Chapter 1: Accounting in Action

Chapter 1: Accounting in Action

You might also like

- Assessment - 1: Student Name: Arth Patel Student Id: UEDT505Document12 pagesAssessment - 1: Student Name: Arth Patel Student Id: UEDT505Fayyaz HussainNo ratings yet

- Module 1 - Recording Business TransactionDocument11 pagesModule 1 - Recording Business Transactionem fabi100% (1)

- Company Outsiders: Resources TodayDocument20 pagesCompany Outsiders: Resources TodaySarbani Mishra0% (1)

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionMohammed Merajul IslamNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionFarhan TariqNo ratings yet

- Chapter-3: Adjusting The AccountsDocument30 pagesChapter-3: Adjusting The Accountssadif sayeedNo ratings yet

- Chapter-3: Adjusting The AccountsDocument30 pagesChapter-3: Adjusting The AccountsMohammed Merajul IslamNo ratings yet

- Chapter 11Document32 pagesChapter 11Mohammed Merajul IslamNo ratings yet

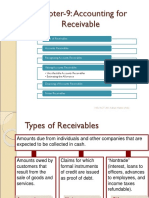

- Chapter-9: Accounting For Receivable: Types of ReceivablesDocument24 pagesChapter-9: Accounting For Receivable: Types of ReceivablesMohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For ReceivableDocument24 pagesChapter-9: Accounting For ReceivableArif HossainNo ratings yet

- The Account Steps in The Recording Process The Trial BalanceDocument17 pagesThe Account Steps in The Recording Process The Trial BalanceMohammed Merajul IslamNo ratings yet

- ACT201 Chap001 NBNDocument18 pagesACT201 Chap001 NBNAudity PaulNo ratings yet

- Understanding Financial Statements, Taxes, and Cash Flows Ch. 3 - Evaluating A Firm's Financial PerformanceDocument53 pagesUnderstanding Financial Statements, Taxes, and Cash Flows Ch. 3 - Evaluating A Firm's Financial PerformanceDhinar Ardhy SutrisnoNo ratings yet

- Chapter-5: Accounting For Merchandising OperationsDocument36 pagesChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamNo ratings yet

- Accounting in ActionDocument42 pagesAccounting in ActionMuhammad TausiqueNo ratings yet

- REVISION PaDocument54 pagesREVISION PaNgoc Nguyen ThanhNo ratings yet

- Fundamentals of Finance: Ignacio Lezaun English Edition 2021Document22 pagesFundamentals of Finance: Ignacio Lezaun English Edition 2021Elias Macher CarpenaNo ratings yet

- Topic 1 2Document16 pagesTopic 1 2lala lianNo ratings yet

- L2 - Accounting Equation & Transaction Analysis - Edited With AnsswerDocument39 pagesL2 - Accounting Equation & Transaction Analysis - Edited With AnsswerEslam SamyNo ratings yet

- Accounting 1-4Document37 pagesAccounting 1-4Abed M. SallamNo ratings yet

- Chap 2 Basic Acctg EquationDocument28 pagesChap 2 Basic Acctg Equationellamangapis2003No ratings yet

- Lesson 01Document5 pagesLesson 01mahrashmentNo ratings yet

- Accounting Chapter 1 Sec 8,9,10 UpdatedDocument36 pagesAccounting Chapter 1 Sec 8,9,10 Updatedrashedkhan1722No ratings yet

- Accounting 1Document25 pagesAccounting 1Afsarul HaqueNo ratings yet

- Accounting Equations PaDocument24 pagesAccounting Equations PaAisyah Ayu SaputriNo ratings yet

- Persamaan Akuntansi (Kieso Modified)Document24 pagesPersamaan Akuntansi (Kieso Modified)Hervin DiahNo ratings yet

- 1&2 Meaning and Definition of AccountingDocument73 pages1&2 Meaning and Definition of AccountingPrasad BhanageNo ratings yet

- Financial Accounting & Analysis PDFDocument6 pagesFinancial Accounting & Analysis PDFGorakhpuria MNo ratings yet

- Lecture Slides - Chapter 1 & 2Document66 pagesLecture Slides - Chapter 1 & 2Phan Đỗ QuỳnhNo ratings yet

- 7 Financial ManagementDocument46 pages7 Financial ManagementJames OwusuNo ratings yet

- Lecture Slides - Chapter 1 2Document66 pagesLecture Slides - Chapter 1 2Van Dat100% (1)

- Ch.2 - Recording Business Transactions (Pearson 6th Edition) - MHDocument56 pagesCh.2 - Recording Business Transactions (Pearson 6th Edition) - MHSamZhao100% (1)

- What Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingDocument41 pagesWhat Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingMd. Haseeb KhanNo ratings yet

- GGGGDocument12 pagesGGGGSami BoyNo ratings yet

- Chapter 12 Review Updated 11th EdDocument13 pagesChapter 12 Review Updated 11th Edangelsalvador05082006No ratings yet

- Accounting Tutorials Day 1Document8 pagesAccounting Tutorials Day 1Richboy Jude VillenaNo ratings yet

- Clase 14 ITAM Financial Statements & Models Otoño 2017Document25 pagesClase 14 ITAM Financial Statements & Models Otoño 2017Gabriel Ruiz HerreraNo ratings yet

- Accounting Notes FinallyDocument72 pagesAccounting Notes FinallyHaaris UsmanNo ratings yet

- Lec 1& 2Document37 pagesLec 1& 2Museera IffatNo ratings yet

- BBAW2103 - Tutorial 1Document69 pagesBBAW2103 - Tutorial 1M THREE THOUSAND RESOURCESNo ratings yet

- ch07 STDocument31 pagesch07 STquangle.31221025758No ratings yet

- Revision 2017 PDFDocument72 pagesRevision 2017 PDFKUUNDJUAUNENo ratings yet

- Chapter 1 of Principles of AccountingDocument49 pagesChapter 1 of Principles of AccountingNhật LinhNo ratings yet

- The Accounting EquationDocument11 pagesThe Accounting EquationMIA DEITANo ratings yet

- Intro To Financial Accounting Chapter 1Document41 pagesIntro To Financial Accounting Chapter 1hermitpassiNo ratings yet

- Power Point Presentation 2Document39 pagesPower Point Presentation 2268gunnaNo ratings yet

- Module I: Basics of Credit and Credit Process: Chapter 4: Cash Flow Statement AnalysisDocument26 pagesModule I: Basics of Credit and Credit Process: Chapter 4: Cash Flow Statement Analysissagar7No ratings yet

- IGCSE Revision-2024.Document72 pagesIGCSE Revision-2024.TaNo ratings yet

- 1) Week 2 Slides - Statement of Financial PositionDocument56 pages1) Week 2 Slides - Statement of Financial PositionTaimoor BaigNo ratings yet

- Lecture Slides - Chapter 1 2Document69 pagesLecture Slides - Chapter 1 2Nhi BuiNo ratings yet

- Principles of Accounting: Weygandt Kieso KimmelDocument38 pagesPrinciples of Accounting: Weygandt Kieso KimmelAfsar AhmedNo ratings yet

- CH 01Document54 pagesCH 01Ngân Hà ĐỗNo ratings yet

- Exercises Set B 1 Exercises Set B CompressDocument7 pagesExercises Set B 1 Exercises Set B CompressHoèn Hoèn100% (1)

- Chapter 1 - Acctg NotesDocument6 pagesChapter 1 - Acctg Notesfennyl婷.No ratings yet

- 1.1 - Accounting in ActionDocument12 pages1.1 - Accounting in ActionarjunaidbdNo ratings yet

- Chapter 12 ReviewDocument14 pagesChapter 12 ReviewDonna Mae HernandezNo ratings yet

- 001.CB Lecture FundamentalsDocument28 pages001.CB Lecture FundamentalskunyangNo ratings yet

- Accounting 1Document59 pagesAccounting 1Teodora IrimiaNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Financial ManagementDocument4 pagesFinancial Managementkiran gaikwad0% (1)

- Application Form - PLO AMP - County Reps and AmbassadorsDocument6 pagesApplication Form - PLO AMP - County Reps and AmbassadorsLazarus Kadett Ndivayele100% (1)

- Registration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Document2 pagesRegistration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Sunlight FoundationNo ratings yet

- Macke vs. Camps G.R. No. 2962Document2 pagesMacke vs. Camps G.R. No. 2962Maria Fiona Duran MerquitaNo ratings yet

- Barut Vs CabacunganDocument7 pagesBarut Vs CabacunganCharm Divina LascotaNo ratings yet

- (Ebook PDF) (Ebook PDF) Advanced Accounting, Global Edition 11th Edition All ChapterDocument43 pages(Ebook PDF) (Ebook PDF) Advanced Accounting, Global Edition 11th Edition All Chaptergryansafiul100% (9)

- Gandhi and National MovementDocument30 pagesGandhi and National MovementArun kumar SethiNo ratings yet

- StatCon Compilation of Cases Part 1Document21 pagesStatCon Compilation of Cases Part 1Angel Agustine O. Japitan IINo ratings yet

- Heirs of ClaudelDocument5 pagesHeirs of ClaudelZyldjyh C. Pactol-Portuguez100% (1)

- Indian BankDocument381 pagesIndian BankganeshNo ratings yet

- A60 - 780 - 3 - C4-Pressure Relief Valve Instrument Data Sheet & PDFDocument109 pagesA60 - 780 - 3 - C4-Pressure Relief Valve Instrument Data Sheet & PDFSoumiyaNo ratings yet

- Consequentialism EssayDocument15 pagesConsequentialism EssayKatya RobinsonNo ratings yet

- RA No. 8762 Retail Trade Liberalization Act of 2000Document5 pagesRA No. 8762 Retail Trade Liberalization Act of 2000SZNo ratings yet

- New Stockiest Appointment Check ListDocument18 pagesNew Stockiest Appointment Check ListRamana GNo ratings yet

- Erin Cullaro Response To Notary ComplaintDocument8 pagesErin Cullaro Response To Notary ComplaintForeclosure Fraud100% (1)

- Tafseer Mariful Quran Sura 109 Al Kafirun English Translation PDFDocument6 pagesTafseer Mariful Quran Sura 109 Al Kafirun English Translation PDFamaanking8bpNo ratings yet

- Justice: What's The Right Thing To Do? Episode 01 "The Moral Side of Murder"Document31 pagesJustice: What's The Right Thing To Do? Episode 01 "The Moral Side of Murder"asdasdasNo ratings yet

- Assignment - Natural JusticeDocument6 pagesAssignment - Natural JusticeYash SinghNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Income TAX Chapter 13 ReviewerDocument31 pagesIncome TAX Chapter 13 ReviewerEryn GabrielleNo ratings yet

- Zayed Sustainability PrizeDocument7 pagesZayed Sustainability PrizeKenneth BlessingNo ratings yet

- Detailed Computation ITR-1 2012-13Document2 pagesDetailed Computation ITR-1 2012-13georgenehaNo ratings yet

- Đề thi HP Ngân hàng thương mại1 E - LMS - 22.11.2021Document1 pageĐề thi HP Ngân hàng thương mại1 E - LMS - 22.11.2021Quynh NguyenNo ratings yet

- Thayer US-Burma Policy ChangeDocument2 pagesThayer US-Burma Policy ChangeCarlyle Alan ThayerNo ratings yet

- Court DateDocument1 pageCourt DateThe Daily DotNo ratings yet

- Rutgers Newark Course Schedule Spring 2018Document2 pagesRutgers Newark Course Schedule Spring 2018abdulrehman786No ratings yet

- Exam Cheat SheetDocument2 pagesExam Cheat SheetJustin BrownNo ratings yet

- Class 6 Olympiad: Choose Correct Answer(s) From The Given ChoicesDocument3 pagesClass 6 Olympiad: Choose Correct Answer(s) From The Given ChoicesRUPANo ratings yet

- Jeff Pippenger - Seven Times in LeviticusDocument16 pagesJeff Pippenger - Seven Times in LeviticusKelly K.R. RossNo ratings yet

- Big Tech InjunctionDocument155 pagesBig Tech InjunctionWashington ExaminerNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Assessment - 1: Student Name: Arth Patel Student Id: UEDT505Document12 pagesAssessment - 1: Student Name: Arth Patel Student Id: UEDT505Fayyaz HussainNo ratings yet

- Module 1 - Recording Business TransactionDocument11 pagesModule 1 - Recording Business Transactionem fabi100% (1)

- Company Outsiders: Resources TodayDocument20 pagesCompany Outsiders: Resources TodaySarbani Mishra0% (1)

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionMohammed Merajul IslamNo ratings yet

- Chapter 1: Accounting in ActionDocument31 pagesChapter 1: Accounting in ActionFarhan TariqNo ratings yet

- Chapter-3: Adjusting The AccountsDocument30 pagesChapter-3: Adjusting The Accountssadif sayeedNo ratings yet

- Chapter-3: Adjusting The AccountsDocument30 pagesChapter-3: Adjusting The AccountsMohammed Merajul IslamNo ratings yet

- Chapter 11Document32 pagesChapter 11Mohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For Receivable: Types of ReceivablesDocument24 pagesChapter-9: Accounting For Receivable: Types of ReceivablesMohammed Merajul IslamNo ratings yet

- Chapter-9: Accounting For ReceivableDocument24 pagesChapter-9: Accounting For ReceivableArif HossainNo ratings yet

- The Account Steps in The Recording Process The Trial BalanceDocument17 pagesThe Account Steps in The Recording Process The Trial BalanceMohammed Merajul IslamNo ratings yet

- ACT201 Chap001 NBNDocument18 pagesACT201 Chap001 NBNAudity PaulNo ratings yet

- Understanding Financial Statements, Taxes, and Cash Flows Ch. 3 - Evaluating A Firm's Financial PerformanceDocument53 pagesUnderstanding Financial Statements, Taxes, and Cash Flows Ch. 3 - Evaluating A Firm's Financial PerformanceDhinar Ardhy SutrisnoNo ratings yet

- Chapter-5: Accounting For Merchandising OperationsDocument36 pagesChapter-5: Accounting For Merchandising OperationsMohammed Merajul IslamNo ratings yet

- Accounting in ActionDocument42 pagesAccounting in ActionMuhammad TausiqueNo ratings yet

- REVISION PaDocument54 pagesREVISION PaNgoc Nguyen ThanhNo ratings yet

- Fundamentals of Finance: Ignacio Lezaun English Edition 2021Document22 pagesFundamentals of Finance: Ignacio Lezaun English Edition 2021Elias Macher CarpenaNo ratings yet

- Topic 1 2Document16 pagesTopic 1 2lala lianNo ratings yet

- L2 - Accounting Equation & Transaction Analysis - Edited With AnsswerDocument39 pagesL2 - Accounting Equation & Transaction Analysis - Edited With AnsswerEslam SamyNo ratings yet

- Accounting 1-4Document37 pagesAccounting 1-4Abed M. SallamNo ratings yet

- Chap 2 Basic Acctg EquationDocument28 pagesChap 2 Basic Acctg Equationellamangapis2003No ratings yet

- Lesson 01Document5 pagesLesson 01mahrashmentNo ratings yet

- Accounting Chapter 1 Sec 8,9,10 UpdatedDocument36 pagesAccounting Chapter 1 Sec 8,9,10 Updatedrashedkhan1722No ratings yet

- Accounting 1Document25 pagesAccounting 1Afsarul HaqueNo ratings yet

- Accounting Equations PaDocument24 pagesAccounting Equations PaAisyah Ayu SaputriNo ratings yet

- Persamaan Akuntansi (Kieso Modified)Document24 pagesPersamaan Akuntansi (Kieso Modified)Hervin DiahNo ratings yet

- 1&2 Meaning and Definition of AccountingDocument73 pages1&2 Meaning and Definition of AccountingPrasad BhanageNo ratings yet

- Financial Accounting & Analysis PDFDocument6 pagesFinancial Accounting & Analysis PDFGorakhpuria MNo ratings yet

- Lecture Slides - Chapter 1 & 2Document66 pagesLecture Slides - Chapter 1 & 2Phan Đỗ QuỳnhNo ratings yet

- 7 Financial ManagementDocument46 pages7 Financial ManagementJames OwusuNo ratings yet

- Lecture Slides - Chapter 1 2Document66 pagesLecture Slides - Chapter 1 2Van Dat100% (1)

- Ch.2 - Recording Business Transactions (Pearson 6th Edition) - MHDocument56 pagesCh.2 - Recording Business Transactions (Pearson 6th Edition) - MHSamZhao100% (1)

- What Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingDocument41 pagesWhat Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingMd. Haseeb KhanNo ratings yet

- GGGGDocument12 pagesGGGGSami BoyNo ratings yet

- Chapter 12 Review Updated 11th EdDocument13 pagesChapter 12 Review Updated 11th Edangelsalvador05082006No ratings yet

- Accounting Tutorials Day 1Document8 pagesAccounting Tutorials Day 1Richboy Jude VillenaNo ratings yet

- Clase 14 ITAM Financial Statements & Models Otoño 2017Document25 pagesClase 14 ITAM Financial Statements & Models Otoño 2017Gabriel Ruiz HerreraNo ratings yet

- Accounting Notes FinallyDocument72 pagesAccounting Notes FinallyHaaris UsmanNo ratings yet

- Lec 1& 2Document37 pagesLec 1& 2Museera IffatNo ratings yet

- BBAW2103 - Tutorial 1Document69 pagesBBAW2103 - Tutorial 1M THREE THOUSAND RESOURCESNo ratings yet

- ch07 STDocument31 pagesch07 STquangle.31221025758No ratings yet

- Revision 2017 PDFDocument72 pagesRevision 2017 PDFKUUNDJUAUNENo ratings yet

- Chapter 1 of Principles of AccountingDocument49 pagesChapter 1 of Principles of AccountingNhật LinhNo ratings yet

- The Accounting EquationDocument11 pagesThe Accounting EquationMIA DEITANo ratings yet

- Intro To Financial Accounting Chapter 1Document41 pagesIntro To Financial Accounting Chapter 1hermitpassiNo ratings yet

- Power Point Presentation 2Document39 pagesPower Point Presentation 2268gunnaNo ratings yet

- Module I: Basics of Credit and Credit Process: Chapter 4: Cash Flow Statement AnalysisDocument26 pagesModule I: Basics of Credit and Credit Process: Chapter 4: Cash Flow Statement Analysissagar7No ratings yet

- IGCSE Revision-2024.Document72 pagesIGCSE Revision-2024.TaNo ratings yet

- 1) Week 2 Slides - Statement of Financial PositionDocument56 pages1) Week 2 Slides - Statement of Financial PositionTaimoor BaigNo ratings yet

- Lecture Slides - Chapter 1 2Document69 pagesLecture Slides - Chapter 1 2Nhi BuiNo ratings yet

- Principles of Accounting: Weygandt Kieso KimmelDocument38 pagesPrinciples of Accounting: Weygandt Kieso KimmelAfsar AhmedNo ratings yet

- CH 01Document54 pagesCH 01Ngân Hà ĐỗNo ratings yet

- Exercises Set B 1 Exercises Set B CompressDocument7 pagesExercises Set B 1 Exercises Set B CompressHoèn Hoèn100% (1)

- Chapter 1 - Acctg NotesDocument6 pagesChapter 1 - Acctg Notesfennyl婷.No ratings yet

- 1.1 - Accounting in ActionDocument12 pages1.1 - Accounting in ActionarjunaidbdNo ratings yet

- Chapter 12 ReviewDocument14 pagesChapter 12 ReviewDonna Mae HernandezNo ratings yet

- 001.CB Lecture FundamentalsDocument28 pages001.CB Lecture FundamentalskunyangNo ratings yet

- Accounting 1Document59 pagesAccounting 1Teodora IrimiaNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Financial ManagementDocument4 pagesFinancial Managementkiran gaikwad0% (1)

- Application Form - PLO AMP - County Reps and AmbassadorsDocument6 pagesApplication Form - PLO AMP - County Reps and AmbassadorsLazarus Kadett Ndivayele100% (1)

- Registration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Document2 pagesRegistration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Sunlight FoundationNo ratings yet

- Macke vs. Camps G.R. No. 2962Document2 pagesMacke vs. Camps G.R. No. 2962Maria Fiona Duran MerquitaNo ratings yet

- Barut Vs CabacunganDocument7 pagesBarut Vs CabacunganCharm Divina LascotaNo ratings yet

- (Ebook PDF) (Ebook PDF) Advanced Accounting, Global Edition 11th Edition All ChapterDocument43 pages(Ebook PDF) (Ebook PDF) Advanced Accounting, Global Edition 11th Edition All Chaptergryansafiul100% (9)

- Gandhi and National MovementDocument30 pagesGandhi and National MovementArun kumar SethiNo ratings yet

- StatCon Compilation of Cases Part 1Document21 pagesStatCon Compilation of Cases Part 1Angel Agustine O. Japitan IINo ratings yet

- Heirs of ClaudelDocument5 pagesHeirs of ClaudelZyldjyh C. Pactol-Portuguez100% (1)

- Indian BankDocument381 pagesIndian BankganeshNo ratings yet

- A60 - 780 - 3 - C4-Pressure Relief Valve Instrument Data Sheet & PDFDocument109 pagesA60 - 780 - 3 - C4-Pressure Relief Valve Instrument Data Sheet & PDFSoumiyaNo ratings yet

- Consequentialism EssayDocument15 pagesConsequentialism EssayKatya RobinsonNo ratings yet

- RA No. 8762 Retail Trade Liberalization Act of 2000Document5 pagesRA No. 8762 Retail Trade Liberalization Act of 2000SZNo ratings yet

- New Stockiest Appointment Check ListDocument18 pagesNew Stockiest Appointment Check ListRamana GNo ratings yet

- Erin Cullaro Response To Notary ComplaintDocument8 pagesErin Cullaro Response To Notary ComplaintForeclosure Fraud100% (1)

- Tafseer Mariful Quran Sura 109 Al Kafirun English Translation PDFDocument6 pagesTafseer Mariful Quran Sura 109 Al Kafirun English Translation PDFamaanking8bpNo ratings yet

- Justice: What's The Right Thing To Do? Episode 01 "The Moral Side of Murder"Document31 pagesJustice: What's The Right Thing To Do? Episode 01 "The Moral Side of Murder"asdasdasNo ratings yet

- Assignment - Natural JusticeDocument6 pagesAssignment - Natural JusticeYash SinghNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Income TAX Chapter 13 ReviewerDocument31 pagesIncome TAX Chapter 13 ReviewerEryn GabrielleNo ratings yet

- Zayed Sustainability PrizeDocument7 pagesZayed Sustainability PrizeKenneth BlessingNo ratings yet

- Detailed Computation ITR-1 2012-13Document2 pagesDetailed Computation ITR-1 2012-13georgenehaNo ratings yet

- Đề thi HP Ngân hàng thương mại1 E - LMS - 22.11.2021Document1 pageĐề thi HP Ngân hàng thương mại1 E - LMS - 22.11.2021Quynh NguyenNo ratings yet

- Thayer US-Burma Policy ChangeDocument2 pagesThayer US-Burma Policy ChangeCarlyle Alan ThayerNo ratings yet

- Court DateDocument1 pageCourt DateThe Daily DotNo ratings yet

- Rutgers Newark Course Schedule Spring 2018Document2 pagesRutgers Newark Course Schedule Spring 2018abdulrehman786No ratings yet

- Exam Cheat SheetDocument2 pagesExam Cheat SheetJustin BrownNo ratings yet

- Class 6 Olympiad: Choose Correct Answer(s) From The Given ChoicesDocument3 pagesClass 6 Olympiad: Choose Correct Answer(s) From The Given ChoicesRUPANo ratings yet

- Jeff Pippenger - Seven Times in LeviticusDocument16 pagesJeff Pippenger - Seven Times in LeviticusKelly K.R. RossNo ratings yet

- Big Tech InjunctionDocument155 pagesBig Tech InjunctionWashington ExaminerNo ratings yet