Download as ppt, pdf, or txt

You might also like

- Dyslexia and GiftednessDocument64 pagesDyslexia and GiftednessDrs. Fernette and Brock Eide100% (4)

- Public AdminDocument5 pagesPublic AdminMuhammad Iqbal ZamirNo ratings yet

- Cavalieri, S. Garetti, M. Macchi, M. Pinto, R. - A Decision-Making Framework For Managing Maintenance Spare Parts PDFDocument19 pagesCavalieri, S. Garetti, M. Macchi, M. Pinto, R. - A Decision-Making Framework For Managing Maintenance Spare Parts PDFMauro MLR100% (2)

- Test Bank MGMT 126Document8 pagesTest Bank MGMT 126najihachangminNo ratings yet

- Parreto ChartDocument1 pageParreto ChartGulam Mustafa KhanNo ratings yet

- Detail U (Khoan L 16 TR N 3 Thanh H150) : Martech Boiler EngineeringDocument15 pagesDetail U (Khoan L 16 TR N 3 Thanh H150) : Martech Boiler EngineeringNguyen Anh TuanNo ratings yet

- Grain Size Distribution: Client Mbits Project Name Po1 Project Number Po1Document1 pageGrain Size Distribution: Client Mbits Project Name Po1 Project Number Po1Dileep K NambiarNo ratings yet

- Grain Size Distribution: Client Mbits Project Name P05 Project Number Po5Document1 pageGrain Size Distribution: Client Mbits Project Name P05 Project Number Po5Dileep K NambiarNo ratings yet

- First FloorDocument1 pageFirst Floortadesse felekeNo ratings yet

- SIMPLE SLABE CULVERT 1-ModelDocument1 pageSIMPLE SLABE CULVERT 1-ModelFree fire LoverNo ratings yet

- Grain Size Distribution: Client Mbits Project Name P05 Project Number Po5Document1 pageGrain Size Distribution: Client Mbits Project Name P05 Project Number Po5Dileep K NambiarNo ratings yet

- 1st Year, CSE, B Tech Class Roll NO.-43, SEC-B, University of Engineering & KolkataDocument1 page1st Year, CSE, B Tech Class Roll NO.-43, SEC-B, University of Engineering & KolkataSHIBANANDA SAHOONo ratings yet

- 641 Final Detail of Dranage Spout, RCC Railing & Bearing-Railing 1Document1 page641 Final Detail of Dranage Spout, RCC Railing & Bearing-Railing 1shashi rajhansNo ratings yet

- Field Proven: Southeast Asia Southern OklahomaDocument1 pageField Proven: Southeast Asia Southern OklahomaAquiles CarreraNo ratings yet

- Cotton World Market and Trade Report: Month September 2010Document28 pagesCotton World Market and Trade Report: Month September 2010cottontradeNo ratings yet

- Corpiño ImprimirDocument1 pageCorpiño ImprimirSebastianNo ratings yet

- 28 AgustusDocument1 page28 Agustusans prcNo ratings yet

- Excelente Amante - BassDocument2 pagesExcelente Amante - BassFernando Silva LNo ratings yet

- Pediatric Primary Care 6Th Edition Catherine E Burns Editor All ChapterDocument67 pagesPediatric Primary Care 6Th Edition Catherine E Burns Editor All Chaptermargie.lee200100% (9)

- SBGR pdc-1-sbgr PDC 20200521Document2 pagesSBGR pdc-1-sbgr PDC 20200521Arthur GarciaNo ratings yet

- BaseLink 1Document1 pageBaseLink 1Han NguyenNo ratings yet

- 40.10 CadDocument1 page40.10 Cadfredyraposa2No ratings yet

- IEA Bioenergy Algae Report Update - Final Template 20170131Document16 pagesIEA Bioenergy Algae Report Update - Final Template 20170131Carlos A. VillanuevaNo ratings yet

- Spring Support Exhaust LineDocument1 pageSpring Support Exhaust LinepowerplantunicaneNo ratings yet

- Glide Path ComparisonDocument2 pagesGlide Path ComparisonChrabąszczWacławNo ratings yet

- Que Diga Na - Sol y Lluvia - CelloDocument4 pagesQue Diga Na - Sol y Lluvia - CelloOrquesta InfantilNo ratings yet

- PHFLrev 3Document1 pagePHFLrev 3Rauf MehdiyevNo ratings yet

- 3 No AssaigmentDocument1 page3 No AssaigmentSHIBANANDA SAHOONo ratings yet

- PMXAVD800Document1 pagePMXAVD800nathan.howNo ratings yet

- Detail Siku Landasan: Penutup Atap TrimdecDocument1 pageDetail Siku Landasan: Penutup Atap TrimdecMuhammad FikryNo ratings yet

- BBBBDocument16 pagesBBBBLidetu AbebeNo ratings yet

- Job Sheet 13Document1 pageJob Sheet 13septya hanantaNo ratings yet

- II - Equerre: 1:1 XXX A2Document1 pageII - Equerre: 1:1 XXX A2Ghazali GhazaliNo ratings yet

- Vyvo Vista Plus PDFDocument10 pagesVyvo Vista Plus PDFSteven SengNo ratings yet

- John Deer 2254 Cane Loader Boom-SHT-3Document1 pageJohn Deer 2254 Cane Loader Boom-SHT-3Jordane PretoriusNo ratings yet

- WP 1382Document27 pagesWP 1382quynhhuynh.31211027045No ratings yet

- Technical Guide OS COMEM BR 23 09 2021 INTERATTIVODocument13 pagesTechnical Guide OS COMEM BR 23 09 2021 INTERATTIVOnobitaddlNo ratings yet

- Super Skill Pinball - Cyberhack - FREEDocument1 pageSuper Skill Pinball - Cyberhack - FREEAlfonso CáceresNo ratings yet

- PP 45 X 30Document1 pagePP 45 X 30Alex LimoNo ratings yet

- Cymb IDocument1 pageCymb IDamián Dominguez BautistaNo ratings yet

- KM36+178 MPA-TypicalDocument3 pagesKM36+178 MPA-TypicalAfrizal Dwi PutrantoNo ratings yet

- Pool Fire T-77 GraficaDocument1 pagePool Fire T-77 GraficaManuel SaavedraNo ratings yet

- La Guia MetAs 10 06 Densidad AguaDocument19 pagesLa Guia MetAs 10 06 Densidad AguaMayreneDavilaNo ratings yet

- Niveau S Longrine Type Pou05-S Section 20x25: A-A B-B C-C D-DDocument1 pageNiveau S Longrine Type Pou05-S Section 20x25: A-A B-B C-C D-DAWOUNANGNo ratings yet

- Ultra: Q (US G.P.M.) Q (Imp G.P.M)Document1 pageUltra: Q (US G.P.M.) Q (Imp G.P.M)Jerry Andréi Vigo LinaresNo ratings yet

- Direct Reading1Document2 pagesDirect Reading1joseph chungNo ratings yet

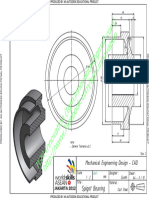

- Machine Design Section-CAE Indian Institute of Technology Chennai Tamil Nadu 600036Document1 pageMachine Design Section-CAE Indian Institute of Technology Chennai Tamil Nadu 600036Deepak K RNo ratings yet

- Diagrama de Molière R134a: RefrigerantesDocument1 pageDiagrama de Molière R134a: RefrigerantesHumnerNo ratings yet

- The Private Sector Financial Balance As A Predictor of Financial CrisesDocument12 pagesThe Private Sector Financial Balance As A Predictor of Financial CrisesIsaac GoldNo ratings yet

- Loading Bar: Title: Pt. Indocitra Widhitama IndustriesDocument1 pageLoading Bar: Title: Pt. Indocitra Widhitama IndustriesArief Sagita WidodoNo ratings yet

- Exalted2 Character Sheet FullNPC v1.0Document2 pagesExalted2 Character Sheet FullNPC v1.0Lenice EscadaNo ratings yet

- Connections CheckDocument83 pagesConnections CheckzewilkNo ratings yet

- WILO Yonos PARA RKA, RS 25-6Document2 pagesWILO Yonos PARA RKA, RS 25-6Mirela Paul100% (1)

- O.5 - Fabry Perot Resonator PDFDocument19 pagesO.5 - Fabry Perot Resonator PDFAlexeiNo ratings yet

- 10 1007@s41742-018Document9 pages10 1007@s41742-018Radouane El-AmriNo ratings yet

- Descripcion Cleaver: Nombre: Puesto: Edad: 0 FECHA: 30-Dec-99 Escolaridad: 0Document4 pagesDescripcion Cleaver: Nombre: Puesto: Edad: 0 FECHA: 30-Dec-99 Escolaridad: 0Isadora BotelloNo ratings yet

- Usps April27meetingDocument18 pagesUsps April27meetingtmurseNo ratings yet

- SDS H F 1, 2016: Warm-UpsDocument6 pagesSDS H F 1, 2016: Warm-UpsDendi YESHWANTHNo ratings yet

- 4823-STC-0001 Platform DETAIL-signedDocument9 pages4823-STC-0001 Platform DETAIL-signedMuhammad Rizky ImaduddinNo ratings yet

- View 4A View 5A: C L Direction of Drive of WB Tunnel CrownDocument3 pagesView 4A View 5A: C L Direction of Drive of WB Tunnel CrownRaymond CiaoNo ratings yet

- Pepsi Mechanical EngineerDocument21 pagesPepsi Mechanical Engineerlennardo LeslieNo ratings yet

- Omdeo Packers and Movers PVT LTDDocument2 pagesOmdeo Packers and Movers PVT LTDShivamNo ratings yet

- Concept Note and AgendaDocument5 pagesConcept Note and AgendaEgyir AggreyNo ratings yet

- Operating Segment: Pfrs 8Document28 pagesOperating Segment: Pfrs 8Giellay OyaoNo ratings yet

- Nucleon, Inc.: June 28th, 2019 - Group 5 - Bishwadeep - Gulshan - Mitali - RaghaviDocument12 pagesNucleon, Inc.: June 28th, 2019 - Group 5 - Bishwadeep - Gulshan - Mitali - RaghaviGulshan DhananiNo ratings yet

- Requirements and Competencies: Assessment of Professional Competence (APC)Document67 pagesRequirements and Competencies: Assessment of Professional Competence (APC)Matthew BulgerNo ratings yet

- What Is EconometricsDocument6 pagesWhat Is Econometricsmirika3shirin50% (2)

- PT Alkindo Naratama TBK Dan Entitas Anak/ and SubsidiariesDocument99 pagesPT Alkindo Naratama TBK Dan Entitas Anak/ and SubsidiariesTiara AprilliaNo ratings yet

- Abebaw Shimelis 2003Document164 pagesAbebaw Shimelis 2003Rafez JoneNo ratings yet

- RBI Issues SARFAESI Act 2002 Guidelines and Directions As Amendment Upto 30th June 2015Document26 pagesRBI Issues SARFAESI Act 2002 Guidelines and Directions As Amendment Upto 30th June 2015Kapil Dev SaggiNo ratings yet

- Indian Financial System Chapter 1Document16 pagesIndian Financial System Chapter 1Rahul GhosaleNo ratings yet

- Remote Working and Work Life BalanceDocument16 pagesRemote Working and Work Life BalanceDwayne DevonishNo ratings yet

- Tybfm Sem 6 Venture Capital Unit II & IIIDocument19 pagesTybfm Sem 6 Venture Capital Unit II & IIIElamathiNo ratings yet

- Business Ethics and Social Responsibility: SeniorDocument67 pagesBusiness Ethics and Social Responsibility: SeniorManny SelmaNo ratings yet

- Quality Management - Ch.9 2Document15 pagesQuality Management - Ch.9 2manarNo ratings yet

- Chapter 3 The Double-Entry System: Discussion QuestionsDocument16 pagesChapter 3 The Double-Entry System: Discussion QuestionskietNo ratings yet

- Glacier Fish AnnouncementDocument2 pagesGlacier Fish AnnouncementDeckbossNo ratings yet

- Chapter 7 Co-BrandingDocument30 pagesChapter 7 Co-BrandingHoNo ratings yet

- VCOSS VICBUDGET UPDATE Web PDFDocument10 pagesVCOSS VICBUDGET UPDATE Web PDFVCOSSNo ratings yet

- SAP Transaction CodesDocument10 pagesSAP Transaction Codesnanduri.aparna161No ratings yet

- Pink - Not Sure But Possible Answer Orange - Wrong Answer Note For Questions With Computations: Your Answer Should Be A Whole Number. Do Not UseDocument26 pagesPink - Not Sure But Possible Answer Orange - Wrong Answer Note For Questions With Computations: Your Answer Should Be A Whole Number. Do Not UseGene Albert LopezNo ratings yet

- ASF - Youth Empowerment Initiative (Poster)Document2 pagesASF - Youth Empowerment Initiative (Poster)Burton MwakilasaNo ratings yet

- HP Blueprint - PsDocument87 pagesHP Blueprint - PsRangabashyam100% (2)

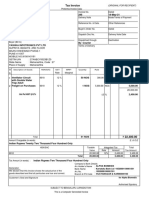

- Tax Invoice: Alpha Biomedix 295 14-May-21Document3 pagesTax Invoice: Alpha Biomedix 295 14-May-21Neha UkaleNo ratings yet

- Idioms BussinesDocument33 pagesIdioms Bussinesmadalinam78No ratings yet

- Profit Maximization1Document14 pagesProfit Maximization1AYA707No ratings yet

- PLO 1a: Our Graduates Will Be Able To Identify The Business Problem in A Given SituationDocument4 pagesPLO 1a: Our Graduates Will Be Able To Identify The Business Problem in A Given SituationMEENA J RCBSNo ratings yet