Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Chapter 2 - Rent Seeking and The Making of An Unequal SocietyDocument6 pagesChapter 2 - Rent Seeking and The Making of An Unequal SocietyShahida67% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 14 Different Types of Garment SamplesDocument5 pages14 Different Types of Garment SamplesSnigdhojit BijonNo ratings yet

- Bytedance Deck PDFDocument47 pagesBytedance Deck PDFJohn AngNo ratings yet

- Corporate Brochure - Rhee BrosDocument15 pagesCorporate Brochure - Rhee BrosMaggie HartonoNo ratings yet

- w8 Wizard Lições 181 e 182Document4 pagesw8 Wizard Lições 181 e 182rafaela popovNo ratings yet

- Jawaban Tugas Bab 3 Dan 4Document4 pagesJawaban Tugas Bab 3 Dan 4Made Ari HandayaniNo ratings yet

- Chapter Six: Cost EstimationDocument25 pagesChapter Six: Cost EstimationMade Ari HandayaniNo ratings yet

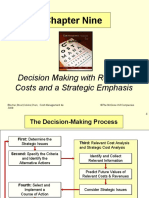

- Chapter Nine: Decision Making With Relevant Costs and A Strategic EmphasisDocument36 pagesChapter Nine: Decision Making With Relevant Costs and A Strategic EmphasisMade Ari HandayaniNo ratings yet

- Chapter Ten: Cost Planning For The Product Life Cycle: Target Costing, Theory of Constraints, and Strategic PricingDocument45 pagesChapter Ten: Cost Planning For The Product Life Cycle: Target Costing, Theory of Constraints, and Strategic PricingMade Ari HandayaniNo ratings yet

- CFM Unlimited (Final)Document26 pagesCFM Unlimited (Final)Jhazzette MirasNo ratings yet

- 1 ACI Philippines, Inc. vs. Coquia - UnlockedDocument14 pages1 ACI Philippines, Inc. vs. Coquia - Unlockedmartin vincentNo ratings yet

- Marketing: EssentialsDocument35 pagesMarketing: EssentialsrianNo ratings yet

- M&A Walmart TakeoverDocument2 pagesM&A Walmart TakeoverPhilip HabersaatNo ratings yet

- Framework For Competitor AnalysisDocument2 pagesFramework For Competitor AnalysisPallabi Pattanayak100% (2)

- Robinhood Users Get To Own Robinhood - BloombergDocument10 pagesRobinhood Users Get To Own Robinhood - BloombergRafael AlejandroNo ratings yet

- Installment Sales and Long Term Construction ContractDocument13 pagesInstallment Sales and Long Term Construction ContractPaupauNo ratings yet

- Assign 2Document2 pagesAssign 2Muhammad Ahsen FahimNo ratings yet

- Zeeta Electricals AND Engineering PVT - LTDDocument75 pagesZeeta Electricals AND Engineering PVT - LTDPiyush PatelNo ratings yet

- CBSE Class 12 English Core Question Paper 2023 Set 1Document42 pagesCBSE Class 12 English Core Question Paper 2023 Set 1tuki100% (1)

- RA 8751 Countervailing LawDocument6 pagesRA 8751 Countervailing LawAgnus SiorNo ratings yet

- Case Study AssignmentDocument3 pagesCase Study AssignmentSalma AlyNo ratings yet

- 71 F. Susandra, I. Gandara Pengambilan Keputusan Keuangan Dengan Pendekatan AnalisisDocument11 pages71 F. Susandra, I. Gandara Pengambilan Keputusan Keuangan Dengan Pendekatan Analisiskristina dewiNo ratings yet

- Introduction To Financial Accounting NotesDocument3 pagesIntroduction To Financial Accounting NotesRaksa HemNo ratings yet

- Zappkode SolutionsDocument10 pagesZappkode SolutionsZappkode SolutionsNo ratings yet

- Operations and Total Quality ManagementDocument49 pagesOperations and Total Quality ManagementBryzan Dela CruzNo ratings yet

- PT. Pelindo 3 SyndicateDocument32 pagesPT. Pelindo 3 Syndicategalihdiadi-1No ratings yet

- Uditi Bhandari - BlogDocument4 pagesUditi Bhandari - BlogUditi BhandariNo ratings yet

- PDF Review Materials For Finals Q - CompressDocument20 pagesPDF Review Materials For Finals Q - CompressAndrea Florence Guy Vidal100% (1)

- CH 03Document48 pagesCH 03kevin echiverriNo ratings yet

- Vehicle Sales Agreement TemplateDocument4 pagesVehicle Sales Agreement TemplateSatya Prakash Trivedi100% (1)

- Contract of Sale of GoodsDocument4 pagesContract of Sale of GoodsVanessa Evans CruzNo ratings yet

- Solution Chapter 11 Afar by Dayag CompressDocument16 pagesSolution Chapter 11 Afar by Dayag Compressholmeshaeley1No ratings yet

- GROUP 5 Chapter 1Document11 pagesGROUP 5 Chapter 1BlueBladeNo ratings yet

- Stock Price (EUR) Exchange RateDocument2 pagesStock Price (EUR) Exchange RateHoàng NhưNo ratings yet