Download as pptx, pdf, or txt

You might also like

- Notes From Walmart AcademyDocument6 pagesNotes From Walmart AcademyLisa Hoheisel50% (2)

- Bank Audit ProgramDocument6 pagesBank Audit Programramu9999100% (1)

- Week 7Document7 pagesWeek 7SanjeevParajuliNo ratings yet

- Bank Branch Audit ManualDocument55 pagesBank Branch Audit ManualNeeraj Goyal100% (1)

- Approach To Bank Audit DNS 17 18 FinalDocument45 pagesApproach To Bank Audit DNS 17 18 FinalSowmya GuptaNo ratings yet

- Accounting ManualDocument79 pagesAccounting ManualJanelle janeo100% (4)

- What Is A Lockbox?Document7 pagesWhat Is A Lockbox?sureshyadamNo ratings yet

- AuditDocument10 pagesAuditlucinossNo ratings yet

- Revenue AuditDocument4 pagesRevenue AuditSaurabh SanandNo ratings yet

- Concurrent Audit: Dr. Saroj UpadhyayDocument40 pagesConcurrent Audit: Dr. Saroj Upadhyayharsh143352No ratings yet

- Regirsters and ReportsDocument6 pagesRegirsters and ReportsyaagyawalkNo ratings yet

- Wa0001Document64 pagesWa0001anil khamariNo ratings yet

- PRe 6 MaterialsDocument15 pagesPRe 6 MaterialsV-Heron BanalNo ratings yet

- Auditing Done in BanksDocument15 pagesAuditing Done in BanksRahul SinghNo ratings yet

- D2.4 - Revenue Audit, Undercharges & RAUDIT Reports 31.03.2023Document30 pagesD2.4 - Revenue Audit, Undercharges & RAUDIT Reports 31.03.2023vijayjhingaNo ratings yet

- Cash ProgramDocument13 pagesCash Programapi-3828505No ratings yet

- CAS Tally TRAINING MaterialDocument39 pagesCAS Tally TRAINING MaterialTesfa HunderaNo ratings yet

- Deaf 22.01.2018Document38 pagesDeaf 22.01.2018shubhamNo ratings yet

- BCH 601 SM13Document10 pagesBCH 601 SM13technical analysisNo ratings yet

- Annx-2-Con Audit Policy 2012-13Document55 pagesAnnx-2-Con Audit Policy 2012-13as14jnNo ratings yet

- Why See Proxy AccountsDocument6 pagesWhy See Proxy AccountsRohitNo ratings yet

- 03 Audit of CashDocument14 pages03 Audit of CashJoyce Anne GarduqueNo ratings yet

- Finance LTD.: 1 & 2 QuarterDocument6 pagesFinance LTD.: 1 & 2 QuarterSushil ShresthaNo ratings yet

- CAS Tally TRAINING Material PDFDocument39 pagesCAS Tally TRAINING Material PDFKingg2009100% (1)

- Illustrative Bank Branch Audit Programme For The Year Ended March 31, 2019Document21 pagesIllustrative Bank Branch Audit Programme For The Year Ended March 31, 2019rahul giriNo ratings yet

- Audit of Banks With The Help of FinacleDocument8 pagesAudit of Banks With The Help of FinacleKartikey RanaNo ratings yet

- Bank Branch Audit - Audit PlanningDocument36 pagesBank Branch Audit - Audit Planningbharat100% (3)

- 1 The Accounting Equation Accounting Cycle Steps 1 4Document6 pages1 The Accounting Equation Accounting Cycle Steps 1 4Jerric CristobalNo ratings yet

- Financial Accounting and Reporting - Week 1 Topic 5 - Review of The Accounting ProcessDocument7 pagesFinancial Accounting and Reporting - Week 1 Topic 5 - Review of The Accounting ProcessLuisitoNo ratings yet

- Rekonsiliasi Bank 1718764831Document11 pagesRekonsiliasi Bank 1718764831dqk2tqvpnhNo ratings yet

- Assignment For Audit AssistantDocument3 pagesAssignment For Audit AssistantDipali PatilNo ratings yet

- Chapter 6 - Cash & Internal ControlDocument12 pagesChapter 6 - Cash & Internal ControlHareem Zoya WarsiNo ratings yet

- Acconts Payable PDFDocument17 pagesAcconts Payable PDFN Tarun ManjunathNo ratings yet

- Wp-Trade, Other Ar & RevDocument10 pagesWp-Trade, Other Ar & RevteresaypilNo ratings yet

- Annexure I (Scope of Audit - Concurrent Auditor)Document29 pagesAnnexure I (Scope of Audit - Concurrent Auditor)Niraj JainNo ratings yet

- Advance Auditing and EDP Assigment-1 Group 8Document25 pagesAdvance Auditing and EDP Assigment-1 Group 8Abel BerhanuNo ratings yet

- Trial Test Auditing 3.2Document5 pagesTrial Test Auditing 3.2phuongvietngoNo ratings yet

- Bank Audit RelatedDocument6 pagesBank Audit RelatedNikhil Kharat NiCkNo ratings yet

- CIS Research - Quiz.3Document4 pagesCIS Research - Quiz.3Mary Jhocis P. ZaballaNo ratings yet

- Tugas Uts (Irmawati Datu Manik) 176602083Document39 pagesTugas Uts (Irmawati Datu Manik) 176602083Klopo KlepoNo ratings yet

- Apc 301 Week 8Document2 pagesApc 301 Week 8Angel Lourdie Lyn HosenillaNo ratings yet

- Cash Flow StatementDocument37 pagesCash Flow Statementg28720081No ratings yet

- Check List For Revenue Audit of A BankDocument4 pagesCheck List For Revenue Audit of A Bankjibujinson50% (2)

- Study and Evaluation of Internal Control and Revenue CycleDocument21 pagesStudy and Evaluation of Internal Control and Revenue CycleScribdTranslationsNo ratings yet

- Accounting For Non-AccountantsDocument15 pagesAccounting For Non-AccountantsMarlou Paige CortesNo ratings yet

- Procedure For Handling Npa Two Accounts at Cbs BranchesDocument3 pagesProcedure For Handling Npa Two Accounts at Cbs BranchessunilNo ratings yet

- Accounting Cycle For PostingDocument14 pagesAccounting Cycle For PostingJerrald Meyer L. BayaniNo ratings yet

- Module 1 Review of The Accounting ProcessDocument14 pagesModule 1 Review of The Accounting ProcessmcanutoNo ratings yet

- Audit ProgrammeDocument12 pagesAudit ProgrammeCA Nagendranadh TadikondaNo ratings yet

- CHAPTER 4.lecture Note-Apr 2023Document16 pagesCHAPTER 4.lecture Note-Apr 2023Eyuel SintayehuNo ratings yet

- Instruction Circular No.: 2608 Department Running No.: 351Document4 pagesInstruction Circular No.: 2608 Department Running No.: 351sanjog patnaikNo ratings yet

- MYOB Data Import ProcedureDocument3 pagesMYOB Data Import ProcedureAnonymous 7mJIoO1bh4No ratings yet

- Process Financial Transactions and Extract Interim Reports - 025735Document37 pagesProcess Financial Transactions and Extract Interim Reports - 025735l2557206No ratings yet

- Scope of Concurrent AuditDocument17 pagesScope of Concurrent AuditAnandNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- The Controller's Function: The Work of the Managerial AccountantFrom EverandThe Controller's Function: The Work of the Managerial AccountantRating: 2 out of 5 stars2/5 (1)

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 4.5 out of 5 stars4.5/5 (2)

- B.C.M Arya Model SR - Sec. School, Shastri Nagar Ludhiana GK L-1 (Look Out) Class-1 (2020-2021)Document2 pagesB.C.M Arya Model SR - Sec. School, Shastri Nagar Ludhiana GK L-1 (Look Out) Class-1 (2020-2021)sahil rohitNo ratings yet

- ( KBKBK R (Gs Fog'On) (B/Yk, Ftzs NS/ B/Yk GVSKB BKB Pzxs Nfxekohnk BJH) GKR 1 Fbzih V?NK GKR 1 Fbzih V?NK GKR 1 Fbzih V?NK GKR 1 Fbzih V?NKDocument4 pages( KBKBK R (Gs Fog'On) (B/Yk, Ftzs NS/ B/Yk GVSKB BKB Pzxs Nfxekohnk BJH) GKR 1 Fbzih V?NK GKR 1 Fbzih V?NK GKR 1 Fbzih V?NK GKR 1 Fbzih V?NKsahil rohitNo ratings yet

- 1-All-5462-ENGLISH READING PDFDocument4 pages1-All-5462-ENGLISH READING PDFsahil rohitNo ratings yet

- Application For Admission in Ukg DpsDocument1 pageApplication For Admission in Ukg Dpssahil rohitNo ratings yet

- Microsoft Word - Application For Admission in UkgDocument1 pageMicrosoft Word - Application For Admission in Ukgsahil rohitNo ratings yet

- Risk and Return (Part I)Document16 pagesRisk and Return (Part I)mimiNo ratings yet

- Solution 20 MarksDocument17 pagesSolution 20 Marksneha MistryNo ratings yet

- EIB-551 - Summer 2020 - PP - Exporting - Bangladeshi - VegetableDocument14 pagesEIB-551 - Summer 2020 - PP - Exporting - Bangladeshi - VegetableFarhan TanvirNo ratings yet

- Revision Notes MicroeconomicsDocument12 pagesRevision Notes MicroeconomicsChiragNo ratings yet

- AS S1 Essay IG-AS SIADocument5 pagesAS S1 Essay IG-AS SIA2537771050No ratings yet

- MAS 2 CAp BudgetingDocument45 pagesMAS 2 CAp BudgetingMarian B TersonaNo ratings yet

- 4 The Firm's Capital Structure and Degree of LeverageDocument9 pages4 The Firm's Capital Structure and Degree of LeverageMariel GarraNo ratings yet

- Pots and Trade: Spacefillers or Objets D'Art?: Article by David W. J. GillDocument11 pagesPots and Trade: Spacefillers or Objets D'Art?: Article by David W. J. GillThomas SwantonNo ratings yet

- FM - Module 2Document23 pagesFM - Module 2Alok Arun MohapatraNo ratings yet

- Factors Affecting ProductivityDocument16 pagesFactors Affecting ProductivityArslan MunawarNo ratings yet

- Technopreneurship 101: Module 6: Business ModelDocument83 pagesTechnopreneurship 101: Module 6: Business ModelTOLENTINO, Julius Mark VirayNo ratings yet

- BMO Tax Documents 2023-02-15 15-27-03Document2 pagesBMO Tax Documents 2023-02-15 15-27-03elenaNo ratings yet

- Form PDF 710924950260719Document6 pagesForm PDF 710924950260719Parteek SharmaNo ratings yet

- How Economics Affects Business: The Creation and Distribution of WealthDocument37 pagesHow Economics Affects Business: The Creation and Distribution of WealthRio DanovanNo ratings yet

- Mobilizing The Indo-Pacific Infrastructure Response To China S Belt and Road Initiative in Southeast AsiaDocument15 pagesMobilizing The Indo-Pacific Infrastructure Response To China S Belt and Road Initiative in Southeast AsiaValentina SadchenkoNo ratings yet

- PT Rina Indonesia BVD 23 - 08 - 2022 04 - 41Document61 pagesPT Rina Indonesia BVD 23 - 08 - 2022 04 - 41harryxwjNo ratings yet

- Morning: Yinson's Major Shareholder Acquires 50.2% Stake in Icon Offshore Triggers MGO at 63.5 Sen Per ShareDocument24 pagesMorning: Yinson's Major Shareholder Acquires 50.2% Stake in Icon Offshore Triggers MGO at 63.5 Sen Per ShareQuint WongNo ratings yet

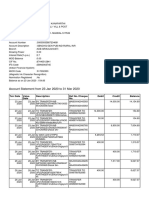

- 23 Jan To 31mar 2020 Sbi Suresh StateDocument12 pages23 Jan To 31mar 2020 Sbi Suresh Stateravi lingamNo ratings yet

- Agencies in MumbaiDocument5 pagesAgencies in MumbaiPriyanku BhatnagarNo ratings yet

- Corporations: Organization, Capital Stock Transactions, and DividendsDocument64 pagesCorporations: Organization, Capital Stock Transactions, and DividendsDesta MaldinaNo ratings yet

- This Study Resource Was: Afar de Leon/De Leon/De Leon Quiz 2 Set A Batch: M A Y 2018Document2 pagesThis Study Resource Was: Afar de Leon/De Leon/De Leon Quiz 2 Set A Batch: M A Y 2018Jamaica DavidNo ratings yet

- Initial Off-Take Agreement Signed With Leading European Tungsten RefinerDocument2 pagesInitial Off-Take Agreement Signed With Leading European Tungsten RefinerKOMATSU SHOVELNo ratings yet

- JSW Steel IR 2018-19 Final PDFDocument424 pagesJSW Steel IR 2018-19 Final PDFSweta SinhaNo ratings yet

- ShubakanthDocument1 pageShubakanthshubakanthNo ratings yet

- CONTRACT OF SALE - Gamma Farms LimitedDocument4 pagesCONTRACT OF SALE - Gamma Farms LimitedPrince Amisi ChirwaNo ratings yet

- Vdocuments - MX Internship Report 58bd59f3d6a33Document68 pagesVdocuments - MX Internship Report 58bd59f3d6a33Eyuael SolomonNo ratings yet

- Statement 2023 07 09Document4 pagesStatement 2023 07 09blackson knightsonNo ratings yet

- Devaynes V Noble Baring V Noble (1831) 39 ER 482Document5 pagesDevaynes V Noble Baring V Noble (1831) 39 ER 482akhil SrinadhuNo ratings yet

- KTT TELEX CODE PAYMENT (Signed)Document4 pagesKTT TELEX CODE PAYMENT (Signed)ChristianMNo ratings yet