Download as pptx, pdf, or txt

You might also like

- Magic Quadrant For IT Vendor Risk Management ToolsDocument3 pagesMagic Quadrant For IT Vendor Risk Management ToolsJohn RhoNo ratings yet

- Management of Short Term Assets and Liabilities by P.rai87@gmailDocument22 pagesManagement of Short Term Assets and Liabilities by P.rai87@gmailPRAVEEN RAI100% (4)

- Intacc Cash and Cash EquivalentsDocument2 pagesIntacc Cash and Cash EquivalentsKristalen ArmandoNo ratings yet

- Key Fact Document Fixed Deposit EnglishDocument2 pagesKey Fact Document Fixed Deposit EnglishradithsalujaNo ratings yet

- Deposit Accounts: Learning ObjectivesDocument25 pagesDeposit Accounts: Learning ObjectivesSỹ Hoàng TrầnNo ratings yet

- Banking ServicesDocument11 pagesBanking ServicesSwarna GuptaNo ratings yet

- Long-Term Financing: Debts: Financial Management Part IIDocument11 pagesLong-Term Financing: Debts: Financial Management Part IIKisha QuirozNo ratings yet

- Short-Term FinancingDocument15 pagesShort-Term FinancingyukiNo ratings yet

- Concept Map (Garcia, Plata, Villamin) PDFDocument6 pagesConcept Map (Garcia, Plata, Villamin) PDFMinji OhNo ratings yet

- DuPontSupplierFinancingbyCiti CostDocument2 pagesDuPontSupplierFinancingbyCiti Costamr.mans95No ratings yet

- Mod 4 Topic Term DepositsDocument40 pagesMod 4 Topic Term Depositsnarwalshab1997No ratings yet

- Short Term FinancingDocument15 pagesShort Term FinancingJoshua Cabinas100% (1)

- Commercial Bank OperationsDocument2 pagesCommercial Bank OperationsMeilin Denise MEDRANANo ratings yet

- Chapter-4: Sources and Uses of Funds, Performance Evaluation and Bank FailureDocument16 pagesChapter-4: Sources and Uses of Funds, Performance Evaluation and Bank FailureEEL KfWBMZ2.1No ratings yet

- Types of Bank Accounts: Explained in DetailsDocument2 pagesTypes of Bank Accounts: Explained in DetailsRamachandran RamNo ratings yet

- Cash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsDocument30 pagesCash & Cash Equivalent: If The Problem Is Silent, Daily, They Are Part of Cash and Cash EquivalentsKim Audrey JalalainNo ratings yet

- $R069RD5Document18 pages$R069RD5MuhammadFahimNo ratings yet

- Sources Short Term FinanceDocument29 pagesSources Short Term FinanceShruti AshokNo ratings yet

- Damodaran On Cap StructureDocument145 pagesDamodaran On Cap Structuregioro_miNo ratings yet

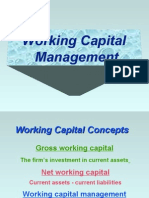

- Working Capital Management: Details in Fixed Income)Document1 pageWorking Capital Management: Details in Fixed Income)Ngân HàNo ratings yet

- Finance PresentationDocument11 pagesFinance PresentationRahul KapurNo ratings yet

- 1.1 Audit of Cash and Cash EquivalentsDocument2 pages1.1 Audit of Cash and Cash EquivalentsANGELU RANE BAGARES INTOLNo ratings yet

- WorkingDocument39 pagesWorkingvishal198900No ratings yet

- FAR 002 Summary Notes - Cash & Proof of CashDocument8 pagesFAR 002 Summary Notes - Cash & Proof of CashMarynelle Labrador SevillaNo ratings yet

- Branch BankingDocument14 pagesBranch BankingMuhammad UmarNo ratings yet

- Intacc ReviewerDocument20 pagesIntacc ReviewerAvos NnNo ratings yet

- Module 5 - Substantive Test of CashDocument6 pagesModule 5 - Substantive Test of CashJesievelle Villafuerte NapaoNo ratings yet

- AE 111 Midterm Formative Assessment 1Document4 pagesAE 111 Midterm Formative Assessment 1Djunah ArellanoNo ratings yet

- Dalay - Sec1 - Act1104 - Cce SummaryDocument3 pagesDalay - Sec1 - Act1104 - Cce SummaryJazmine Arianne DalayNo ratings yet

- BNKG319 Reviewer PDFDocument21 pagesBNKG319 Reviewer PDFjustine hernandezNo ratings yet

- If Silent As To Date of Acquisition, Assume As Current: Cash and Cash Equivalents 1. CashDocument3 pagesIf Silent As To Date of Acquisition, Assume As Current: Cash and Cash Equivalents 1. CashKent Raysil PamaongNo ratings yet

- Unit 12 - BankingDocument92 pagesUnit 12 - BankingNhung Cẩm NguyễnNo ratings yet

- Export and Import FinancingDocument4 pagesExport and Import FinancingTamzid AlifNo ratings yet

- Banking Products and FacilitiesDocument36 pagesBanking Products and FacilitiesMadihah JamianNo ratings yet

- Fixed Deposit Product Disclosure EnglishDocument3 pagesFixed Deposit Product Disclosure EnglishdlndlaminiNo ratings yet

- Cash EquivalentDocument8 pagesCash EquivalentEyra MercadejasNo ratings yet

- Intermediate Accounting NotesDocument7 pagesIntermediate Accounting NotesKyle Angela IlanNo ratings yet

- Pointers To Review: FABM 2: Recording Phase: Answer KeyDocument9 pagesPointers To Review: FABM 2: Recording Phase: Answer KeyMaria Janelle BlanzaNo ratings yet

- Ratio AnalysisDocument30 pagesRatio AnalysisSrujana GantaNo ratings yet

- Sources of FinanceDocument42 pagesSources of Financeravi bhushan100% (2)

- BANKING - Reviewer Module 2.1.1Document5 pagesBANKING - Reviewer Module 2.1.1Arianne JhadeNo ratings yet

- 34 34 Sources of FinanceDocument23 pages34 34 Sources of FinanceShri DongareNo ratings yet

- Arief Taufiqqurrakhman (C1B018115) Cash and Marketable Securities Management and Working Capital and Short-Term Financing PDFDocument6 pagesArief Taufiqqurrakhman (C1B018115) Cash and Marketable Securities Management and Working Capital and Short-Term Financing PDFBikin RelaxNo ratings yet

- W5. Production Factor-Labour, Capital, MachineryDocument9 pagesW5. Production Factor-Labour, Capital, MachineryNor AziraNo ratings yet

- Bank Management LecturesDocument59 pagesBank Management LecturesKushal SharmaNo ratings yet

- PPT2.1-1 Cash and Cash Equivalents (2020)Document42 pagesPPT2.1-1 Cash and Cash Equivalents (2020)Avery Paul MateoNo ratings yet

- 3 Sources of FinanceDocument23 pages3 Sources of FinanceSuryakant FulpagarNo ratings yet

- Sources of Business Finance (Hanith Forman)Document5 pagesSources of Business Finance (Hanith Forman)Hanith Adam FormanNo ratings yet

- CHP 17 - Commercial Bank Sources & Uses of FundsDocument22 pagesCHP 17 - Commercial Bank Sources & Uses of Fundsrashu892No ratings yet

- FinanceDocument7 pagesFinanceFrancine FloresNo ratings yet

- Loan StructuringDocument10 pagesLoan StructuringNhư Hoài ThươngNo ratings yet

- Banking Reviewer - HMPDocument15 pagesBanking Reviewer - HMPjieNo ratings yet

- Cash Management Problrms SolvedDocument42 pagesCash Management Problrms SolvedKarthikNo ratings yet

- NW Import Collection Factsheet PDFDocument2 pagesNW Import Collection Factsheet PDFWill LumNo ratings yet

- Business FinanceDocument20 pagesBusiness Financegracella oktaviaNo ratings yet

- Cash and Cash EquivalentsDocument5 pagesCash and Cash EquivalentsseunjeincraftNo ratings yet

- 1.2 Cash and Cash EquivalentDocument3 pages1.2 Cash and Cash EquivalentThalia Angela HipeNo ratings yet

- Credit FinalsDocument4 pagesCredit FinalsJane Alyssa SevillaNo ratings yet

- Types of Accounts, Bank Guarantee, LC, Line of CreditDocument44 pagesTypes of Accounts, Bank Guarantee, LC, Line of Creditkaren sunilNo ratings yet

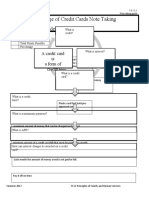

- Tak e Charge of Credit Cards Note Taking Guide: A Credit Card Is A Form of Credit!Document3 pagesTak e Charge of Credit Cards Note Taking Guide: A Credit Card Is A Form of Credit!jackson WNo ratings yet

- Evaluating Your Email MarketingDocument2 pagesEvaluating Your Email MarketingIdham MuqoddasNo ratings yet

- Intro Letter SmartCal ServiceDocument5 pagesIntro Letter SmartCal ServiceNdra PompomorinNo ratings yet

- Negotiation Skills-Chapter 3: Prof. Ouijdane Iddoub 2018-2019Document12 pagesNegotiation Skills-Chapter 3: Prof. Ouijdane Iddoub 2018-2019Yassine MerizakNo ratings yet

- R2301F PDF ENG CompressedDocument18 pagesR2301F PDF ENG CompressedMarioAbuyeresNo ratings yet

- Business Differences in Developing CountriesDocument2 pagesBusiness Differences in Developing CountriesSevinc SalmanovaNo ratings yet

- OverviewDocument6 pagesOverviewDia rielNo ratings yet

- Demographic Factors, Personality and Entrepreneurial InclinationDocument18 pagesDemographic Factors, Personality and Entrepreneurial InclinationKwadwo Owusu MainooNo ratings yet

- Dawlance Final PresentationDocument40 pagesDawlance Final PresentationTalha AamirNo ratings yet

- ImgDocument2 pagesImgIR SyamNo ratings yet

- Blue & Yellow Professional Future Technology PresentationDocument11 pagesBlue & Yellow Professional Future Technology PresentationJoaquin PalominoNo ratings yet

- Skin Feedback: General Cost and Benefit OverviewDocument6 pagesSkin Feedback: General Cost and Benefit OverviewVictor RamirezNo ratings yet

- Bahagian A Mengandungi LIMA Soalan. Jawab SEMUA.: BBAW2103 (SAMPLE 1)Document6 pagesBahagian A Mengandungi LIMA Soalan. Jawab SEMUA.: BBAW2103 (SAMPLE 1)Faidz FuadNo ratings yet

- (PDF) Strategy and Organisation at Singapore Airlines - Achieving Sustainable Advantage Through Dual StrategyDocument6 pages(PDF) Strategy and Organisation at Singapore Airlines - Achieving Sustainable Advantage Through Dual Strategyishkol39No ratings yet

- Business Consulting Services: Comprehensive Practice Management Solutions For Independent Investment AdvisorsDocument12 pagesBusiness Consulting Services: Comprehensive Practice Management Solutions For Independent Investment AdvisorsPaaforiNo ratings yet

- Acc 111 Exam GeleraDocument11 pagesAcc 111 Exam GeleraCheska GeleraNo ratings yet

- MC Report Group A1Document31 pagesMC Report Group A1SAURAV KUMAR GUPTANo ratings yet

- STP StrategyDocument3 pagesSTP StrategyEly Francis BrosolaNo ratings yet

- Course Code: Acfn2102: Financial Management-IDocument45 pagesCourse Code: Acfn2102: Financial Management-Itemesgen yohannesNo ratings yet

- "Credit Appraisal For Working Capital Finance To Small and Medium Enterprises at State Bank of IDocument93 pages"Credit Appraisal For Working Capital Finance To Small and Medium Enterprises at State Bank of Iverma_sk289% (9)

- Marek Answering Concerns That Revenue in Poland Is Not Being Brought To Nigeria (Recovered) (Recovered) (Recovered) PDFDocument5 pagesMarek Answering Concerns That Revenue in Poland Is Not Being Brought To Nigeria (Recovered) (Recovered) (Recovered) PDFDavid HundeyinNo ratings yet

- Uma Maheswari - ITAT ChennaiDocument6 pagesUma Maheswari - ITAT ChennaiLakshmivenkataraman T.SNo ratings yet

- Technology Social Venture A New Genr of So 2012 Procedia Social and BehavDocument6 pagesTechnology Social Venture A New Genr of So 2012 Procedia Social and BehavMadhura AbhyankarNo ratings yet

- Charter UpdatedDocument2 pagesCharter UpdatedAnubhav OjhaNo ratings yet

- Program GovernanceDocument213 pagesProgram GovernanceUsman A. KalamNo ratings yet

- Global Fop BrochureDocument18 pagesGlobal Fop BrochureYelena KogushiNo ratings yet

- BP-080 Future Process Model OM V1.0Document43 pagesBP-080 Future Process Model OM V1.0UdhayanNo ratings yet

- What Is ASES PDFDocument7 pagesWhat Is ASES PDFmvelsky100% (3)

- GREEN Chemicals®Co. Commercial Proposal - PT Integra Oilfield Services (3.august.2023)Document6 pagesGREEN Chemicals®Co. Commercial Proposal - PT Integra Oilfield Services (3.august.2023)Ricky WibowoNo ratings yet

- Workshop 8 SolutionsDocument8 pagesWorkshop 8 SolutionsAssessment Help SolutionsNo ratings yet