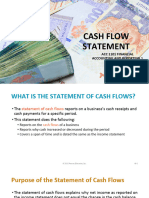

Preparation of Internal and Published Financial Statements

Preparation of Internal and Published Financial Statements

You might also like

- Shoplot Tenancy Agreement 2020: WhereasDocument9 pagesShoplot Tenancy Agreement 2020: WhereasChristine Liew100% (1)

- What is Financial Accounting and BookkeepingFrom EverandWhat is Financial Accounting and BookkeepingRating: 4 out of 5 stars4/5 (10)

- Financial Management:: Understanding Financial Statements, Taxes, and Cash FlowsDocument102 pagesFinancial Management:: Understanding Financial Statements, Taxes, and Cash FlowsArgem Jay PorioNo ratings yet

- Auca Press 1Document15 pagesAuca Press 1Dev DuttNo ratings yet

- 1907 Stevens Cyclopedia of FraternitiesDocument466 pages1907 Stevens Cyclopedia of Fraternitiesal mooreNo ratings yet

- The Adjusting ProcessDocument69 pagesThe Adjusting ProcessDonnie SalazarNo ratings yet

- 03 The Adjusting ProcessDocument68 pages03 The Adjusting Processalice paronNo ratings yet

- CH - 03 (1) 2Document25 pagesCH - 03 (1) 2asd.ksa1090No ratings yet

- Pinto pm5 Inppt 03Document31 pagesPinto pm5 Inppt 03Gabriel Korletey0% (1)

- Nobles Finmgr6 PPT 04 RevisedDocument64 pagesNobles Finmgr6 PPT 04 RevisedzezegallyNo ratings yet

- Lecture 4 PDFDocument60 pagesLecture 4 PDFRachel TamNo ratings yet

- Cost Accounting: Sixteenth Edition, Global EditionDocument32 pagesCost Accounting: Sixteenth Edition, Global EditionAhmed El KhateebNo ratings yet

- pp16Document21 pagespp16David Rivera ArjonaNo ratings yet

- Management and Cost Accounting FundamentalsDocument52 pagesManagement and Cost Accounting FundamentalsDeserie Francisco BaloranNo ratings yet

- pp13 - Ratio AnalysisDocument47 pagespp13 - Ratio AnalysisChristopher MalcolmNo ratings yet

- BUS 142 - Slides Chap 3. The Adjusting ProcessDocument50 pagesBUS 142 - Slides Chap 3. The Adjusting ProcessJess Ica100% (1)

- Topic 8Document36 pagesTopic 8Felicia TangNo ratings yet

- Day-6 Cash FlowsDocument47 pagesDay-6 Cash FlowsRajsri RaajarrathinamNo ratings yet

- The Adjusting Process: © 2016 Pearson Education, LTDDocument53 pagesThe Adjusting Process: © 2016 Pearson Education, LTDEce BarlasNo ratings yet

- CH 11Document31 pagesCH 11HIMANSHU AGRAWALNo ratings yet

- Cost Accounting CombinedDocument143 pagesCost Accounting CombinedNeamat HassanNo ratings yet

- Results Accountability - PPT NotesDocument72 pagesResults Accountability - PPT NotesEmma WongNo ratings yet

- Beams10e Ch04 Consolidation Techniques and ProceduresDocument48 pagesBeams10e Ch04 Consolidation Techniques and Proceduresjeankopler0% (1)

- The Adjusting ProcessDocument51 pagesThe Adjusting ProcessM.Sobhan KasaeiNo ratings yet

- Project ManagementDocument15 pagesProject ManagementminhNo ratings yet

- Financial Accounting: Conceptual FrameworkDocument50 pagesFinancial Accounting: Conceptual Frameworkirma makharoblidzeNo ratings yet

- CH 19Document48 pagesCH 19dichngalinhkietNo ratings yet

- 1.business EnviironmentDocument48 pages1.business EnviironmentAbdelmajid JamaneNo ratings yet

- Financial Accounting: Cash FlowsDocument69 pagesFinancial Accounting: Cash FlowsRachel TamNo ratings yet

- FFE-Unit 1Document98 pagesFFE-Unit 1adityasjadhav2505No ratings yet

- Topik 4 KeuanganDocument68 pagesTopik 4 KeuanganraniNo ratings yet

- Long Term Financial PlanningDocument27 pagesLong Term Financial PlanningKeshav AhujaNo ratings yet

- Mba Financial AssgDocument10 pagesMba Financial Assgseifu deraraNo ratings yet

- School Od Business and Management Institut Teknologi BandungDocument53 pagesSchool Od Business and Management Institut Teknologi BandungadamobirkNo ratings yet

- Byrd PPT Ch14Document38 pagesByrd PPT Ch14Muhammad ImranNo ratings yet

- Accounting in Organization & SocietyDocument8 pagesAccounting in Organization & SocietyLinh Giang Hà0% (1)

- Assignment Brief Management Accounting Unit 5Document15 pagesAssignment Brief Management Accounting Unit 5EngrAbeer Arif67% (12)

- Intermediate Accounting Vol 1 Canadian 3Rd Edition Lo Solutions Manual Full Chapter PDFDocument36 pagesIntermediate Accounting Vol 1 Canadian 3Rd Edition Lo Solutions Manual Full Chapter PDFmarcus.hartley804100% (19)

- Cost Accounting: Sixteenth EditionDocument37 pagesCost Accounting: Sixteenth EditionMohammed S. ZughoulNo ratings yet

- Cha 5 ABC & Activity Based ManagementDocument34 pagesCha 5 ABC & Activity Based ManagementCheng ChengNo ratings yet

- CostAccounting PDFDocument25 pagesCostAccounting PDFAliza Ishra100% (1)

- CHAPTER 23 Performance Measurement, Compensation, and Multinational ConsiderationsDocument32 pagesCHAPTER 23 Performance Measurement, Compensation, and Multinational ConsiderationsSierra.No ratings yet

- Cost Accounting 1Document30 pagesCost Accounting 1Rut LumbantobingNo ratings yet

- Financial Accounting: 1-1 ReservedDocument51 pagesFinancial Accounting: 1-1 ReservedOsiris HernandezNo ratings yet

- Financial Information For Managers Overview of Interpretation Week 5 Dr. Mary NanyondoDocument37 pagesFinancial Information For Managers Overview of Interpretation Week 5 Dr. Mary Nanyondojeff28No ratings yet

- Topic 12 Cashflow StatementDocument34 pagesTopic 12 Cashflow StatementAbd AL Rahman Shah Bin Azlan ShahNo ratings yet

- ch01 (Online Module)Document91 pagesch01 (Online Module)Nazmul Ahshan SawonNo ratings yet

- Topic 3 Accounting For ManagersDocument47 pagesTopic 3 Accounting For ManagersJack BlackNo ratings yet

- CH3 Titman 12eDocument84 pagesCH3 Titman 12elouise carinoNo ratings yet

- Akuntansi Biaya - PPT UAS (Merged)Document182 pagesAkuntansi Biaya - PPT UAS (Merged)Dhanu Alfarizi1No ratings yet

- Murphy ContemporaryLogistics 12e PPT Ch03Document33 pagesMurphy ContemporaryLogistics 12e PPT Ch03Ege GoksuzogluNo ratings yet

- CH 12 Analyzing Financial Statements and Measuring PerformanceDocument79 pagesCH 12 Analyzing Financial Statements and Measuring PerformanceannsuvidavidNo ratings yet

- Cost AccountingDocument25 pagesCost AccountingRizan MohamedNo ratings yet

- Cost Accounting: Sixteenth Edition, Global EditionDocument34 pagesCost Accounting: Sixteenth Edition, Global EditionRania barabaNo ratings yet

- 150 Harrison FAIFRS11e Inppt 04Document43 pages150 Harrison FAIFRS11e Inppt 04irma makharoblidzeNo ratings yet

- C13 Ruchira Papers LTDDocument10 pagesC13 Ruchira Papers LTDRohit DubeyNo ratings yet

- Accounting Theories and ProblemsDocument9 pagesAccounting Theories and ProblemsDonnelly Keith MumarNo ratings yet

- 150 Harrison FAIFRS11e Inppt 03Document55 pages150 Harrison FAIFRS11e Inppt 03irma makharoblidzeNo ratings yet

- FRA DisclosuresDocument25 pagesFRA DisclosuresAishwarya RajeshNo ratings yet

- Topic 3: Project SelectionDocument31 pagesTopic 3: Project Selectionayushi kNo ratings yet

- Bovee Bia8 Inppt 17Document40 pagesBovee Bia8 Inppt 17Usman AliAsifNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Mindanao Development Authority v. CADocument14 pagesMindanao Development Authority v. CAKadzNitura0% (1)

- Last 6 Months RBI in News Part 2 NiharDocument6 pagesLast 6 Months RBI in News Part 2 NiharbuhhbubuhgNo ratings yet

- Modul Berbicara 1Document49 pagesModul Berbicara 1Alif Satuhu100% (1)

- Alejo Carpentier: Cuban Musicologist Latin American Literature "Boom" Period Lausanne Havana CubaDocument19 pagesAlejo Carpentier: Cuban Musicologist Latin American Literature "Boom" Period Lausanne Havana CubaalexcvsNo ratings yet

- Social Science PortfolioDocument2 pagesSocial Science Portfoliorajesh duaNo ratings yet

- KaramuntingDocument14 pagesKaramuntingHaresti MariantoNo ratings yet

- IA 6 Module 5-Edited-CorpuzDocument15 pagesIA 6 Module 5-Edited-CorpuzAngeline AlesnaNo ratings yet

- Sibal Demo TeachingDocument69 pagesSibal Demo TeachingNizeth Jane Macion CuajotorNo ratings yet

- St. Martin vs. LWVDocument2 pagesSt. Martin vs. LWVBaby T. Agcopra100% (5)

- UNIT 8 Types of Punishment For Crimes RedactataDocument17 pagesUNIT 8 Types of Punishment For Crimes Redactataanna825020No ratings yet

- 1423 - MAR - VIDAS - New Mini VIDAS - Version R5.6.0 - Global LaunchDocument21 pages1423 - MAR - VIDAS - New Mini VIDAS - Version R5.6.0 - Global LaunchJunior SallesNo ratings yet

- Soc Psych Research 2Document6 pagesSoc Psych Research 2OSABEL GILLIANNo ratings yet

- BCA - 17UBC4A4 Computer Based Optimization TechniquesDocument16 pagesBCA - 17UBC4A4 Computer Based Optimization Techniquesabhijeetbhojak1No ratings yet

- Advanced Vehicle Technologies, Autonomous Vehicles and CyclingDocument15 pagesAdvanced Vehicle Technologies, Autonomous Vehicles and CyclingGiampaolo PastorinoNo ratings yet

- UK v. Albania (Corfu Channel Case) Use of ForceDocument2 pagesUK v. Albania (Corfu Channel Case) Use of ForceJacob FerrerNo ratings yet

- CIR Vs RhombusDocument2 pagesCIR Vs RhombusKateBarrionEspinosaNo ratings yet

- Carrick-On-Suir, A Glimpse Into Ireland's HistoryDocument13 pagesCarrick-On-Suir, A Glimpse Into Ireland's HistoryPaul JennepinNo ratings yet

- Case Comment On Uttam V Saubhag SinghDocument8 pagesCase Comment On Uttam V Saubhag SinghARJU JAMBHULKARNo ratings yet

- Nguyen Duc Viet-FTU - English CVDocument2 pagesNguyen Duc Viet-FTU - English CVNgô Trí Tuấn AnhNo ratings yet

- Information Before Stay BFDocument7 pagesInformation Before Stay BFBrat SiostraNo ratings yet

- Chapter 2 LAW ON PARTNERSHIPDocument22 pagesChapter 2 LAW ON PARTNERSHIPApril Ann C. GarciaNo ratings yet

- Definition:: Handover NotesDocument3 pagesDefinition:: Handover NotesRalkan KantonNo ratings yet

- Case Study (The Flaundering Expatriate)Document9 pagesCase Study (The Flaundering Expatriate)Pratima SrivastavaNo ratings yet

- Social Essay - ObreroDocument5 pagesSocial Essay - ObreroMarian Camille ObreroNo ratings yet

- De Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2Document21 pagesDe Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2mit maiNo ratings yet

- Maix BitDocument2 pagesMaix BitloborisNo ratings yet

- Latihan Soal Chapter 7 Kelas ViiiDocument3 pagesLatihan Soal Chapter 7 Kelas ViiiChalwa AnjumitaNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Shoplot Tenancy Agreement 2020: WhereasDocument9 pagesShoplot Tenancy Agreement 2020: WhereasChristine Liew100% (1)

- What is Financial Accounting and BookkeepingFrom EverandWhat is Financial Accounting and BookkeepingRating: 4 out of 5 stars4/5 (10)

- Financial Management:: Understanding Financial Statements, Taxes, and Cash FlowsDocument102 pagesFinancial Management:: Understanding Financial Statements, Taxes, and Cash FlowsArgem Jay PorioNo ratings yet

- Auca Press 1Document15 pagesAuca Press 1Dev DuttNo ratings yet

- 1907 Stevens Cyclopedia of FraternitiesDocument466 pages1907 Stevens Cyclopedia of Fraternitiesal mooreNo ratings yet

- The Adjusting ProcessDocument69 pagesThe Adjusting ProcessDonnie SalazarNo ratings yet

- 03 The Adjusting ProcessDocument68 pages03 The Adjusting Processalice paronNo ratings yet

- CH - 03 (1) 2Document25 pagesCH - 03 (1) 2asd.ksa1090No ratings yet

- Pinto pm5 Inppt 03Document31 pagesPinto pm5 Inppt 03Gabriel Korletey0% (1)

- Nobles Finmgr6 PPT 04 RevisedDocument64 pagesNobles Finmgr6 PPT 04 RevisedzezegallyNo ratings yet

- Lecture 4 PDFDocument60 pagesLecture 4 PDFRachel TamNo ratings yet

- Cost Accounting: Sixteenth Edition, Global EditionDocument32 pagesCost Accounting: Sixteenth Edition, Global EditionAhmed El KhateebNo ratings yet

- pp16Document21 pagespp16David Rivera ArjonaNo ratings yet

- Management and Cost Accounting FundamentalsDocument52 pagesManagement and Cost Accounting FundamentalsDeserie Francisco BaloranNo ratings yet

- pp13 - Ratio AnalysisDocument47 pagespp13 - Ratio AnalysisChristopher MalcolmNo ratings yet

- BUS 142 - Slides Chap 3. The Adjusting ProcessDocument50 pagesBUS 142 - Slides Chap 3. The Adjusting ProcessJess Ica100% (1)

- Topic 8Document36 pagesTopic 8Felicia TangNo ratings yet

- Day-6 Cash FlowsDocument47 pagesDay-6 Cash FlowsRajsri RaajarrathinamNo ratings yet

- The Adjusting Process: © 2016 Pearson Education, LTDDocument53 pagesThe Adjusting Process: © 2016 Pearson Education, LTDEce BarlasNo ratings yet

- CH 11Document31 pagesCH 11HIMANSHU AGRAWALNo ratings yet

- Cost Accounting CombinedDocument143 pagesCost Accounting CombinedNeamat HassanNo ratings yet

- Results Accountability - PPT NotesDocument72 pagesResults Accountability - PPT NotesEmma WongNo ratings yet

- Beams10e Ch04 Consolidation Techniques and ProceduresDocument48 pagesBeams10e Ch04 Consolidation Techniques and Proceduresjeankopler0% (1)

- The Adjusting ProcessDocument51 pagesThe Adjusting ProcessM.Sobhan KasaeiNo ratings yet

- Project ManagementDocument15 pagesProject ManagementminhNo ratings yet

- Financial Accounting: Conceptual FrameworkDocument50 pagesFinancial Accounting: Conceptual Frameworkirma makharoblidzeNo ratings yet

- CH 19Document48 pagesCH 19dichngalinhkietNo ratings yet

- 1.business EnviironmentDocument48 pages1.business EnviironmentAbdelmajid JamaneNo ratings yet

- Financial Accounting: Cash FlowsDocument69 pagesFinancial Accounting: Cash FlowsRachel TamNo ratings yet

- FFE-Unit 1Document98 pagesFFE-Unit 1adityasjadhav2505No ratings yet

- Topik 4 KeuanganDocument68 pagesTopik 4 KeuanganraniNo ratings yet

- Long Term Financial PlanningDocument27 pagesLong Term Financial PlanningKeshav AhujaNo ratings yet

- Mba Financial AssgDocument10 pagesMba Financial Assgseifu deraraNo ratings yet

- School Od Business and Management Institut Teknologi BandungDocument53 pagesSchool Od Business and Management Institut Teknologi BandungadamobirkNo ratings yet

- Byrd PPT Ch14Document38 pagesByrd PPT Ch14Muhammad ImranNo ratings yet

- Accounting in Organization & SocietyDocument8 pagesAccounting in Organization & SocietyLinh Giang Hà0% (1)

- Assignment Brief Management Accounting Unit 5Document15 pagesAssignment Brief Management Accounting Unit 5EngrAbeer Arif67% (12)

- Intermediate Accounting Vol 1 Canadian 3Rd Edition Lo Solutions Manual Full Chapter PDFDocument36 pagesIntermediate Accounting Vol 1 Canadian 3Rd Edition Lo Solutions Manual Full Chapter PDFmarcus.hartley804100% (19)

- Cost Accounting: Sixteenth EditionDocument37 pagesCost Accounting: Sixteenth EditionMohammed S. ZughoulNo ratings yet

- Cha 5 ABC & Activity Based ManagementDocument34 pagesCha 5 ABC & Activity Based ManagementCheng ChengNo ratings yet

- CostAccounting PDFDocument25 pagesCostAccounting PDFAliza Ishra100% (1)

- CHAPTER 23 Performance Measurement, Compensation, and Multinational ConsiderationsDocument32 pagesCHAPTER 23 Performance Measurement, Compensation, and Multinational ConsiderationsSierra.No ratings yet

- Cost Accounting 1Document30 pagesCost Accounting 1Rut LumbantobingNo ratings yet

- Financial Accounting: 1-1 ReservedDocument51 pagesFinancial Accounting: 1-1 ReservedOsiris HernandezNo ratings yet

- Financial Information For Managers Overview of Interpretation Week 5 Dr. Mary NanyondoDocument37 pagesFinancial Information For Managers Overview of Interpretation Week 5 Dr. Mary Nanyondojeff28No ratings yet

- Topic 12 Cashflow StatementDocument34 pagesTopic 12 Cashflow StatementAbd AL Rahman Shah Bin Azlan ShahNo ratings yet

- ch01 (Online Module)Document91 pagesch01 (Online Module)Nazmul Ahshan SawonNo ratings yet

- Topic 3 Accounting For ManagersDocument47 pagesTopic 3 Accounting For ManagersJack BlackNo ratings yet

- CH3 Titman 12eDocument84 pagesCH3 Titman 12elouise carinoNo ratings yet

- Akuntansi Biaya - PPT UAS (Merged)Document182 pagesAkuntansi Biaya - PPT UAS (Merged)Dhanu Alfarizi1No ratings yet

- Murphy ContemporaryLogistics 12e PPT Ch03Document33 pagesMurphy ContemporaryLogistics 12e PPT Ch03Ege GoksuzogluNo ratings yet

- CH 12 Analyzing Financial Statements and Measuring PerformanceDocument79 pagesCH 12 Analyzing Financial Statements and Measuring PerformanceannsuvidavidNo ratings yet

- Cost AccountingDocument25 pagesCost AccountingRizan MohamedNo ratings yet

- Cost Accounting: Sixteenth Edition, Global EditionDocument34 pagesCost Accounting: Sixteenth Edition, Global EditionRania barabaNo ratings yet

- 150 Harrison FAIFRS11e Inppt 04Document43 pages150 Harrison FAIFRS11e Inppt 04irma makharoblidzeNo ratings yet

- C13 Ruchira Papers LTDDocument10 pagesC13 Ruchira Papers LTDRohit DubeyNo ratings yet

- Accounting Theories and ProblemsDocument9 pagesAccounting Theories and ProblemsDonnelly Keith MumarNo ratings yet

- 150 Harrison FAIFRS11e Inppt 03Document55 pages150 Harrison FAIFRS11e Inppt 03irma makharoblidzeNo ratings yet

- FRA DisclosuresDocument25 pagesFRA DisclosuresAishwarya RajeshNo ratings yet

- Topic 3: Project SelectionDocument31 pagesTopic 3: Project Selectionayushi kNo ratings yet

- Bovee Bia8 Inppt 17Document40 pagesBovee Bia8 Inppt 17Usman AliAsifNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Mindanao Development Authority v. CADocument14 pagesMindanao Development Authority v. CAKadzNitura0% (1)

- Last 6 Months RBI in News Part 2 NiharDocument6 pagesLast 6 Months RBI in News Part 2 NiharbuhhbubuhgNo ratings yet

- Modul Berbicara 1Document49 pagesModul Berbicara 1Alif Satuhu100% (1)

- Alejo Carpentier: Cuban Musicologist Latin American Literature "Boom" Period Lausanne Havana CubaDocument19 pagesAlejo Carpentier: Cuban Musicologist Latin American Literature "Boom" Period Lausanne Havana CubaalexcvsNo ratings yet

- Social Science PortfolioDocument2 pagesSocial Science Portfoliorajesh duaNo ratings yet

- KaramuntingDocument14 pagesKaramuntingHaresti MariantoNo ratings yet

- IA 6 Module 5-Edited-CorpuzDocument15 pagesIA 6 Module 5-Edited-CorpuzAngeline AlesnaNo ratings yet

- Sibal Demo TeachingDocument69 pagesSibal Demo TeachingNizeth Jane Macion CuajotorNo ratings yet

- St. Martin vs. LWVDocument2 pagesSt. Martin vs. LWVBaby T. Agcopra100% (5)

- UNIT 8 Types of Punishment For Crimes RedactataDocument17 pagesUNIT 8 Types of Punishment For Crimes Redactataanna825020No ratings yet

- 1423 - MAR - VIDAS - New Mini VIDAS - Version R5.6.0 - Global LaunchDocument21 pages1423 - MAR - VIDAS - New Mini VIDAS - Version R5.6.0 - Global LaunchJunior SallesNo ratings yet

- Soc Psych Research 2Document6 pagesSoc Psych Research 2OSABEL GILLIANNo ratings yet

- BCA - 17UBC4A4 Computer Based Optimization TechniquesDocument16 pagesBCA - 17UBC4A4 Computer Based Optimization Techniquesabhijeetbhojak1No ratings yet

- Advanced Vehicle Technologies, Autonomous Vehicles and CyclingDocument15 pagesAdvanced Vehicle Technologies, Autonomous Vehicles and CyclingGiampaolo PastorinoNo ratings yet

- UK v. Albania (Corfu Channel Case) Use of ForceDocument2 pagesUK v. Albania (Corfu Channel Case) Use of ForceJacob FerrerNo ratings yet

- CIR Vs RhombusDocument2 pagesCIR Vs RhombusKateBarrionEspinosaNo ratings yet

- Carrick-On-Suir, A Glimpse Into Ireland's HistoryDocument13 pagesCarrick-On-Suir, A Glimpse Into Ireland's HistoryPaul JennepinNo ratings yet

- Case Comment On Uttam V Saubhag SinghDocument8 pagesCase Comment On Uttam V Saubhag SinghARJU JAMBHULKARNo ratings yet

- Nguyen Duc Viet-FTU - English CVDocument2 pagesNguyen Duc Viet-FTU - English CVNgô Trí Tuấn AnhNo ratings yet

- Information Before Stay BFDocument7 pagesInformation Before Stay BFBrat SiostraNo ratings yet

- Chapter 2 LAW ON PARTNERSHIPDocument22 pagesChapter 2 LAW ON PARTNERSHIPApril Ann C. GarciaNo ratings yet

- Definition:: Handover NotesDocument3 pagesDefinition:: Handover NotesRalkan KantonNo ratings yet

- Case Study (The Flaundering Expatriate)Document9 pagesCase Study (The Flaundering Expatriate)Pratima SrivastavaNo ratings yet

- Social Essay - ObreroDocument5 pagesSocial Essay - ObreroMarian Camille ObreroNo ratings yet

- De Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2Document21 pagesDe Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2mit maiNo ratings yet

- Maix BitDocument2 pagesMaix BitloborisNo ratings yet

- Latihan Soal Chapter 7 Kelas ViiiDocument3 pagesLatihan Soal Chapter 7 Kelas ViiiChalwa AnjumitaNo ratings yet