Download as pptx, pdf, or txt

You might also like

- Prudential SurrenderDocument5 pagesPrudential SurrenderBriltex IndustriesNo ratings yet

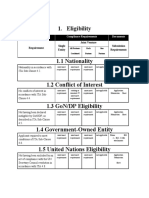

- Eligibility: Criteria Compliance Requirements DocumentsDocument2 pagesEligibility: Criteria Compliance Requirements DocumentsRameshNo ratings yet

- Ister On Thursday, August 17, 2006 (71Document1 pageIster On Thursday, August 17, 2006 (71IRSNo ratings yet

- Iii. Negotiable Instruments Law (Act No. 2031)Document4 pagesIii. Negotiable Instruments Law (Act No. 2031)A SNo ratings yet

- 2019 Tax Rev Finals Digests PDFDocument178 pages2019 Tax Rev Finals Digests PDFDooNo ratings yet

- 21 53 Solved Scanner Cs Executive Programme Module II Economic and Labour Law Part A June 2009Document10 pages21 53 Solved Scanner Cs Executive Programme Module II Economic and Labour Law Part A June 2009mbeadarshNo ratings yet

- FR OID Annuities 98-20Document6 pagesFR OID Annuities 98-20Theplaymaker508No ratings yet

- Nidhi-Amendment 2019-20Document12 pagesNidhi-Amendment 2019-20Manoj KumarNo ratings yet

- The Foreign Worker Recruitment and Immigration Services RegulationsDocument12 pagesThe Foreign Worker Recruitment and Immigration Services RegulationsaghowelNo ratings yet

- Real Estate and Business Agents (General) Regulations 1979 - (08-g0-03)Document51 pagesReal Estate and Business Agents (General) Regulations 1979 - (08-g0-03)Anonymous I5hdhuCxNo ratings yet

- Fem 17Document599 pagesFem 17arti deviNo ratings yet

- Tax 2Document19 pagesTax 2SNLTNo ratings yet

- Instructions For Filling Out FORM ITR-2Document7 pagesInstructions For Filling Out FORM ITR-2haryy1234567No ratings yet

- Judge ChecklistDocument14 pagesJudge ChecklistVbs ReddyNo ratings yet

- MIFIDPRU 7 Annex 5R Notification Under MIFIDPRU 7.7.14R in Relation To Level of Liquid AssetsDocument2 pagesMIFIDPRU 7 Annex 5R Notification Under MIFIDPRU 7.7.14R in Relation To Level of Liquid AssetsTrung PhanNo ratings yet

- Residential TenanciesDocument20 pagesResidential TenanciesDylan PowellNo ratings yet

- Qualification Criteria (Fast Track 9B)Document5 pagesQualification Criteria (Fast Track 9B)Sarrows PrazzapatiNo ratings yet

- Instructions For Form 1042-SDocument37 pagesInstructions For Form 1042-SWalter GuttlerNo ratings yet

- 2.1.4 Occupiers' LiabilityDocument9 pages2.1.4 Occupiers' LiabilityRomsamBlaNo ratings yet

- Frontline AR 2009Document136 pagesFrontline AR 2009Shawn LaiNo ratings yet

- Taxation 2 Course Outline Midterms DraftDocument6 pagesTaxation 2 Course Outline Midterms DraftIra Francia AlcazarNo ratings yet

- BanktruptcyDocument18 pagesBanktruptcycarahulsaxena2000No ratings yet

- Chapter 11 - CARO 2016Document1 pageChapter 11 - CARO 2016Tax Payer100% (1)

- Chapter 8 - Companies (Auditor's Report) Order, 2016Document1 pageChapter 8 - Companies (Auditor's Report) Order, 2016saikrupaNo ratings yet

- (Vol IX), 2017 Rules For Single Point Mooring, 2017Document76 pages(Vol IX), 2017 Rules For Single Point Mooring, 2017ije ajeNo ratings yet

- Reg Section 1.937-1Document13 pagesReg Section 1.937-1EDC AdminNo ratings yet

- Form10 PDFDocument4 pagesForm10 PDFJuliet LalonneNo ratings yet

- Tax 1 - Outline (Gross Income and Income Tax) Part1Document6 pagesTax 1 - Outline (Gross Income and Income Tax) Part1Katrina Marie OraldeNo ratings yet

- Conformed To Federal Register VersionDocument163 pagesConformed To Federal Register VersionRituraj ParmarNo ratings yet

- U.S. Mortgage Loan AgreementDocument111 pagesU.S. Mortgage Loan Agreement6qhgf978svNo ratings yet

- Agriculture Law: 12-01Document11 pagesAgriculture Law: 12-01AgricultureCaseLawNo ratings yet

- Analysis of Return Final Rules 05.06.2017Document32 pagesAnalysis of Return Final Rules 05.06.2017rajanraorajanNo ratings yet

- NegoDocument6 pagesNegoArnel MangilimanNo ratings yet

- 18-154 SR 001Document28 pages18-154 SR 001beechezparisNo ratings yet

- lc270 Limitation of ActionsDocument318 pageslc270 Limitation of ActionsJames LomasNo ratings yet

- Final A-V Section of Nh-8 - RFQDocument70 pagesFinal A-V Section of Nh-8 - RFQrps_78No ratings yet

- Nationa Credit Act FormsDocument114 pagesNationa Credit Act FormsrodystjamesNo ratings yet

- Form 8-K: Current Report Pursuant To Section 13 OR 15 (D) of The Securities Exchange Act of 1934Document22 pagesForm 8-K: Current Report Pursuant To Section 13 OR 15 (D) of The Securities Exchange Act of 1934g6hNo ratings yet

- IT Act With Master Guide To Income Tax ActDocument22 pagesIT Act With Master Guide To Income Tax ActManoj RaghavNo ratings yet

- Week 5 Law On Other Business TransactionsDocument1 pageWeek 5 Law On Other Business TransactionsSyrille ClementineNo ratings yet

- Letter Compendium KG KGA ENDocument12 pagesLetter Compendium KG KGA ENKhamed TabetNo ratings yet

- Form 8-K: Current Report Pursuant To Section 13 OR 15 (D) of The Securities Exchange Act of 1934Document22 pagesForm 8-K: Current Report Pursuant To Section 13 OR 15 (D) of The Securities Exchange Act of 1934IsaacCorralesNo ratings yet

- Monitoring Policy of IIIPI 18th Jan 2019Document19 pagesMonitoring Policy of IIIPI 18th Jan 2019Payal DubeyNo ratings yet

- CPWA CODE 101-150 (Guide Part 4) PDFDocument15 pagesCPWA CODE 101-150 (Guide Part 4) PDFshekarj80% (5)

- Self-Employed Mortgage Access ActDocument3 pagesSelf-Employed Mortgage Access ActMarkWarner0% (1)

- Rishabh 239Document1 pageRishabh 239Anikate SharmaNo ratings yet

- UP Law Tax 2 Syllabus Estate TaxDocument6 pagesUP Law Tax 2 Syllabus Estate TaxGRNo ratings yet

- Investor Focus: Taxpert Professionals Private LimitedDocument7 pagesInvestor Focus: Taxpert Professionals Private LimitedTaxpert mukeshNo ratings yet

- Fidelity Savings & Investment Co. v. New Hope Baptist Robert Stone Jeffrey Alan Dietert, 880 F.2d 1172, 10th Cir. (1989)Document9 pagesFidelity Savings & Investment Co. v. New Hope Baptist Robert Stone Jeffrey Alan Dietert, 880 F.2d 1172, 10th Cir. (1989)Scribd Government DocsNo ratings yet

- Federal Register-02-28544Document2 pagesFederal Register-02-28544POTUSNo ratings yet

- Adobe Scan 03 Oct 2023Document16 pagesAdobe Scan 03 Oct 2023acgstdiv4No ratings yet

- US Internal Revenue Service: I3468 - 1996Document3 pagesUS Internal Revenue Service: I3468 - 1996IRSNo ratings yet

- EoI RFQ For Development of Visakhapatnam Metro Rail ProjectDocument91 pagesEoI RFQ For Development of Visakhapatnam Metro Rail Projectkmmanoj1968No ratings yet

- MPEP E8r7 - 0200 - Types, Cross-Noting, & StatusDocument108 pagesMPEP E8r7 - 0200 - Types, Cross-Noting, & StatusespSCRIBDNo ratings yet

- US Internal Revenue Service: 20070801fDocument7 pagesUS Internal Revenue Service: 20070801fIRSNo ratings yet

- Salient Features of The Industrial Disputes Act, 1947: M.L.PandiaDocument85 pagesSalient Features of The Industrial Disputes Act, 1947: M.L.PandiaVaibhav GangwarNo ratings yet

- BA Cbap Application Worksheet TemplateDocument10 pagesBA Cbap Application Worksheet TemplateVitalii LiakhNo ratings yet

- Technical SpecificationsDocument9 pagesTechnical SpecificationsVitalii LiakhNo ratings yet

- Functional SpecificationDocument5 pagesFunctional SpecificationVitalii LiakhNo ratings yet

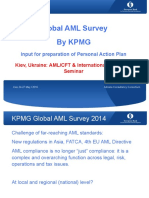

- EBRD - KPMG Study KievDocument20 pagesEBRD - KPMG Study KievVitalii LiakhNo ratings yet

- EBRD - REV Anti Corruption and PEPs KIEV 2016Document35 pagesEBRD - REV Anti Corruption and PEPs KIEV 2016Vitalii LiakhNo ratings yet

- EBRD Practical Exercise 1 - Kiev 1Document2 pagesEBRD Practical Exercise 1 - Kiev 1Vitalii LiakhNo ratings yet

- EBRD - Anti Corruption and PEPs KIEV 2016Document36 pagesEBRD - Anti Corruption and PEPs KIEV 2016Vitalii LiakhNo ratings yet

- EBRD - Intl Standards 1st Group KIEVDocument20 pagesEBRD - Intl Standards 1st Group KIEVVitalii LiakhNo ratings yet

- Sanctions Individuals Russia UkraineDocument10 pagesSanctions Individuals Russia UkraineVitalii LiakhNo ratings yet

- EBRD - Intl Standards KIEVDocument26 pagesEBRD - Intl Standards KIEVVitalii LiakhNo ratings yet

- 060 FATCA - QI Compliance PolicyDocument16 pages060 FATCA - QI Compliance PolicyVitalii LiakhNo ratings yet

- Crimea AdvisoryDocument2 pagesCrimea AdvisoryVitalii LiakhNo ratings yet

- W-9 Ukr: Request For Taxpayer Identification Number and CertificationDocument1 pageW-9 Ukr: Request For Taxpayer Identification Number and CertificationVitalii LiakhNo ratings yet

- Code of Conduct "Universal Bank" Regarding Banking Secrecy, Staff Transactions, Staff Conflict of Interest EtcDocument22 pagesCode of Conduct "Universal Bank" Regarding Banking Secrecy, Staff Transactions, Staff Conflict of Interest EtcVitalii LiakhNo ratings yet

- PWC FATCA Newsbrief Overview 02.27.12Document20 pagesPWC FATCA Newsbrief Overview 02.27.12Vitalii LiakhNo ratings yet

- Credit Card Application Supplementary CardsDocument1 pageCredit Card Application Supplementary CardsLANo ratings yet

- Info Update Form Aug2016Document3 pagesInfo Update Form Aug2016Kate PotinganNo ratings yet

- Fatca - NSDL Non Ind. V. 21.3 (PG 1-4)Document4 pagesFatca - NSDL Non Ind. V. 21.3 (PG 1-4)digitaltarun99No ratings yet

- Annex UreaDocument184 pagesAnnex UreasaravananNo ratings yet

- FATCA QuestionnaireDocument1 pageFATCA Questionnaireblue606No ratings yet

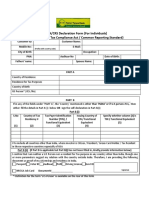

- 4.fatca Self Declaraton Form Individuals PDFDocument2 pages4.fatca Self Declaraton Form Individuals PDFbala krishnanNo ratings yet

- FW 8 BenDocument1 pageFW 8 BenMario Vargas HerreraNo ratings yet

- Form Submitted Using OTP Authentication (Through Email and Mobile)Document6 pagesForm Submitted Using OTP Authentication (Through Email and Mobile)News Side Effects.No ratings yet

- Very ImportantDocument17 pagesVery ImportantpradeebhaNo ratings yet

- Thawte SSL Web Server CertificatesDocument5 pagesThawte SSL Web Server CertificatesalirezaNo ratings yet

- w9 PDFDocument4 pagesw9 PDFoceanic23No ratings yet

- DBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002Document4 pagesDBS Bank India Limited Ground Floor, Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-66388888 DBSS0IN0811 400641002Isana SatishNo ratings yet

- Kotak Securities NRI AccountDocument6 pagesKotak Securities NRI AccountRohit JoshiNo ratings yet

- Fatca Form NewDocument1 pageFatca Form NewgaurdevNo ratings yet

- CP - Digital Service List and Other InfoDocument23 pagesCP - Digital Service List and Other InfoTerry wei shengNo ratings yet

- 13-01-02 Letter To Bank Hapoalim, BM, Chief Internal Auditor Jacob Orbach Re: Blocking of Customer's Accounts, Failure To Produce Bank DocumentsDocument1 page13-01-02 Letter To Bank Hapoalim, BM, Chief Internal Auditor Jacob Orbach Re: Blocking of Customer's Accounts, Failure To Produce Bank DocumentsSELA - Human Rights Alert - IsraelNo ratings yet

- FATCA-CRS Declaration & Supplementary KYC Information: Declaration Form For EntitiesDocument6 pagesFATCA-CRS Declaration & Supplementary KYC Information: Declaration Form For Entitiesvikas9saraswatNo ratings yet

- Request For Change of Existing Resident Account To Nro AccountDocument4 pagesRequest For Change of Existing Resident Account To Nro Accountviraj duaNo ratings yet

- Tax HavenDocument16 pagesTax HavenAbdellahBouzelmadNo ratings yet

- Application Form: Systematic Transfer Plan (STP), Systematic Withdrawal Plan (SWP)Document2 pagesApplication Form: Systematic Transfer Plan (STP), Systematic Withdrawal Plan (SWP)Chintan JainNo ratings yet

- T24 Induction Business - Customer - R14Document47 pagesT24 Induction Business - Customer - R14Developer T240% (1)

- Application Form: Systematic Transfer Plan (STP), Systematic Withdrawal Plan (SWP)Document2 pagesApplication Form: Systematic Transfer Plan (STP), Systematic Withdrawal Plan (SWP)Gargi ShuklaNo ratings yet

- Factiva 20191022 1021 PDFDocument2 pagesFactiva 20191022 1021 PDFAnonymous tTk3g8No ratings yet

- 2 Compliance Questionnaire STANDARDDocument3 pages2 Compliance Questionnaire STANDARDchung elaineNo ratings yet

- ICICI Equity & DEBT Form With Auto Debit FormDocument2 pagesICICI Equity & DEBT Form With Auto Debit FormSaurabh JainNo ratings yet

- Electronic W8 (E-W8) FactsheetDocument1 pageElectronic W8 (E-W8) FactsheetFelix ChanNo ratings yet

- RinggitPlus Application Form GRGPWB0916Document4 pagesRinggitPlus Application Form GRGPWB0916Pang Jia WoeiNo ratings yet

- HDFC Application FormDocument5 pagesHDFC Application FormMuukund ChikeralliNo ratings yet

- S1FormDocument5 pagesS1FormShantanu ManeNo ratings yet