Download as pptx, pdf, or txt

You might also like

- Personal Finance 5th Edition Jeff Madura Solutions Manual 1Document8 pagesPersonal Finance 5th Edition Jeff Madura Solutions Manual 1kurt100% (51)

- TAX 2202E TBS01 02.solutionDocument2 pagesTAX 2202E TBS01 02.solutionZhitong LuNo ratings yet

- Discharge of Surety's Liability by AbhishekDocument9 pagesDischarge of Surety's Liability by AbhishekAbhishek Kamat100% (1)

- Chapter 3, Basic Elements of Financial SystemDocument27 pagesChapter 3, Basic Elements of Financial Systemmiracle123No ratings yet

- 2020 NCAA Financial Report-South CarolinaDocument80 pages2020 NCAA Financial Report-South CarolinaMatt BrownNo ratings yet

- Chapter 5. Banking and Interest RatesDocument40 pagesChapter 5. Banking and Interest RatesNguyen Dac ThichNo ratings yet

- L7 Financial ManagementDocument42 pagesL7 Financial Managementfairylucas708No ratings yet

- Chapter 12Document65 pagesChapter 12Francisca Rojas CameronNo ratings yet

- Lecture Week 3&4 - BFDocument28 pagesLecture Week 3&4 - BFMuhammad HasnainNo ratings yet

- Financial Institutions, Functions and Importance.: Prepared By: Dr. Albert C. RocesDocument12 pagesFinancial Institutions, Functions and Importance.: Prepared By: Dr. Albert C. RocesAMNo ratings yet

- Chapter Five: Management of Monetary AssetsDocument30 pagesChapter Five: Management of Monetary AssetsSwati PorwalNo ratings yet

- Corporate FinancingDocument25 pagesCorporate FinancingHoai ThuongNo ratings yet

- Managing Your Cash and SavingsDocument48 pagesManaging Your Cash and SavingsAbigail ConstantinoNo ratings yet

- AFN 221 W04 Savings vF2021Document19 pagesAFN 221 W04 Savings vF2021Dina SboulNo ratings yet

- Module 1.1 Financial MarketsDocument60 pagesModule 1.1 Financial MarketssateeshjorliNo ratings yet

- Msme Week 7 - Finance and Small BusinessFile-1Document55 pagesMsme Week 7 - Finance and Small BusinessFile-1Rahiana AminNo ratings yet

- Presentation (6) Business FinanceDocument17 pagesPresentation (6) Business FinancecycygajatorNo ratings yet

- Chapter Six: Risk Management in Financial InstitutionsDocument22 pagesChapter Six: Risk Management in Financial InstitutionsMikias DegwaleNo ratings yet

- Personal Finance 4 - 1Document47 pagesPersonal Finance 4 - 1Taeyeon KimNo ratings yet

- Polytechnic University of The Philippines: Financing CompaniesDocument48 pagesPolytechnic University of The Philippines: Financing CompaniesMomo MontefalcoNo ratings yet

- Chapter - 10 - Fixed Income Securities - GitmanDocument39 pagesChapter - 10 - Fixed Income Securities - GitmanJessica Charoline PangkeyNo ratings yet

- Money and Banking & Managing FinanceDocument29 pagesMoney and Banking & Managing FinancebanghazimNo ratings yet

- Access To Capital Forum 2015Document136 pagesAccess To Capital Forum 2015Bronwen Elizabeth MaddenNo ratings yet

- FMI REPORTING Group 1Document18 pagesFMI REPORTING Group 1Stephanie DesembranaNo ratings yet

- Chapter 1aDocument33 pagesChapter 1aVasunNo ratings yet

- Finacial Institutions and Its Role: Entrepreneurship ProjectDocument17 pagesFinacial Institutions and Its Role: Entrepreneurship ProjectAyush GiriNo ratings yet

- 5-Non-Banking Financial InstitutionsDocument19 pages5-Non-Banking Financial InstitutionsSharleen Joy TuguinayNo ratings yet

- Personal Finance 5th Edition Jeff Madura Solutions Manual 1Document36 pagesPersonal Finance 5th Edition Jeff Madura Solutions Manual 1karenhalesondbatxme100% (33)

- PPCH 08 ADocument55 pagesPPCH 08 AumaNo ratings yet

- Rift Valley: UnversityDocument11 pagesRift Valley: Unversitybirook lemaNo ratings yet

- Unit IV. Non Banking Financial InstitutionsDocument19 pagesUnit IV. Non Banking Financial InstitutionsclatowedNo ratings yet

- Oct 17 WS 1 Understanding Credit and How To Improve Your Credit ScoreDocument19 pagesOct 17 WS 1 Understanding Credit and How To Improve Your Credit ScorePîslaru NicoletaNo ratings yet

- Personal Finance 6th Edition Madura Solutions Manual 1Document36 pagesPersonal Finance 6th Edition Madura Solutions Manual 1karenhalesondbatxme100% (25)

- Financial Economics Chapter ThreeDocument21 pagesFinancial Economics Chapter ThreeGenemo FitalaNo ratings yet

- Financialservices: Kanika BhasinDocument14 pagesFinancialservices: Kanika BhasinkanikaNo ratings yet

- Bank of Maharashtra ProjectDocument67 pagesBank of Maharashtra ProjectDilip JainNo ratings yet

- Chap I Introduction To Financial InstitutionsDocument57 pagesChap I Introduction To Financial InstitutionsGing freexNo ratings yet

- Sources of Business FinanceDocument12 pagesSources of Business Financepriyanshu ahujaNo ratings yet

- Financial Institutions: 1. Life Insurance Companies, Which Sell Life Insurance, Annuities and PensionsDocument7 pagesFinancial Institutions: 1. Life Insurance Companies, Which Sell Life Insurance, Annuities and PensionssamouNo ratings yet

- Sources of Finance: Neeta Asnani Alpana Garg Pratibha Arora Kalpana TewaniDocument23 pagesSources of Finance: Neeta Asnani Alpana Garg Pratibha Arora Kalpana TewaniMahima LounganiNo ratings yet

- Ae18-004-The Philippine Financial SystemDocument30 pagesAe18-004-The Philippine Financial SystemLaezelie PalajeNo ratings yet

- Financial Services-Basics: LT P. Abdul Azees Farook College IndiaDocument18 pagesFinancial Services-Basics: LT P. Abdul Azees Farook College IndiaVivek SharmaNo ratings yet

- BCH FE NotesDocument25 pagesBCH FE NotesDownload MovieNo ratings yet

- Corporate BankingDocument21 pagesCorporate BankingPadma NarayananNo ratings yet

- Chapter ThreeDocument25 pagesChapter Threeshraddha amatyaNo ratings yet

- Financial Markets and InstitutionsDocument11 pagesFinancial Markets and InstitutionsEarl Daniel RemorozaNo ratings yet

- Kuratko 8 e CH 08Document35 pagesKuratko 8 e CH 08waqasNo ratings yet

- MODULE 3 SVV Banking StudentDocument6 pagesMODULE 3 SVV Banking StudentJessica RosalesNo ratings yet

- Presentation On Financial InstitutionDocument20 pagesPresentation On Financial InstitutionBushra KashafNo ratings yet

- Entrepreneur CH 6Document37 pagesEntrepreneur CH 6Getahun AbebawNo ratings yet

- CH 6Document19 pagesCH 6george manNo ratings yet

- MN2615 T5 Session 2 - Small Business FinanceDocument59 pagesMN2615 T5 Session 2 - Small Business FinanceHaseeb DarNo ratings yet

- Banks and Other Financial Intermediaries: By: John Paulo H. PobleteDocument12 pagesBanks and Other Financial Intermediaries: By: John Paulo H. PobleteMary Elleonice Franchette QuiambaoNo ratings yet

- Part - I: Introduction: Chapter 2: Overview of The Financial SystemDocument25 pagesPart - I: Introduction: Chapter 2: Overview of The Financial SystemAKSHIT JAINNo ratings yet

- Debt and Equity Markets As Source of LT FinanceDocument23 pagesDebt and Equity Markets As Source of LT FinanceAbhishekNo ratings yet

- Indian Financial SystemDocument23 pagesIndian Financial SystemAkash YadavNo ratings yet

- B.AEco (Hon) - Macro - 4th Sem - Lesson 9Document15 pagesB.AEco (Hon) - Macro - 4th Sem - Lesson 9Sharad RanjanNo ratings yet

- BF Week 9 Short and Long Term FundsDocument29 pagesBF Week 9 Short and Long Term FundsNathasha Mitch FontanaresNo ratings yet

- Financial Management: 12 Abm-Jonah Mr. Raffy Rey DomasianDocument24 pagesFinancial Management: 12 Abm-Jonah Mr. Raffy Rey DomasianDioselin Pegoria SoloNo ratings yet

- UNIT 1 Core Banking Vs Allied Banking Activities AKG-1Document21 pagesUNIT 1 Core Banking Vs Allied Banking Activities AKG-1A Walk To InfinityNo ratings yet

- Module 4 - Non-Bank Financial InstitutionsDocument19 pagesModule 4 - Non-Bank Financial InstitutionsMICHELLE MILANANo ratings yet

- Chapter 7 Source of Finance PDFDocument30 pagesChapter 7 Source of Finance PDFtharinduNo ratings yet

- Exam LTAM: You Have What It Takes To PassDocument12 pagesExam LTAM: You Have What It Takes To Passderianfg100% (1)

- Smart Scholar: Best Investment Plan For Children's EducationDocument1 pageSmart Scholar: Best Investment Plan For Children's EducationTricolor C ANo ratings yet

- G.R. No. L-18452Document6 pagesG.R. No. L-18452Hanifa D. Al-ObinayNo ratings yet

- Krishna ProjectDocument32 pagesKrishna Projectprashant mhatreNo ratings yet

- Lic CaseDocument3 pagesLic CaseDhriti DhingraNo ratings yet

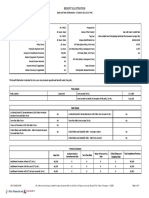

- Benefit Illustration: UIN: 104N116V08 Page 1 of 2Document4 pagesBenefit Illustration: UIN: 104N116V08 Page 1 of 2Onn InternationalNo ratings yet

- Internship Program at IDL IMFDocument2 pagesInternship Program at IDL IMFsakshi srivastavaNo ratings yet

- It FileDocument16 pagesIt Filedishu kumarNo ratings yet

- Mint Article Unclaimed 13 July 2023Document9 pagesMint Article Unclaimed 13 July 2023cosoxal118No ratings yet

- All You Need To Know About Angelique KantengwaDocument2 pagesAll You Need To Know About Angelique KantengwaAngelique KantengwaNo ratings yet

- Introducing Acko HealthDocument12 pagesIntroducing Acko HealthtamaldNo ratings yet

- Job Ad - CSODocument1 pageJob Ad - CSOMuhammad AdnanNo ratings yet

- Platinum Trio Hmo 0-25 Offex m0033963 01-24 SBCDocument9 pagesPlatinum Trio Hmo 0-25 Offex m0033963 01-24 SBCapi-531507901No ratings yet

- What If I Die Without A Business PartnerDocument2 pagesWhat If I Die Without A Business PartnerDave SeemsNo ratings yet

- Car Auto Repair Research QuestionsDocument5 pagesCar Auto Repair Research QuestionsFatima SethiNo ratings yet

- Great Pacific Life-vs-CADocument2 pagesGreat Pacific Life-vs-CAmario navalezNo ratings yet

- Smart Income LeafletDocument2 pagesSmart Income Leafletsspublicationservices indiaNo ratings yet

- Construction Law Senet Fall 2020Document64 pagesConstruction Law Senet Fall 2020Rhyzan CroomesNo ratings yet

- Insurance Case Digest Batch 2Document4 pagesInsurance Case Digest Batch 2Di CanNo ratings yet

- Your Guide To Disability BenefitsDocument11 pagesYour Guide To Disability BenefitsStephenFitchNo ratings yet

- SIP FileDocument62 pagesSIP FileswetaNo ratings yet

- Quiz 1 Tax - AnswerDocument9 pagesQuiz 1 Tax - AnswerHannahNo ratings yet

- Axis Bank PrintDocument41 pagesAxis Bank PrintRudrasish BeheraNo ratings yet

- Finance e PN 2016 17Document69 pagesFinance e PN 2016 17Ancy RajNo ratings yet

- Lapse Study: Date: August 13, 2012 By: Albert Li, Simon HirstDocument33 pagesLapse Study: Date: August 13, 2012 By: Albert Li, Simon Hirstmatematikawan muslimNo ratings yet

- Northwestern State University of Louisiana Certification of Financial Responsibility InstructionsDocument2 pagesNorthwestern State University of Louisiana Certification of Financial Responsibility InstructionsOlawale DawoduNo ratings yet

- Computation of Taxable Income Under Various HeadsDocument155 pagesComputation of Taxable Income Under Various Headsdajit1100% (6)