Download as pptx, pdf, or txt

You might also like

- Government and Not For Profit Accounting 7th Edition PDFDocument3 pagesGovernment and Not For Profit Accounting 7th Edition PDFChristian23% (13)

- TAX - Final Pre-Board With Answer Key Batch Exodus - EncryptedDocument16 pagesTAX - Final Pre-Board With Answer Key Batch Exodus - EncryptedSophia Perez100% (1)

- Thomas & Ely (1996) - "Making Differences Matter: A New Paradigm For Managing Diversity," Harvard Business ReviewDocument2 pagesThomas & Ely (1996) - "Making Differences Matter: A New Paradigm For Managing Diversity," Harvard Business ReviewEdison Bitencourt de Almeida100% (1)

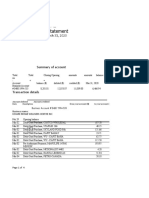

- Bank StatementDocument14 pagesBank StatementLJ AggabaoNo ratings yet

- Financial Deepening Challenge Fund Strategic Project ReviewDocument58 pagesFinancial Deepening Challenge Fund Strategic Project ReviewArini Putri Sari IINo ratings yet

- SFAS No 117Document70 pagesSFAS No 117abekaforumNo ratings yet

- EFFECT OF COST ACCOUNTING TO MANAGEMENT FinalDocument103 pagesEFFECT OF COST ACCOUNTING TO MANAGEMENT FinalFolake OlowookereNo ratings yet

- Consolidated Financial Statements: On Date of Business CombinationDocument53 pagesConsolidated Financial Statements: On Date of Business Combinationankursharma06No ratings yet

- CPAR87 Final PB - AFARDocument15 pagesCPAR87 Final PB - AFARLJ AggabaoNo ratings yet

- Afar 8617Document5 pagesAfar 8617LJ AggabaoNo ratings yet

- Executive Summary: Focus Group ReportDocument4 pagesExecutive Summary: Focus Group ReportkaranNo ratings yet

- Accounting For Non-Profit OrganizationDocument76 pagesAccounting For Non-Profit OrganizationQuennie Desullan0% (1)

- InventoryDocument45 pagesInventoryjoyabyssNo ratings yet

- Profitability Sustainability RatiosDocument3 pagesProfitability Sustainability RatiosRhodelbert Rizare Del SocorroNo ratings yet

- Audtheo Q2Document749 pagesAudtheo Q2Haynako100% (1)

- Lean Software DevelopmentDocument6 pagesLean Software DevelopmentYasir KazmNo ratings yet

- APP Sustainability Report 2010-2011Document152 pagesAPP Sustainability Report 2010-2011Asia Pulp and PaperNo ratings yet

- TOR For Project Financial Management SpecialistDocument4 pagesTOR For Project Financial Management SpecialistEmil LeauNo ratings yet

- Format CoA - SAIDocument8 pagesFormat CoA - SAIarlinaNo ratings yet

- Basics of Accounting Level IIDocument63 pagesBasics of Accounting Level IIjustvicky1000No ratings yet

- Accounting For Not-for-Profit OrganizationsDocument52 pagesAccounting For Not-for-Profit OrganizationsSalsabiilaa HerlambangNo ratings yet

- Sales Return-FlowchartDocument1 pageSales Return-Flowchartkate trishaNo ratings yet

- Financial Ratio Analysis, Exercise and WorksheetDocument4 pagesFinancial Ratio Analysis, Exercise and Worksheetatiqahrahim90No ratings yet

- Balance Sheet Ratio Analysis FormulaDocument9 pagesBalance Sheet Ratio Analysis FormulaAbu Jahid100% (1)

- Preparing Simple Consolidated Financial StatementsDocument10 pagesPreparing Simple Consolidated Financial Statementstapia4yeabuNo ratings yet

- Welcome To The Presentation of The: Group 4Document126 pagesWelcome To The Presentation of The: Group 4Ronald Jason RomeroNo ratings yet

- Ortega, Wendy B. Prof. Malanum Bsba FTM 3-4: What Is Credit Management?Document7 pagesOrtega, Wendy B. Prof. Malanum Bsba FTM 3-4: What Is Credit Management?Mhabel MaglasangNo ratings yet

- Analysis and Design Accounting Information System PDFDocument5 pagesAnalysis and Design Accounting Information System PDFHeilen PratiwiNo ratings yet

- Module 1 PDFDocument11 pagesModule 1 PDFAangela Del Rosario CorpuzNo ratings yet

- Zambia National Budget and Development Planning Policy (Draft)Document17 pagesZambia National Budget and Development Planning Policy (Draft)Chola Mukanga100% (2)

- Accountng ProcessDocument12 pagesAccountng ProcessJessica CorpuzNo ratings yet

- Harmonisation of Accounting StandardsDocument39 pagesHarmonisation of Accounting StandardsKam YinNo ratings yet

- Literature Review On SME Access To Credit in South Africa - Final Report - NCR - Dec 2011 PDFDocument92 pagesLiterature Review On SME Access To Credit in South Africa - Final Report - NCR - Dec 2011 PDFtharani1771_32442248No ratings yet

- AIS Chapter 1Document5 pagesAIS Chapter 1Reyna Marie Labadan-LasacarNo ratings yet

- Revenue RecognitionDocument9 pagesRevenue RecognitionBerlian NovitaNo ratings yet

- Basic Accounting SystemDocument37 pagesBasic Accounting SystemGetie TigetNo ratings yet

- Hewlett-Packard (HP) and Autonomy AcquisitionDocument21 pagesHewlett-Packard (HP) and Autonomy AcquisitionPhạm Thu HuyềnNo ratings yet

- Govt & NFP Accounting - Ch2Document70 pagesGovt & NFP Accounting - Ch2Fãhâd Õró ÂhmédNo ratings yet

- Chapter 3 AccountingDocument11 pagesChapter 3 AccountingĐỗ ĐăngNo ratings yet

- Credit Managers. Lesson 3Document40 pagesCredit Managers. Lesson 3Joseph PoNo ratings yet

- GNFP CH 3Document41 pagesGNFP CH 3Bilisummaa GeetahuunNo ratings yet

- 13Document63 pages13amysilverbergNo ratings yet

- Dokumen - Tips Ch03test Bank Jeter Chapter 3Document18 pagesDokumen - Tips Ch03test Bank Jeter Chapter 3Evelyn Purnama SariNo ratings yet

- Financial Accounting and Reporting 01Document9 pagesFinancial Accounting and Reporting 01Nuah SilvestreNo ratings yet

- Ale Aubrey Bsma 3 1.lguDocument6 pagesAle Aubrey Bsma 3 1.lguAstrid XiNo ratings yet

- PAS 1 Presentation of Financial StatementsDocument53 pagesPAS 1 Presentation of Financial Statementsjan petosilNo ratings yet

- Analysis & Interpretation of Financial StatementsDocument44 pagesAnalysis & Interpretation of Financial StatementsSecret DeityNo ratings yet

- Activity 6 Reflection Paper On User ExperienceDocument2 pagesActivity 6 Reflection Paper On User Experiencekyla recintoNo ratings yet

- Midterm Audcis ReviewerDocument29 pagesMidterm Audcis Reviewerintacc recordingsNo ratings yet

- Capital BudgetingDocument10 pagesCapital BudgetingAkatsuki no YonaNo ratings yet

- Solution For Accounting Information Systems Basic Concepts and Current Issues 4th Edition PDFDocument11 pagesSolution For Accounting Information Systems Basic Concepts and Current Issues 4th Edition PDFCB OrdersNo ratings yet

- Paps 1013Document18 pagesPaps 1013Zillah BuldaNo ratings yet

- As-1 Disclosure of Accounting PoliciesDocument7 pagesAs-1 Disclosure of Accounting PoliciesPrakash_Tandon_583No ratings yet

- CH04 Revenue Cycle PDFDocument73 pagesCH04 Revenue Cycle PDFZion Ilagan0% (1)

- Auditing QuestionsDocument10 pagesAuditing Questionssalva8983No ratings yet

- Week 1 Conceptual Framework For Financial ReportingDocument17 pagesWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARRONo ratings yet

- Acfn 723 Chapter 3 - 2019Document84 pagesAcfn 723 Chapter 3 - 2019nigusNo ratings yet

- Auditor's ReportDocument20 pagesAuditor's ReportSivabalan AchchuthanNo ratings yet

- Chapter 9 Audit of Investing CycleDocument11 pagesChapter 9 Audit of Investing CycleconsulivyNo ratings yet

- Domestic Bank ListDocument14 pagesDomestic Bank Listfadli_zulNo ratings yet

- Audit Report PDFDocument14 pagesAudit Report PDFঅাজবমানুষNo ratings yet

- Chapter 2-Audits of Financial Statements PDFDocument23 pagesChapter 2-Audits of Financial Statements PDFCaryll Joy BisnanNo ratings yet

- AC518 Supplement - NPOsDocument7 pagesAC518 Supplement - NPOsAngelyn SusonNo ratings yet

- IR 2 Mod 11 Non For ProfitDocument7 pagesIR 2 Mod 11 Non For ProfitAndrea LanuzaNo ratings yet

- Government AccountingDocument6 pagesGovernment AccountingShem CasimiroNo ratings yet

- ASSIGNMENTDocument4 pagesASSIGNMENTLJ AggabaoNo ratings yet

- Seatwork Joint ArrangementsDocument1 pageSeatwork Joint ArrangementsLJ AggabaoNo ratings yet

- Government Accounting Exam PhilippinesDocument4 pagesGovernment Accounting Exam PhilippinesLJ Aggabao100% (1)

- Hospital Revenues (1-32)Document13 pagesHospital Revenues (1-32)LJ AggabaoNo ratings yet

- A11 9.8.23Document4 pagesA11 9.8.23LJ AggabaoNo ratings yet

- Law 101-The Law On Obligation and Contracts: Prelims Dterms FinalsDocument2 pagesLaw 101-The Law On Obligation and Contracts: Prelims Dterms FinalsLJ AggabaoNo ratings yet

- Leave Revised FloricelDocument2 pagesLeave Revised FloricelLJ AggabaoNo ratings yet

- Nature of Government AccountingDocument16 pagesNature of Government AccountingLJ AggabaoNo ratings yet

- Advanced Accounting Chapter 21Document9 pagesAdvanced Accounting Chapter 21LJ AggabaoNo ratings yet

- Advanced Accounting Chapter 20Document12 pagesAdvanced Accounting Chapter 20LJ AggabaoNo ratings yet

- Advanced Accounting Chapter 22Document9 pagesAdvanced Accounting Chapter 22LJ AggabaoNo ratings yet

- Quiz Acctng 603Document10 pagesQuiz Acctng 603LJ AggabaoNo ratings yet

- Final PB87 Sol. MASDocument2 pagesFinal PB87 Sol. MASLJ AggabaoNo ratings yet

- Acctg 403 SyllabusDocument12 pagesAcctg 403 SyllabusLJ AggabaoNo ratings yet

- Afar 8722Document2 pagesAfar 8722LJ AggabaoNo ratings yet

- Mas 8711Document12 pagesMas 8711LJ AggabaoNo ratings yet

- MAS8702Document16 pagesMAS8702LJ AggabaoNo ratings yet

- Quiz NPO Multiple ChoiceDocument4 pagesQuiz NPO Multiple ChoiceLJ Aggabao0% (1)

- Income Taxation - 2020 - 2021Document9 pagesIncome Taxation - 2020 - 2021LJ AggabaoNo ratings yet

- NPD AssignmentDocument3 pagesNPD AssignmentNicky BojeNo ratings yet

- Capital Structure Self Correction ProblemsDocument53 pagesCapital Structure Self Correction ProblemsTamoor BaigNo ratings yet

- Animated Scrolling Dashboard PPT by Gemo EditsDocument12 pagesAnimated Scrolling Dashboard PPT by Gemo Editssantaanaalfie137No ratings yet

- MegaProjectsin Bangladeshandits ImpactonNational EconomyDocument42 pagesMegaProjectsin Bangladeshandits ImpactonNational Economywindows masterNo ratings yet

- Internal Control ChecklistDocument5 pagesInternal Control ChecklistPHILLIT CLASSNo ratings yet

- Form 26QBDocument1 pageForm 26QBYashu GoelNo ratings yet

- Taxation Midterm Exam With Answer KeyDocument25 pagesTaxation Midterm Exam With Answer Keychelissamaerojas100% (1)

- Proposal Project WholeDocument6 pagesProposal Project WholeJohn Daryl LuceroNo ratings yet

- Repayment Notification 123583047 2014-12-16Document2 pagesRepayment Notification 123583047 2014-12-16MiguelThaxNo ratings yet

- Business PlanDocument26 pagesBusiness PlanJad LavillaNo ratings yet

- Case Comment On Vivek Narayan SharmaDocument11 pagesCase Comment On Vivek Narayan SharmaG P60 MOOTER 1No ratings yet

- BBM Lead-Magnet Beginner Popular-IndicatorsDocument10 pagesBBM Lead-Magnet Beginner Popular-IndicatorsFotis PapatheofanousNo ratings yet

- Enumerating The AssetsDocument11 pagesEnumerating The AssetsShikha Dubey0% (1)

- Building A Flexible Supply Chain in Low Volume High Mix IndustrialsDocument9 pagesBuilding A Flexible Supply Chain in Low Volume High Mix IndustrialsThanhquy NguyenNo ratings yet

- Employees' Provident Fund Scheme, 1952: Fujitsu Employee Code: Contact Email Id: Contact Cell No.Document2 pagesEmployees' Provident Fund Scheme, 1952: Fujitsu Employee Code: Contact Email Id: Contact Cell No.adityajain104No ratings yet

- Maryam JabeenDocument47 pagesMaryam JabeenMaryam JabeenNo ratings yet

- Part FourDocument3 pagesPart FourHannah CorpuzNo ratings yet

- Kolehiyo NG Lungsod NG LipaDocument72 pagesKolehiyo NG Lungsod NG LipaMJ ArandaNo ratings yet

- Central Bank Circular No. 905: General ProvisionsDocument6 pagesCentral Bank Circular No. 905: General ProvisionsRaezel Louise VelayoNo ratings yet

- Macroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYDocument54 pagesMacroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYkaylaNo ratings yet

- Topic: 1.1 What Is Accounting? 1.2 Who Uses The Accounting Data 1.3 The Basic Accounting EquationDocument6 pagesTopic: 1.1 What Is Accounting? 1.2 Who Uses The Accounting Data 1.3 The Basic Accounting EquationAnn Ameera OraisNo ratings yet

- Core Assets DefinitionDocument7 pagesCore Assets Definitionako akoNo ratings yet

- WB - Paper-17 CMA FINALDocument131 pagesWB - Paper-17 CMA FINALvijaykumartaxNo ratings yet

- Intended Learning Outcomes: Principles of Customs Administration LESSON 1: Profile of The Bureau of CustomsDocument10 pagesIntended Learning Outcomes: Principles of Customs Administration LESSON 1: Profile of The Bureau of CustomsAbdurahman shuaibNo ratings yet

- The Budgeting Process and Budget Trends in The National Government of The PhilippinesDocument60 pagesThe Budgeting Process and Budget Trends in The National Government of The PhilippinestentenNo ratings yet

- Suitability of Pavement Type For Developing Countries From An Economic Perspective Using Life Cycle Cost AnalysisDocument8 pagesSuitability of Pavement Type For Developing Countries From An Economic Perspective Using Life Cycle Cost AnalysisAlazar DestaNo ratings yet

- Evaluation of Digital Realty Trust IncDocument18 pagesEvaluation of Digital Realty Trust Incwafula stanNo ratings yet