Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- XLS092-XLS-EnG Tire City - RaghuDocument49 pagesXLS092-XLS-EnG Tire City - RaghuSohini Mo BanerjeeNo ratings yet

- Butler Excel Sheets (Group 2)Document11 pagesButler Excel Sheets (Group 2)Nathan ClarkinNo ratings yet

- Budgets & EncumbrancesDocument31 pagesBudgets & EncumbrancesvishyNo ratings yet

- Review Notes #2 - Comprehensive Problem PDFDocument3 pagesReview Notes #2 - Comprehensive Problem PDFtankofdoom 4No ratings yet

- Premiums and WarrantyDocument8 pagesPremiums and WarrantyMarela Velasquez100% (2)

- P1 1.3CashBasisAccrualBasisSingleEntryZETADocument3 pagesP1 1.3CashBasisAccrualBasisSingleEntryZETASophia AprilNo ratings yet

- Financial Modelling AssignmentDocument6 pagesFinancial Modelling AssignmentMomin AbrarNo ratings yet

- Provisions Related Standards: Pas 37 - Provisions, Contingent Liabilities & Contingent AssetsDocument7 pagesProvisions Related Standards: Pas 37 - Provisions, Contingent Liabilities & Contingent AssetsJulie Mae Caling MalitNo ratings yet

- Financial Compliance Audits PSC 20-21Document44 pagesFinancial Compliance Audits PSC 20-21NBC MontanaNo ratings yet

- Financial Management On Square Toiletries LTDDocument73 pagesFinancial Management On Square Toiletries LTDShahriar AlamNo ratings yet

- Nek DVP Sample BPDocument36 pagesNek DVP Sample BPajNo ratings yet

- SAP Library - GlossaryDocument53 pagesSAP Library - Glossaryccwilliams5No ratings yet

- Accruals and PrepaymentsDocument4 pagesAccruals and PrepaymentsMuhammad Zubair YounasNo ratings yet

- Janice Tamagi Is The Accountant For Thin Dime LTD Which PDFDocument1 pageJanice Tamagi Is The Accountant For Thin Dime LTD Which PDFMiroslav GegoskiNo ratings yet

- 1.5.1 ActivityDocument3 pages1.5.1 ActivityGWYNETTE CAMIDCHOLNo ratings yet

- 2022 Annual Report Final - Dizon MinesDocument112 pages2022 Annual Report Final - Dizon MinesJun BelenNo ratings yet

- ACCO 20063 Homework 4 Review of Accounting CycleDocument3 pagesACCO 20063 Homework 4 Review of Accounting CycleVincent Luigil Alcera100% (1)

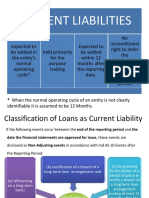

- Current Liabilities: When The Normal Operating Cycle of An Entity Is Not ClearlyDocument9 pagesCurrent Liabilities: When The Normal Operating Cycle of An Entity Is Not Clearlysispita dashNo ratings yet

- Final CHP T 2Document152 pagesFinal CHP T 2Marikrishna Chandran CA100% (1)

- An Introduction To Absence Plan Carryover Feature in Oracle HCM Cloud Application - Fusion Practices LTDDocument13 pagesAn Introduction To Absence Plan Carryover Feature in Oracle HCM Cloud Application - Fusion Practices LTDsachanpreetiNo ratings yet

- Obtaining of Clearances Related To Defence, Airspace and EnvironmentDocument15 pagesObtaining of Clearances Related To Defence, Airspace and EnvironmentMaheshkv MahiNo ratings yet

- Module 3-BONDS PAYABLEDocument24 pagesModule 3-BONDS PAYABLEJeanivyle CarmonaNo ratings yet

- Salaries: After Studying This Chapter, You Would Be Able ToDocument82 pagesSalaries: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Accounting 1A Exam 1 - Spring 2011 - Section 1 - SolutionsDocument14 pagesAccounting 1A Exam 1 - Spring 2011 - Section 1 - SolutionsRex Tang100% (1)

- Cash and Accrual BasisDocument5 pagesCash and Accrual BasisLeisleiRago100% (1)

- How To Read Finanacial ReportsDocument48 pagesHow To Read Finanacial ReportsdeepakNo ratings yet

- Preparation of Adjusting EntriesDocument25 pagesPreparation of Adjusting EntriesMemey C.100% (1)

- Introduction To The Scope of Syllabus and Paper Format.: ISC 2021 Accounts ProjectDocument20 pagesIntroduction To The Scope of Syllabus and Paper Format.: ISC 2021 Accounts ProjectMariamNo ratings yet

- Financial Reporting 2Nd Edition Loftus Solutions Manual Full Chapter PDFDocument62 pagesFinancial Reporting 2Nd Edition Loftus Solutions Manual Full Chapter PDFalicebellamyq3yj100% (11)