Download as ppt, pdf, or txt

You might also like

- 2020 Mock Exam B - Morning SessionDocument27 pages2020 Mock Exam B - Morning SessionLê Chấn Phong100% (2)

- Summary: Financial Intelligence: Review and Analysis of Berman and Knight's BookFrom EverandSummary: Financial Intelligence: Review and Analysis of Berman and Knight's BookNo ratings yet

- Fundamentals of Basic Accounting AlilingDocument9 pagesFundamentals of Basic Accounting AlilingEmil EnriquezNo ratings yet

- Synthesis ReviewerDocument10 pagesSynthesis ReviewerStela Marie CarandangNo ratings yet

- Company Outsiders: Resources TodayDocument20 pagesCompany Outsiders: Resources TodaySarbani Mishra0% (1)

- External Users: Not Directly Involved. These Are Secondary Users of Financial Information Who Are PartiesDocument8 pagesExternal Users: Not Directly Involved. These Are Secondary Users of Financial Information Who Are PartiesAizel AlindoyNo ratings yet

- Culminating Activity: Quarter 1 - Module 1Document38 pagesCulminating Activity: Quarter 1 - Module 1Kelvin Jay Sebastian Sapla95% (19)

- Chemilite Case StudyDocument12 pagesChemilite Case StudyRavi Pratap Singh Tomar100% (3)

- E1925 - F2020 Project Guidelines PDFDocument3 pagesE1925 - F2020 Project Guidelines PDFjuenaticsNo ratings yet

- Structured Product PresentationDocument12 pagesStructured Product PresentationVibhusha SinghNo ratings yet

- An Intro To Bussiness AccountingDocument57 pagesAn Intro To Bussiness AccountingNadia AnuarNo ratings yet

- Financialmanagementconceptroles 120129211622 Phpapp 01Document23 pagesFinancialmanagementconceptroles 120129211622 Phpapp 01Ricardo ValverdeNo ratings yet

- Financial AccountingDocument25 pagesFinancial AccountingTanishi JaiswalNo ratings yet

- Class 2 PDFDocument17 pagesClass 2 PDFRajat AgrawalNo ratings yet

- FAR 1st Discusssion NoteDocument5 pagesFAR 1st Discusssion NoteApril GumiranNo ratings yet

- Chapter 1 Notes: Created Tags UpdatedDocument6 pagesChapter 1 Notes: Created Tags UpdatedTristan RamosNo ratings yet

- Ais P1Document55 pagesAis P1cali cdNo ratings yet

- Additional Reading 2Document32 pagesAdditional Reading 2Htain Lin MaungNo ratings yet

- (2020) #1 - Intro To Cost Analysis EstimationDocument27 pages(2020) #1 - Intro To Cost Analysis EstimationSiti Aisyah Nor HalisaNo ratings yet

- Accounting Concepts and Principles: Chapter TwoDocument50 pagesAccounting Concepts and Principles: Chapter TwoAnteneh GetahunNo ratings yet

- Financial AccountingDocument54 pagesFinancial Accountingnisha deotaleNo ratings yet

- Chapter 1 Intro To AccoutingDocument32 pagesChapter 1 Intro To Accoutingprincekelvin09No ratings yet

- Trading Basics: AccountingDocument10 pagesTrading Basics: AccountingNonameforeverNo ratings yet

- AccountingDocument10 pagesAccountingNataly Toro ZoaNo ratings yet

- Introduction To AccountancyDocument8 pagesIntroduction To Accountancyjo jo paopNo ratings yet

- DPB2012 - T6Document26 pagesDPB2012 - T6suhanaNo ratings yet

- FMA NotesDocument19 pagesFMA NotesLAXIANo ratings yet

- FAR Acc111 Week 1-3 Definition ReviewerDocument5 pagesFAR Acc111 Week 1-3 Definition ReviewerRIJANE MAE EMPLEO100% (1)

- Cost and Management AccountingDocument51 pagesCost and Management Accountingabhijeet0% (1)

- Hand Out in Basic AccountingDocument32 pagesHand Out in Basic AccountingJemuell RedNo ratings yet

- Lecture NotesDocument100 pagesLecture Notesgrace.kokhcNo ratings yet

- Part Two: Financial Accounting: An IntroductionDocument139 pagesPart Two: Financial Accounting: An IntroductionRobel Habtamu100% (1)

- Introduction To AccountingDocument58 pagesIntroduction To Accountingmahendrabpatel100% (3)

- Financial Accounting For ManagersDocument40 pagesFinancial Accounting For ManagersRAHUL G JAIN 1727621No ratings yet

- For 2007-09, PGDM Batch: Basic Accounting: Concepts, Techniques, ConventionsDocument18 pagesFor 2007-09, PGDM Batch: Basic Accounting: Concepts, Techniques, ConventionsHriday PrasadNo ratings yet

- Flash Card SlidesDocument29 pagesFlash Card SlidesMary100% (2)

- Chapter 1Document28 pagesChapter 1soujanyaNo ratings yet

- Fundamentals of AccountingDocument26 pagesFundamentals of AccountingSofia Naraine OnilongoNo ratings yet

- Key Terms of Accounting PrinciplesDocument16 pagesKey Terms of Accounting PrinciplesANH DAO BUI LANNo ratings yet

- FAE4e - SM - Ch02 120216 - Excluding Assignment QuestionsDocument37 pagesFAE4e - SM - Ch02 120216 - Excluding Assignment QuestionsKathy Thanh PKNo ratings yet

- Basics of AccountingDocument43 pagesBasics of Accounting6pdqqsf59rNo ratings yet

- Chapter 1 MBA 560Document47 pagesChapter 1 MBA 560CendorlyNo ratings yet

- Topic 2 Regulatory and Conceptual FrameworkDocument15 pagesTopic 2 Regulatory and Conceptual FrameworkfeyNo ratings yet

- Importance of Accounting: IdentifiesDocument20 pagesImportance of Accounting: IdentifiesNikhil GargNo ratings yet

- 1 Accounting and Its EnvironmentDocument30 pages1 Accounting and Its EnvironmentJohn Alfred CastinoNo ratings yet

- Session 1 - Introduction To Accounting and Balance SheetDocument32 pagesSession 1 - Introduction To Accounting and Balance Sheethieucaiminh155No ratings yet

- Finance For Non Finance Professionals Statements and RatiosDocument32 pagesFinance For Non Finance Professionals Statements and Ratioskrithika1288No ratings yet

- Overview of Businesses: Prelims ReviewerDocument3 pagesOverview of Businesses: Prelims ReviewerZymon Andrew MaquintoNo ratings yet

- Accounting in ActionDocument7 pagesAccounting in ActionIda PaluszczyszynNo ratings yet

- Basic Accounting ConceptsDocument61 pagesBasic Accounting ConceptsJAY Solanki100% (1)

- Chapter One FABDocument63 pagesChapter One FABKirubel SolomonNo ratings yet

- Notes - Introduction To Financial Statements, Ratio Analysis, Business OrganisationDocument8 pagesNotes - Introduction To Financial Statements, Ratio Analysis, Business OrganisationSilke HerbertNo ratings yet

- Financial Statements AnalysisDocument36 pagesFinancial Statements AnalysisinasNo ratings yet

- Research SupportDocument28 pagesResearch SupportVikãsh MishrâNo ratings yet

- Accounting Information: Users and UsesDocument38 pagesAccounting Information: Users and UsesVia Oktaviani KusnadiNo ratings yet

- 01-Accounting Principles CHE40Document34 pages01-Accounting Principles CHE40Faye Blair MarkovaNo ratings yet

- Accounting Slides 2Document100 pagesAccounting Slides 2Nawaf Al-HarthiNo ratings yet

- CH - 01 - Accounting in Action (BUP) (EDITED)Document45 pagesCH - 01 - Accounting in Action (BUP) (EDITED)jimfinch512No ratings yet

- POA Key TermsDocument23 pagesPOA Key TermsAnonymous LC5kFdtcNo ratings yet

- Chapter 1-SETECDocument32 pagesChapter 1-SETEChemaakithNo ratings yet

- Aat Level 3 Fapr 1-2Document29 pagesAat Level 3 Fapr 1-2Ira CașuNo ratings yet

- Chapter 1 - Accounting in ActionDocument42 pagesChapter 1 - Accounting in ActionFify AmalindaNo ratings yet

- Sole Proprietorship: Role of AccountingDocument18 pagesSole Proprietorship: Role of Accountingelise limNo ratings yet

- Fme Accounting Terminology ChecklistDocument6 pagesFme Accounting Terminology ChecklistLATIFNo ratings yet

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

- Module 3Document3 pagesModule 3Kelvin Jay Sebastian SaplaNo ratings yet

- Module 3Document3 pagesModule 3Kelvin Jay Sebastian SaplaNo ratings yet

- Teachers ProfileDocument1 pageTeachers ProfileKelvin Jay Sebastian SaplaNo ratings yet

- Module 2 - OkDocument7 pagesModule 2 - OkKelvin Jay Sebastian Sapla67% (3)

- Most Essential Learning Competency: 1. 2. 3Document3 pagesMost Essential Learning Competency: 1. 2. 3Kelvin Jay Sebastian SaplaNo ratings yet

- Module 3Document4 pagesModule 3Kelvin Jay Sebastian Sapla100% (2)

- Sapla & Arrieta Joint Account: Month AmountDocument1 pageSapla & Arrieta Joint Account: Month AmountKelvin Jay Sebastian SaplaNo ratings yet

- Activity 005Document2 pagesActivity 005Kelvin Jay Sebastian SaplaNo ratings yet

- Lesson 1: The Nature and Forms of Business OrganizationsDocument5 pagesLesson 1: The Nature and Forms of Business OrganizationsKelvin Jay Sebastian SaplaNo ratings yet

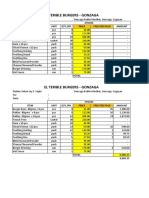

- El Terible Burgers-Gonzaga: Percentage 100.00% 58.87% Net Sales 41.13% 29.35% Net Profit 11.78%Document6 pagesEl Terible Burgers-Gonzaga: Percentage 100.00% 58.87% Net Sales 41.13% 29.35% Net Profit 11.78%Kelvin Jay Sebastian SaplaNo ratings yet

- Bayle Sa Kayle: Note 1 Note 2 Note 3Document3 pagesBayle Sa Kayle: Note 1 Note 2 Note 3Kelvin Jay Sebastian SaplaNo ratings yet

- Ethics Audit and Risk AssessmentsDocument2 pagesEthics Audit and Risk AssessmentsKelvin Jay Sebastian SaplaNo ratings yet

- Quarter 1st Quarter 2nd Quarter 3rd Quarter 90,000.00 4th Quarter 53,333.33Document3 pagesQuarter 1st Quarter 2nd Quarter 3rd Quarter 90,000.00 4th Quarter 53,333.33Kelvin Jay Sebastian SaplaNo ratings yet

- El Terible Burgers - Gonzaga: Stocks Item Unit QTY./PK. Price Free Per Pack AmountDocument4 pagesEl Terible Burgers - Gonzaga: Stocks Item Unit QTY./PK. Price Free Per Pack AmountKelvin Jay Sebastian SaplaNo ratings yet

- Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterDocument3 pagesQuarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterKelvin Jay Sebastian SaplaNo ratings yet

- A. Contrasting Naturopathy With Allopathic Medicine: Prevention vs. CureDocument1 pageA. Contrasting Naturopathy With Allopathic Medicine: Prevention vs. CureKelvin Jay Sebastian SaplaNo ratings yet

- A Reading From The Holy Gospel According To MatthewDocument1 pageA Reading From The Holy Gospel According To MatthewKelvin Jay Sebastian SaplaNo ratings yet

- Application Letter - LuckyDocument1 pageApplication Letter - LuckyKelvin Jay Sebastian Sapla100% (1)

- MADRIAGA, NORALYN - OkDocument3 pagesMADRIAGA, NORALYN - OkKelvin Jay Sebastian SaplaNo ratings yet

- Enidal Mosmera - OKDocument3 pagesEnidal Mosmera - OKKelvin Jay Sebastian SaplaNo ratings yet

- RICA CIELO SANTIAGO - OkDocument3 pagesRICA CIELO SANTIAGO - OkKelvin Jay Sebastian SaplaNo ratings yet

- Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterDocument3 pagesQuarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterKelvin Jay Sebastian SaplaNo ratings yet

- Quarter 1st Quarter 45,000.00 2nd Quarter 48,300.00 3rd Quarter 53,333.33 4th Quarter 57,025.00Document3 pagesQuarter 1st Quarter 45,000.00 2nd Quarter 48,300.00 3rd Quarter 53,333.33 4th Quarter 57,025.00Kelvin Jay Sebastian SaplaNo ratings yet

- Quarter 1st Quarter 60,000.00 2nd Quarter 45,000.00 3rd Quarter 55,000.00 4th Quarter 60,000.00Document3 pagesQuarter 1st Quarter 60,000.00 2nd Quarter 45,000.00 3rd Quarter 55,000.00 4th Quarter 60,000.00Kelvin Jay Sebastian SaplaNo ratings yet

- Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterDocument3 pagesQuarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterKelvin Jay Sebastian SaplaNo ratings yet

- Thelma Saldo - OKDocument3 pagesThelma Saldo - OKKelvin Jay Sebastian SaplaNo ratings yet

- LICUAN, NOLIMAR - OkDocument3 pagesLICUAN, NOLIMAR - OkKelvin Jay Sebastian SaplaNo ratings yet

- TONY PUTDAAN - OkDocument3 pagesTONY PUTDAAN - OkKelvin Jay Sebastian SaplaNo ratings yet

- Frances Leah Sapla - OKDocument3 pagesFrances Leah Sapla - OKKelvin Jay Sebastian SaplaNo ratings yet

- Bimb HoldingsDocument13 pagesBimb HoldingsraihanaNo ratings yet

- Modern Portfolio Theory and Investment Analysis, 9 Edition: Elton, Gruber, Brown, & GoetzmannDocument10 pagesModern Portfolio Theory and Investment Analysis, 9 Edition: Elton, Gruber, Brown, & GoetzmanneniNo ratings yet

- Depreciation and Its AccountingDocument4 pagesDepreciation and Its AccountingSatish SheoranNo ratings yet

- Project Report On Indian Banking SystemDocument21 pagesProject Report On Indian Banking SystemSudesh KalraNo ratings yet

- BGC Client Account - NewDocument9 pagesBGC Client Account - Newsubbu1228No ratings yet

- Ramya Canara Bank Project Final ReportDocument106 pagesRamya Canara Bank Project Final ReportShiva Kumar Mahadevappa79% (14)

- Knowledge ManagementDocument24 pagesKnowledge ManagementNuril GumantoroNo ratings yet

- Breadtalk Group LTD: Singapore Company GuideDocument11 pagesBreadtalk Group LTD: Singapore Company GuideBrandon TanNo ratings yet

- Notes FAR Investment in Associates Equity MethodDocument4 pagesNotes FAR Investment in Associates Equity MethodKerwin Lester MandacNo ratings yet

- Fin MGT - Mock Exams2Document9 pagesFin MGT - Mock Exams2Chloekurtj DelNo ratings yet

- Businesses Supporting Planned Parenthood and AbortionDocument3 pagesBusinesses Supporting Planned Parenthood and AbortionspringsaboNo ratings yet

- On The Mechanics of Economic Development - Robert LucasDocument40 pagesOn The Mechanics of Economic Development - Robert LucasMalandragem dá um tempoNo ratings yet

- Types of Bond PDFDocument2 pagesTypes of Bond PDFjherica baltazarNo ratings yet

- Chapter 12Document34 pagesChapter 12LBL_Lowkee100% (1)

- Ratio Anaylsis With Excel (Hypothetical)Document7 pagesRatio Anaylsis With Excel (Hypothetical)awhan sarangiNo ratings yet

- Investment Banking Course NotesDocument44 pagesInvestment Banking Course NotesPenn CollinsNo ratings yet

- A2 Economics: MicroeconomicsDocument170 pagesA2 Economics: MicroeconomicsHeap Ke XinNo ratings yet

- Chapter: 3 Theory Base of AccountingDocument2 pagesChapter: 3 Theory Base of AccountingJedhbf DndnrnNo ratings yet

- Landacquisition Fasttrack 120918053142 Phpapp02Document191 pagesLandacquisition Fasttrack 120918053142 Phpapp02Naveen Kumar RudhraNo ratings yet

- Financial Statements Decoded (English)Document2 pagesFinancial Statements Decoded (English)ytm2014100% (1)

- Quiz Week 2 SolnsDocument5 pagesQuiz Week 2 SolnsRiri FahraniNo ratings yet

- Problems and Prospects by Suleiman AbdullahiDocument6 pagesProblems and Prospects by Suleiman AbdullahiUmar Bala UmarNo ratings yet

- Working Capital On BEMLDocument103 pagesWorking Capital On BEMLAjay Karthik100% (2)

- Du Pont PresentationDocument20 pagesDu Pont PresentationPreetesh ChoudhariNo ratings yet

- Chapter No.08 The Analysis and Valuation of Bonds - STDocument13 pagesChapter No.08 The Analysis and Valuation of Bonds - STBlue StoneNo ratings yet

- One BookDocument29 pagesOne BookOnebookNo ratings yet