rizzle RabadillaNo ratings yet

- Banking FinanceDocument9 pagesBanking FinanceAstik TripathiNo ratings yet

- The Repayment of The Loan Depends Upon The BorrowerDocument4 pagesThe Repayment of The Loan Depends Upon The BorrowerSadia Rahman100% (1)

- Types of LoansDocument16 pagesTypes of LoansHardik PatelNo ratings yet

- Finance ReviewerDocument28 pagesFinance ReviewerZariah GtNo ratings yet

- Credit Distinguished From DebtDocument3 pagesCredit Distinguished From DebtDIASANTA Gene Kenneth C.No ratings yet

- Dipali Project ReportDocument58 pagesDipali Project ReportAshish MOHARENo ratings yet

- Unit 3 Letter of Credit and Loan CommitmentsDocument10 pagesUnit 3 Letter of Credit and Loan Commitmentssaurabh thakurNo ratings yet

- Written Report in Entreprenuerial MindDocument21 pagesWritten Report in Entreprenuerial MindAndrea OrbisoNo ratings yet

- Written Report in Entreprenuerial MindDocument21 pagesWritten Report in Entreprenuerial MindAndrea OrbisoNo ratings yet

- DMMF Cia 3-1 (1720552)Document17 pagesDMMF Cia 3-1 (1720552)Prarthana MNo ratings yet

- What Is 'Education Loan': An Introduction To Student Loans and The FAFSA College Loans: Private vs. FederalDocument18 pagesWhat Is 'Education Loan': An Introduction To Student Loans and The FAFSA College Loans: Private vs. FederalvaishaliNo ratings yet

- Adverse Selection & Moral HazardDocument4 pagesAdverse Selection & Moral HazardAJAY KUMAR SAHUNo ratings yet

- 02 Credit System - PDFDocument49 pages02 Credit System - PDFsharmaine gonzagaNo ratings yet

- Full Notes MBF22408T Credit Risk and Recovery ManagementDocument90 pagesFull Notes MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Unit I MBF22408T Credit Risk and Recovery ManagementDocument17 pagesUnit I MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Unit 05 - Principles of Bank LendingDocument18 pagesUnit 05 - Principles of Bank LendingSayak GhoshNo ratings yet

- Unit 1 Consumer Credit & DebtDocument9 pagesUnit 1 Consumer Credit & DebtDanoNo ratings yet

- Lending OperationsDocument54 pagesLending OperationsFaraz Ahmed FarooqiNo ratings yet

- Consumer Credit February 14, 2011Document23 pagesConsumer Credit February 14, 2011arithzNo ratings yet

- FINANCIAL CREDIT RISK ANALYTICS - Unit 1Document11 pagesFINANCIAL CREDIT RISK ANALYTICS - Unit 1Mansi sharmaNo ratings yet

- Credit and Collection Finmgt3: A Self-Regulated Learning ModuleDocument8 pagesCredit and Collection Finmgt3: A Self-Regulated Learning ModuleGenesis JavierNo ratings yet

- US Consumer Debt Relief: Industry, Overview, Laws & RegulationsFrom EverandUS Consumer Debt Relief: Industry, Overview, Laws & RegulationsNo ratings yet

- GCAS 17 - PE-3 Dance/Swimming (FRI 1:30-3:30) : Basic Folk Dance Terms BrushDocument3 pagesGCAS 17 - PE-3 Dance/Swimming (FRI 1:30-3:30) : Basic Folk Dance Terms BrushAndreaNicoleAurelioNo ratings yet

- GCAS 17-PE 3 - Swimming/DanceDocument9 pagesGCAS 17-PE 3 - Swimming/DanceAndreaNicoleAurelioNo ratings yet

- Theoretical Orientation To DanceDocument8 pagesTheoretical Orientation To DanceAndreaNicoleAurelioNo ratings yet

- Lesson 3 (Philippine Folk Dance) CariñosaDocument5 pagesLesson 3 (Philippine Folk Dance) CariñosaAndreaNicoleAurelioNo ratings yet

- MGT 201 - Business Communication: Business Communication Is The Process of Sharing Information Between People Within andDocument3 pagesMGT 201 - Business Communication: Business Communication Is The Process of Sharing Information Between People Within andAndreaNicoleAurelioNo ratings yet

- Intellectual Revolution That Defines Society in AsiaDocument20 pagesIntellectual Revolution That Defines Society in AsiaAndreaNicoleAurelioNo ratings yet

- EEN 443: Power Distribution Research Assignment: Mohammed Riad Elchadli Mohammed Shiful Maged Al SharafiDocument4 pagesEEN 443: Power Distribution Research Assignment: Mohammed Riad Elchadli Mohammed Shiful Maged Al SharafiMohammed ShifulNo ratings yet

- Metode Data Mining SomDocument22 pagesMetode Data Mining SomAnonymous N22g3i4No ratings yet

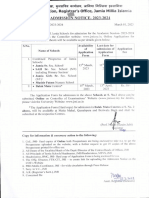

- Notice Admission School 2023march1Document1 pageNotice Admission School 2023march1asif khanNo ratings yet

- MobileApp Checklist 2017Document21 pagesMobileApp Checklist 2017Trico AndreasNo ratings yet

- An Example VHDL Application For The TM-4Document6 pagesAn Example VHDL Application For The TM-4anilshaw27No ratings yet

- Ict 2300Document19 pagesIct 2300Jim Carlo Abegonia Amansec100% (2)

- Smart City Padova 06740844Document426 pagesSmart City Padova 06740844Soumitra BhowmickNo ratings yet

- Energy Dissipation Capacity of Flexure-Dominated Reinforced Concrete MembersDocument12 pagesEnergy Dissipation Capacity of Flexure-Dominated Reinforced Concrete Members01010No ratings yet

- ExamDocument12 pagesExamPaul GarnerNo ratings yet

- Design IIDocument16 pagesDesign IIPrasant0% (1)

- QuarryDocument4 pagesQuarryAnujith K BabuNo ratings yet

- Sample Resume ITMDocument2 pagesSample Resume ITMRajveer RajNo ratings yet

- Air PollutionDocument35 pagesAir PollutionNur HazimahNo ratings yet

- Legal Ethics Syllabus CompleteDocument4 pagesLegal Ethics Syllabus CompletejessieNo ratings yet

- M-Class Parts Catalog 92-2505-01 EDocument24 pagesM-Class Parts Catalog 92-2505-01 EjNo ratings yet

- DSKH Ngan Hang Vietcombank Gui TienDocument32 pagesDSKH Ngan Hang Vietcombank Gui TienTi TanNo ratings yet

- Digital Dopamine: 2015 Global Digital Marketing ReportDocument39 pagesDigital Dopamine: 2015 Global Digital Marketing ReportPepMySpaceNo ratings yet

- Caso 2 - Gerencia de Operaciones 2023Document3 pagesCaso 2 - Gerencia de Operaciones 2023Eyner PeñaNo ratings yet

- Sem 3 Module 3Document5 pagesSem 3 Module 3Joshua HernandezNo ratings yet

- OctaneRenderUserManualBeta2 46Document137 pagesOctaneRenderUserManualBeta2 46Romeo CostanNo ratings yet

- Labio, Roan Claire BSN-4: Staffing ScheduleDocument2 pagesLabio, Roan Claire BSN-4: Staffing Schedulenoronisa talusobNo ratings yet

- CPC 2 2021Document3 pagesCPC 2 2021Sarthak SabbarwalNo ratings yet

- Literature Review Early Childhood EducationDocument10 pagesLiterature Review Early Childhood Educationafmzzulfmzbxet100% (1)

- Numerical DifferentiationDocument26 pagesNumerical DifferentiationchibenNo ratings yet

- Allwinner H3 Datasheet V1.1Document616 pagesAllwinner H3 Datasheet V1.1Daniel Trejo0% (1)

- TANF BenefitsDocument2 pagesTANF BenefitsStatesman JournalNo ratings yet