Download as ppt, pdf, or txt

You might also like

- Internship Report: Organizational Study at Tvs-Electronics ChennaiDocument44 pagesInternship Report: Organizational Study at Tvs-Electronics Chennaishjaya14% (7)

- The Internal Assessment: Strategic Management Concepts & CasesDocument41 pagesThe Internal Assessment: Strategic Management Concepts & CasesusamaNo ratings yet

- The Internal Assessment: Strategic Management: Concepts & Cases 11 Edition Fred DavidDocument89 pagesThe Internal Assessment: Strategic Management: Concepts & Cases 11 Edition Fred DavidFAYA AUGUSTIAN ARIESTYARININo ratings yet

- Implementing Strategies: Management Issues: Strategic Management Concepts & CasesDocument25 pagesImplementing Strategies: Management Issues: Strategic Management Concepts & CasesALI SHER HaidriNo ratings yet

- Implementing Strategies-Management IssuesDocument27 pagesImplementing Strategies-Management IssuesTelvin GwengweNo ratings yet

- The Internal Assessment: Strategic Management: Concepts & Cases 10 Edition Fred DavidDocument88 pagesThe Internal Assessment: Strategic Management: Concepts & Cases 10 Edition Fred DavidAnggun WidyaNo ratings yet

- The Internal Assessment: Strategic Management: Concepts & Cases 13 Edition Fred DavidDocument30 pagesThe Internal Assessment: Strategic Management: Concepts & Cases 13 Edition Fred DavidteguhisNo ratings yet

- Nature of Strategic ManagementDocument49 pagesNature of Strategic ManagementAneesa BhattiNo ratings yet

- Management Strategies Management StrategiesDocument39 pagesManagement Strategies Management StrategiesTrihandoyo Budi CahyantoNo ratings yet

- The Nature of Strategic ManagementDocument42 pagesThe Nature of Strategic ManagementPratipal SinghNo ratings yet

- The Internal AssessmentDocument70 pagesThe Internal AssessmentavvNo ratings yet

- Nature of Strategic ManagementDocument31 pagesNature of Strategic ManagementAli UsmanNo ratings yet

- CH 4 Audit Internal RRSDocument30 pagesCH 4 Audit Internal RRSadindariskianimsNo ratings yet

- Strategic Management: Concepts and CasesDocument56 pagesStrategic Management: Concepts and Casesمحمود احمدNo ratings yet

- David ch1 RevisedDocument16 pagesDavid ch1 RevisedAsif ZoniNo ratings yet

- Ebert ch05 InstruDocument28 pagesEbert ch05 InstruKristian SuhartadiNo ratings yet

- Topic 1 Intro To Strat MGT - COMPILEDDocument22 pagesTopic 1 Intro To Strat MGT - COMPILEDShekinah CruzNo ratings yet

- Chap 1Document59 pagesChap 1SanaNo ratings yet

- David PPT Abbrev Ch01-1aDocument17 pagesDavid PPT Abbrev Ch01-1aSalman SeadNo ratings yet

- Chapter4 Internal AssessmentDocument45 pagesChapter4 Internal Assessmentinnocent angelNo ratings yet

- Chapter 4 Strategic ManagementDocument61 pagesChapter 4 Strategic ManagementHafsa KhanNo ratings yet

- UNIT I - Startegic ManagementDocument58 pagesUNIT I - Startegic Managementshaifali pandeyNo ratings yet

- Fast Food Organizational StructureDocument33 pagesFast Food Organizational StructureSaid Al Jaafari0% (1)

- SM Ch1Document65 pagesSM Ch1CancelynshrnpNo ratings yet

- CH 1 Nature of StramanDocument17 pagesCH 1 Nature of StramanSadAccountantNo ratings yet

- The Nature of Strategic ManagementDocument17 pagesThe Nature of Strategic ManagementRose MagsinoNo ratings yet

- 1.Ch 9-Performance Management AppraisalDocument31 pages1.Ch 9-Performance Management AppraisalHassaan Bin KhalidNo ratings yet

- Chapter 1 - The Nature of Strategic ManagementDocument45 pagesChapter 1 - The Nature of Strategic ManagementRRTNo ratings yet

- Implementing Strategies: Management & Operations Issues: Strategic Management: Concepts & Cases 13 Edition Fred DavidDocument23 pagesImplementing Strategies: Management & Operations Issues: Strategic Management: Concepts & Cases 13 Edition Fred DavidAslam PervaizNo ratings yet

- Why Strategic Planning Is Important To All ManagersDocument23 pagesWhy Strategic Planning Is Important To All ManagersShopify SEONo ratings yet

- Internal Audit by Fred DavidDocument67 pagesInternal Audit by Fred DavidTJ ZamoraNo ratings yet

- The Internal Assessment: Strategic Management Concepts & CasesDocument67 pagesThe Internal Assessment: Strategic Management Concepts & CasesNissar BadharudheenNo ratings yet

- Managing For Business SuccessDocument44 pagesManaging For Business SuccessTruong NguyenNo ratings yet

- Implementing Strategies: Management & Operations Issues: Strategic Management: Concepts & Cases 13 Edition Fred DavidDocument23 pagesImplementing Strategies: Management & Operations Issues: Strategic Management: Concepts & Cases 13 Edition Fred Davidmiftakhul jannahNo ratings yet

- ch4 PDFDocument59 pagesch4 PDFwaheeba84No ratings yet

- The Internal Assessment: Strategic Management Concepts & CasesDocument33 pagesThe Internal Assessment: Strategic Management Concepts & CasesALI SHER HaidriNo ratings yet

- Lecture 7 Implementation of StrategiesDocument18 pagesLecture 7 Implementation of Strategiesnatasha carmichaelNo ratings yet

- Analisis Lingkungan Internal Pertemuan 9: Matakuliah: J0134/ Manajemen Strategik Tahun: 2006Document20 pagesAnalisis Lingkungan Internal Pertemuan 9: Matakuliah: J0134/ Manajemen Strategik Tahun: 2006Bursa KerjaNo ratings yet

- Business Essentials Business EssentialsDocument29 pagesBusiness Essentials Business EssentialsFadhila Bondan SukmawatiNo ratings yet

- Chapter Seven Implementing Strategies Management and Operation IssueDocument23 pagesChapter Seven Implementing Strategies Management and Operation IssueAbdifatah AbdilahiNo ratings yet

- Stratma Topic 7-MergedDocument86 pagesStratma Topic 7-Mergedmisonim.eNo ratings yet

- Chap 09Document38 pagesChap 09Asif ZoniNo ratings yet

- The Internal AssessmentDocument67 pagesThe Internal AssessmentAbdullah ButtNo ratings yet

- HR ScorecardDocument40 pagesHR ScorecardDhairya MehtaNo ratings yet

- Analisis Beban Kerja-FTEDocument84 pagesAnalisis Beban Kerja-FTEDestri DianaNo ratings yet

- Barney SMCA4 08Document17 pagesBarney SMCA4 08taghavi1347No ratings yet

- The Internal Assessment: Strategic Management: Concepts & Cases 17 Edition Global Edition Fred DavidDocument42 pagesThe Internal Assessment: Strategic Management: Concepts & Cases 17 Edition Global Edition Fred DavidIm NayeonNo ratings yet

- Strategic Management: Concepts and Cases: Arab World EditionDocument64 pagesStrategic Management: Concepts and Cases: Arab World Editionwaheeba84No ratings yet

- Chapter 3Document53 pagesChapter 3MOSTAKIN ROYNo ratings yet

- Chapter 08Document50 pagesChapter 08raziabuhakmeh781No ratings yet

- Performance Management and Appraisal: Part Three - Training and DevelopmentDocument50 pagesPerformance Management and Appraisal: Part Three - Training and Developmentarmaan malikNo ratings yet

- Slides Business ModelsDocument26 pagesSlides Business ModelsFrank StandaertNo ratings yet

- Implementation Plan For Strategic HR Business Partner FunctionDocument24 pagesImplementation Plan For Strategic HR Business Partner FunctionuhrNo ratings yet

- Workload AnalysisDocument85 pagesWorkload AnalysisEsthi FebrianiNo ratings yet

- BahasaDocument61 pagesBahasaOnyxas HillepNo ratings yet

- SM MBA-BK 2021 (s4)Document51 pagesSM MBA-BK 2021 (s4)Dang DangNo ratings yet

- HR DashboardDocument39 pagesHR DashboardMD Ahiduzzaman100% (3)

- Compensation Management - PPT DownloadDocument28 pagesCompensation Management - PPT DownloadJerome Formalejo,No ratings yet

- 6A Strategy Analysis and ChoiceDocument22 pages6A Strategy Analysis and ChoiceALI SHER HaidriNo ratings yet

- DavidDocument17 pagesDavidFiera ChueraNo ratings yet

- University of Agriculture Faisalabad: Food Product AdvertisementDocument4 pagesUniversity of Agriculture Faisalabad: Food Product AdvertisementALI SHER HaidriNo ratings yet

- English Lecturer Test 2Document7 pagesEnglish Lecturer Test 2ALI SHER HaidriNo ratings yet

- English Lectuerer Test 8Document7 pagesEnglish Lectuerer Test 8ALI SHER HaidriNo ratings yet

- Answer Key English Lectuerer Test 4Document7 pagesAnswer Key English Lectuerer Test 4ALI SHER Haidri100% (1)

- Audit EvDocument2 pagesAudit EvDhierissa LeeNo ratings yet

- EI - 2010 - High Level Framework PSMDocument43 pagesEI - 2010 - High Level Framework PSMMaxNo ratings yet

- Governance Risk ControlDocument8 pagesGovernance Risk ControlAwneeshNo ratings yet

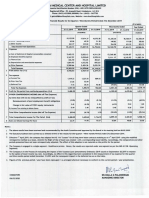

- Kovai Medical Center and Hospital Limited: PartlcularsDocument2 pagesKovai Medical Center and Hospital Limited: PartlcularsVickyNo ratings yet

- Pinky Final Internship ReportDocument49 pagesPinky Final Internship Reportsonudinesh2003No ratings yet

- Resume ContohDocument3 pagesResume Contohmuhammad_marzuki_8No ratings yet

- Cost Auditor Professional Ethics and ResponsibilitiesDocument14 pagesCost Auditor Professional Ethics and ResponsibilitiesAbhijith ViratNo ratings yet

- Principles of Auditing and Other Assurance Services 21st Edition Whittington Test BankDocument24 pagesPrinciples of Auditing and Other Assurance Services 21st Edition Whittington Test Bankraftbungofqy6100% (32)

- AGCUB - Audit Policy-2021Document15 pagesAGCUB - Audit Policy-2021rassouakNo ratings yet

- GPS Process Stakeholder Interfaces 202211 1Document19 pagesGPS Process Stakeholder Interfaces 202211 1SeidlNo ratings yet

- RFP - Pkg-II & III Chhattisgarh (PBMC) Final ModeDocument233 pagesRFP - Pkg-II & III Chhattisgarh (PBMC) Final Modenaman naharNo ratings yet

- 173335Document148 pages173335Taskeen AliNo ratings yet

- Mahindra Sustainability Report 2015 16Document137 pagesMahindra Sustainability Report 2015 16Shivam GoyalNo ratings yet

- Audit of Ultratech Cement LimitedDocument43 pagesAudit of Ultratech Cement Limitedpallavi21_1992No ratings yet

- NABSAMRUDDHI Annual Report 21-22 FinalDocument112 pagesNABSAMRUDDHI Annual Report 21-22 FinalSumit Kumar GuptaNo ratings yet

- Responsibilities and Functions of Internal EmployeesDocument2 pagesResponsibilities and Functions of Internal EmployeesJeremie LoyolaNo ratings yet

- AI Gains Momentum in Core Financial Services Functions 1691763089Document9 pagesAI Gains Momentum in Core Financial Services Functions 1691763089Vinod GhorpadeNo ratings yet

- Change Management PlanDocument44 pagesChange Management Plancostas_jacovides13470% (1)

- ISO IEC TS 17021-10 2018 (Inglés)Document16 pagesISO IEC TS 17021-10 2018 (Inglés)Jose Luis Sanchez SotresNo ratings yet

- Galvin Report Pt4Document18 pagesGalvin Report Pt4MunnkeymannNo ratings yet

- Code of EthicsDocument54 pagesCode of EthicsPeter BanjaoNo ratings yet

- Yegi Prasad: Experience SummaryDocument3 pagesYegi Prasad: Experience SummaryRohit SrivastavaNo ratings yet

- 6.3 Internal Check, Internal Control, Internal AuditDocument37 pages6.3 Internal Check, Internal Control, Internal AuditDhana SekarNo ratings yet

- Risk Based Audit - ISA 320 MaterialityDocument14 pagesRisk Based Audit - ISA 320 MaterialityFachrurroziNo ratings yet

- Atoha PMPPRO S6 - QualityDocument38 pagesAtoha PMPPRO S6 - QualityHai LeNo ratings yet

- CMMI ArtifactDocument2 pagesCMMI ArtifactsivaniranjanNo ratings yet

- Ca Niranjan JoshiDocument96 pagesCa Niranjan JoshiharshalpNo ratings yet

- CISA Practice Questions To Prep For The ExamDocument14 pagesCISA Practice Questions To Prep For The ExamAntar ShaddadNo ratings yet

- MSD57331Document48 pagesMSD57331aaravswastikNo ratings yet