Download as pptx, pdf, or txt

You might also like

- 100 Q&A of GCE O'Level Economics 2281Document32 pages100 Q&A of GCE O'Level Economics 2281Hassan Asghar100% (4)

- The Ultimate Guide To Drum Programming - EDMProdDocument32 pagesThe Ultimate Guide To Drum Programming - EDMProdSteveJones100% (4)

- THINK L4 Unit 6 Grammar BasicDocument2 pagesTHINK L4 Unit 6 Grammar Basicniyazi polatNo ratings yet

- Budget CallDocument5 pagesBudget CallNoe S. Elizaga Jr.100% (3)

- Local FinanceDocument7 pagesLocal FinanceGelyn RabanesNo ratings yet

- Share From National WealthDocument6 pagesShare From National WealthLeonard ServedadNo ratings yet

- Office of The Municipal MayorDocument6 pagesOffice of The Municipal MayorVIRGILIO OCOY III100% (1)

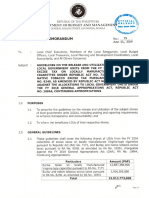

- Local Budget Memorandum: Department OF Budget AND ManagementDocument3 pagesLocal Budget Memorandum: Department OF Budget AND ManagementJethro BorjaNo ratings yet

- LBM No72Document16 pagesLBM No72Daryll DecanoNo ratings yet

- Fees and Charges Subject To Such Guidelines and Limitations As The Congress May Provide, Consistent With TheDocument11 pagesFees and Charges Subject To Such Guidelines and Limitations As The Congress May Provide, Consistent With TheAnne DerramasNo ratings yet

- FAQs Mandanas-Garcia RulingDocument27 pagesFAQs Mandanas-Garcia RulingJohnny MandocdocNo ratings yet

- Arkansas Bill SB38Document3 pagesArkansas Bill SB38capsearchNo ratings yet

- Annexure - II) .: TH THDocument18 pagesAnnexure - II) .: TH THLLM 2019No ratings yet

- Internal Revenue Allotment-ALBERTDocument14 pagesInternal Revenue Allotment-ALBERTJoy Dales100% (1)

- Draft AOM No. On Due From LGUsDocument5 pagesDraft AOM No. On Due From LGUsWilliam A. Chakas Jr.No ratings yet

- DoraDocument316 pagesDoraKhanyi MalingaNo ratings yet

- 4 DOF National Revenue Forecast FY 2022-2024Document14 pages4 DOF National Revenue Forecast FY 2022-2024Chong BianzNo ratings yet

- Vigan City Executive Summary 2020Document5 pagesVigan City Executive Summary 2020Loriane ArcainaNo ratings yet

- Analysis and Projection of Financial Sustainability PT 1 - Dizon, Erika MaeDocument29 pagesAnalysis and Projection of Financial Sustainability PT 1 - Dizon, Erika MaeBianca CTNo ratings yet

- Waste ManagementDocument5 pagesWaste ManagementWilliam A. Chakas Jr.No ratings yet

- ADM Guidelines Presentation - For DED TrainingDocument42 pagesADM Guidelines Presentation - For DED TrainingTita AdlawanNo ratings yet

- K-Local Budget Memoramdum No. 71Document17 pagesK-Local Budget Memoramdum No. 71Erin CruzNo ratings yet

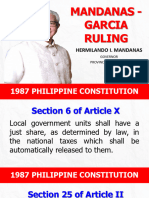

- Impact of SC Ruling To The DILG & LGUsDocument26 pagesImpact of SC Ruling To The DILG & LGUsMarijenLeaño100% (1)

- House Bill Sample OnlyDocument3 pagesHouse Bill Sample OnlyKimmy SabadoNo ratings yet

- JHB 2023-24 Final TariffsDocument254 pagesJHB 2023-24 Final TariffsMike BarkerNo ratings yet

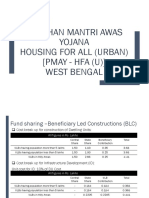

- Pradhan Mantri Awas Yojana Housing For All (Urban) (Pmay - Hfa (U) ) West BengalDocument31 pagesPradhan Mantri Awas Yojana Housing For All (Urban) (Pmay - Hfa (U) ) West BengalKunjan MitraNo ratings yet

- Local Budget Memorandum: - Republic OF THE Philippines Department OF Budget AND ManagementDocument3 pagesLocal Budget Memorandum: - Republic OF THE Philippines Department OF Budget AND ManagementJB VillanuevaNo ratings yet

- Local Budget Memorandum No. 75 PDFDocument21 pagesLocal Budget Memorandum No. 75 PDFsuzyNo ratings yet

- Local Budget Memorandum No. 75 PDFDocument21 pagesLocal Budget Memorandum No. 75 PDFArnold ImbisanNo ratings yet

- 09Document47 pages09bpsc08No ratings yet

- Sibalom Executive Summary 2020Document4 pagesSibalom Executive Summary 2020unodostreslautaroNo ratings yet

- Arkansas Bill SB43Document5 pagesArkansas Bill SB43capsearchNo ratings yet

- LBMNo 69Document10 pagesLBMNo 69Daryll DecanoNo ratings yet

- Naga Executive Summary 2015Document7 pagesNaga Executive Summary 2015Maria CharessaNo ratings yet

- Atc 163 2023 11 21 EngDocument48 pagesAtc 163 2023 11 21 Enghome87921020No ratings yet

- Division of Revenue ActDocument52 pagesDivision of Revenue ActSammyNo ratings yet

- 2022TaxLevyBy Law Setnewdatefor2022 6b13ca9267Document4 pages2022TaxLevyBy Law Setnewdatefor2022 6b13ca9267OcelNo ratings yet

- Local Budget Memorandum No.78-ADocument4 pagesLocal Budget Memorandum No.78-AWilmar TagleNo ratings yet

- !:ourt: L/epublic of TbeDocument21 pages!:ourt: L/epublic of TbeHannah Keziah Dela CernaNo ratings yet

- Mandanas v. Executive SecretaryDocument12 pagesMandanas v. Executive SecretaryBrillantes JoyNo ratings yet

- (B3 - 2021) (Division of Revenue)Document332 pages(B3 - 2021) (Division of Revenue)Diana MukuraNo ratings yet

- Apalit2022 CARDocument12 pagesApalit2022 CARTerry AceNo ratings yet

- Role of Local GovernmentDocument39 pagesRole of Local GovernmentJezrell Del Castillo Orobia100% (1)

- Mandanas Ruling - 22 August 2023Document41 pagesMandanas Ruling - 22 August 20232ndyearacc05No ratings yet

- Local Government Financing and Fiscal ManagementDocument8 pagesLocal Government Financing and Fiscal ManagementJean Jamailah TomugdanNo ratings yet

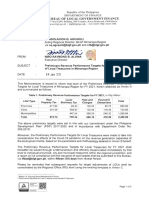

- BLGF Memo To BLGF Mimaropa Region - Preliminary Revenue Performance Targets For FY 2021 - 08 Jan 2021 - ApprovedDocument8 pagesBLGF Memo To BLGF Mimaropa Region - Preliminary Revenue Performance Targets For FY 2021 - 08 Jan 2021 - Approvedباليواغ الجيNo ratings yet

- Arkansas Bill HB1173Document3 pagesArkansas Bill HB1173capsearchNo ratings yet

- Capping Circular Debt Report Sept 2015Document22 pagesCapping Circular Debt Report Sept 2015umairNo ratings yet

- State Financ2003Document12 pagesState Financ2003pmanikNo ratings yet

- Prov of Batangas V Romulo FACTS: President Joseph Ejercito Estrada IssuedDocument15 pagesProv of Batangas V Romulo FACTS: President Joseph Ejercito Estrada IssuedAdmin DivisionNo ratings yet

- 2021 Budget Plan Executive Summary: City of Akron, Ohio Dan Horrigan, MayorDocument8 pages2021 Budget Plan Executive Summary: City of Akron, Ohio Dan Horrigan, MayorDougNo ratings yet

- Separate OpinionDocument61 pagesSeparate OpinionMA. TRISHA RAMENTONo ratings yet

- Green ! Green! Green!Document13 pagesGreen ! Green! Green!Rheii EstandarteNo ratings yet

- Budget For 2010/2011 Financial YearDocument6 pagesBudget For 2010/2011 Financial YearJapie BoschNo ratings yet

- Local Budget Memorandum No 79Document18 pagesLocal Budget Memorandum No 79Daryll DecanoNo ratings yet

- Notes 6-Revenue SourcesDocument19 pagesNotes 6-Revenue SourcesJaphet Grace MoletaNo ratings yet

- Review of The Third Plan: Plan Outlay & Its AllocationDocument6 pagesReview of The Third Plan: Plan Outlay & Its AllocationShruti WynfordNo ratings yet

- Manaoag 07112023Document5 pagesManaoag 07112023Sarah WilliamsNo ratings yet

- Annex 1Document3 pagesAnnex 1Rowena BriosoNo ratings yet

- Province of Batangas v. RomuloDocument25 pagesProvince of Batangas v. RomuloJakielyn Anne CruzNo ratings yet

- DBM Local Budget Circular 136Document9 pagesDBM Local Budget Circular 136RapplerNo ratings yet

- Budget Rigidity in Latin America and the Caribbean: Causes, Consequences, and Policy ImplicationsFrom EverandBudget Rigidity in Latin America and the Caribbean: Causes, Consequences, and Policy ImplicationsNo ratings yet

- Decentralization, Local Governance, and Local Economic Development in MongoliaFrom EverandDecentralization, Local Governance, and Local Economic Development in MongoliaNo ratings yet

- Component B Laying The FoundationDocument19 pagesComponent B Laying The Foundationrodel d hilarioNo ratings yet

- DILG-NCR - Manual BNEO Webinar PlatformDocument40 pagesDILG-NCR - Manual BNEO Webinar Platformrodel d hilarioNo ratings yet

- Advisory On Brgy CTT PDFDocument1 pageAdvisory On Brgy CTT PDFrodel d hilarioNo ratings yet

- Legal Ethics Chapter I - Lawyer and Society: What Is Amicus Curiae?Document10 pagesLegal Ethics Chapter I - Lawyer and Society: What Is Amicus Curiae?rodel d hilarioNo ratings yet

- PPP 2 PPP Overview 2Document40 pagesPPP 2 PPP Overview 2rodel d hilarioNo ratings yet

- Curriculum OF Environmental Science BS/MS: (Revised 2013)Document120 pagesCurriculum OF Environmental Science BS/MS: (Revised 2013)Jamal Ud Din QureshiNo ratings yet

- Bal Natu - Glimpses of The God-Man, Meher Baba - 1943-1948 (Vol. I) (1997)Document431 pagesBal Natu - Glimpses of The God-Man, Meher Baba - 1943-1948 (Vol. I) (1997)Kumar KNo ratings yet

- 1 Cyber Law PDFDocument2 pages1 Cyber Law PDFKRISHNA VIDHUSHANo ratings yet

- Iqra University - Karachi Faculty of Business AdministrationDocument31 pagesIqra University - Karachi Faculty of Business Administrationsyed aliNo ratings yet

- Optimization Module For Abaqus/CAE Based On Genetic AlgorithmDocument1 pageOptimization Module For Abaqus/CAE Based On Genetic AlgorithmSIMULIACorpNo ratings yet

- Chem 26.1 Lab Manual 2017 Edition (2019) PDFDocument63 pagesChem 26.1 Lab Manual 2017 Edition (2019) PDFBea JacintoNo ratings yet

- Mod Jeemain - GuruDocument31 pagesMod Jeemain - Guruparamarthasom1974No ratings yet

- Cooltech PPM (Final 3.8.17)Document54 pagesCooltech PPM (Final 3.8.17)Teri Buhl100% (1)

- Indonesian - 1 - 1 - Audiobook - KopyaDocument93 pagesIndonesian - 1 - 1 - Audiobook - KopyaBurcu BurcuNo ratings yet

- 2013 848evo DucatiOmahaDocument140 pages2013 848evo DucatiOmahaFabian Alejandro Ramos SandovalNo ratings yet

- User Manual 13398Document44 pagesUser Manual 13398Diy DoeNo ratings yet

- MSP432 Chapter2 v1Document59 pagesMSP432 Chapter2 v1Akshat TulsaniNo ratings yet

- Portfolio Output No. 17: Reflections On Personal RelationshipsDocument3 pagesPortfolio Output No. 17: Reflections On Personal RelationshipsKatrina De VeraNo ratings yet

- Better Get 'It in Your SoulDocument4 pagesBetter Get 'It in Your SoulJeremiah AnnorNo ratings yet

- Explore (As) : Types of Commission and InterestsDocument4 pagesExplore (As) : Types of Commission and InterestsTiffany Joy Lencioco GambalanNo ratings yet

- MAN0019215 - TaqPathCOVID-19 - CE-IVD - RT-PCR Kit - IFUDocument27 pagesMAN0019215 - TaqPathCOVID-19 - CE-IVD - RT-PCR Kit - IFUFe LipeNo ratings yet

- Store Name: United Food Company Kaust: It Code DescriptionDocument20 pagesStore Name: United Food Company Kaust: It Code DescriptionFazlul RifazNo ratings yet

- Harvatek Corp. v. Nichia Corp. - ComplaintDocument51 pagesHarvatek Corp. v. Nichia Corp. - ComplaintSarah BursteinNo ratings yet

- Pre-Feasibility of Tunnel Farming in BahawalpurDocument10 pagesPre-Feasibility of Tunnel Farming in Bahawalpurshahidameen2100% (1)

- Nes D2188Document6 pagesNes D2188prasannaNo ratings yet

- Caro PresentationDocument33 pagesCaro PresentationVIJAY GARGNo ratings yet

- 1999 Aversion Therapy-BEDocument6 pages1999 Aversion Therapy-BEprabhaNo ratings yet

- Swelling Properties of Chitosan Hydrogels: David R Rohindra, Ashveen V Nand, Jagjit R KhurmaDocument4 pagesSwelling Properties of Chitosan Hydrogels: David R Rohindra, Ashveen V Nand, Jagjit R KhurmaSeptian Perwira YudhaNo ratings yet

- Hispanic Tradition in Philippine ArtsDocument14 pagesHispanic Tradition in Philippine ArtsRoger Pascual Cuaresma100% (1)

- Masonic SymbolismDocument19 pagesMasonic SymbolismOscar Cortez100% (7)

- Social Work As A ProfessionDocument4 pagesSocial Work As A ProfessionIssa KhalidNo ratings yet

- Will Love Make You HappyDocument2 pagesWill Love Make You HappyMuhammad Musa HaiderNo ratings yet