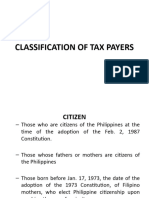

Lesson 2 Taxation of Individuals

Lesson 2 Taxation of Individuals

You might also like

- Thesis Format and StyleDocument56 pagesThesis Format and StyleQuenie De la CruzNo ratings yet

- Bill HotelDocument54 pagesBill Hotelidhul bram sakti100% (1)

- Advance ITT Exam 1 Day Revision Notes Module Ii Unit 1 - Advanced Excel Chapter 1 - Working With XMLDocument23 pagesAdvance ITT Exam 1 Day Revision Notes Module Ii Unit 1 - Advanced Excel Chapter 1 - Working With XMLvanshika agarwal75% (4)

- Handout 3Document51 pagesHandout 3Jilian Kate Alpapara Bustamante100% (1)

- Income Taxation Lecture Notes.5.Classifications of Individual TaxpayersDocument5 pagesIncome Taxation Lecture Notes.5.Classifications of Individual Taxpayerseinel dc100% (1)

- Reviewer Chapter 2Document6 pagesReviewer Chapter 2Ken NavarroNo ratings yet

- Module 2 - Functions of BSPDocument14 pagesModule 2 - Functions of BSPQuenie De la CruzNo ratings yet

- Rel11 FSCM RPD DB Mapping SCMDocument96 pagesRel11 FSCM RPD DB Mapping SCMAnonymous STmh9rbfKNo ratings yet

- Deloitte Annual Review of Football Finance (2014)Document10 pagesDeloitte Annual Review of Football Finance (2014)Tifoso BilanciatoNo ratings yet

- 2019 FY NCAA Budget Report FAUDocument79 pages2019 FY NCAA Budget Report FAUMatt BrownNo ratings yet

- Chapter 23 Solutions Manual ExamDocument15 pagesChapter 23 Solutions Manual ExamMariance Romaulina Malau67% (3)

- Classification of Tax PayersDocument24 pagesClassification of Tax PayersHilarie JeanNo ratings yet

- Prelim Income TaxationDocument55 pagesPrelim Income TaxationclytemnestraNo ratings yet

- Introduction To Individual Income Taxation Chapter Overview and ObjectivesDocument25 pagesIntroduction To Individual Income Taxation Chapter Overview and ObjectivesMatta, Jherrie MaeNo ratings yet

- What Are The Kinds of TaxpayersDocument4 pagesWhat Are The Kinds of TaxpayersALee Bud100% (1)

- 20240313T061944584 Att 908654264076627Document113 pages20240313T061944584 Att 908654264076627klee042697No ratings yet

- Template Taxation Unit IIDocument29 pagesTemplate Taxation Unit IINacion, Jaime G.No ratings yet

- MODULE 5 Individual TaxationDocument3 pagesMODULE 5 Individual TaxationCEDRICK MARX ABRIGARNo ratings yet

- Introduction To Income Taxation - 625041052Document21 pagesIntroduction To Income Taxation - 625041052ANGELA JOY FLORESNo ratings yet

- Income Tax For IndividualsDocument90 pagesIncome Tax For IndividualsRubyjane Kim100% (1)

- (TAX) Income Taxation Updated Jan 9 2022Document133 pages(TAX) Income Taxation Updated Jan 9 2022Reginald ValenciaNo ratings yet

- Chapter 2 Income TaxationDocument31 pagesChapter 2 Income TaxationRieven BaracinasNo ratings yet

- Individual Taxpayers (Ordinary Income and Fringe Benefits)Document86 pagesIndividual Taxpayers (Ordinary Income and Fringe Benefits)ipbsalanguitNo ratings yet

- TAX-5.0 - Individual Income TaxDocument65 pagesTAX-5.0 - Individual Income TaxCharmaine RosalesNo ratings yet

- Train Individual INCOME TAXDocument48 pagesTrain Individual INCOME TAXMeireen Ann100% (2)

- Classification of Individual Taxpayers - AlienDocument32 pagesClassification of Individual Taxpayers - AlienMarria FrancezcaNo ratings yet

- 3 - Income Tax On IndividualsDocument22 pages3 - Income Tax On IndividualsRylleMatthanCorderoNo ratings yet

- Taxation of IndividualsDocument49 pagesTaxation of IndividualsAnastasha Grey100% (1)

- M2u Classification Individual Taxation P1Document30 pagesM2u Classification Individual Taxation P1Xehdrickke FernandezNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- Classification of Individual TaxpayerDocument31 pagesClassification of Individual TaxpayerPatrick BituinNo ratings yet

- TAX Reviewer FINALSDocument9 pagesTAX Reviewer FINALSLalaine SantiagoNo ratings yet

- Handout TaxationDocument2 pagesHandout TaxationJohn Oicemen RocaNo ratings yet

- Types of Income Tax PayersDocument3 pagesTypes of Income Tax PayersAce Fati-igNo ratings yet

- Types of TaxpayerDocument23 pagesTypes of TaxpayerReina Rose LebrillaNo ratings yet

- Inroduction To Income TaxationDocument20 pagesInroduction To Income TaxationW-304-Bautista,PreciousNo ratings yet

- Income Taxation Week 3Document20 pagesIncome Taxation Week 3Hannah Rae ChingNo ratings yet

- Basergo, Lovers Mae B. General Classification of Individual TaxpayersDocument2 pagesBasergo, Lovers Mae B. General Classification of Individual Taxpayerslavender kayeNo ratings yet

- Income Recognition, Measurement and Reporting and Taxpayer ClassificationsDocument27 pagesIncome Recognition, Measurement and Reporting and Taxpayer ClassificationsAries Queencel Bernante BocarNo ratings yet

- Tax 1 MidtermsDocument18 pagesTax 1 MidtermsElaine Yap100% (1)

- 2 Classification of Individual TaxpayersDocument2 pages2 Classification of Individual TaxpayersDiana SheineNo ratings yet

- Individual ItDocument12 pagesIndividual ItlouellasoleilgpNo ratings yet

- Income Taxation IndividualsDocument19 pagesIncome Taxation IndividualsJenniNo ratings yet

- Citizenship FINALDocument88 pagesCitizenship FINALBek AhNo ratings yet

- Lesson 5 Inclusions Exclusions From Gi Final TaxDocument17 pagesLesson 5 Inclusions Exclusions From Gi Final TaxOrduna Mae AnnNo ratings yet

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- Classification of Individual TaxpayerDocument4 pagesClassification of Individual TaxpayerJj helterbrandNo ratings yet

- HO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Document5 pagesHO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Erine ContranoNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErvin Ray FernandezNo ratings yet

- Classification of TaxpayersDocument1 pageClassification of Taxpayersskyle meniaNo ratings yet

- Introduction To Income TaxationDocument3 pagesIntroduction To Income TaxationescrowNo ratings yet

- Assignment 2Document2 pagesAssignment 2Caroline Dy DimakilingNo ratings yet

- Income Tax On Individuals PDFDocument20 pagesIncome Tax On Individuals PDFKaren Joy MagsayoNo ratings yet

- SRRVDocument25 pagesSRRVMhatet Malanum Tagulinao-TongcoNo ratings yet

- 3PO1 U1L2 PreTest Q5 - General Principles of Taxation - Tax LawsDocument1 page3PO1 U1L2 PreTest Q5 - General Principles of Taxation - Tax LawsKimberly MartinezNo ratings yet

- Chapter 2Document9 pagesChapter 2Sheilamae Sernadilla GregorioNo ratings yet

- Classification of Individual Income TaxpayersDocument3 pagesClassification of Individual Income TaxpayersOdessa De JesusNo ratings yet

- Taxation of IndividualsDocument9 pagesTaxation of IndividualsBrielle GabNo ratings yet

- Citizenship and Residency Inside RP Outside RPDocument2 pagesCitizenship and Residency Inside RP Outside RPRhea Royce CabuhatNo ratings yet

- Tax601 Individual Itx Lecture Notes 122Document12 pagesTax601 Individual Itx Lecture Notes 122Justine JaymaNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- Summary Lesson 4Document6 pagesSummary Lesson 4Janien MedestomasNo ratings yet

- 2nd Semester Income Taxation Module 5 Classification of TaxpayersDocument5 pages2nd Semester Income Taxation Module 5 Classification of TaxpayersMaryrose SumulongNo ratings yet

- Tax-Review-Handouts-INDV FWT CGT FBT EST PDFDocument34 pagesTax-Review-Handouts-INDV FWT CGT FBT EST PDFMarinella Oppa100% (1)

- Gross Income (Classification of Taxpayers)Document12 pagesGross Income (Classification of Taxpayers)Michael Thom MacabuhayNo ratings yet

- Income Tax ConDocument2 pagesIncome Tax ConMaricon EstradaNo ratings yet

- Executive BrieferDocument1 pageExecutive BrieferQuenie De la CruzNo ratings yet

- BOARD RESOLUTION TablasDocument6 pagesBOARD RESOLUTION TablasQuenie De la CruzNo ratings yet

- Monitoring List of Potential ClientsDocument1 pageMonitoring List of Potential ClientsQuenie De la CruzNo ratings yet

- Cultural Heritage Tourism LBT Paper 2020 David Ketz Anne Ketz 1Document18 pagesCultural Heritage Tourism LBT Paper 2020 David Ketz Anne Ketz 1Quenie De la CruzNo ratings yet

- Validation Letter (Edited)Document1 pageValidation Letter (Edited)Quenie De la CruzNo ratings yet

- Q2 2023-EndDocument77 pagesQ2 2023-EndQuenie De la CruzNo ratings yet

- Survey Form QuestionnairesDocument3 pagesSurvey Form QuestionnairesQuenie De la CruzNo ratings yet

- Importance of Technology in Facilitating Learning - Jasper M. VillanuevaDocument2 pagesImportance of Technology in Facilitating Learning - Jasper M. VillanuevaQuenie De la CruzNo ratings yet

- EI THESIS Need To CritiqueDocument72 pagesEI THESIS Need To CritiqueQuenie De la CruzNo ratings yet

- Letter For SurveyDocument1 pageLetter For SurveyQuenie De la CruzNo ratings yet

- Thesis Group-30Document41 pagesThesis Group-30Quenie De la CruzNo ratings yet

- Thesis Template EIDocument22 pagesThesis Template EIQuenie De la CruzNo ratings yet

- Art Appreciation - Module 2 - Week 2Document7 pagesArt Appreciation - Module 2 - Week 2Quenie De la CruzNo ratings yet

- List of Gov. Universities in Western Visayas With PresidentsDocument2 pagesList of Gov. Universities in Western Visayas With PresidentsQuenie De la CruzNo ratings yet

- Excuse LetterDocument1 pageExcuse LetterQuenie De la CruzNo ratings yet

- EI Questionnaires For ValidationDocument4 pagesEI Questionnaires For ValidationQuenie De la CruzNo ratings yet

- Brochure LalalaDocument2 pagesBrochure LalalaQuenie De la CruzNo ratings yet

- MKTG 1 - Q1 - 2022 - 8-9 (Responses)Document2 pagesMKTG 1 - Q1 - 2022 - 8-9 (Responses)Quenie De la CruzNo ratings yet

- Module 1 (Chapter 1&2)Document29 pagesModule 1 (Chapter 1&2)Quenie De la CruzNo ratings yet

- Exercise 5 VATDocument3 pagesExercise 5 VATQuenie De la CruzNo ratings yet

- BAA 222 SyllabusDocument7 pagesBAA 222 SyllabusQuenie De la CruzNo ratings yet

- Art Appreciation - Module 1 - Week 1Document15 pagesArt Appreciation - Module 1 - Week 1Quenie De la CruzNo ratings yet

- Compilation of TheoriesDocument15 pagesCompilation of TheoriesQuenie De la Cruz100% (1)

- Chapter 8-Zero Rated SalesDocument8 pagesChapter 8-Zero Rated SalesQuenie De la CruzNo ratings yet

- Quiz - Horizontal AnalysisDocument2 pagesQuiz - Horizontal AnalysisQuenie De la CruzNo ratings yet

- Chapter 4-Reviewing The LiteratureDocument11 pagesChapter 4-Reviewing The LiteratureQuenie De la CruzNo ratings yet

- Chapter 7-Regular Output VATDocument9 pagesChapter 7-Regular Output VATQuenie De la CruzNo ratings yet

- Exercise 2-Chapter 3-Intro To Business TaxationDocument3 pagesExercise 2-Chapter 3-Intro To Business TaxationQuenie De la CruzNo ratings yet

- Fa 102Document20 pagesFa 102Apeksha ChilwalNo ratings yet

- CCRA Final Brochure PDFDocument4 pagesCCRA Final Brochure PDFYogesh LassiNo ratings yet

- MCQ Financial Regulatory FrameworkDocument13 pagesMCQ Financial Regulatory FrameworkNaziya TamboliNo ratings yet

- Firefighter Matrix1Document16 pagesFirefighter Matrix1Leanne FernandesNo ratings yet

- JetBlue Airways IPO ValuationDocument16 pagesJetBlue Airways IPO ValuationDerek Levesque100% (2)

- Chapter 1 Simple Interest and Simple DiscountDocument38 pagesChapter 1 Simple Interest and Simple DiscountAbe Miguel BullecerNo ratings yet

- RTP Dec 18 QNDocument21 pagesRTP Dec 18 QNbinu100% (1)

- Ci-Hqd 0405Document1 pageCi-Hqd 0405Juan Carlos Canarte LeonNo ratings yet

- Project Report On Microfinance in IndiaDocument5 pagesProject Report On Microfinance in Indiaakanksha3No ratings yet

- Certificate of Increase in Capital Stock-Sample FormDocument2 pagesCertificate of Increase in Capital Stock-Sample FormvenaphaniaglysdimungcalNo ratings yet

- Gross IncomeDocument68 pagesGross IncomeNour Aira NaoNo ratings yet

- Narsipatnam Municipality: Form DDocument2 pagesNarsipatnam Municipality: Form Dvikas pallaNo ratings yet

- New Microsoft Office Word DocumentDocument4 pagesNew Microsoft Office Word DocumentMilan KakkadNo ratings yet

- Cfa WMN SCHLRSHPDocument1 pageCfa WMN SCHLRSHPAditi ParvathamNo ratings yet

- Experience Letter FormatDocument1 pageExperience Letter FormatEng Muhammad Afzal AlmaniNo ratings yet

- Capital Structure: Limits To The: Use of DebtDocument9 pagesCapital Structure: Limits To The: Use of DebtArini FalahiyahNo ratings yet

- IAC PPE and Intangible Students FinalDocument4 pagesIAC PPE and Intangible Students FinalJoyce Cagayat100% (1)

- Role of Government and RBI in Money Market - IndianMoneyDocument10 pagesRole of Government and RBI in Money Market - IndianMoneyKushNo ratings yet

- Challenge Bankruptcy Lift Automatic StayDocument9 pagesChallenge Bankruptcy Lift Automatic StayTeresa WattersNo ratings yet

- Jonaxx Trading Corporation 1ST PageDocument1 pageJonaxx Trading Corporation 1ST PageRona Karylle Pamaran DeCastroNo ratings yet

- Turkish Republic of Northern Cyprus: GreeceDocument3 pagesTurkish Republic of Northern Cyprus: GreeceMarNo ratings yet

- Part 2: True/False Questions (Short Explanation Is Required) (2 Marks)Document13 pagesPart 2: True/False Questions (Short Explanation Is Required) (2 Marks)Trần Lâm PhươngNo ratings yet

- Finance Sensitivity Analysis PDFDocument6 pagesFinance Sensitivity Analysis PDFontykerlsNo ratings yet

- SAP Dunning Procedure ConfigurationDocument5 pagesSAP Dunning Procedure ConfigurationPallavi ChawlaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Thesis Format and StyleDocument56 pagesThesis Format and StyleQuenie De la CruzNo ratings yet

- Bill HotelDocument54 pagesBill Hotelidhul bram sakti100% (1)

- Advance ITT Exam 1 Day Revision Notes Module Ii Unit 1 - Advanced Excel Chapter 1 - Working With XMLDocument23 pagesAdvance ITT Exam 1 Day Revision Notes Module Ii Unit 1 - Advanced Excel Chapter 1 - Working With XMLvanshika agarwal75% (4)

- Handout 3Document51 pagesHandout 3Jilian Kate Alpapara Bustamante100% (1)

- Income Taxation Lecture Notes.5.Classifications of Individual TaxpayersDocument5 pagesIncome Taxation Lecture Notes.5.Classifications of Individual Taxpayerseinel dc100% (1)

- Reviewer Chapter 2Document6 pagesReviewer Chapter 2Ken NavarroNo ratings yet

- Module 2 - Functions of BSPDocument14 pagesModule 2 - Functions of BSPQuenie De la CruzNo ratings yet

- Rel11 FSCM RPD DB Mapping SCMDocument96 pagesRel11 FSCM RPD DB Mapping SCMAnonymous STmh9rbfKNo ratings yet

- Deloitte Annual Review of Football Finance (2014)Document10 pagesDeloitte Annual Review of Football Finance (2014)Tifoso BilanciatoNo ratings yet

- 2019 FY NCAA Budget Report FAUDocument79 pages2019 FY NCAA Budget Report FAUMatt BrownNo ratings yet

- Chapter 23 Solutions Manual ExamDocument15 pagesChapter 23 Solutions Manual ExamMariance Romaulina Malau67% (3)

- Classification of Tax PayersDocument24 pagesClassification of Tax PayersHilarie JeanNo ratings yet

- Prelim Income TaxationDocument55 pagesPrelim Income TaxationclytemnestraNo ratings yet

- Introduction To Individual Income Taxation Chapter Overview and ObjectivesDocument25 pagesIntroduction To Individual Income Taxation Chapter Overview and ObjectivesMatta, Jherrie MaeNo ratings yet

- What Are The Kinds of TaxpayersDocument4 pagesWhat Are The Kinds of TaxpayersALee Bud100% (1)

- 20240313T061944584 Att 908654264076627Document113 pages20240313T061944584 Att 908654264076627klee042697No ratings yet

- Template Taxation Unit IIDocument29 pagesTemplate Taxation Unit IINacion, Jaime G.No ratings yet

- MODULE 5 Individual TaxationDocument3 pagesMODULE 5 Individual TaxationCEDRICK MARX ABRIGARNo ratings yet

- Introduction To Income Taxation - 625041052Document21 pagesIntroduction To Income Taxation - 625041052ANGELA JOY FLORESNo ratings yet

- Income Tax For IndividualsDocument90 pagesIncome Tax For IndividualsRubyjane Kim100% (1)

- (TAX) Income Taxation Updated Jan 9 2022Document133 pages(TAX) Income Taxation Updated Jan 9 2022Reginald ValenciaNo ratings yet

- Chapter 2 Income TaxationDocument31 pagesChapter 2 Income TaxationRieven BaracinasNo ratings yet

- Individual Taxpayers (Ordinary Income and Fringe Benefits)Document86 pagesIndividual Taxpayers (Ordinary Income and Fringe Benefits)ipbsalanguitNo ratings yet

- TAX-5.0 - Individual Income TaxDocument65 pagesTAX-5.0 - Individual Income TaxCharmaine RosalesNo ratings yet

- Train Individual INCOME TAXDocument48 pagesTrain Individual INCOME TAXMeireen Ann100% (2)

- Classification of Individual Taxpayers - AlienDocument32 pagesClassification of Individual Taxpayers - AlienMarria FrancezcaNo ratings yet

- 3 - Income Tax On IndividualsDocument22 pages3 - Income Tax On IndividualsRylleMatthanCorderoNo ratings yet

- Taxation of IndividualsDocument49 pagesTaxation of IndividualsAnastasha Grey100% (1)

- M2u Classification Individual Taxation P1Document30 pagesM2u Classification Individual Taxation P1Xehdrickke FernandezNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- Classification of Individual TaxpayerDocument31 pagesClassification of Individual TaxpayerPatrick BituinNo ratings yet

- TAX Reviewer FINALSDocument9 pagesTAX Reviewer FINALSLalaine SantiagoNo ratings yet

- Handout TaxationDocument2 pagesHandout TaxationJohn Oicemen RocaNo ratings yet

- Types of Income Tax PayersDocument3 pagesTypes of Income Tax PayersAce Fati-igNo ratings yet

- Types of TaxpayerDocument23 pagesTypes of TaxpayerReina Rose LebrillaNo ratings yet

- Inroduction To Income TaxationDocument20 pagesInroduction To Income TaxationW-304-Bautista,PreciousNo ratings yet

- Income Taxation Week 3Document20 pagesIncome Taxation Week 3Hannah Rae ChingNo ratings yet

- Basergo, Lovers Mae B. General Classification of Individual TaxpayersDocument2 pagesBasergo, Lovers Mae B. General Classification of Individual Taxpayerslavender kayeNo ratings yet

- Income Recognition, Measurement and Reporting and Taxpayer ClassificationsDocument27 pagesIncome Recognition, Measurement and Reporting and Taxpayer ClassificationsAries Queencel Bernante BocarNo ratings yet

- Tax 1 MidtermsDocument18 pagesTax 1 MidtermsElaine Yap100% (1)

- 2 Classification of Individual TaxpayersDocument2 pages2 Classification of Individual TaxpayersDiana SheineNo ratings yet

- Individual ItDocument12 pagesIndividual ItlouellasoleilgpNo ratings yet

- Income Taxation IndividualsDocument19 pagesIncome Taxation IndividualsJenniNo ratings yet

- Citizenship FINALDocument88 pagesCitizenship FINALBek AhNo ratings yet

- Lesson 5 Inclusions Exclusions From Gi Final TaxDocument17 pagesLesson 5 Inclusions Exclusions From Gi Final TaxOrduna Mae AnnNo ratings yet

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- Classification of Individual TaxpayerDocument4 pagesClassification of Individual TaxpayerJj helterbrandNo ratings yet

- HO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Document5 pagesHO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Erine ContranoNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErvin Ray FernandezNo ratings yet

- Classification of TaxpayersDocument1 pageClassification of Taxpayersskyle meniaNo ratings yet

- Introduction To Income TaxationDocument3 pagesIntroduction To Income TaxationescrowNo ratings yet

- Assignment 2Document2 pagesAssignment 2Caroline Dy DimakilingNo ratings yet

- Income Tax On Individuals PDFDocument20 pagesIncome Tax On Individuals PDFKaren Joy MagsayoNo ratings yet

- SRRVDocument25 pagesSRRVMhatet Malanum Tagulinao-TongcoNo ratings yet

- 3PO1 U1L2 PreTest Q5 - General Principles of Taxation - Tax LawsDocument1 page3PO1 U1L2 PreTest Q5 - General Principles of Taxation - Tax LawsKimberly MartinezNo ratings yet

- Chapter 2Document9 pagesChapter 2Sheilamae Sernadilla GregorioNo ratings yet

- Classification of Individual Income TaxpayersDocument3 pagesClassification of Individual Income TaxpayersOdessa De JesusNo ratings yet

- Taxation of IndividualsDocument9 pagesTaxation of IndividualsBrielle GabNo ratings yet

- Citizenship and Residency Inside RP Outside RPDocument2 pagesCitizenship and Residency Inside RP Outside RPRhea Royce CabuhatNo ratings yet

- Tax601 Individual Itx Lecture Notes 122Document12 pagesTax601 Individual Itx Lecture Notes 122Justine JaymaNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- Summary Lesson 4Document6 pagesSummary Lesson 4Janien MedestomasNo ratings yet

- 2nd Semester Income Taxation Module 5 Classification of TaxpayersDocument5 pages2nd Semester Income Taxation Module 5 Classification of TaxpayersMaryrose SumulongNo ratings yet

- Tax-Review-Handouts-INDV FWT CGT FBT EST PDFDocument34 pagesTax-Review-Handouts-INDV FWT CGT FBT EST PDFMarinella Oppa100% (1)

- Gross Income (Classification of Taxpayers)Document12 pagesGross Income (Classification of Taxpayers)Michael Thom MacabuhayNo ratings yet

- Income Tax ConDocument2 pagesIncome Tax ConMaricon EstradaNo ratings yet

- Executive BrieferDocument1 pageExecutive BrieferQuenie De la CruzNo ratings yet

- BOARD RESOLUTION TablasDocument6 pagesBOARD RESOLUTION TablasQuenie De la CruzNo ratings yet

- Monitoring List of Potential ClientsDocument1 pageMonitoring List of Potential ClientsQuenie De la CruzNo ratings yet

- Cultural Heritage Tourism LBT Paper 2020 David Ketz Anne Ketz 1Document18 pagesCultural Heritage Tourism LBT Paper 2020 David Ketz Anne Ketz 1Quenie De la CruzNo ratings yet

- Validation Letter (Edited)Document1 pageValidation Letter (Edited)Quenie De la CruzNo ratings yet

- Q2 2023-EndDocument77 pagesQ2 2023-EndQuenie De la CruzNo ratings yet

- Survey Form QuestionnairesDocument3 pagesSurvey Form QuestionnairesQuenie De la CruzNo ratings yet

- Importance of Technology in Facilitating Learning - Jasper M. VillanuevaDocument2 pagesImportance of Technology in Facilitating Learning - Jasper M. VillanuevaQuenie De la CruzNo ratings yet

- EI THESIS Need To CritiqueDocument72 pagesEI THESIS Need To CritiqueQuenie De la CruzNo ratings yet

- Letter For SurveyDocument1 pageLetter For SurveyQuenie De la CruzNo ratings yet

- Thesis Group-30Document41 pagesThesis Group-30Quenie De la CruzNo ratings yet

- Thesis Template EIDocument22 pagesThesis Template EIQuenie De la CruzNo ratings yet

- Art Appreciation - Module 2 - Week 2Document7 pagesArt Appreciation - Module 2 - Week 2Quenie De la CruzNo ratings yet

- List of Gov. Universities in Western Visayas With PresidentsDocument2 pagesList of Gov. Universities in Western Visayas With PresidentsQuenie De la CruzNo ratings yet

- Excuse LetterDocument1 pageExcuse LetterQuenie De la CruzNo ratings yet

- EI Questionnaires For ValidationDocument4 pagesEI Questionnaires For ValidationQuenie De la CruzNo ratings yet

- Brochure LalalaDocument2 pagesBrochure LalalaQuenie De la CruzNo ratings yet

- MKTG 1 - Q1 - 2022 - 8-9 (Responses)Document2 pagesMKTG 1 - Q1 - 2022 - 8-9 (Responses)Quenie De la CruzNo ratings yet

- Module 1 (Chapter 1&2)Document29 pagesModule 1 (Chapter 1&2)Quenie De la CruzNo ratings yet

- Exercise 5 VATDocument3 pagesExercise 5 VATQuenie De la CruzNo ratings yet

- BAA 222 SyllabusDocument7 pagesBAA 222 SyllabusQuenie De la CruzNo ratings yet

- Art Appreciation - Module 1 - Week 1Document15 pagesArt Appreciation - Module 1 - Week 1Quenie De la CruzNo ratings yet

- Compilation of TheoriesDocument15 pagesCompilation of TheoriesQuenie De la Cruz100% (1)

- Chapter 8-Zero Rated SalesDocument8 pagesChapter 8-Zero Rated SalesQuenie De la CruzNo ratings yet

- Quiz - Horizontal AnalysisDocument2 pagesQuiz - Horizontal AnalysisQuenie De la CruzNo ratings yet

- Chapter 4-Reviewing The LiteratureDocument11 pagesChapter 4-Reviewing The LiteratureQuenie De la CruzNo ratings yet

- Chapter 7-Regular Output VATDocument9 pagesChapter 7-Regular Output VATQuenie De la CruzNo ratings yet

- Exercise 2-Chapter 3-Intro To Business TaxationDocument3 pagesExercise 2-Chapter 3-Intro To Business TaxationQuenie De la CruzNo ratings yet

- Fa 102Document20 pagesFa 102Apeksha ChilwalNo ratings yet

- CCRA Final Brochure PDFDocument4 pagesCCRA Final Brochure PDFYogesh LassiNo ratings yet

- MCQ Financial Regulatory FrameworkDocument13 pagesMCQ Financial Regulatory FrameworkNaziya TamboliNo ratings yet

- Firefighter Matrix1Document16 pagesFirefighter Matrix1Leanne FernandesNo ratings yet

- JetBlue Airways IPO ValuationDocument16 pagesJetBlue Airways IPO ValuationDerek Levesque100% (2)

- Chapter 1 Simple Interest and Simple DiscountDocument38 pagesChapter 1 Simple Interest and Simple DiscountAbe Miguel BullecerNo ratings yet

- RTP Dec 18 QNDocument21 pagesRTP Dec 18 QNbinu100% (1)

- Ci-Hqd 0405Document1 pageCi-Hqd 0405Juan Carlos Canarte LeonNo ratings yet

- Project Report On Microfinance in IndiaDocument5 pagesProject Report On Microfinance in Indiaakanksha3No ratings yet

- Certificate of Increase in Capital Stock-Sample FormDocument2 pagesCertificate of Increase in Capital Stock-Sample FormvenaphaniaglysdimungcalNo ratings yet

- Gross IncomeDocument68 pagesGross IncomeNour Aira NaoNo ratings yet

- Narsipatnam Municipality: Form DDocument2 pagesNarsipatnam Municipality: Form Dvikas pallaNo ratings yet

- New Microsoft Office Word DocumentDocument4 pagesNew Microsoft Office Word DocumentMilan KakkadNo ratings yet

- Cfa WMN SCHLRSHPDocument1 pageCfa WMN SCHLRSHPAditi ParvathamNo ratings yet

- Experience Letter FormatDocument1 pageExperience Letter FormatEng Muhammad Afzal AlmaniNo ratings yet

- Capital Structure: Limits To The: Use of DebtDocument9 pagesCapital Structure: Limits To The: Use of DebtArini FalahiyahNo ratings yet

- IAC PPE and Intangible Students FinalDocument4 pagesIAC PPE and Intangible Students FinalJoyce Cagayat100% (1)

- Role of Government and RBI in Money Market - IndianMoneyDocument10 pagesRole of Government and RBI in Money Market - IndianMoneyKushNo ratings yet

- Challenge Bankruptcy Lift Automatic StayDocument9 pagesChallenge Bankruptcy Lift Automatic StayTeresa WattersNo ratings yet

- Jonaxx Trading Corporation 1ST PageDocument1 pageJonaxx Trading Corporation 1ST PageRona Karylle Pamaran DeCastroNo ratings yet

- Turkish Republic of Northern Cyprus: GreeceDocument3 pagesTurkish Republic of Northern Cyprus: GreeceMarNo ratings yet

- Part 2: True/False Questions (Short Explanation Is Required) (2 Marks)Document13 pagesPart 2: True/False Questions (Short Explanation Is Required) (2 Marks)Trần Lâm PhươngNo ratings yet

- Finance Sensitivity Analysis PDFDocument6 pagesFinance Sensitivity Analysis PDFontykerlsNo ratings yet

- SAP Dunning Procedure ConfigurationDocument5 pagesSAP Dunning Procedure ConfigurationPallavi ChawlaNo ratings yet