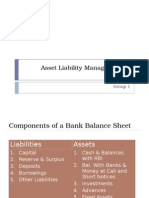

Assets Liability Management

Assets Liability Management

You might also like

- WWADocument8 pagesWWARachid Ahmed100% (4)

- FRM 2019 Part II - Quicksheet PDFDocument6 pagesFRM 2019 Part II - Quicksheet PDFswetha reddy100% (2)

- Credit Risk PolicyDocument32 pagesCredit Risk PolicyRajib Ranjan Samal100% (1)

- Risk CabreraDocument54 pagesRisk CabreraJohn Rey Enriquez100% (2)

- Aci Dealing Certificate Q&aDocument152 pagesAci Dealing Certificate Q&aWesta GeafricaNo ratings yet

- Asset Liability Management in BanksDocument29 pagesAsset Liability Management in Bankseknath2000No ratings yet

- Asset Liability ManagementDocument18 pagesAsset Liability Managementmahesh19689No ratings yet

- Liquidity and Interest Risk ManagementDocument29 pagesLiquidity and Interest Risk Managementjames100% (24)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- The Rothschilds Stage Revolutions in Tunisia and EgyptDocument10 pagesThe Rothschilds Stage Revolutions in Tunisia and EgyptZeka Sumerian OutlawNo ratings yet

- General Economics PDFDocument27 pagesGeneral Economics PDFhkamabi86% (7)

- Commercial BankingDocument15 pagesCommercial BankingDivYaDarBhaNo ratings yet

- 3 - FIG09104 Fin. Mark.& InsDocument49 pages3 - FIG09104 Fin. Mark.& InsMoud KhalfaniNo ratings yet

- Asset Liability Management: in BanksDocument44 pagesAsset Liability Management: in Bankssachin21singhNo ratings yet

- Asset Liability Management - TMDocument11 pagesAsset Liability Management - TMPriyanka Srinivasulu ReddyNo ratings yet

- Bank VivaDocument38 pagesBank VivaDebasis NayakNo ratings yet

- Asset Liability Management in BanksDocument29 pagesAsset Liability Management in BanksAashima Sharma BhasinNo ratings yet

- Risk Management & Asset Liability Management at Union Bank of IndiaDocument24 pagesRisk Management & Asset Liability Management at Union Bank of IndiaVinay GoyalNo ratings yet

- MFS - Asset Liability Management MuskanDocument33 pagesMFS - Asset Liability Management Muskansangambhardwaj64No ratings yet

- Principles of Asset and Liability Management: Minimum Correct Answers For This Module: 4/8Document11 pagesPrinciples of Asset and Liability Management: Minimum Correct Answers For This Module: 4/8Jovan SsenkandwaNo ratings yet

- Asset Liability Management of Icici Bank: Presented By: Paul Caroline Poornima Sonal AnvinDocument47 pagesAsset Liability Management of Icici Bank: Presented By: Paul Caroline Poornima Sonal AnvinsonalsankhlaNo ratings yet

- Asset Liability Management in Banks: Group 1Document29 pagesAsset Liability Management in Banks: Group 1AjDonNo ratings yet

- 1a. MeaningDocument33 pages1a. MeaningalpeshNo ratings yet

- Department of Commerce (PG) Aigs CHAPTER 1: Introduction DefinitionsDocument12 pagesDepartment of Commerce (PG) Aigs CHAPTER 1: Introduction DefinitionsRanjitha NNo ratings yet

- Asset Liability Management Module A C.S.Balakrishnan Faculty Member, SPBT CollegeDocument43 pagesAsset Liability Management Module A C.S.Balakrishnan Faculty Member, SPBT Collegetimtim1496No ratings yet

- Liquidity RiskDocument24 pagesLiquidity RiskTing YangNo ratings yet

- This Report Is On Assets and Liability Management of Different BanksDocument22 pagesThis Report Is On Assets and Liability Management of Different BanksPratik_Gupta_3369No ratings yet

- ALM and Fund ManagementDocument60 pagesALM and Fund Managementmanoj rijalNo ratings yet

- Treasury and Asset-Liability Management: CaiibDocument10 pagesTreasury and Asset-Liability Management: CaiibAksNo ratings yet

- Assets Liabilities ManagementDocument18 pagesAssets Liabilities ManagementNANDINI GUPTANo ratings yet

- BFM Numericals .10Document19 pagesBFM Numericals .10Durga Naik KNo ratings yet

- FMTD - RIsk Management in BanksDocument6 pagesFMTD - RIsk Management in Banksajay_chitreNo ratings yet

- Liquidity RiskDocument19 pagesLiquidity RiskJagjeet AjmaniNo ratings yet

- Asset Liability Management in Banks (Alm) : Follow AllbankingsolutionsDocument6 pagesAsset Liability Management in Banks (Alm) : Follow AllbankingsolutionsSanjeet MohantyNo ratings yet

- Asset Liability ManagementDocument35 pagesAsset Liability ManagementNiket Dattani100% (1)

- 228module - A PDFDocument20 pages228module - A PDFSatishKumarRajendranNo ratings yet

- Ans:ss Prospective Borrower: An Individual, Organization or Company Having Requirement of Additional Fund ForDocument3 pagesAns:ss Prospective Borrower: An Individual, Organization or Company Having Requirement of Additional Fund ForMd AlimNo ratings yet

- ALM Maturity ProfileDocument16 pagesALM Maturity ProfileMorshed Chowdhury ZishanNo ratings yet

- Model ALM PolicyDocument9 pagesModel ALM Policytreddy249No ratings yet

- Asset Liability Management (Alm)Document48 pagesAsset Liability Management (Alm)ingaleabhijeet2010No ratings yet

- ALMDocument15 pagesALMGaurav PandeyNo ratings yet

- Asset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolDocument26 pagesAsset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolBlake SheltonNo ratings yet

- Risk Management Framework: by Prof Santosh KumarDocument30 pagesRisk Management Framework: by Prof Santosh KumarAYUSH RAVINo ratings yet

- Asset - Liability Management System in Banks - Guidelines: 4. ALM Information SystemsDocument12 pagesAsset - Liability Management System in Banks - Guidelines: 4. ALM Information SystemsKevin VazNo ratings yet

- Asset Liability Management Under Risk FrameworkDocument9 pagesAsset Liability Management Under Risk FrameworklinnnehNo ratings yet

- Risk Management in Banks Under Basel NormsDocument53 pagesRisk Management in Banks Under Basel NormsSahni SahniNo ratings yet

- Ubi AlmDocument20 pagesUbi AlmNagendraprasad PuppalaNo ratings yet

- Chapter 22 OutlineDocument6 pagesChapter 22 OutlinemacysilveniaNo ratings yet

- Lecture 1Document9 pagesLecture 1Rafsun HimelNo ratings yet

- Chapter 3 ALM 1Document56 pagesChapter 3 ALM 1Niloy AhmedNo ratings yet

- Asset Liability Management Canara BankDocument102 pagesAsset Liability Management Canara BankAkash Jadhav0% (1)

- Asset Liability Management in Banks 1Document51 pagesAsset Liability Management in Banks 1Akshay JadhavNo ratings yet

- Assessing The Value of Asset Liability Management PakistanDocument16 pagesAssessing The Value of Asset Liability Management PakistanVenkat IyerNo ratings yet

- Iquidity Risk ManagementDocument20 pagesIquidity Risk ManagementMAHENDERNo ratings yet

- Treasury Researched AssignDocument9 pagesTreasury Researched AssignChristian SalazarNo ratings yet

- Asset Liability Management in BanksDocument36 pagesAsset Liability Management in BanksHoàng Trần HữuNo ratings yet

- Lecture 4 - Bank's Assets and Liability ManagementDocument16 pagesLecture 4 - Bank's Assets and Liability ManagementLeyli MelikovaNo ratings yet

- Literature ReviewDocument9 pagesLiterature ReviewAnkur Upadhyay0% (1)

- Paying Creditors:: 1.0 Risk ManagementDocument4 pagesPaying Creditors:: 1.0 Risk Managementdeepak_computerenggNo ratings yet

- Risk Management in Banking CompaniesDocument2 pagesRisk Management in Banking CompaniesPrashanth NaraenNo ratings yet

- Chapter ALMDocument19 pagesChapter ALMFinance & Banking BG 21No ratings yet

- Liquidity Risk Management - SnapshotDocument30 pagesLiquidity Risk Management - SnapshotAhsan AliNo ratings yet

- Asset and Liability ManagementDocument8 pagesAsset and Liability ManagementPriyanka YadavNo ratings yet

- Capital Adequacy: Credit ExposureDocument10 pagesCapital Adequacy: Credit ExposureHimani DhingraNo ratings yet

- BP&SM (Module 4.0) (Strategic Implementation) (BBA - D) (Sem 6)Document55 pagesBP&SM (Module 4.0) (Strategic Implementation) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- Marginal Costing and Cost Volume Profit AnalysisDocument16 pagesMarginal Costing and Cost Volume Profit Analysispriyanka choudharyNo ratings yet

- Public Relations Session 5-CSR: Dr. Priyanka DasguptaDocument6 pagesPublic Relations Session 5-CSR: Dr. Priyanka Dasguptapriyanka choudharyNo ratings yet

- PR Research and MeasurementDocument10 pagesPR Research and Measurementpriyanka choudharyNo ratings yet

- Public Relations Session 4 Writing: Dr. Priyanka DasguptaDocument12 pagesPublic Relations Session 4 Writing: Dr. Priyanka Dasguptapriyanka choudharyNo ratings yet

- Product - StrategyDocument43 pagesProduct - Strategypriyanka choudharyNo ratings yet

- BP&SM (Module 3.0) (Strategic Formulation) (BBA - D) (Sem 6)Document60 pagesBP&SM (Module 3.0) (Strategic Formulation) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- BP&SM (Module 2.0) (Strategic Analysis Models & Tools) (BBA - D) (Sem 6)Document34 pagesBP&SM (Module 2.0) (Strategic Analysis Models & Tools) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- BP&SM (Module 1.0) (Intro To Strategic MGT & Strategic Intent) (BBA - D) (Sem 6)Document56 pagesBP&SM (Module 1.0) (Intro To Strategic MGT & Strategic Intent) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- Charles P.jones Investment & Portfolio SBUChpt2Document25 pagesCharles P.jones Investment & Portfolio SBUChpt2Asfand Yar KhanNo ratings yet

- Risk Management in BankingDocument6 pagesRisk Management in BankingPranto Pritom Roy1531stNo ratings yet

- Financial Crisis in The PhilippinesDocument11 pagesFinancial Crisis in The PhilippinesApril ManjaresNo ratings yet

- Chapter06 TestBankDocument50 pagesChapter06 TestBankannie100% (1)

- Overview of Banking Sector and Credit Analysis ofDocument23 pagesOverview of Banking Sector and Credit Analysis ofrahuln181No ratings yet

- FIM Lecture V VI: Why Do Interest Rates Change?Document15 pagesFIM Lecture V VI: Why Do Interest Rates Change?Aniket GuptaNo ratings yet

- The Impact of IFRS Convergence On Market Liquidity: Evidence From IndiaDocument20 pagesThe Impact of IFRS Convergence On Market Liquidity: Evidence From IndiaEllen AgustinNo ratings yet

- White PaperDocument13 pagesWhite PapercrissalahNo ratings yet

- 3 Minute BB StrategyDocument9 pages3 Minute BB Strategyhammersoup24No ratings yet

- Y Combinator Startup School 2007 NotesDocument20 pagesY Combinator Startup School 2007 Notesotterley100% (90)

- Project Report: Mutual FundDocument32 pagesProject Report: Mutual FundArian HaqueNo ratings yet

- 2CEXAM Mock Question Licensing Examination Paper 8Document9 pages2CEXAM Mock Question Licensing Examination Paper 8Tsz Ngong KoNo ratings yet

- Adjudication Order in Respect of Sureena C Shah Page 1 of 30Document30 pagesAdjudication Order in Respect of Sureena C Shah Page 1 of 30Pratim MajumderNo ratings yet

- Behavioral FinanceDocument31 pagesBehavioral Financevy phạm100% (1)

- Financial Ratios Analysis: NESTLE 2013 TO 2015Document20 pagesFinancial Ratios Analysis: NESTLE 2013 TO 2015Hebatallah FahmyNo ratings yet

- Contemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test BankDocument19 pagesContemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test Bankfrederick100% (30)

- Property Derivatives For Managing European Real-Estate Risk: Frank J. FabozziDocument19 pagesProperty Derivatives For Managing European Real-Estate Risk: Frank J. FabozziVictor GutierrezNo ratings yet

- Summer Internship: " Perception Towards Mutual Fund - A Study of Probable Individual Investors"Document53 pagesSummer Internship: " Perception Towards Mutual Fund - A Study of Probable Individual Investors"Gayatri DasNo ratings yet

- Multiple Choice Questions Financial MarketsDocument16 pagesMultiple Choice Questions Financial Marketshannabee00No ratings yet

- Ratio Short Discussion: Benefits Is The Major Underlying Reason of This Case Despite TheDocument2 pagesRatio Short Discussion: Benefits Is The Major Underlying Reason of This Case Despite TheCJ IbaleNo ratings yet

- Bank of Cyprus Annual Report 2008 ENGDocument169 pagesBank of Cyprus Annual Report 2008 ENGDave LiNo ratings yet

- Mark Scheme (Results) June 2015: International GCSE Accounting (4AC0)Document14 pagesMark Scheme (Results) June 2015: International GCSE Accounting (4AC0)Syeda Malika AnjumNo ratings yet

- Padala Rama Reddi College A Study On Customer Perception Towards Gold As An InvestmentDocument74 pagesPadala Rama Reddi College A Study On Customer Perception Towards Gold As An InvestmentMubeenNo ratings yet

Download as pptx, pdf, or txt

You might also like

- WWADocument8 pagesWWARachid Ahmed100% (4)

- FRM 2019 Part II - Quicksheet PDFDocument6 pagesFRM 2019 Part II - Quicksheet PDFswetha reddy100% (2)

- Credit Risk PolicyDocument32 pagesCredit Risk PolicyRajib Ranjan Samal100% (1)

- Risk CabreraDocument54 pagesRisk CabreraJohn Rey Enriquez100% (2)

- Aci Dealing Certificate Q&aDocument152 pagesAci Dealing Certificate Q&aWesta GeafricaNo ratings yet

- Asset Liability Management in BanksDocument29 pagesAsset Liability Management in Bankseknath2000No ratings yet

- Asset Liability ManagementDocument18 pagesAsset Liability Managementmahesh19689No ratings yet

- Liquidity and Interest Risk ManagementDocument29 pagesLiquidity and Interest Risk Managementjames100% (24)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- The Rothschilds Stage Revolutions in Tunisia and EgyptDocument10 pagesThe Rothschilds Stage Revolutions in Tunisia and EgyptZeka Sumerian OutlawNo ratings yet

- General Economics PDFDocument27 pagesGeneral Economics PDFhkamabi86% (7)

- Commercial BankingDocument15 pagesCommercial BankingDivYaDarBhaNo ratings yet

- 3 - FIG09104 Fin. Mark.& InsDocument49 pages3 - FIG09104 Fin. Mark.& InsMoud KhalfaniNo ratings yet

- Asset Liability Management: in BanksDocument44 pagesAsset Liability Management: in Bankssachin21singhNo ratings yet

- Asset Liability Management - TMDocument11 pagesAsset Liability Management - TMPriyanka Srinivasulu ReddyNo ratings yet

- Bank VivaDocument38 pagesBank VivaDebasis NayakNo ratings yet

- Asset Liability Management in BanksDocument29 pagesAsset Liability Management in BanksAashima Sharma BhasinNo ratings yet

- Risk Management & Asset Liability Management at Union Bank of IndiaDocument24 pagesRisk Management & Asset Liability Management at Union Bank of IndiaVinay GoyalNo ratings yet

- MFS - Asset Liability Management MuskanDocument33 pagesMFS - Asset Liability Management Muskansangambhardwaj64No ratings yet

- Principles of Asset and Liability Management: Minimum Correct Answers For This Module: 4/8Document11 pagesPrinciples of Asset and Liability Management: Minimum Correct Answers For This Module: 4/8Jovan SsenkandwaNo ratings yet

- Asset Liability Management of Icici Bank: Presented By: Paul Caroline Poornima Sonal AnvinDocument47 pagesAsset Liability Management of Icici Bank: Presented By: Paul Caroline Poornima Sonal AnvinsonalsankhlaNo ratings yet

- Asset Liability Management in Banks: Group 1Document29 pagesAsset Liability Management in Banks: Group 1AjDonNo ratings yet

- 1a. MeaningDocument33 pages1a. MeaningalpeshNo ratings yet

- Department of Commerce (PG) Aigs CHAPTER 1: Introduction DefinitionsDocument12 pagesDepartment of Commerce (PG) Aigs CHAPTER 1: Introduction DefinitionsRanjitha NNo ratings yet

- Asset Liability Management Module A C.S.Balakrishnan Faculty Member, SPBT CollegeDocument43 pagesAsset Liability Management Module A C.S.Balakrishnan Faculty Member, SPBT Collegetimtim1496No ratings yet

- Liquidity RiskDocument24 pagesLiquidity RiskTing YangNo ratings yet

- This Report Is On Assets and Liability Management of Different BanksDocument22 pagesThis Report Is On Assets and Liability Management of Different BanksPratik_Gupta_3369No ratings yet

- ALM and Fund ManagementDocument60 pagesALM and Fund Managementmanoj rijalNo ratings yet

- Treasury and Asset-Liability Management: CaiibDocument10 pagesTreasury and Asset-Liability Management: CaiibAksNo ratings yet

- Assets Liabilities ManagementDocument18 pagesAssets Liabilities ManagementNANDINI GUPTANo ratings yet

- BFM Numericals .10Document19 pagesBFM Numericals .10Durga Naik KNo ratings yet

- FMTD - RIsk Management in BanksDocument6 pagesFMTD - RIsk Management in Banksajay_chitreNo ratings yet

- Liquidity RiskDocument19 pagesLiquidity RiskJagjeet AjmaniNo ratings yet

- Asset Liability Management in Banks (Alm) : Follow AllbankingsolutionsDocument6 pagesAsset Liability Management in Banks (Alm) : Follow AllbankingsolutionsSanjeet MohantyNo ratings yet

- Asset Liability ManagementDocument35 pagesAsset Liability ManagementNiket Dattani100% (1)

- 228module - A PDFDocument20 pages228module - A PDFSatishKumarRajendranNo ratings yet

- Ans:ss Prospective Borrower: An Individual, Organization or Company Having Requirement of Additional Fund ForDocument3 pagesAns:ss Prospective Borrower: An Individual, Organization or Company Having Requirement of Additional Fund ForMd AlimNo ratings yet

- ALM Maturity ProfileDocument16 pagesALM Maturity ProfileMorshed Chowdhury ZishanNo ratings yet

- Model ALM PolicyDocument9 pagesModel ALM Policytreddy249No ratings yet

- Asset Liability Management (Alm)Document48 pagesAsset Liability Management (Alm)ingaleabhijeet2010No ratings yet

- ALMDocument15 pagesALMGaurav PandeyNo ratings yet

- Asset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolDocument26 pagesAsset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolBlake SheltonNo ratings yet

- Risk Management Framework: by Prof Santosh KumarDocument30 pagesRisk Management Framework: by Prof Santosh KumarAYUSH RAVINo ratings yet

- Asset - Liability Management System in Banks - Guidelines: 4. ALM Information SystemsDocument12 pagesAsset - Liability Management System in Banks - Guidelines: 4. ALM Information SystemsKevin VazNo ratings yet

- Asset Liability Management Under Risk FrameworkDocument9 pagesAsset Liability Management Under Risk FrameworklinnnehNo ratings yet

- Risk Management in Banks Under Basel NormsDocument53 pagesRisk Management in Banks Under Basel NormsSahni SahniNo ratings yet

- Ubi AlmDocument20 pagesUbi AlmNagendraprasad PuppalaNo ratings yet

- Chapter 22 OutlineDocument6 pagesChapter 22 OutlinemacysilveniaNo ratings yet

- Lecture 1Document9 pagesLecture 1Rafsun HimelNo ratings yet

- Chapter 3 ALM 1Document56 pagesChapter 3 ALM 1Niloy AhmedNo ratings yet

- Asset Liability Management Canara BankDocument102 pagesAsset Liability Management Canara BankAkash Jadhav0% (1)

- Asset Liability Management in Banks 1Document51 pagesAsset Liability Management in Banks 1Akshay JadhavNo ratings yet

- Assessing The Value of Asset Liability Management PakistanDocument16 pagesAssessing The Value of Asset Liability Management PakistanVenkat IyerNo ratings yet

- Iquidity Risk ManagementDocument20 pagesIquidity Risk ManagementMAHENDERNo ratings yet

- Treasury Researched AssignDocument9 pagesTreasury Researched AssignChristian SalazarNo ratings yet

- Asset Liability Management in BanksDocument36 pagesAsset Liability Management in BanksHoàng Trần HữuNo ratings yet

- Lecture 4 - Bank's Assets and Liability ManagementDocument16 pagesLecture 4 - Bank's Assets and Liability ManagementLeyli MelikovaNo ratings yet

- Literature ReviewDocument9 pagesLiterature ReviewAnkur Upadhyay0% (1)

- Paying Creditors:: 1.0 Risk ManagementDocument4 pagesPaying Creditors:: 1.0 Risk Managementdeepak_computerenggNo ratings yet

- Risk Management in Banking CompaniesDocument2 pagesRisk Management in Banking CompaniesPrashanth NaraenNo ratings yet

- Chapter ALMDocument19 pagesChapter ALMFinance & Banking BG 21No ratings yet

- Liquidity Risk Management - SnapshotDocument30 pagesLiquidity Risk Management - SnapshotAhsan AliNo ratings yet

- Asset and Liability ManagementDocument8 pagesAsset and Liability ManagementPriyanka YadavNo ratings yet

- Capital Adequacy: Credit ExposureDocument10 pagesCapital Adequacy: Credit ExposureHimani DhingraNo ratings yet

- BP&SM (Module 4.0) (Strategic Implementation) (BBA - D) (Sem 6)Document55 pagesBP&SM (Module 4.0) (Strategic Implementation) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- Marginal Costing and Cost Volume Profit AnalysisDocument16 pagesMarginal Costing and Cost Volume Profit Analysispriyanka choudharyNo ratings yet

- Public Relations Session 5-CSR: Dr. Priyanka DasguptaDocument6 pagesPublic Relations Session 5-CSR: Dr. Priyanka Dasguptapriyanka choudharyNo ratings yet

- PR Research and MeasurementDocument10 pagesPR Research and Measurementpriyanka choudharyNo ratings yet

- Public Relations Session 4 Writing: Dr. Priyanka DasguptaDocument12 pagesPublic Relations Session 4 Writing: Dr. Priyanka Dasguptapriyanka choudharyNo ratings yet

- Product - StrategyDocument43 pagesProduct - Strategypriyanka choudharyNo ratings yet

- BP&SM (Module 3.0) (Strategic Formulation) (BBA - D) (Sem 6)Document60 pagesBP&SM (Module 3.0) (Strategic Formulation) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- BP&SM (Module 2.0) (Strategic Analysis Models & Tools) (BBA - D) (Sem 6)Document34 pagesBP&SM (Module 2.0) (Strategic Analysis Models & Tools) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- BP&SM (Module 1.0) (Intro To Strategic MGT & Strategic Intent) (BBA - D) (Sem 6)Document56 pagesBP&SM (Module 1.0) (Intro To Strategic MGT & Strategic Intent) (BBA - D) (Sem 6)priyanka choudharyNo ratings yet

- Charles P.jones Investment & Portfolio SBUChpt2Document25 pagesCharles P.jones Investment & Portfolio SBUChpt2Asfand Yar KhanNo ratings yet

- Risk Management in BankingDocument6 pagesRisk Management in BankingPranto Pritom Roy1531stNo ratings yet

- Financial Crisis in The PhilippinesDocument11 pagesFinancial Crisis in The PhilippinesApril ManjaresNo ratings yet

- Chapter06 TestBankDocument50 pagesChapter06 TestBankannie100% (1)

- Overview of Banking Sector and Credit Analysis ofDocument23 pagesOverview of Banking Sector and Credit Analysis ofrahuln181No ratings yet

- FIM Lecture V VI: Why Do Interest Rates Change?Document15 pagesFIM Lecture V VI: Why Do Interest Rates Change?Aniket GuptaNo ratings yet

- The Impact of IFRS Convergence On Market Liquidity: Evidence From IndiaDocument20 pagesThe Impact of IFRS Convergence On Market Liquidity: Evidence From IndiaEllen AgustinNo ratings yet

- White PaperDocument13 pagesWhite PapercrissalahNo ratings yet

- 3 Minute BB StrategyDocument9 pages3 Minute BB Strategyhammersoup24No ratings yet

- Y Combinator Startup School 2007 NotesDocument20 pagesY Combinator Startup School 2007 Notesotterley100% (90)

- Project Report: Mutual FundDocument32 pagesProject Report: Mutual FundArian HaqueNo ratings yet

- 2CEXAM Mock Question Licensing Examination Paper 8Document9 pages2CEXAM Mock Question Licensing Examination Paper 8Tsz Ngong KoNo ratings yet

- Adjudication Order in Respect of Sureena C Shah Page 1 of 30Document30 pagesAdjudication Order in Respect of Sureena C Shah Page 1 of 30Pratim MajumderNo ratings yet

- Behavioral FinanceDocument31 pagesBehavioral Financevy phạm100% (1)

- Financial Ratios Analysis: NESTLE 2013 TO 2015Document20 pagesFinancial Ratios Analysis: NESTLE 2013 TO 2015Hebatallah FahmyNo ratings yet

- Contemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test BankDocument19 pagesContemporary Financial Management 13th Edition by Moyer McGuigan Rao ISBN Test Bankfrederick100% (30)

- Property Derivatives For Managing European Real-Estate Risk: Frank J. FabozziDocument19 pagesProperty Derivatives For Managing European Real-Estate Risk: Frank J. FabozziVictor GutierrezNo ratings yet

- Summer Internship: " Perception Towards Mutual Fund - A Study of Probable Individual Investors"Document53 pagesSummer Internship: " Perception Towards Mutual Fund - A Study of Probable Individual Investors"Gayatri DasNo ratings yet

- Multiple Choice Questions Financial MarketsDocument16 pagesMultiple Choice Questions Financial Marketshannabee00No ratings yet

- Ratio Short Discussion: Benefits Is The Major Underlying Reason of This Case Despite TheDocument2 pagesRatio Short Discussion: Benefits Is The Major Underlying Reason of This Case Despite TheCJ IbaleNo ratings yet

- Bank of Cyprus Annual Report 2008 ENGDocument169 pagesBank of Cyprus Annual Report 2008 ENGDave LiNo ratings yet

- Mark Scheme (Results) June 2015: International GCSE Accounting (4AC0)Document14 pagesMark Scheme (Results) June 2015: International GCSE Accounting (4AC0)Syeda Malika AnjumNo ratings yet

- Padala Rama Reddi College A Study On Customer Perception Towards Gold As An InvestmentDocument74 pagesPadala Rama Reddi College A Study On Customer Perception Towards Gold As An InvestmentMubeenNo ratings yet