Download as ppt, pdf, or txt

You might also like

- Ma1 Mock Test 1Document5 pagesMa1 Mock Test 1Vinh Ngo Nhu83% (12)

- Strat Cost 8-24Document4 pagesStrat Cost 8-24Vivienne Rozenn LaytoNo ratings yet

- Vicenzo Bernard Leandro Tioriman - 01011182025009Document6 pagesVicenzo Bernard Leandro Tioriman - 01011182025009ImVicNo ratings yet

- Akb Tugas Ke 3Document6 pagesAkb Tugas Ke 3mekarNo ratings yet

- BIAYA: Konsep, Klasifikasi Dan PerilakuDocument48 pagesBIAYA: Konsep, Klasifikasi Dan PerilakuAziz SugihartoNo ratings yet

- Lecture 05Document19 pagesLecture 05Mahnoor AzizNo ratings yet

- BIAYA: Konsep, Klasifikasi Dan PerilakuDocument38 pagesBIAYA: Konsep, Klasifikasi Dan PerilakuNetta MonicaNo ratings yet

- Lec 3 Konsep Dan Klasifikasi BiayaDocument33 pagesLec 3 Konsep Dan Klasifikasi BiayaMochamad PutraNo ratings yet

- 2 - Cost Terms Concepts and Classifications - EtudiantDocument38 pages2 - Cost Terms Concepts and Classifications - EtudiantheniosyoutubeNo ratings yet

- Chapter 2Document31 pagesChapter 2Syeda SamiaNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument54 pagesCosts Terms, Concepts and Classifications: Chapter TwosanosyNo ratings yet

- Chapter 2Document29 pagesChapter 2bhagyeshparekh.caNo ratings yet

- Chapter 3Document40 pagesChapter 3Korubel Asegdew YimenuNo ratings yet

- LECT # 3 - Cost Flow & COGSDocument35 pagesLECT # 3 - Cost Flow & COGSmuhammad.16483.acNo ratings yet

- PDF Document 3Document112 pagesPDF Document 3Yarka Buuqa Neceb MuuseNo ratings yet

- Chapter Two: Cost Terms, Concepts and ClassificationsDocument72 pagesChapter Two: Cost Terms, Concepts and ClassificationsYuvaraj SubramaniamNo ratings yet

- Cost Accounting Part 1Document21 pagesCost Accounting Part 1Mostafa ElgendyNo ratings yet

- Chapter 1 - Manufacturing AccountDocument32 pagesChapter 1 - Manufacturing AccountNORZAIHA BINTI ALI MoeNo ratings yet

- BIAYA: Konsep, Klasifikasi Dan PerilakuDocument44 pagesBIAYA: Konsep, Klasifikasi Dan PerilakuAlit SanjayaaNo ratings yet

- ACCO 330 - COMM 305 ReviewDocument33 pagesACCO 330 - COMM 305 ReviewJiedan HuangNo ratings yet

- Xcostcon Cost Accounting CycleDocument14 pagesXcostcon Cost Accounting Cycleabrylle opinianoNo ratings yet

- CH # 08 CompleteDocument28 pagesCH # 08 CompleteMuhammad Kashif HayatNo ratings yet

- Understanding Costs For Management Decisions: Uaa - Acct 650 Seminar in Executive Uses of Accounting Dr. Fred BarbeeDocument92 pagesUnderstanding Costs For Management Decisions: Uaa - Acct 650 Seminar in Executive Uses of Accounting Dr. Fred BarbeeAhmed RazaNo ratings yet

- Lec1 IntroDocument57 pagesLec1 Intronathan panNo ratings yet

- Basic Costing Principles and Manufacturing Concerns PresentationDocument16 pagesBasic Costing Principles and Manufacturing Concerns Presentationzinhlezwane2708No ratings yet

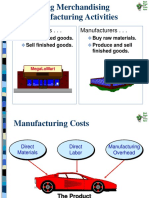

- Comparing Merchandising and ManufacturingDocument14 pagesComparing Merchandising and ManufacturingOna MaeNo ratings yet

- Principles of Cost AccountingDocument28 pagesPrinciples of Cost AccountingKristine AlonzoNo ratings yet

- Chapter 1 - Cost Term, Concept and ClassificationDocument55 pagesChapter 1 - Cost Term, Concept and ClassificationMolla Shoyeb Uddin MithuNo ratings yet

- Cost Terminology and Cost BehaviorsDocument45 pagesCost Terminology and Cost BehaviorsJoyce Anne GarduqueNo ratings yet

- Financial Reporting by Manufacturing Companies: Chapter No. 6Document9 pagesFinancial Reporting by Manufacturing Companies: Chapter No. 6hhaiderNo ratings yet

- Lecture 02Document79 pagesLecture 02chiuchuiyingccyNo ratings yet

- Principles of Cost Accounting 14EDocument30 pagesPrinciples of Cost Accounting 14Etegegn mogessieNo ratings yet

- What Is Cost AccountingDocument165 pagesWhat Is Cost AccountingUy SamuelNo ratings yet

- CH 2 Cost Concepts and BehaviorDocument36 pagesCH 2 Cost Concepts and BehaviorYunita LalaNo ratings yet

- COST OF GOODS MANUFACTURED AND SOLD BarrosDocument8 pagesCOST OF GOODS MANUFACTURED AND SOLD BarrosJINKY TOLENTINONo ratings yet

- Cost Concepts AssignmentDocument4 pagesCost Concepts AssignmentInageaNo ratings yet

- Management Accounting Chapter 4Document53 pagesManagement Accounting Chapter 4yimer100% (1)

- SPPTChap 002Document25 pagesSPPTChap 002Abdulaziz ObaidNo ratings yet

- Chapter 1 - Manufacturing Account (I)Document16 pagesChapter 1 - Manufacturing Account (I)NG JIA LUNGNo ratings yet

- Cost AnalysisDocument36 pagesCost AnalysisHarisagar ThulasiramanNo ratings yet

- 6un44rh0q - Cost Accounting and ControlDocument75 pages6un44rh0q - Cost Accounting and ControlJustine Marie BalderasNo ratings yet

- 02 - Cost Terms Concepts ClassificationsDocument50 pages02 - Cost Terms Concepts ClassificationsGovinda Gde Phillips39No ratings yet

- MA1 T2 MD Cost Terms Concepts and ClassificationsDocument113 pagesMA1 T2 MD Cost Terms Concepts and ClassificationsMae Ciarie YangcoNo ratings yet

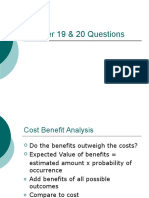

- Chapter 19 & 20 QuestionsDocument10 pagesChapter 19 & 20 Questionsfaizal rizkiNo ratings yet

- Garrison Lecture Chapter 2 - Cost ConceptsDocument80 pagesGarrison Lecture Chapter 2 - Cost Conceptsnahid mushtaqNo ratings yet

- Sesi 2 Akuntansi Manajemen - Rev1Document32 pagesSesi 2 Akuntansi Manajemen - Rev1Dian Permata SariNo ratings yet

- Group 1 - Managerial Accounting and Cost ConceptsDocument47 pagesGroup 1 - Managerial Accounting and Cost ConceptsJeejohn SodustaNo ratings yet

- MQE Cost Acctg Session 1Document78 pagesMQE Cost Acctg Session 1Frances Monique Alburo0% (1)

- 2a. Job Order Costing CRDocument17 pages2a. Job Order Costing CRAnaly Omandac PelayoNo ratings yet

- ACC104 - Job Order Costing - For PostingDocument22 pagesACC104 - Job Order Costing - For PostingYesha SibayanNo ratings yet

- Cost SampleDocument10 pagesCost SampleparulvijayNo ratings yet

- Sesi 2 Akuntansi ManajemenDocument33 pagesSesi 2 Akuntansi ManajemenDian Permata SariNo ratings yet

- Management Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakDocument58 pagesManagement Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakSiddharthNo ratings yet

- Lecture 06Document32 pagesLecture 06Mahnoor AzizNo ratings yet

- Hamsta - Direct Labour and FOHDocument21 pagesHamsta - Direct Labour and FOHHamstaNo ratings yet

- Cost AccountingDocument17 pagesCost AccountingFaisal RafiqNo ratings yet

- MM140 - Unit II - Costs and PricingDocument34 pagesMM140 - Unit II - Costs and PricingFranz Hendrix GagarinNo ratings yet

- Basic Cost Terms and ConceptsDocument8 pagesBasic Cost Terms and Conceptstegegn mogessieNo ratings yet

- Chapter 02Document57 pagesChapter 02Adam AbdullahiNo ratings yet

- Pengelompokan BiayaDocument17 pagesPengelompokan BiayaMaya BangunNo ratings yet

- Basic Cost Terms and ConceptsDocument8 pagesBasic Cost Terms and Conceptstegegn mogessieNo ratings yet

- Chapter 02Document17 pagesChapter 02Arshia EmamiNo ratings yet

- Chapter 2-Cost Terminology and Cost Behaviors: True/FalseDocument34 pagesChapter 2-Cost Terminology and Cost Behaviors: True/FalseKristan John ZernaNo ratings yet

- Cost Concepts and Analysis PDFDocument17 pagesCost Concepts and Analysis PDFHansNo ratings yet

- Master Budget Practice Quiz Questions W My NotesDocument14 pagesMaster Budget Practice Quiz Questions W My NoteswhinzielynarmendiNo ratings yet

- Product CostDocument10 pagesProduct CostApple BaldemoroNo ratings yet

- Chapter 18Document35 pagesChapter 18Mariechi Binuya100% (1)

- MGT402 Assignment No 1 Solution12Document2 pagesMGT402 Assignment No 1 Solution12Muhammad Tayyab IshaqNo ratings yet

- Application Form For Business Loans: Aquaculture Seed Fund-Youth Empowerment Initiative 2020Document7 pagesApplication Form For Business Loans: Aquaculture Seed Fund-Youth Empowerment Initiative 2020muhammadkamaraNo ratings yet

- Markstrat Sample ReportDocument29 pagesMarkstrat Sample Reportananth080864No ratings yet

- Inventories, Biological Assets, Etc.Document3 pagesInventories, Biological Assets, Etc.Jobelle Candace Flores AbreraNo ratings yet

- Mock Final Exam S2023Document15 pagesMock Final Exam S2023Charlotte GillandersNo ratings yet

- Product and Service DesignDocument10 pagesProduct and Service DesignNisar AhmadNo ratings yet

- Cpar Practical Accounting Ii Problems Oct 2010 Final Pre Board W SolutionsDocument14 pagesCpar Practical Accounting Ii Problems Oct 2010 Final Pre Board W SolutionsKyla MilanNo ratings yet

- Chapter 1 Introduction To Cost AccountingDocument42 pagesChapter 1 Introduction To Cost AccountingPotato FriesNo ratings yet

- 6 - JIT Manufacturing and Lean AccountingDocument40 pages6 - JIT Manufacturing and Lean AccountingJovelle AlcoberNo ratings yet

- Flash MemoryDocument14 pagesFlash MemoryPranav TatavarthiNo ratings yet

- ABM2 Q1 Mod3 Statement of Comprehensive Income Multi StepDocument27 pagesABM2 Q1 Mod3 Statement of Comprehensive Income Multi StepLeigh GuittapNo ratings yet

- Lecture 5 - Management Accounting Anf Cost Concepts - Terms and ClassificationsDocument29 pagesLecture 5 - Management Accounting Anf Cost Concepts - Terms and ClassificationsOphelia MensahNo ratings yet

- Fsa Assignment 1 PDFDocument19 pagesFsa Assignment 1 PDFMUHAMMAD UMARNo ratings yet

- Chapter 7 - ProblemsDocument10 pagesChapter 7 - ProblemsfltimbangNo ratings yet

- Mas Drills Weeks 1-7 & DiagnosticDocument56 pagesMas Drills Weeks 1-7 & DiagnosticMitch MinglanaNo ratings yet

- A Level Accounting NotesDocument16 pagesA Level Accounting NotesChaiwatTippuwananNo ratings yet

- Quiz 3 Cost AccountingDocument2 pagesQuiz 3 Cost AccountingRocel DomingoNo ratings yet

- Ascuncion InventoriesDocument22 pagesAscuncion InventoriesKendrew SujideNo ratings yet

- Chapter 02Document53 pagesChapter 02Vanitha ThiagarajNo ratings yet

- ACC100 Midterm - Winter 2012 - FINAL SOLUTION - StudentDocument7 pagesACC100 Midterm - Winter 2012 - FINAL SOLUTION - Studentseville240% (1)

- InventoriesDocument62 pagesInventoriesdwi studyNo ratings yet

- Ratio Analysis of TafeDocument56 pagesRatio Analysis of TafeGourav AoliyaNo ratings yet