Chap013 Target Costing Cost MNGT

Chap013 Target Costing Cost MNGT

You might also like

- Payroll Project Chapter 7 - 2019Document79 pagesPayroll Project Chapter 7 - 2019Andrea Cox88% (135)

- CASE Solution VyadermDocument8 pagesCASE Solution VyadermIshan Shah100% (2)

- Wallace Garden SupplyDocument4 pagesWallace Garden SupplyestoniloannNo ratings yet

- Tugas Akmen 3.2A - 3.3ADocument2 pagesTugas Akmen 3.2A - 3.3ADias AdhyaksaNo ratings yet

- Ilovepdf MergedDocument100 pagesIlovepdf MergedVinny AujlaNo ratings yet

- BTEC L3, Unit 7 - Business Decision Making NotesDocument41 pagesBTEC L3, Unit 7 - Business Decision Making NotesJoy100% (1)

- NetworkDocument12 pagesNetworkDira Silvia IrvannyNo ratings yet

- 33707graphical MethodDocument4 pages33707graphical MethodMehak KalraNo ratings yet

- Chapter 18. CH 18-06 Build A ModelDocument4 pagesChapter 18. CH 18-06 Build A ModelNguyễn Thu PhươngNo ratings yet

- 1 Semester, 2014/2015 Examination Fin 210: Introduction To Finance Time Allowed 90 Minutes Use For Questions 1 To 5Document22 pages1 Semester, 2014/2015 Examination Fin 210: Introduction To Finance Time Allowed 90 Minutes Use For Questions 1 To 5Daniel Adegboye100% (1)

- Management Accounting Individual AssignmentDocument10 pagesManagement Accounting Individual AssignmentendalNo ratings yet

- Network Model - Problem SetDocument3 pagesNetwork Model - Problem SetRyan Jeffrey Padua CurbanoNo ratings yet

- Working Capital Management of AccDocument52 pagesWorking Capital Management of AccSoham Khanna75% (4)

- Collaborative Review Task IDocument3 pagesCollaborative Review Task IAbdullah AlGhamdiNo ratings yet

- Capacity Planning: Mcgraw-Hill/IrwinDocument15 pagesCapacity Planning: Mcgraw-Hill/IrwinKader KARAAĞAÇNo ratings yet

- Balance Sheet Presentation of Liabilities: Problem 10.2ADocument4 pagesBalance Sheet Presentation of Liabilities: Problem 10.2AMuhammad Haris100% (1)

- CH 13Document15 pagesCH 13alfiNo ratings yet

- Production StrategyDocument14 pagesProduction StrategyJD_04100% (3)

- Cost Allocation and Budgeting 1Document85 pagesCost Allocation and Budgeting 1CPAREVIEWNo ratings yet

- Handout 3 - Plant Assets, Natural Resources, and Intangible AssetsDocument81 pagesHandout 3 - Plant Assets, Natural Resources, and Intangible Assetsyoussef abdellatifNo ratings yet

- Standard CostingDocument18 pagesStandard Costingpakistan 123No ratings yet

- Topic 2 Support Department Cost AllocationDocument27 pagesTopic 2 Support Department Cost Allocationluckystar251095No ratings yet

- CH 12Document3 pagesCH 12ghsoub777No ratings yet

- Operations Management: For Competitive AdvantageDocument47 pagesOperations Management: For Competitive AdvantagedurgaselvamNo ratings yet

- Ama Long QuestionDocument30 pagesAma Long Questionmalikahsanrazaawan7No ratings yet

- Notes Capital Revenue AnsDocument3 pagesNotes Capital Revenue AnsMuhammad JavedNo ratings yet

- Chapter 16 - Depreciation MethodsDocument13 pagesChapter 16 - Depreciation MethodsCedrick S TanNo ratings yet

- LP Formulation and SolutionDocument7 pagesLP Formulation and SolutionPhanieNo ratings yet

- Learning CurvesDocument33 pagesLearning Curvesayushc27No ratings yet

- PERT and CPMDocument118 pagesPERT and CPMVIGNESH DHANASHEKHARNo ratings yet

- Lloyd Industries Manufactures Electrical Equipment From Specifications Received From CustomersDocument2 pagesLloyd Industries Manufactures Electrical Equipment From Specifications Received From CustomersAmit PandeyNo ratings yet

- Future Worth Comparison of Alternatives: Answer: A. FWM - $230,500, FWN - $170,700Document9 pagesFuture Worth Comparison of Alternatives: Answer: A. FWM - $230,500, FWN - $170,700CloeNo ratings yet

- Senior High School: First Semester S.Y. 2020-2021Document9 pagesSenior High School: First Semester S.Y. 2020-2021sheilame nudaloNo ratings yet

- Midterm 5101Document4 pagesMidterm 5101MD Hafizul Islam HafizNo ratings yet

- Weeks 1-7 Examples Answers and Key Concepts Discussion ProblemsDocument57 pagesWeeks 1-7 Examples Answers and Key Concepts Discussion ProblemsAshish BhallaNo ratings yet

- Cost2 - Finals SY 2020 21 PDFDocument10 pagesCost2 - Finals SY 2020 21 PDFshengNo ratings yet

- Chapter 10 Activity Based CostingDocument10 pagesChapter 10 Activity Based CostingRuby P. MadejaNo ratings yet

- Accounting 1 FinalDocument2 pagesAccounting 1 FinalchiknaaaNo ratings yet

- Activity 4 Job Order CostingDocument4 pagesActivity 4 Job Order CostingJOSCEL SYJONGTIANNo ratings yet

- Ifa I Chapter 5Document22 pagesIfa I Chapter 5Nigussie BerhanuNo ratings yet

- IAS 02: Inventories: Requirement: SolutionDocument2 pagesIAS 02: Inventories: Requirement: SolutionMD Hafizul Islam Hafiz100% (1)

- Time Value of Money Sample QuestionsDocument4 pagesTime Value of Money Sample Questionssakshi tomar100% (1)

- Fair Value Measurement and ImpairmentDocument2 pagesFair Value Measurement and Impairmentyonatan tesemaNo ratings yet

- Class Exercise On Linear Programming PDFDocument3 pagesClass Exercise On Linear Programming PDFKaran KakkarNo ratings yet

- Sajid. PEPSICODocument61 pagesSajid. PEPSICOSajid HussainNo ratings yet

- Financial AccountingDocument9 pagesFinancial AccountingAnonymous VmhXGNlFyNo ratings yet

- Chapter 1: Flexible Budgeting and The Management of Overhead and Support Activity Costs Answer KeyDocument33 pagesChapter 1: Flexible Budgeting and The Management of Overhead and Support Activity Costs Answer KeyRafaelDelaCruz50% (2)

- Working Capital AnalysisDocument9 pagesWorking Capital AnalysisDr Siddharth DarjiNo ratings yet

- Chapter 4Document6 pagesChapter 4Ervin AawitinNo ratings yet

- Ch5 ProblemsDocument9 pagesCh5 ProblemsRody El KhalilNo ratings yet

- The Cost of Quality and Accounting For Production LossesDocument19 pagesThe Cost of Quality and Accounting For Production Lossesjammy AgnoNo ratings yet

- Principle of Accounting 1 - Chapter 2Document29 pagesPrinciple of Accounting 1 - Chapter 2ferejagi8No ratings yet

- IPSAS 4 - The Effects of Changes in Foreign Exchange RatesDocument20 pagesIPSAS 4 - The Effects of Changes in Foreign Exchange RatesAida MohammedNo ratings yet

- Cost Accounting - Author William K. Carter - 14ed-297-298Document2 pagesCost Accounting - Author William K. Carter - 14ed-297-298dindaNo ratings yet

- Internal Rate of ReturnDocument6 pagesInternal Rate of ReturnDagnachew Amare DagnachewNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument56 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Case 1-4 Boeing's E-Enabled AdvantageDocument12 pagesCase 1-4 Boeing's E-Enabled AdvantageanjiroNo ratings yet

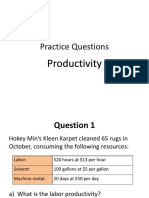

- Week 2 Practice Questions - ProductivityDocument6 pagesWeek 2 Practice Questions - ProductivityHeah Wan YeeNo ratings yet

- Management Science FinalDocument8 pagesManagement Science FinalAAUMCLNo ratings yet

- Management Accounting Tauseef A.Qureshi Assignment No 5 (Budgeting) Problem No 1: (Gulick Company)Document9 pagesManagement Accounting Tauseef A.Qureshi Assignment No 5 (Budgeting) Problem No 1: (Gulick Company)Mustafa ArshadNo ratings yet

- Chapter 03 TP EndDocument43 pagesChapter 03 TP EndMesfin MekuriaNo ratings yet

- Chap013 Target Costing Cost MNGTDocument49 pagesChap013 Target Costing Cost MNGTramaNo ratings yet

- CHAPTER 2 (Strategic Management Accounting)Document61 pagesCHAPTER 2 (Strategic Management Accounting)MuhdTaQiuNo ratings yet

- ManagementDocument71 pagesManagementmartamckeenNo ratings yet

- Productions and Operations ManagementDocument34 pagesProductions and Operations ManagementmartamckeenNo ratings yet

- The Relationship Between Target Costing Method and Pricing - Development of Products in Industrial CompaniesDocument12 pagesThe Relationship Between Target Costing Method and Pricing - Development of Products in Industrial CompaniesstuntNo ratings yet

- Commercial Roofing Help EbookDocument22 pagesCommercial Roofing Help EbookChoice Roof Contractor Group100% (1)

- 5Document2 pages5noneofyourbusinessNo ratings yet

- Manuals For Participants PDFDocument5 pagesManuals For Participants PDFindra alverdianNo ratings yet

- Practice TestDocument8 pagesPractice TestDivya VanwariNo ratings yet

- Topic 2 - The Allocation of Resources 5 PDFDocument18 pagesTopic 2 - The Allocation of Resources 5 PDFMxni ChyNo ratings yet

- RMT-FALL-Assignment - Waqar Yousfi 02-111172-288 BBA-7-DDocument4 pagesRMT-FALL-Assignment - Waqar Yousfi 02-111172-288 BBA-7-DWaqar YousfiNo ratings yet

- Chapter 31 - AnswerDocument15 pagesChapter 31 - AnswerPam PolonioNo ratings yet

- Broker Account Opening Form IndividualDocument27 pagesBroker Account Opening Form IndividualAbdul QayoomNo ratings yet

- IntroductionDocument85 pagesIntroductionRitika MittalNo ratings yet

- Simon Fraser University: Beedie School of BusinessDocument3 pagesSimon Fraser University: Beedie School of BusinessvwzhaoNo ratings yet

- Larsen & Toubro Limited, ConstructionDocument2 pagesLarsen & Toubro Limited, ConstructionNitesh KumarNo ratings yet

- International Financial Management Abridged 10 Edition: by Jeff MaduraDocument12 pagesInternational Financial Management Abridged 10 Edition: by Jeff MaduraHiếu Nhi TrịnhNo ratings yet

- Topic: Time Value of Money: BY Kajal VipaniDocument50 pagesTopic: Time Value of Money: BY Kajal VipaniAakarshak nandwaniNo ratings yet

- LabourDocument15 pagesLabourRakhiNo ratings yet

- Zero HungerDocument1 pageZero HungerJohnrey FeguroNo ratings yet

- Investment Banks Hedge Funds and Private Equity David P Stowell Full ChapterDocument67 pagesInvestment Banks Hedge Funds and Private Equity David P Stowell Full Chapterangel.attaway709100% (4)

- European Commission Glossary of Terms Used in Eu Competition Policy - Antitrust and Control of ConcentrationsDocument59 pagesEuropean Commission Glossary of Terms Used in Eu Competition Policy - Antitrust and Control of ConcentrationsAndreea ToncuNo ratings yet

- Technoprenuership Final Exam Attempt ReviewDocument22 pagesTechnoprenuership Final Exam Attempt ReviewLoving Angel100% (1)

- Invest in Real Estate For Inflationary TimesDocument8 pagesInvest in Real Estate For Inflationary TimesCraigNo ratings yet

- Sbi LifeDocument16 pagesSbi LifesahilNo ratings yet

- 2013-2-28 HoBee Press Release FY2012Document4 pages2013-2-28 HoBee Press Release FY2012phuawlNo ratings yet

- Annualreport 2012Document100 pagesAnnualreport 2012Asghar IqbalNo ratings yet

- De Dollar Is at I On AnonymousDocument36 pagesDe Dollar Is at I On AnonymousTanmaye ShagotraNo ratings yet

- Income From Salary Chapter QuestionsDocument5 pagesIncome From Salary Chapter Questionsanon_595315274100% (1)

Download as pptx, pdf, or txt

You might also like

- Payroll Project Chapter 7 - 2019Document79 pagesPayroll Project Chapter 7 - 2019Andrea Cox88% (135)

- CASE Solution VyadermDocument8 pagesCASE Solution VyadermIshan Shah100% (2)

- Wallace Garden SupplyDocument4 pagesWallace Garden SupplyestoniloannNo ratings yet

- Tugas Akmen 3.2A - 3.3ADocument2 pagesTugas Akmen 3.2A - 3.3ADias AdhyaksaNo ratings yet

- Ilovepdf MergedDocument100 pagesIlovepdf MergedVinny AujlaNo ratings yet

- BTEC L3, Unit 7 - Business Decision Making NotesDocument41 pagesBTEC L3, Unit 7 - Business Decision Making NotesJoy100% (1)

- NetworkDocument12 pagesNetworkDira Silvia IrvannyNo ratings yet

- 33707graphical MethodDocument4 pages33707graphical MethodMehak KalraNo ratings yet

- Chapter 18. CH 18-06 Build A ModelDocument4 pagesChapter 18. CH 18-06 Build A ModelNguyễn Thu PhươngNo ratings yet

- 1 Semester, 2014/2015 Examination Fin 210: Introduction To Finance Time Allowed 90 Minutes Use For Questions 1 To 5Document22 pages1 Semester, 2014/2015 Examination Fin 210: Introduction To Finance Time Allowed 90 Minutes Use For Questions 1 To 5Daniel Adegboye100% (1)

- Management Accounting Individual AssignmentDocument10 pagesManagement Accounting Individual AssignmentendalNo ratings yet

- Network Model - Problem SetDocument3 pagesNetwork Model - Problem SetRyan Jeffrey Padua CurbanoNo ratings yet

- Working Capital Management of AccDocument52 pagesWorking Capital Management of AccSoham Khanna75% (4)

- Collaborative Review Task IDocument3 pagesCollaborative Review Task IAbdullah AlGhamdiNo ratings yet

- Capacity Planning: Mcgraw-Hill/IrwinDocument15 pagesCapacity Planning: Mcgraw-Hill/IrwinKader KARAAĞAÇNo ratings yet

- Balance Sheet Presentation of Liabilities: Problem 10.2ADocument4 pagesBalance Sheet Presentation of Liabilities: Problem 10.2AMuhammad Haris100% (1)

- CH 13Document15 pagesCH 13alfiNo ratings yet

- Production StrategyDocument14 pagesProduction StrategyJD_04100% (3)

- Cost Allocation and Budgeting 1Document85 pagesCost Allocation and Budgeting 1CPAREVIEWNo ratings yet

- Handout 3 - Plant Assets, Natural Resources, and Intangible AssetsDocument81 pagesHandout 3 - Plant Assets, Natural Resources, and Intangible Assetsyoussef abdellatifNo ratings yet

- Standard CostingDocument18 pagesStandard Costingpakistan 123No ratings yet

- Topic 2 Support Department Cost AllocationDocument27 pagesTopic 2 Support Department Cost Allocationluckystar251095No ratings yet

- CH 12Document3 pagesCH 12ghsoub777No ratings yet

- Operations Management: For Competitive AdvantageDocument47 pagesOperations Management: For Competitive AdvantagedurgaselvamNo ratings yet

- Ama Long QuestionDocument30 pagesAma Long Questionmalikahsanrazaawan7No ratings yet

- Notes Capital Revenue AnsDocument3 pagesNotes Capital Revenue AnsMuhammad JavedNo ratings yet

- Chapter 16 - Depreciation MethodsDocument13 pagesChapter 16 - Depreciation MethodsCedrick S TanNo ratings yet

- LP Formulation and SolutionDocument7 pagesLP Formulation and SolutionPhanieNo ratings yet

- Learning CurvesDocument33 pagesLearning Curvesayushc27No ratings yet

- PERT and CPMDocument118 pagesPERT and CPMVIGNESH DHANASHEKHARNo ratings yet

- Lloyd Industries Manufactures Electrical Equipment From Specifications Received From CustomersDocument2 pagesLloyd Industries Manufactures Electrical Equipment From Specifications Received From CustomersAmit PandeyNo ratings yet

- Future Worth Comparison of Alternatives: Answer: A. FWM - $230,500, FWN - $170,700Document9 pagesFuture Worth Comparison of Alternatives: Answer: A. FWM - $230,500, FWN - $170,700CloeNo ratings yet

- Senior High School: First Semester S.Y. 2020-2021Document9 pagesSenior High School: First Semester S.Y. 2020-2021sheilame nudaloNo ratings yet

- Midterm 5101Document4 pagesMidterm 5101MD Hafizul Islam HafizNo ratings yet

- Weeks 1-7 Examples Answers and Key Concepts Discussion ProblemsDocument57 pagesWeeks 1-7 Examples Answers and Key Concepts Discussion ProblemsAshish BhallaNo ratings yet

- Cost2 - Finals SY 2020 21 PDFDocument10 pagesCost2 - Finals SY 2020 21 PDFshengNo ratings yet

- Chapter 10 Activity Based CostingDocument10 pagesChapter 10 Activity Based CostingRuby P. MadejaNo ratings yet

- Accounting 1 FinalDocument2 pagesAccounting 1 FinalchiknaaaNo ratings yet

- Activity 4 Job Order CostingDocument4 pagesActivity 4 Job Order CostingJOSCEL SYJONGTIANNo ratings yet

- Ifa I Chapter 5Document22 pagesIfa I Chapter 5Nigussie BerhanuNo ratings yet

- IAS 02: Inventories: Requirement: SolutionDocument2 pagesIAS 02: Inventories: Requirement: SolutionMD Hafizul Islam Hafiz100% (1)

- Time Value of Money Sample QuestionsDocument4 pagesTime Value of Money Sample Questionssakshi tomar100% (1)

- Fair Value Measurement and ImpairmentDocument2 pagesFair Value Measurement and Impairmentyonatan tesemaNo ratings yet

- Class Exercise On Linear Programming PDFDocument3 pagesClass Exercise On Linear Programming PDFKaran KakkarNo ratings yet

- Sajid. PEPSICODocument61 pagesSajid. PEPSICOSajid HussainNo ratings yet

- Financial AccountingDocument9 pagesFinancial AccountingAnonymous VmhXGNlFyNo ratings yet

- Chapter 1: Flexible Budgeting and The Management of Overhead and Support Activity Costs Answer KeyDocument33 pagesChapter 1: Flexible Budgeting and The Management of Overhead and Support Activity Costs Answer KeyRafaelDelaCruz50% (2)

- Working Capital AnalysisDocument9 pagesWorking Capital AnalysisDr Siddharth DarjiNo ratings yet

- Chapter 4Document6 pagesChapter 4Ervin AawitinNo ratings yet

- Ch5 ProblemsDocument9 pagesCh5 ProblemsRody El KhalilNo ratings yet

- The Cost of Quality and Accounting For Production LossesDocument19 pagesThe Cost of Quality and Accounting For Production Lossesjammy AgnoNo ratings yet

- Principle of Accounting 1 - Chapter 2Document29 pagesPrinciple of Accounting 1 - Chapter 2ferejagi8No ratings yet

- IPSAS 4 - The Effects of Changes in Foreign Exchange RatesDocument20 pagesIPSAS 4 - The Effects of Changes in Foreign Exchange RatesAida MohammedNo ratings yet

- Cost Accounting - Author William K. Carter - 14ed-297-298Document2 pagesCost Accounting - Author William K. Carter - 14ed-297-298dindaNo ratings yet

- Internal Rate of ReturnDocument6 pagesInternal Rate of ReturnDagnachew Amare DagnachewNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument56 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Case 1-4 Boeing's E-Enabled AdvantageDocument12 pagesCase 1-4 Boeing's E-Enabled AdvantageanjiroNo ratings yet

- Week 2 Practice Questions - ProductivityDocument6 pagesWeek 2 Practice Questions - ProductivityHeah Wan YeeNo ratings yet

- Management Science FinalDocument8 pagesManagement Science FinalAAUMCLNo ratings yet

- Management Accounting Tauseef A.Qureshi Assignment No 5 (Budgeting) Problem No 1: (Gulick Company)Document9 pagesManagement Accounting Tauseef A.Qureshi Assignment No 5 (Budgeting) Problem No 1: (Gulick Company)Mustafa ArshadNo ratings yet

- Chapter 03 TP EndDocument43 pagesChapter 03 TP EndMesfin MekuriaNo ratings yet

- Chap013 Target Costing Cost MNGTDocument49 pagesChap013 Target Costing Cost MNGTramaNo ratings yet

- CHAPTER 2 (Strategic Management Accounting)Document61 pagesCHAPTER 2 (Strategic Management Accounting)MuhdTaQiuNo ratings yet

- ManagementDocument71 pagesManagementmartamckeenNo ratings yet

- Productions and Operations ManagementDocument34 pagesProductions and Operations ManagementmartamckeenNo ratings yet

- The Relationship Between Target Costing Method and Pricing - Development of Products in Industrial CompaniesDocument12 pagesThe Relationship Between Target Costing Method and Pricing - Development of Products in Industrial CompaniesstuntNo ratings yet

- Commercial Roofing Help EbookDocument22 pagesCommercial Roofing Help EbookChoice Roof Contractor Group100% (1)

- 5Document2 pages5noneofyourbusinessNo ratings yet

- Manuals For Participants PDFDocument5 pagesManuals For Participants PDFindra alverdianNo ratings yet

- Practice TestDocument8 pagesPractice TestDivya VanwariNo ratings yet

- Topic 2 - The Allocation of Resources 5 PDFDocument18 pagesTopic 2 - The Allocation of Resources 5 PDFMxni ChyNo ratings yet

- RMT-FALL-Assignment - Waqar Yousfi 02-111172-288 BBA-7-DDocument4 pagesRMT-FALL-Assignment - Waqar Yousfi 02-111172-288 BBA-7-DWaqar YousfiNo ratings yet

- Chapter 31 - AnswerDocument15 pagesChapter 31 - AnswerPam PolonioNo ratings yet

- Broker Account Opening Form IndividualDocument27 pagesBroker Account Opening Form IndividualAbdul QayoomNo ratings yet

- IntroductionDocument85 pagesIntroductionRitika MittalNo ratings yet

- Simon Fraser University: Beedie School of BusinessDocument3 pagesSimon Fraser University: Beedie School of BusinessvwzhaoNo ratings yet

- Larsen & Toubro Limited, ConstructionDocument2 pagesLarsen & Toubro Limited, ConstructionNitesh KumarNo ratings yet

- International Financial Management Abridged 10 Edition: by Jeff MaduraDocument12 pagesInternational Financial Management Abridged 10 Edition: by Jeff MaduraHiếu Nhi TrịnhNo ratings yet

- Topic: Time Value of Money: BY Kajal VipaniDocument50 pagesTopic: Time Value of Money: BY Kajal VipaniAakarshak nandwaniNo ratings yet

- LabourDocument15 pagesLabourRakhiNo ratings yet

- Zero HungerDocument1 pageZero HungerJohnrey FeguroNo ratings yet

- Investment Banks Hedge Funds and Private Equity David P Stowell Full ChapterDocument67 pagesInvestment Banks Hedge Funds and Private Equity David P Stowell Full Chapterangel.attaway709100% (4)

- European Commission Glossary of Terms Used in Eu Competition Policy - Antitrust and Control of ConcentrationsDocument59 pagesEuropean Commission Glossary of Terms Used in Eu Competition Policy - Antitrust and Control of ConcentrationsAndreea ToncuNo ratings yet

- Technoprenuership Final Exam Attempt ReviewDocument22 pagesTechnoprenuership Final Exam Attempt ReviewLoving Angel100% (1)

- Invest in Real Estate For Inflationary TimesDocument8 pagesInvest in Real Estate For Inflationary TimesCraigNo ratings yet

- Sbi LifeDocument16 pagesSbi LifesahilNo ratings yet

- 2013-2-28 HoBee Press Release FY2012Document4 pages2013-2-28 HoBee Press Release FY2012phuawlNo ratings yet

- Annualreport 2012Document100 pagesAnnualreport 2012Asghar IqbalNo ratings yet

- De Dollar Is at I On AnonymousDocument36 pagesDe Dollar Is at I On AnonymousTanmaye ShagotraNo ratings yet

- Income From Salary Chapter QuestionsDocument5 pagesIncome From Salary Chapter Questionsanon_595315274100% (1)