Introduction To Business Finance: by MK

Introduction To Business Finance: by MK

You might also like

- Inception ReportDocument9 pagesInception ReportFasika Tegegn100% (2)

- Ratio Analysis Project Shankar - NewDocument15 pagesRatio Analysis Project Shankar - NewShubham SinghalNo ratings yet

- Silhouettes - MansfieldDocument2 pagesSilhouettes - MansfieldValentinaNo ratings yet

- Boost Your Brain PowerDocument2 pagesBoost Your Brain PowerStrafalogea SerbanNo ratings yet

- Ratio Kotak Mahindra BankDocument64 pagesRatio Kotak Mahindra Bankdk6666No ratings yet

- Ratio Analysis SeminarDocument26 pagesRatio Analysis Seminardeepti_gaddamNo ratings yet

- FM ProjectDocument18 pagesFM Projectqureshi shireenNo ratings yet

- Ratio Analysis: We Will First Explain Why We Are Discussing Ratios?Document15 pagesRatio Analysis: We Will First Explain Why We Are Discussing Ratios?Avneet Kaur Bedi100% (1)

- Ratio AnalysisDocument21 pagesRatio Analysisvivek0999guptaNo ratings yet

- Classification of RatiosDocument10 pagesClassification of Ratiosaym_6005100% (2)

- Chapter-Two Financial AnalysisDocument94 pagesChapter-Two Financial AnalysisDejene GurmesaNo ratings yet

- Project On Kotak MahindraDocument64 pagesProject On Kotak Mahindrasamson901683% (6)

- Financial Analysis of PNBDocument73 pagesFinancial Analysis of PNBPrithviNo ratings yet

- 19wj1e0022 Financial Statment Analysis RelianceDocument67 pages19wj1e0022 Financial Statment Analysis RelianceWebsoft Tech-HydNo ratings yet

- FM Assignment1Document25 pagesFM Assignment1Rutuja ValteNo ratings yet

- RatioDocument20 pagesRatioAkashdeep MarwahaNo ratings yet

- FINMANDocument16 pagesFINMANSecret SecretNo ratings yet

- 4c. Financial Ratio AnalysisDocument12 pages4c. Financial Ratio AnalysisOmair AbbasNo ratings yet

- Chapter 1Document53 pagesChapter 1Prashob KoodathilNo ratings yet

- Ratio Analysis.Document3 pagesRatio Analysis.রুবাইয়াত নিবিড়No ratings yet

- Samle 8Document2 pagesSamle 8Mane DaralNo ratings yet

- Ratio AnalysisDocument9 pagesRatio Analysisbharti gupta100% (1)

- Management Accounting Assignment Topic:Ratio Analysis: Room 34Document18 pagesManagement Accounting Assignment Topic:Ratio Analysis: Room 34nuttynehal17100% (1)

- Report On Ratio Analysis ProjectDocument2 pagesReport On Ratio Analysis ProjectYadnesh NikhrgeNo ratings yet

- AFM Project Ratio AnalysisDocument41 pagesAFM Project Ratio AnalysisBharat GhoghariNo ratings yet

- Bilt ProjectDocument124 pagesBilt ProjectMukul BabbarNo ratings yet

- Brand Awairness Cocacola ProjectDocument70 pagesBrand Awairness Cocacola Projectthella deva prasadNo ratings yet

- Brand Awairness Cocacola ProjectDocument70 pagesBrand Awairness Cocacola Projectanikesinght123No ratings yet

- Stability RatioDocument27 pagesStability RatioashokkeeliNo ratings yet

- Synopsis Ratio AnalysisDocument3 pagesSynopsis Ratio Analysisaks_swamiNo ratings yet

- Ratio AnalysisDocument74 pagesRatio AnalysisKarthik NarambatlaNo ratings yet

- Financial Analysis ProjectDocument13 pagesFinancial Analysis ProjectAnonymous NflYP4O100% (1)

- Barkavi Bcom ProjectDocument28 pagesBarkavi Bcom Projectkamalesh kanna kamalesh kannaNo ratings yet

- Ratio AnalysisDocument11 pagesRatio AnalysisNanndita AggarwalNo ratings yet

- Accounting RatiosDocument23 pagesAccounting RatiosPratyush SainiNo ratings yet

- Financial Analysis An IntroductionDocument34 pagesFinancial Analysis An IntroductionnavjeetkumarNo ratings yet

- Ratio Analysis On Optcl, BBSRDocument47 pagesRatio Analysis On Optcl, BBSRSusmita Nayak100% (1)

- Ratio AnalysisDocument4 pagesRatio AnalysisKartikeyaDwivediNo ratings yet

- Financial Statement Analysis Financial Statement Analysis Is A Systematic Process of Identifying The Financial Strengths andDocument7 pagesFinancial Statement Analysis Financial Statement Analysis Is A Systematic Process of Identifying The Financial Strengths andrajivkingofspadesNo ratings yet

- Presentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDDocument12 pagesPresentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDEra ChaudharyNo ratings yet

- FM - Lesson 4 - Fin. Analysis - RatiosDocument8 pagesFM - Lesson 4 - Fin. Analysis - RatiosRena MabinseNo ratings yet

- Definition and Explanation of Financial Statement AnalysisDocument9 pagesDefinition and Explanation of Financial Statement AnalysisadaktanuNo ratings yet

- BHEL FinanceDocument44 pagesBHEL FinanceJayanth C VNo ratings yet

- Ratio AnalysisDocument7 pagesRatio AnalysisShalemRaj100% (1)

- Definition and Explanation of Financial Statement AnalysisDocument7 pagesDefinition and Explanation of Financial Statement Analysismedbest11No ratings yet

- Theoretical PerspectiveDocument12 pagesTheoretical PerspectivepopliyogeshanilNo ratings yet

- Chapter-1-Ratio AnalysisDocument8 pagesChapter-1-Ratio AnalysisRG RAJNo ratings yet

- Analysis of Financial StatementDocument86 pagesAnalysis of Financial StatementSandipan Basu100% (2)

- Meaning of Ratio AnalysisDocument31 pagesMeaning of Ratio AnalysisPrakash Bhanushali100% (1)

- Financial and Accounting Digital Assignment-2Document22 pagesFinancial and Accounting Digital Assignment-2Vignesh ShanmugamNo ratings yet

- Ratio AnalysisDocument21 pagesRatio Analysisindusunkari200No ratings yet

- Financial ANalysis Final ReportDocument70 pagesFinancial ANalysis Final ReportNeha Sable DeshmukhNo ratings yet

- Ratio Analysis ClassDocument20 pagesRatio Analysis ClassRanjith KumarNo ratings yet

- Chapter # 2 Financial AnalysisDocument94 pagesChapter # 2 Financial Analysiswondosen birhanuNo ratings yet

- Introduction Part 123Document11 pagesIntroduction Part 123shaik karishmaNo ratings yet

- Mahesh Total Project 1Document70 pagesMahesh Total Project 1Kaveti Madhu lathaNo ratings yet

- My ProjectDocument72 pagesMy ProjectPrashob Koodathil0% (1)

- AccountsDocument4 pagesAccountsAnita YadavNo ratings yet

- Ratio Analysis NotesDocument9 pagesRatio Analysis Noteshussainnaqvi1194No ratings yet

- Fabm ReviewerDocument3 pagesFabm ReviewerRiguel Jameson AllejeNo ratings yet

- Ratio Analysis NoteDocument7 pagesRatio Analysis NoteVinesh Kumar100% (1)

- Financial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesFrom EverandFinancial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Computer McqsDocument32 pagesComputer McqsDarshan KhatriNo ratings yet

- IslamiyatDocument71 pagesIslamiyatDarshan KhatriNo ratings yet

- EnglishDocument8 pagesEnglishDarshan KhatriNo ratings yet

- Introduction To Business Finance: by MKDocument30 pagesIntroduction To Business Finance: by MKDarshan KhatriNo ratings yet

- Introduction To Business Finance: by MKDocument35 pagesIntroduction To Business Finance: by MKDarshan KhatriNo ratings yet

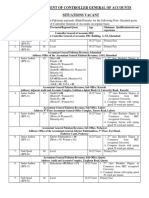

- Controller General of Accounts: As Per AdvertisementDocument2 pagesController General of Accounts: As Per AdvertisementDarshan KhatriNo ratings yet

- Department of Controller General of Accounts Situations VacantDocument4 pagesDepartment of Controller General of Accounts Situations VacantDarshan KhatriNo ratings yet

- IB Mathematics A&I SL Syllabus Outcomes: Numbers and Algebra Common SLDocument3 pagesIB Mathematics A&I SL Syllabus Outcomes: Numbers and Algebra Common SLLorraine SabbaghNo ratings yet

- PMLS 2 Lesson 1Document4 pagesPMLS 2 Lesson 1Void MelromarcNo ratings yet

- Muslim Army of Jesus & Mahdi & Their 7 SignsDocument13 pagesMuslim Army of Jesus & Mahdi & Their 7 SignsAbdulaziz Khattak Abu FatimaNo ratings yet

- Prepared By: Abhishek Jaiswal (14) Vikram Gupta (19) Gaurav Kumar (21) Ateet Gupta (28) Varun Yadav (47) Siddharth LohoDocument14 pagesPrepared By: Abhishek Jaiswal (14) Vikram Gupta (19) Gaurav Kumar (21) Ateet Gupta (28) Varun Yadav (47) Siddharth LohoateetiimNo ratings yet

- Lecture Notes NanomaterialsDocument34 pagesLecture Notes NanomaterialsEsther Yesudasan67% (3)

- Hiberno-English Powerpoint Feb 2017 PDFDocument24 pagesHiberno-English Powerpoint Feb 2017 PDFceippuigdenvalls100% (1)

- FFT Tutorial: 1 Getting To Know The FFTDocument6 pagesFFT Tutorial: 1 Getting To Know The FFTDavid NasaelNo ratings yet

- GRE Physics Test: Practice BookDocument91 pagesGRE Physics Test: Practice BookGalo CandelaNo ratings yet

- Crime and Punishment British English Teacher Ver2 BWDocument5 pagesCrime and Punishment British English Teacher Ver2 BWinaNo ratings yet

- Product Category LifecyclesDocument13 pagesProduct Category LifecyclesAdam Andrew OngNo ratings yet

- 5 2 ConceptualDocument4 pages5 2 ConceptualArfiNo ratings yet

- COT3 IDocument2 pagesCOT3 IKamsha Uy100% (1)

- Operations Research: Assignment 1Document7 pagesOperations Research: Assignment 1Shashank JainNo ratings yet

- Lesson PlanDocument3 pagesLesson Planapi-530241350No ratings yet

- My Sexual Autobiography Vol 1Document218 pagesMy Sexual Autobiography Vol 1megan fisher50% (2)

- Postgraduate Research Supervision Logbook For SupervisorDocument4 pagesPostgraduate Research Supervision Logbook For SupervisorMuhammad Hilmi bin Abd Rashid Fakulti Pendidikan & Sains Sosial (FPSS)No ratings yet

- 2024 South African Hindu Maha Sabha Calendar Hindu CalenderDocument1 page2024 South African Hindu Maha Sabha Calendar Hindu CalenderAmichand Maraj100% (1)

- Georgios T. Halkias - Richard K. Payne - Ryan Overbey - Anna Andreeva - Robert F. Rhodes - James Apple - Thomas Eijo Dreitlein - Aaron P Proffitt - Charles B. Jones - Fabio Rambelli - Michihi - KopyaDocument808 pagesGeorgios T. Halkias - Richard K. Payne - Ryan Overbey - Anna Andreeva - Robert F. Rhodes - James Apple - Thomas Eijo Dreitlein - Aaron P Proffitt - Charles B. Jones - Fabio Rambelli - Michihi - KopyaHaşim LokmanhekimNo ratings yet

- Renault Twizzy Electric CarDocument114 pagesRenault Twizzy Electric CarsawankuyaNo ratings yet

- (Q2) - Improving The Experience For Software-Measurement System End-UsersDocument25 pages(Q2) - Improving The Experience For Software-Measurement System End-UserscheikhNo ratings yet

- Master EK's Commentary On "Aham Vrkshasya Rerivā " in His Tai.U. Rahasya PrakāsaDocument2 pagesMaster EK's Commentary On "Aham Vrkshasya Rerivā " in His Tai.U. Rahasya PrakāsaBala Subrahmanyam PiratlaNo ratings yet

- Ram Rattan V State of UPDocument8 pagesRam Rattan V State of UPNiveditha Ramakrishnan ThantlaNo ratings yet

- Equipment Reliability AnalysisDocument1 pageEquipment Reliability AnalysisnukkeNo ratings yet

- Violated and Transcended BodiesDocument80 pagesViolated and Transcended BodiesFideblaymid CruzNo ratings yet

- People Vs Rizal (1981)Document21 pagesPeople Vs Rizal (1981)Abigail DeeNo ratings yet

- OralComm Q2 W6 GLAKDocument20 pagesOralComm Q2 W6 GLAKCherryl GallegoNo ratings yet

- Heart Copy of Demonstration-Teaching-Rating-Sheet-ICTDocument3 pagesHeart Copy of Demonstration-Teaching-Rating-Sheet-ICTLouann Heart Lupo100% (1)

Download as pptx, pdf, or txt

You might also like

- Inception ReportDocument9 pagesInception ReportFasika Tegegn100% (2)

- Ratio Analysis Project Shankar - NewDocument15 pagesRatio Analysis Project Shankar - NewShubham SinghalNo ratings yet

- Silhouettes - MansfieldDocument2 pagesSilhouettes - MansfieldValentinaNo ratings yet

- Boost Your Brain PowerDocument2 pagesBoost Your Brain PowerStrafalogea SerbanNo ratings yet

- Ratio Kotak Mahindra BankDocument64 pagesRatio Kotak Mahindra Bankdk6666No ratings yet

- Ratio Analysis SeminarDocument26 pagesRatio Analysis Seminardeepti_gaddamNo ratings yet

- FM ProjectDocument18 pagesFM Projectqureshi shireenNo ratings yet

- Ratio Analysis: We Will First Explain Why We Are Discussing Ratios?Document15 pagesRatio Analysis: We Will First Explain Why We Are Discussing Ratios?Avneet Kaur Bedi100% (1)

- Ratio AnalysisDocument21 pagesRatio Analysisvivek0999guptaNo ratings yet

- Classification of RatiosDocument10 pagesClassification of Ratiosaym_6005100% (2)

- Chapter-Two Financial AnalysisDocument94 pagesChapter-Two Financial AnalysisDejene GurmesaNo ratings yet

- Project On Kotak MahindraDocument64 pagesProject On Kotak Mahindrasamson901683% (6)

- Financial Analysis of PNBDocument73 pagesFinancial Analysis of PNBPrithviNo ratings yet

- 19wj1e0022 Financial Statment Analysis RelianceDocument67 pages19wj1e0022 Financial Statment Analysis RelianceWebsoft Tech-HydNo ratings yet

- FM Assignment1Document25 pagesFM Assignment1Rutuja ValteNo ratings yet

- RatioDocument20 pagesRatioAkashdeep MarwahaNo ratings yet

- FINMANDocument16 pagesFINMANSecret SecretNo ratings yet

- 4c. Financial Ratio AnalysisDocument12 pages4c. Financial Ratio AnalysisOmair AbbasNo ratings yet

- Chapter 1Document53 pagesChapter 1Prashob KoodathilNo ratings yet

- Ratio Analysis.Document3 pagesRatio Analysis.রুবাইয়াত নিবিড়No ratings yet

- Samle 8Document2 pagesSamle 8Mane DaralNo ratings yet

- Ratio AnalysisDocument9 pagesRatio Analysisbharti gupta100% (1)

- Management Accounting Assignment Topic:Ratio Analysis: Room 34Document18 pagesManagement Accounting Assignment Topic:Ratio Analysis: Room 34nuttynehal17100% (1)

- Report On Ratio Analysis ProjectDocument2 pagesReport On Ratio Analysis ProjectYadnesh NikhrgeNo ratings yet

- AFM Project Ratio AnalysisDocument41 pagesAFM Project Ratio AnalysisBharat GhoghariNo ratings yet

- Bilt ProjectDocument124 pagesBilt ProjectMukul BabbarNo ratings yet

- Brand Awairness Cocacola ProjectDocument70 pagesBrand Awairness Cocacola Projectthella deva prasadNo ratings yet

- Brand Awairness Cocacola ProjectDocument70 pagesBrand Awairness Cocacola Projectanikesinght123No ratings yet

- Stability RatioDocument27 pagesStability RatioashokkeeliNo ratings yet

- Synopsis Ratio AnalysisDocument3 pagesSynopsis Ratio Analysisaks_swamiNo ratings yet

- Ratio AnalysisDocument74 pagesRatio AnalysisKarthik NarambatlaNo ratings yet

- Financial Analysis ProjectDocument13 pagesFinancial Analysis ProjectAnonymous NflYP4O100% (1)

- Barkavi Bcom ProjectDocument28 pagesBarkavi Bcom Projectkamalesh kanna kamalesh kannaNo ratings yet

- Ratio AnalysisDocument11 pagesRatio AnalysisNanndita AggarwalNo ratings yet

- Accounting RatiosDocument23 pagesAccounting RatiosPratyush SainiNo ratings yet

- Financial Analysis An IntroductionDocument34 pagesFinancial Analysis An IntroductionnavjeetkumarNo ratings yet

- Ratio Analysis On Optcl, BBSRDocument47 pagesRatio Analysis On Optcl, BBSRSusmita Nayak100% (1)

- Ratio AnalysisDocument4 pagesRatio AnalysisKartikeyaDwivediNo ratings yet

- Financial Statement Analysis Financial Statement Analysis Is A Systematic Process of Identifying The Financial Strengths andDocument7 pagesFinancial Statement Analysis Financial Statement Analysis Is A Systematic Process of Identifying The Financial Strengths andrajivkingofspadesNo ratings yet

- Presentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDDocument12 pagesPresentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDEra ChaudharyNo ratings yet

- FM - Lesson 4 - Fin. Analysis - RatiosDocument8 pagesFM - Lesson 4 - Fin. Analysis - RatiosRena MabinseNo ratings yet

- Definition and Explanation of Financial Statement AnalysisDocument9 pagesDefinition and Explanation of Financial Statement AnalysisadaktanuNo ratings yet

- BHEL FinanceDocument44 pagesBHEL FinanceJayanth C VNo ratings yet

- Ratio AnalysisDocument7 pagesRatio AnalysisShalemRaj100% (1)

- Definition and Explanation of Financial Statement AnalysisDocument7 pagesDefinition and Explanation of Financial Statement Analysismedbest11No ratings yet

- Theoretical PerspectiveDocument12 pagesTheoretical PerspectivepopliyogeshanilNo ratings yet

- Chapter-1-Ratio AnalysisDocument8 pagesChapter-1-Ratio AnalysisRG RAJNo ratings yet

- Analysis of Financial StatementDocument86 pagesAnalysis of Financial StatementSandipan Basu100% (2)

- Meaning of Ratio AnalysisDocument31 pagesMeaning of Ratio AnalysisPrakash Bhanushali100% (1)

- Financial and Accounting Digital Assignment-2Document22 pagesFinancial and Accounting Digital Assignment-2Vignesh ShanmugamNo ratings yet

- Ratio AnalysisDocument21 pagesRatio Analysisindusunkari200No ratings yet

- Financial ANalysis Final ReportDocument70 pagesFinancial ANalysis Final ReportNeha Sable DeshmukhNo ratings yet

- Ratio Analysis ClassDocument20 pagesRatio Analysis ClassRanjith KumarNo ratings yet

- Chapter # 2 Financial AnalysisDocument94 pagesChapter # 2 Financial Analysiswondosen birhanuNo ratings yet

- Introduction Part 123Document11 pagesIntroduction Part 123shaik karishmaNo ratings yet

- Mahesh Total Project 1Document70 pagesMahesh Total Project 1Kaveti Madhu lathaNo ratings yet

- My ProjectDocument72 pagesMy ProjectPrashob Koodathil0% (1)

- AccountsDocument4 pagesAccountsAnita YadavNo ratings yet

- Ratio Analysis NotesDocument9 pagesRatio Analysis Noteshussainnaqvi1194No ratings yet

- Fabm ReviewerDocument3 pagesFabm ReviewerRiguel Jameson AllejeNo ratings yet

- Ratio Analysis NoteDocument7 pagesRatio Analysis NoteVinesh Kumar100% (1)

- Financial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesFrom EverandFinancial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Computer McqsDocument32 pagesComputer McqsDarshan KhatriNo ratings yet

- IslamiyatDocument71 pagesIslamiyatDarshan KhatriNo ratings yet

- EnglishDocument8 pagesEnglishDarshan KhatriNo ratings yet

- Introduction To Business Finance: by MKDocument30 pagesIntroduction To Business Finance: by MKDarshan KhatriNo ratings yet

- Introduction To Business Finance: by MKDocument35 pagesIntroduction To Business Finance: by MKDarshan KhatriNo ratings yet

- Controller General of Accounts: As Per AdvertisementDocument2 pagesController General of Accounts: As Per AdvertisementDarshan KhatriNo ratings yet

- Department of Controller General of Accounts Situations VacantDocument4 pagesDepartment of Controller General of Accounts Situations VacantDarshan KhatriNo ratings yet

- IB Mathematics A&I SL Syllabus Outcomes: Numbers and Algebra Common SLDocument3 pagesIB Mathematics A&I SL Syllabus Outcomes: Numbers and Algebra Common SLLorraine SabbaghNo ratings yet

- PMLS 2 Lesson 1Document4 pagesPMLS 2 Lesson 1Void MelromarcNo ratings yet

- Muslim Army of Jesus & Mahdi & Their 7 SignsDocument13 pagesMuslim Army of Jesus & Mahdi & Their 7 SignsAbdulaziz Khattak Abu FatimaNo ratings yet

- Prepared By: Abhishek Jaiswal (14) Vikram Gupta (19) Gaurav Kumar (21) Ateet Gupta (28) Varun Yadav (47) Siddharth LohoDocument14 pagesPrepared By: Abhishek Jaiswal (14) Vikram Gupta (19) Gaurav Kumar (21) Ateet Gupta (28) Varun Yadav (47) Siddharth LohoateetiimNo ratings yet

- Lecture Notes NanomaterialsDocument34 pagesLecture Notes NanomaterialsEsther Yesudasan67% (3)

- Hiberno-English Powerpoint Feb 2017 PDFDocument24 pagesHiberno-English Powerpoint Feb 2017 PDFceippuigdenvalls100% (1)

- FFT Tutorial: 1 Getting To Know The FFTDocument6 pagesFFT Tutorial: 1 Getting To Know The FFTDavid NasaelNo ratings yet

- GRE Physics Test: Practice BookDocument91 pagesGRE Physics Test: Practice BookGalo CandelaNo ratings yet

- Crime and Punishment British English Teacher Ver2 BWDocument5 pagesCrime and Punishment British English Teacher Ver2 BWinaNo ratings yet

- Product Category LifecyclesDocument13 pagesProduct Category LifecyclesAdam Andrew OngNo ratings yet

- 5 2 ConceptualDocument4 pages5 2 ConceptualArfiNo ratings yet

- COT3 IDocument2 pagesCOT3 IKamsha Uy100% (1)

- Operations Research: Assignment 1Document7 pagesOperations Research: Assignment 1Shashank JainNo ratings yet

- Lesson PlanDocument3 pagesLesson Planapi-530241350No ratings yet

- My Sexual Autobiography Vol 1Document218 pagesMy Sexual Autobiography Vol 1megan fisher50% (2)

- Postgraduate Research Supervision Logbook For SupervisorDocument4 pagesPostgraduate Research Supervision Logbook For SupervisorMuhammad Hilmi bin Abd Rashid Fakulti Pendidikan & Sains Sosial (FPSS)No ratings yet

- 2024 South African Hindu Maha Sabha Calendar Hindu CalenderDocument1 page2024 South African Hindu Maha Sabha Calendar Hindu CalenderAmichand Maraj100% (1)

- Georgios T. Halkias - Richard K. Payne - Ryan Overbey - Anna Andreeva - Robert F. Rhodes - James Apple - Thomas Eijo Dreitlein - Aaron P Proffitt - Charles B. Jones - Fabio Rambelli - Michihi - KopyaDocument808 pagesGeorgios T. Halkias - Richard K. Payne - Ryan Overbey - Anna Andreeva - Robert F. Rhodes - James Apple - Thomas Eijo Dreitlein - Aaron P Proffitt - Charles B. Jones - Fabio Rambelli - Michihi - KopyaHaşim LokmanhekimNo ratings yet

- Renault Twizzy Electric CarDocument114 pagesRenault Twizzy Electric CarsawankuyaNo ratings yet

- (Q2) - Improving The Experience For Software-Measurement System End-UsersDocument25 pages(Q2) - Improving The Experience For Software-Measurement System End-UserscheikhNo ratings yet

- Master EK's Commentary On "Aham Vrkshasya Rerivā " in His Tai.U. Rahasya PrakāsaDocument2 pagesMaster EK's Commentary On "Aham Vrkshasya Rerivā " in His Tai.U. Rahasya PrakāsaBala Subrahmanyam PiratlaNo ratings yet

- Ram Rattan V State of UPDocument8 pagesRam Rattan V State of UPNiveditha Ramakrishnan ThantlaNo ratings yet

- Equipment Reliability AnalysisDocument1 pageEquipment Reliability AnalysisnukkeNo ratings yet

- Violated and Transcended BodiesDocument80 pagesViolated and Transcended BodiesFideblaymid CruzNo ratings yet

- People Vs Rizal (1981)Document21 pagesPeople Vs Rizal (1981)Abigail DeeNo ratings yet

- OralComm Q2 W6 GLAKDocument20 pagesOralComm Q2 W6 GLAKCherryl GallegoNo ratings yet

- Heart Copy of Demonstration-Teaching-Rating-Sheet-ICTDocument3 pagesHeart Copy of Demonstration-Teaching-Rating-Sheet-ICTLouann Heart Lupo100% (1)