Recording Business Transactions: 2-1 © 2015 Pearson Education, Limited

Recording Business Transactions: 2-1 © 2015 Pearson Education, Limited

You might also like

- College Accounting A Career Approach 13th Edition Scott Solutions ManualDocument35 pagesCollege Accounting A Career Approach 13th Edition Scott Solutions ManualCalvinMataazscm100% (17)

- Horngrens Accounting 12th Edition Nobles Solutions ManualDocument109 pagesHorngrens Accounting 12th Edition Nobles Solutions ManualAnnGregoryDDSytidk100% (16)

- Syndicated Leveraged Loans During and After The CrisisDocument25 pagesSyndicated Leveraged Loans During and After The Crisisresat gürNo ratings yet

- Fintech Business ModelsDocument8 pagesFintech Business ModelsSarthak0% (1)

- NFO SBI Balanced Advantage Fund PresentationDocument25 pagesNFO SBI Balanced Advantage Fund PresentationJohnTP100% (1)

- Basic Accounting For Non-AccountantsDocument34 pagesBasic Accounting For Non-Accountantsekta100% (1)

- Accounting TransactionsDocument28 pagesAccounting TransactionsPaolo100% (1)

- Nobles Acctg10 PPT 02Document39 pagesNobles Acctg10 PPT 02Tayar ElieNo ratings yet

- Recording Business TransactionsDocument39 pagesRecording Business TransactionsNajwa Al-khateebNo ratings yet

- Chapter 2Document25 pagesChapter 2Jose Carlos SouzaNo ratings yet

- 2-Accounting Equation & Journal Entries, Posting To LedgersDocument12 pages2-Accounting Equation & Journal Entries, Posting To LedgershattarvapeNo ratings yet

- Fa PPT CH 2 - 7eDocument59 pagesFa PPT CH 2 - 7eMaria GomezNo ratings yet

- Topic 2 Financial Statements, Taxes and CashflowsDocument22 pagesTopic 2 Financial Statements, Taxes and CashflowsQianyiiNo ratings yet

- Learning Outcome and Programme Learning Objectives (Plos)Document64 pagesLearning Outcome and Programme Learning Objectives (Plos)ANGEL ROBIN RCBSNo ratings yet

- 3-ACC 1101 Topic 3Document51 pages3-ACC 1101 Topic 3Abd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Financial Statements - Basis of AnalysisDocument44 pagesFinancial Statements - Basis of AnalysisJasmine ActaNo ratings yet

- 10 Examples of Double Entry Accounting 1683305482Document33 pages10 Examples of Double Entry Accounting 1683305482co1g4xqxNo ratings yet

- Accounting Pre Q1 Mid-Term Review 11thDocument36 pagesAccounting Pre Q1 Mid-Term Review 11thOscar Armando Villeda AlvaradoNo ratings yet

- AFM CH 2Document58 pagesAFM CH 2Birhanu MengisteNo ratings yet

- Recording Business Transactions: © 2016 Pearson Education, LTDDocument53 pagesRecording Business Transactions: © 2016 Pearson Education, LTDEce BarlasNo ratings yet

- Financial Accounting, 4eDocument49 pagesFinancial Accounting, 4eZulfiqarNo ratings yet

- Accounting Concepts & PrinciplesDocument26 pagesAccounting Concepts & PrinciplesThy Ngoc100% (1)

- Accounting Basics Using Quickbooks: Presented by Mike KimutaiDocument17 pagesAccounting Basics Using Quickbooks: Presented by Mike KimutaiMike Kimutai 'Sonko'No ratings yet

- CH 2 - FudDocument16 pagesCH 2 - FudbavanthinilNo ratings yet

- Chapter 11 Bookkeeping EntrepDocument37 pagesChapter 11 Bookkeeping EntrepJacel GadonNo ratings yet

- Module 6: Accounting Equation, T-Account, Rules of Debit and Credit and Normal BalancesDocument10 pagesModule 6: Accounting Equation, T-Account, Rules of Debit and Credit and Normal BalancesDarwin AniarNo ratings yet

- PPT 2 - Business TransactionDocument29 pagesPPT 2 - Business Transactionthinkaboutbe14No ratings yet

- The Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Document28 pagesThe Income Statement and Adjusting Entries: Financial Accounting - Lecture 2minghuiNo ratings yet

- Introduction To AccountingDocument39 pagesIntroduction To AccountingVikash HurrydossNo ratings yet

- BBAW2103 - Tutorial 1Document69 pagesBBAW2103 - Tutorial 1M THREE THOUSAND RESOURCESNo ratings yet

- Project On Final Accounts: Vishal Jadhav Nilesh Wadhwa Pankaj Kathayat Ravi Gera MBA 2010Document23 pagesProject On Final Accounts: Vishal Jadhav Nilesh Wadhwa Pankaj Kathayat Ravi Gera MBA 2010Ravi GeraNo ratings yet

- Senior High School Department: Quarter 3 - Module 4: Debit and Credit-The Double - Entry SystemDocument13 pagesSenior High School Department: Quarter 3 - Module 4: Debit and Credit-The Double - Entry SystemJaye Ruanto100% (1)

- Basics of Accounting in VEDocument25 pagesBasics of Accounting in VEIpang NoyoNo ratings yet

- JPIA 1st Tutorial Basic AccountingDocument6 pagesJPIA 1st Tutorial Basic AccountingZee SantisasNo ratings yet

- MAF CH 2 NEWDocument58 pagesMAF CH 2 NEWAsegid H/meskelNo ratings yet

- Basics of Accounting in VEDocument25 pagesBasics of Accounting in VEIpang NoyoNo ratings yet

- Module 4 - Double Entry Bookkeeping System and The Accounting EquationDocument9 pagesModule 4 - Double Entry Bookkeeping System and The Accounting EquationMark Christian BrlNo ratings yet

- Week 9: Introductory Accounting and The Balance Sheet: Public Health Accounting and Budgeting Lili Elkins-ThompsonDocument64 pagesWeek 9: Introductory Accounting and The Balance Sheet: Public Health Accounting and Budgeting Lili Elkins-Thompsons430230No ratings yet

- Slides Review - Final - Exam Prof. EnacheDocument126 pagesSlides Review - Final - Exam Prof. EnachesarahodettemartinezNo ratings yet

- Basic AccountingDocument48 pagesBasic Accounting3122No ratings yet

- To Financial Statement AnalysisDocument23 pagesTo Financial Statement AnalysisKa Hou ChgNo ratings yet

- BOOKKEEPINGDocument102 pagesBOOKKEEPINGAtty. Rheneir MoraNo ratings yet

- Financial AccountingDocument124 pagesFinancial AccountingShashi Ranjan100% (1)

- Dwnload Full College Accounting A Career Approach 13th Edition Scott Solutions Manual PDFDocument20 pagesDwnload Full College Accounting A Career Approach 13th Edition Scott Solutions Manual PDFraisable.maugerg07jpg100% (16)

- Accounting 101 Chapter 1Document39 pagesAccounting 101 Chapter 1Md. Riyad Mahmud 183-15-11991No ratings yet

- Financial Accounting - MGT101 Power Point Slides Lecture 02Document15 pagesFinancial Accounting - MGT101 Power Point Slides Lecture 02Advance KnowledgeNo ratings yet

- Recording Transactions: Powerpoint Presentation by Phil Johnson ©2015 John Wiley & Sons Australia LTDDocument34 pagesRecording Transactions: Powerpoint Presentation by Phil Johnson ©2015 John Wiley & Sons Australia LTDShiTheng Love UNo ratings yet

- Topic 3 - Recording Transactions (STU)Document60 pagesTopic 3 - Recording Transactions (STU)thiennnannn45No ratings yet

- ABM 1 COURSE PACK - WITH EXCEL DISCUSSION Lesson 3Document27 pagesABM 1 COURSE PACK - WITH EXCEL DISCUSSION Lesson 3May AnneNo ratings yet

- CH 1 Part 1Document41 pagesCH 1 Part 1hstptr8wdwNo ratings yet

- Lesson 1Document9 pagesLesson 1Bervette HansNo ratings yet

- The Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Document21 pagesThe Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Peter Shang100% (1)

- CHAPTER 1 - PPT Intro To AccountingDocument14 pagesCHAPTER 1 - PPT Intro To AccountingAmrinNo ratings yet

- School Od Business and Management Institut Teknologi BandungDocument53 pagesSchool Od Business and Management Institut Teknologi BandungadamobirkNo ratings yet

- Accounting Principles: Second Canadian EditionDocument39 pagesAccounting Principles: Second Canadian EditionGizachew ZelekeNo ratings yet

- Part B: Computerised AccountingDocument6 pagesPart B: Computerised AccountingSonakshi JainNo ratings yet

- Financial Analysis - IMIDocument9 pagesFinancial Analysis - IMIrangoli maheshwariNo ratings yet

- Pertemuan 5: Profitability ActivitiesDocument21 pagesPertemuan 5: Profitability ActivitiesSofyan AliNo ratings yet

- 12ENTREP Q2 Module 8 Terminal Report of Business OperationsDocument10 pages12ENTREP Q2 Module 8 Terminal Report of Business OperationsJM Almaden AbadNo ratings yet

- SOB - Financial Accounting and Reporting 1Document87 pagesSOB - Financial Accounting and Reporting 1Miccccch50% (2)

- Lecture01-Introduction To AccountingDocument26 pagesLecture01-Introduction To Accounting錢永健No ratings yet

- Introduction To Accounting and FinanceDocument39 pagesIntroduction To Accounting and FinanceEngr Muhammad RohanNo ratings yet

- The Institutes' Waiver Request Form: For Approval, Please SubmitDocument2 pagesThe Institutes' Waiver Request Form: For Approval, Please SubmitShanmuganathan RamanathanNo ratings yet

- Islamic Banking and Finance Insight On Possibilities For EuropeDocument100 pagesIslamic Banking and Finance Insight On Possibilities For EuropeZulejha IsmihanNo ratings yet

- Unit 3 Financial Services: An Introduction: ObjectivesDocument19 pagesUnit 3 Financial Services: An Introduction: ObjectivesKashif UddinNo ratings yet

- Study Notes With Case Studes HSC Business Studies 2021 VersionDocument71 pagesStudy Notes With Case Studes HSC Business Studies 2021 VersionZoeNo ratings yet

- New MCQS On FM 4 - Managing Banks & Financial InstitutionsDocument7 pagesNew MCQS On FM 4 - Managing Banks & Financial InstitutionsSakshi DongreNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- MBA Accounting Managers 1styear Notes 1Document286 pagesMBA Accounting Managers 1styear Notes 1gibNo ratings yet

- 7-21 (Objectives 7-3, 7-4) : Chapter 7 & 8Document8 pages7-21 (Objectives 7-3, 7-4) : Chapter 7 & 8GuinevereNo ratings yet

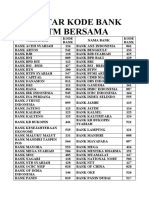

- DAFTAR KODE BANK ScibdDocument2 pagesDAFTAR KODE BANK ScibdKuroi ShinigamiNo ratings yet

- AIS Midterm NotesDocument30 pagesAIS Midterm NotesArielle CabritoNo ratings yet

- ACCT1101 Wk6 Tutorial 5 SolutionsDocument7 pagesACCT1101 Wk6 Tutorial 5 SolutionskyleNo ratings yet

- Kyc Aml CFTDocument201 pagesKyc Aml CFTkunal tyagi100% (2)

- 03 Ch3 Money Market - Practice SheetDocument17 pages03 Ch3 Money Market - Practice SheetDhruvi VachhaniNo ratings yet

- 8int 2011 Jun ADocument9 pages8int 2011 Jun ADawn CaldeiraNo ratings yet

- Corporate Finance Group Assigment - Case Study 2Document24 pagesCorporate Finance Group Assigment - Case Study 2PK LNo ratings yet

- Multiple Choice Questions of TYBBI Auditing (Sem 5)Document15 pagesMultiple Choice Questions of TYBBI Auditing (Sem 5)jai shree krishnaNo ratings yet

- Credo CompanyDocument2 pagesCredo CompanyYan TagleNo ratings yet

- Tool 7 Template Materiality Assessment PaperDocument4 pagesTool 7 Template Materiality Assessment PaperMargenete CasianoNo ratings yet

- Fundamental Analysis ModuleDocument2 pagesFundamental Analysis ModuleJayesh ShahNo ratings yet

- Note Topic 2Document4 pagesNote Topic 2ModraNo ratings yet

- ISB535 Individual AssingmentDocument11 pagesISB535 Individual AssingmentnazrysllNo ratings yet

- Customer Perception Towards Plastic MoneyDocument65 pagesCustomer Perception Towards Plastic Moneyfrnds4everz71% (7)

- Intermediate Acctg 3 Finals With Answers PDFDocument6 pagesIntermediate Acctg 3 Finals With Answers PDFPrincesNo ratings yet

- QUESTIONAIREDocument3 pagesQUESTIONAIREsunny12101986No ratings yet

- New Issue Market in IndiaDocument3 pagesNew Issue Market in IndiaAbhi SinhaNo ratings yet

- GFMP - Debt Markets - Money MarketDocument16 pagesGFMP - Debt Markets - Money MarketrudypatilNo ratings yet

- Partnership AgreementDocument1 pagePartnership AgreementCAMILLE CRIS B. MONASTERIALNo ratings yet

Download as ppt, pdf, or txt

You might also like

- College Accounting A Career Approach 13th Edition Scott Solutions ManualDocument35 pagesCollege Accounting A Career Approach 13th Edition Scott Solutions ManualCalvinMataazscm100% (17)

- Horngrens Accounting 12th Edition Nobles Solutions ManualDocument109 pagesHorngrens Accounting 12th Edition Nobles Solutions ManualAnnGregoryDDSytidk100% (16)

- Syndicated Leveraged Loans During and After The CrisisDocument25 pagesSyndicated Leveraged Loans During and After The Crisisresat gürNo ratings yet

- Fintech Business ModelsDocument8 pagesFintech Business ModelsSarthak0% (1)

- NFO SBI Balanced Advantage Fund PresentationDocument25 pagesNFO SBI Balanced Advantage Fund PresentationJohnTP100% (1)

- Basic Accounting For Non-AccountantsDocument34 pagesBasic Accounting For Non-Accountantsekta100% (1)

- Accounting TransactionsDocument28 pagesAccounting TransactionsPaolo100% (1)

- Nobles Acctg10 PPT 02Document39 pagesNobles Acctg10 PPT 02Tayar ElieNo ratings yet

- Recording Business TransactionsDocument39 pagesRecording Business TransactionsNajwa Al-khateebNo ratings yet

- Chapter 2Document25 pagesChapter 2Jose Carlos SouzaNo ratings yet

- 2-Accounting Equation & Journal Entries, Posting To LedgersDocument12 pages2-Accounting Equation & Journal Entries, Posting To LedgershattarvapeNo ratings yet

- Fa PPT CH 2 - 7eDocument59 pagesFa PPT CH 2 - 7eMaria GomezNo ratings yet

- Topic 2 Financial Statements, Taxes and CashflowsDocument22 pagesTopic 2 Financial Statements, Taxes and CashflowsQianyiiNo ratings yet

- Learning Outcome and Programme Learning Objectives (Plos)Document64 pagesLearning Outcome and Programme Learning Objectives (Plos)ANGEL ROBIN RCBSNo ratings yet

- 3-ACC 1101 Topic 3Document51 pages3-ACC 1101 Topic 3Abd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Financial Statements - Basis of AnalysisDocument44 pagesFinancial Statements - Basis of AnalysisJasmine ActaNo ratings yet

- 10 Examples of Double Entry Accounting 1683305482Document33 pages10 Examples of Double Entry Accounting 1683305482co1g4xqxNo ratings yet

- Accounting Pre Q1 Mid-Term Review 11thDocument36 pagesAccounting Pre Q1 Mid-Term Review 11thOscar Armando Villeda AlvaradoNo ratings yet

- AFM CH 2Document58 pagesAFM CH 2Birhanu MengisteNo ratings yet

- Recording Business Transactions: © 2016 Pearson Education, LTDDocument53 pagesRecording Business Transactions: © 2016 Pearson Education, LTDEce BarlasNo ratings yet

- Financial Accounting, 4eDocument49 pagesFinancial Accounting, 4eZulfiqarNo ratings yet

- Accounting Concepts & PrinciplesDocument26 pagesAccounting Concepts & PrinciplesThy Ngoc100% (1)

- Accounting Basics Using Quickbooks: Presented by Mike KimutaiDocument17 pagesAccounting Basics Using Quickbooks: Presented by Mike KimutaiMike Kimutai 'Sonko'No ratings yet

- CH 2 - FudDocument16 pagesCH 2 - FudbavanthinilNo ratings yet

- Chapter 11 Bookkeeping EntrepDocument37 pagesChapter 11 Bookkeeping EntrepJacel GadonNo ratings yet

- Module 6: Accounting Equation, T-Account, Rules of Debit and Credit and Normal BalancesDocument10 pagesModule 6: Accounting Equation, T-Account, Rules of Debit and Credit and Normal BalancesDarwin AniarNo ratings yet

- PPT 2 - Business TransactionDocument29 pagesPPT 2 - Business Transactionthinkaboutbe14No ratings yet

- The Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Document28 pagesThe Income Statement and Adjusting Entries: Financial Accounting - Lecture 2minghuiNo ratings yet

- Introduction To AccountingDocument39 pagesIntroduction To AccountingVikash HurrydossNo ratings yet

- BBAW2103 - Tutorial 1Document69 pagesBBAW2103 - Tutorial 1M THREE THOUSAND RESOURCESNo ratings yet

- Project On Final Accounts: Vishal Jadhav Nilesh Wadhwa Pankaj Kathayat Ravi Gera MBA 2010Document23 pagesProject On Final Accounts: Vishal Jadhav Nilesh Wadhwa Pankaj Kathayat Ravi Gera MBA 2010Ravi GeraNo ratings yet

- Senior High School Department: Quarter 3 - Module 4: Debit and Credit-The Double - Entry SystemDocument13 pagesSenior High School Department: Quarter 3 - Module 4: Debit and Credit-The Double - Entry SystemJaye Ruanto100% (1)

- Basics of Accounting in VEDocument25 pagesBasics of Accounting in VEIpang NoyoNo ratings yet

- JPIA 1st Tutorial Basic AccountingDocument6 pagesJPIA 1st Tutorial Basic AccountingZee SantisasNo ratings yet

- MAF CH 2 NEWDocument58 pagesMAF CH 2 NEWAsegid H/meskelNo ratings yet

- Basics of Accounting in VEDocument25 pagesBasics of Accounting in VEIpang NoyoNo ratings yet

- Module 4 - Double Entry Bookkeeping System and The Accounting EquationDocument9 pagesModule 4 - Double Entry Bookkeeping System and The Accounting EquationMark Christian BrlNo ratings yet

- Week 9: Introductory Accounting and The Balance Sheet: Public Health Accounting and Budgeting Lili Elkins-ThompsonDocument64 pagesWeek 9: Introductory Accounting and The Balance Sheet: Public Health Accounting and Budgeting Lili Elkins-Thompsons430230No ratings yet

- Slides Review - Final - Exam Prof. EnacheDocument126 pagesSlides Review - Final - Exam Prof. EnachesarahodettemartinezNo ratings yet

- Basic AccountingDocument48 pagesBasic Accounting3122No ratings yet

- To Financial Statement AnalysisDocument23 pagesTo Financial Statement AnalysisKa Hou ChgNo ratings yet

- BOOKKEEPINGDocument102 pagesBOOKKEEPINGAtty. Rheneir MoraNo ratings yet

- Financial AccountingDocument124 pagesFinancial AccountingShashi Ranjan100% (1)

- Dwnload Full College Accounting A Career Approach 13th Edition Scott Solutions Manual PDFDocument20 pagesDwnload Full College Accounting A Career Approach 13th Edition Scott Solutions Manual PDFraisable.maugerg07jpg100% (16)

- Accounting 101 Chapter 1Document39 pagesAccounting 101 Chapter 1Md. Riyad Mahmud 183-15-11991No ratings yet

- Financial Accounting - MGT101 Power Point Slides Lecture 02Document15 pagesFinancial Accounting - MGT101 Power Point Slides Lecture 02Advance KnowledgeNo ratings yet

- Recording Transactions: Powerpoint Presentation by Phil Johnson ©2015 John Wiley & Sons Australia LTDDocument34 pagesRecording Transactions: Powerpoint Presentation by Phil Johnson ©2015 John Wiley & Sons Australia LTDShiTheng Love UNo ratings yet

- Topic 3 - Recording Transactions (STU)Document60 pagesTopic 3 - Recording Transactions (STU)thiennnannn45No ratings yet

- ABM 1 COURSE PACK - WITH EXCEL DISCUSSION Lesson 3Document27 pagesABM 1 COURSE PACK - WITH EXCEL DISCUSSION Lesson 3May AnneNo ratings yet

- CH 1 Part 1Document41 pagesCH 1 Part 1hstptr8wdwNo ratings yet

- Lesson 1Document9 pagesLesson 1Bervette HansNo ratings yet

- The Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Document21 pagesThe Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Peter Shang100% (1)

- CHAPTER 1 - PPT Intro To AccountingDocument14 pagesCHAPTER 1 - PPT Intro To AccountingAmrinNo ratings yet

- School Od Business and Management Institut Teknologi BandungDocument53 pagesSchool Od Business and Management Institut Teknologi BandungadamobirkNo ratings yet

- Accounting Principles: Second Canadian EditionDocument39 pagesAccounting Principles: Second Canadian EditionGizachew ZelekeNo ratings yet

- Part B: Computerised AccountingDocument6 pagesPart B: Computerised AccountingSonakshi JainNo ratings yet

- Financial Analysis - IMIDocument9 pagesFinancial Analysis - IMIrangoli maheshwariNo ratings yet

- Pertemuan 5: Profitability ActivitiesDocument21 pagesPertemuan 5: Profitability ActivitiesSofyan AliNo ratings yet

- 12ENTREP Q2 Module 8 Terminal Report of Business OperationsDocument10 pages12ENTREP Q2 Module 8 Terminal Report of Business OperationsJM Almaden AbadNo ratings yet

- SOB - Financial Accounting and Reporting 1Document87 pagesSOB - Financial Accounting and Reporting 1Miccccch50% (2)

- Lecture01-Introduction To AccountingDocument26 pagesLecture01-Introduction To Accounting錢永健No ratings yet

- Introduction To Accounting and FinanceDocument39 pagesIntroduction To Accounting and FinanceEngr Muhammad RohanNo ratings yet

- The Institutes' Waiver Request Form: For Approval, Please SubmitDocument2 pagesThe Institutes' Waiver Request Form: For Approval, Please SubmitShanmuganathan RamanathanNo ratings yet

- Islamic Banking and Finance Insight On Possibilities For EuropeDocument100 pagesIslamic Banking and Finance Insight On Possibilities For EuropeZulejha IsmihanNo ratings yet

- Unit 3 Financial Services: An Introduction: ObjectivesDocument19 pagesUnit 3 Financial Services: An Introduction: ObjectivesKashif UddinNo ratings yet

- Study Notes With Case Studes HSC Business Studies 2021 VersionDocument71 pagesStudy Notes With Case Studes HSC Business Studies 2021 VersionZoeNo ratings yet

- New MCQS On FM 4 - Managing Banks & Financial InstitutionsDocument7 pagesNew MCQS On FM 4 - Managing Banks & Financial InstitutionsSakshi DongreNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- MBA Accounting Managers 1styear Notes 1Document286 pagesMBA Accounting Managers 1styear Notes 1gibNo ratings yet

- 7-21 (Objectives 7-3, 7-4) : Chapter 7 & 8Document8 pages7-21 (Objectives 7-3, 7-4) : Chapter 7 & 8GuinevereNo ratings yet

- DAFTAR KODE BANK ScibdDocument2 pagesDAFTAR KODE BANK ScibdKuroi ShinigamiNo ratings yet

- AIS Midterm NotesDocument30 pagesAIS Midterm NotesArielle CabritoNo ratings yet

- ACCT1101 Wk6 Tutorial 5 SolutionsDocument7 pagesACCT1101 Wk6 Tutorial 5 SolutionskyleNo ratings yet

- Kyc Aml CFTDocument201 pagesKyc Aml CFTkunal tyagi100% (2)

- 03 Ch3 Money Market - Practice SheetDocument17 pages03 Ch3 Money Market - Practice SheetDhruvi VachhaniNo ratings yet

- 8int 2011 Jun ADocument9 pages8int 2011 Jun ADawn CaldeiraNo ratings yet

- Corporate Finance Group Assigment - Case Study 2Document24 pagesCorporate Finance Group Assigment - Case Study 2PK LNo ratings yet

- Multiple Choice Questions of TYBBI Auditing (Sem 5)Document15 pagesMultiple Choice Questions of TYBBI Auditing (Sem 5)jai shree krishnaNo ratings yet

- Credo CompanyDocument2 pagesCredo CompanyYan TagleNo ratings yet

- Tool 7 Template Materiality Assessment PaperDocument4 pagesTool 7 Template Materiality Assessment PaperMargenete CasianoNo ratings yet

- Fundamental Analysis ModuleDocument2 pagesFundamental Analysis ModuleJayesh ShahNo ratings yet

- Note Topic 2Document4 pagesNote Topic 2ModraNo ratings yet

- ISB535 Individual AssingmentDocument11 pagesISB535 Individual AssingmentnazrysllNo ratings yet

- Customer Perception Towards Plastic MoneyDocument65 pagesCustomer Perception Towards Plastic Moneyfrnds4everz71% (7)

- Intermediate Acctg 3 Finals With Answers PDFDocument6 pagesIntermediate Acctg 3 Finals With Answers PDFPrincesNo ratings yet

- QUESTIONAIREDocument3 pagesQUESTIONAIREsunny12101986No ratings yet

- New Issue Market in IndiaDocument3 pagesNew Issue Market in IndiaAbhi SinhaNo ratings yet

- GFMP - Debt Markets - Money MarketDocument16 pagesGFMP - Debt Markets - Money MarketrudypatilNo ratings yet

- Partnership AgreementDocument1 pagePartnership AgreementCAMILLE CRIS B. MONASTERIALNo ratings yet