Download as ppt, pdf, or txt

You might also like

- Testing PlanDocument2 pagesTesting PlanAngMniNo ratings yet

- Customer Retention Strategies at HDFC BankDocument20 pagesCustomer Retention Strategies at HDFC BankHemantSharma100% (1)

- ELX 121 - Digital Television MultiplexingDocument22 pagesELX 121 - Digital Television MultiplexingClark Linogao FelisildaNo ratings yet

- Unit 10 Mortgage Financing and Fraud Awareness: Session 1 Introduction To Mortgages - Mortgage ConceptsDocument21 pagesUnit 10 Mortgage Financing and Fraud Awareness: Session 1 Introduction To Mortgages - Mortgage ConceptsPro MalikNo ratings yet

- Your Deposit Account Agreement: Effective May 11, 2020Document33 pagesYour Deposit Account Agreement: Effective May 11, 2020Steph BryattNo ratings yet

- Backup Withholding - What Is It and How Can I Obtain A RefundDocument35 pagesBackup Withholding - What Is It and How Can I Obtain A RefundAyodeji Badaki100% (2)

- The Financial Plan: Serjoe Orven Gutierrez - Mmed ReporterDocument41 pagesThe Financial Plan: Serjoe Orven Gutierrez - Mmed ReporterSerjoe GutierrezNo ratings yet

- Lecture For Promissory NoteDocument9 pagesLecture For Promissory Notejas jaasNo ratings yet

- Credit 3 Pt2Document29 pagesCredit 3 Pt2soojung jungNo ratings yet

- US Internal Revenue Service: p3381Document3 pagesUS Internal Revenue Service: p3381IRSNo ratings yet

- Employer Identification Number: Understanding Your EINDocument36 pagesEmployer Identification Number: Understanding Your EINgarnett19No ratings yet

- Advanced Certification - Study Guide (For Tax Season 2017)Document7 pagesAdvanced Certification - Study Guide (For Tax Season 2017)Center for Economic Progress100% (4)

- DEBT Tutoria BankingDocument21 pagesDEBT Tutoria BankingJenniferNo ratings yet

- Financial Institutions in The Financial SystemDocument15 pagesFinancial Institutions in The Financial SystemNigussie Berhanu100% (1)

- Rights of Drawers Banks and Holders in Bank Checks and Other CADocument57 pagesRights of Drawers Banks and Holders in Bank Checks and Other CASiddharth Singh TomarNo ratings yet

- Automotive Sales, Use & Lease Tax Guide: September 2019Document16 pagesAutomotive Sales, Use & Lease Tax Guide: September 2019student_physicianNo ratings yet

- Banking Terms and DefinitionsDocument36 pagesBanking Terms and DefinitionsARULSHANMUGAVEL S VNo ratings yet

- All Bank Branch CodesDocument44 pagesAll Bank Branch CodesakilamadushankeNo ratings yet

- United States v. Damian Jackson, Et Al, Complaint 2012Document25 pagesUnited States v. Damian Jackson, Et Al, Complaint 2012Beverly TranNo ratings yet

- Savings BondsDocument2 pagesSavings BondsffsdfsfdftrertNo ratings yet

- Advanced Scenario 6 - Quincy and Marian Pike (2018)Document10 pagesAdvanced Scenario 6 - Quincy and Marian Pike (2018)Center for Economic ProgressNo ratings yet

- BankerDocument2 pagesBankercrystal_angel0% (1)

- A Bank Is A Financial Intermediary That Accepts Deposits and Channels Those Deposits Into Lending ActivitiesDocument13 pagesA Bank Is A Financial Intermediary That Accepts Deposits and Channels Those Deposits Into Lending ActivitiesaimensajidNo ratings yet

- W8 Instructions PDFDocument15 pagesW8 Instructions PDFKrisdenNo ratings yet

- Assignment and Transfer of Contractual DutiesDocument38 pagesAssignment and Transfer of Contractual Dutieslicopodicum7670No ratings yet

- Mortgage and Types of MortgageDocument24 pagesMortgage and Types of MortgageHarshvardhan MelantaNo ratings yet

- Underwriter NotesDocument6 pagesUnderwriter Notessambamurthy sunkaraNo ratings yet

- 8 Get Your Finances & Credit in OrderDocument15 pages8 Get Your Finances & Credit in OrdercropdownunderNo ratings yet

- PPP Debt, Deposit and Remittance Heads of Accounts Session 7Document41 pagesPPP Debt, Deposit and Remittance Heads of Accounts Session 7Balu Mahendra SusarlaNo ratings yet

- UntitledDocument1 pageUntitledCarlosNo ratings yet

- Duke Energy PremierNotes ProspectusDocument37 pagesDuke Energy PremierNotes ProspectusshoppingonlyNo ratings yet

- Financial InstrumentsDocument9 pagesFinancial InstrumentsKristine Joy MercadoNo ratings yet

- Secured Borrowing and A Sale of ReceivablesDocument1 pageSecured Borrowing and A Sale of Receivableswarsidi100% (2)

- T1 Checklist Establishment of A TrustDocument4 pagesT1 Checklist Establishment of A TrustRod NewmanNo ratings yet

- Issue of DebenturesDocument23 pagesIssue of Debenturesramandeep kaurNo ratings yet

- 9 Debt Securities PDFDocument32 pages9 Debt Securities PDFKing is KingNo ratings yet

- Federal Deposit Insurance Corporation v. Bracero & Rivera, Inc., 895 F.2d 824, 1st Cir. (1990)Document9 pagesFederal Deposit Insurance Corporation v. Bracero & Rivera, Inc., 895 F.2d 824, 1st Cir. (1990)Scribd Government DocsNo ratings yet

- InstructionsDocument3 pagesInstructionsmreagansNo ratings yet

- US Internal Revenue Service: p15 - 1994Document64 pagesUS Internal Revenue Service: p15 - 1994IRSNo ratings yet

- Basics of Accounting 1 IntroductionDocument38 pagesBasics of Accounting 1 Introductionjiten zopeNo ratings yet

- IRS Publication 15 Withholding Tax Tables 2010Document73 pagesIRS Publication 15 Withholding Tax Tables 2010Wayne Schulz100% (1)

- Law of Banking, Negotiable Instruments and InsuranceDocument193 pagesLaw of Banking, Negotiable Instruments and InsuranceHabtamu Gabisa100% (1)

- Characteristic of Bond: Financial Management 2Document4 pagesCharacteristic of Bond: Financial Management 2zarfarie aronNo ratings yet

- ContractPayInformation 011110Document42 pagesContractPayInformation 011110Franseh MuyaNo ratings yet

- Debt InstrumentsDocument8 pagesDebt InstrumentsparulshinyNo ratings yet

- Chpater 5 - Banking SystemDocument10 pagesChpater 5 - Banking System21augustNo ratings yet

- Irrevocable Stock/Bond Power FormDocument1 pageIrrevocable Stock/Bond Power Formflextechvip100% (1)

- What Is The Indirect MethodDocument3 pagesWhat Is The Indirect MethodHsin Wua ChiNo ratings yet

- Why Banks Don't Need Your Money To Make LoansDocument10 pagesWhy Banks Don't Need Your Money To Make Loansabarnettceo9659No ratings yet

- IT-40 Full-Year Resident: IndianaDocument48 pagesIT-40 Full-Year Resident: IndianaLady PayneNo ratings yet

- Disclosure RetrieverDocument30 pagesDisclosure RetrievermattloyaltyNo ratings yet

- C8 Recievable Financing Pledge Assignment FactoringDocument32 pagesC8 Recievable Financing Pledge Assignment FactoringAngelie LaxaNo ratings yet

- Bills of Exchange Unit-5Document15 pagesBills of Exchange Unit-5Bell BottleNo ratings yet

- Investment Income and Expenses: (Including Capital Gains and Losses)Document76 pagesInvestment Income and Expenses: (Including Capital Gains and Losses)Kenny Svatek100% (1)

- Double-Entry Book-KeepingDocument6 pagesDouble-Entry Book-KeepingFarman AfzalNo ratings yet

- Bank Ing Laws and Practice: Ques Tion Book Let For TDP (Gen Eral) /TDP (Hon Ours) 6th Se Mes Ter Exam., 2020Document12 pagesBank Ing Laws and Practice: Ques Tion Book Let For TDP (Gen Eral) /TDP (Hon Ours) 6th Se Mes Ter Exam., 2020Subhajit singhaNo ratings yet

- General BankingDocument167 pagesGeneral BankingSuvasish DasguptaNo ratings yet

- Trusts: 8 Sept 2020Document8 pagesTrusts: 8 Sept 2020Ella B.No ratings yet

- Department of The TreasuryDocument1 pageDepartment of The TreasuryShevis Singleton Sr.No ratings yet

- (Insert "Maker" If Maker and Borrower Are The Same EntityDocument5 pages(Insert "Maker" If Maker and Borrower Are The Same EntityJames neteruNo ratings yet

- Basic Account Works: Unit Title of Competency:Develop Understanding of Debt and Consumer CreditDocument15 pagesBasic Account Works: Unit Title of Competency:Develop Understanding of Debt and Consumer CreditIsrael KifleNo ratings yet

- 1a. Introduction To RetailDocument32 pages1a. Introduction To RetailAbhay Singh SolankiNo ratings yet

- What Are Computer NetworksDocument5 pagesWhat Are Computer NetworksJASMEET SinghNo ratings yet

- RequestDocument36 pagesRequestMiro ManoNo ratings yet

- Europages ReportDocument21 pagesEuropages ReportVishwaMohanNo ratings yet

- Processed oDocument2 pagesProcessed oHemanth KumarNo ratings yet

- Jlakshya - 10-12-2020 4.53.21 PDFDocument8 pagesJlakshya - 10-12-2020 4.53.21 PDFAnuNo ratings yet

- Bajaj Allianz General Insurance Company Limited.: Details of Primary InsuredDocument5 pagesBajaj Allianz General Insurance Company Limited.: Details of Primary InsuredGkrishnanS2012No ratings yet

- Canonigo Reservation ScriptDocument3 pagesCanonigo Reservation ScriptJush Evanne CanonigoNo ratings yet

- 2-09-98-PHA DT 16.01.2002 BSNLDocument1 page2-09-98-PHA DT 16.01.2002 BSNLbsnl jamkandornaNo ratings yet

- SOA ReportDocument6 pagesSOA ReportNitin ChoukikerNo ratings yet

- Ensuring A Smooth RideDocument106 pagesEnsuring A Smooth RideShantanuNo ratings yet

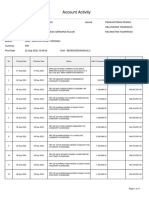

- Account ActivityDocument11 pagesAccount ActivityIrone Akatshuki LeaderNo ratings yet

- New VAS 6154A Aftersales Support ProcessDocument6 pagesNew VAS 6154A Aftersales Support Processvalentin750No ratings yet

- Prosanjit CVDocument2 pagesProsanjit CVMd. Nazmus SakibNo ratings yet

- Cyber Laundering FinalDocument70 pagesCyber Laundering Finalsalman jamali100% (2)

- Various Health Committees: Module 1: Chapter 4Document7 pagesVarious Health Committees: Module 1: Chapter 4Nalina BathranNo ratings yet

- CHAPTER 7 AND CHAPTER 8 Retail ManagementDocument10 pagesCHAPTER 7 AND CHAPTER 8 Retail ManagementEwan DikoNo ratings yet

- E-Commerce Sales Life Cycle (ESLC) ModelDocument3 pagesE-Commerce Sales Life Cycle (ESLC) ModelBhaswati Panda100% (3)

- Hurricane Sandy: How The Continuum Hospitals of New York Served The NYC CommunitiesDocument6 pagesHurricane Sandy: How The Continuum Hospitals of New York Served The NYC CommunitiesContinuum Hospitals of New YorkNo ratings yet

- DGDADocument4 pagesDGDAS RahmanNo ratings yet

- Update List Product Sultan DecDocument126 pagesUpdate List Product Sultan DecTIDAK ADILNo ratings yet

- 2022 06 15 2022 07 06 - Invoice - SummaryDocument1 page2022 06 15 2022 07 06 - Invoice - SummaryTwentytree EmpireNo ratings yet

- Making Digital Homes With Joyful Lifestyle and For A Safer CommunityDocument2 pagesMaking Digital Homes With Joyful Lifestyle and For A Safer CommunityNATHANNo ratings yet

- 5 Container Corporation of IndiaDocument19 pages5 Container Corporation of IndiaSaki Saki SakiNo ratings yet

- Abdul Manan IS1Document20 pagesAbdul Manan IS1Chakwal ReactionsNo ratings yet

- Importance of Digital MediaDocument5 pagesImportance of Digital MediaMazia MansoorNo ratings yet

- Elliya T. Sinaga Resume 2023Document4 pagesElliya T. Sinaga Resume 2023DEWI PATRICIANo ratings yet