Download as ppt, pdf, or txt

You might also like

- Prajwal G Bharadwaj - EY Internship ReportDocument55 pagesPrajwal G Bharadwaj - EY Internship ReportBharathi Raju100% (2)

- BUS 400 Business Model CanvasDocument2 pagesBUS 400 Business Model CanvasMugambi OliverNo ratings yet

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDocument7 pagesAccounting For Managers (Assignment One (E-Finance) ) Question OnehananNo ratings yet

- V-Ride, Inc.: Case 4-1Document11 pagesV-Ride, Inc.: Case 4-1Dave Castillo Bangisan100% (1)

- Chapter 12 SolutionsDocument10 pagesChapter 12 Solutionshassan.murad100% (2)

- De Beers, Marketing Diamonds To MillennialsDocument13 pagesDe Beers, Marketing Diamonds To MillennialsNitish100% (1)

- Personal Branding WorksheetDocument3 pagesPersonal Branding WorksheetAgnes DessyNo ratings yet

- Business Plan of Manufacturing Air PurifiersDocument7 pagesBusiness Plan of Manufacturing Air PurifiersSakshi BaiwalNo ratings yet

- RUNNING HEAD: Accounting Questions 1Document6 pagesRUNNING HEAD: Accounting Questions 1Chirayu ThapaNo ratings yet

- Harvard Financial Accounting Final Exam 3Document11 pagesHarvard Financial Accounting Final Exam 3Bharathi Raju0% (1)

- Harvard Financial Accounting Final Exam 2Document12 pagesHarvard Financial Accounting Final Exam 2Bharathi RajuNo ratings yet

- Applying Mindstate Marketing For Consistent Brand Growth 06082020Document17 pagesApplying Mindstate Marketing For Consistent Brand Growth 06082020Sergiu Alexandru VlasceanuNo ratings yet

- Resolución CaseDocument21 pagesResolución CaseyojaniNo ratings yet

- Prestige Telephone CompanyDocument8 pagesPrestige Telephone CompanyRiandy Ar RasyidNo ratings yet

- FABM2 Chapter2Document7 pagesFABM2 Chapter2Archie CampomanesNo ratings yet

- Cost Management Accounting DEC 2023Document4 pagesCost Management Accounting DEC 2023Aash RedmiNo ratings yet

- Cost Management Accounting AM1 STDocument5 pagesCost Management Accounting AM1 STAash RedmiNo ratings yet

- Tutorial 3 AnswersDocument7 pagesTutorial 3 AnswersFEI FEINo ratings yet

- Prestige Telephone Company Work SheetDocument8 pagesPrestige Telephone Company Work SheetaaaaNo ratings yet

- A Case Study On Roxor Watch Company Pty LTD Team Divergents 120522 10.41pmDocument5 pagesA Case Study On Roxor Watch Company Pty LTD Team Divergents 120522 10.41pmKrystel Joie Caraig ChangNo ratings yet

- Income Statement TemplateDocument4 pagesIncome Statement Templatesally ngNo ratings yet

- Ch13-Leverage, Capital Structure-Part 2Document32 pagesCh13-Leverage, Capital Structure-Part 2Hatem MohammedNo ratings yet

- GSBA002 - Management Accounting - Realyn Austria - Case Study 3BDocument4 pagesGSBA002 - Management Accounting - Realyn Austria - Case Study 3BRealyn AustriaNo ratings yet

- Prestige Data Services Exhibit 1 Jan Feb MarDocument3 pagesPrestige Data Services Exhibit 1 Jan Feb MarRajat GargNo ratings yet

- AC2105 Seminar 3 Group 3Document37 pagesAC2105 Seminar 3 Group 3Kwang Yi JuinNo ratings yet

- Assignment 3 ACT502Document6 pagesAssignment 3 ACT502Mahdi KhanNo ratings yet

- Acc AssignmentDocument8 pagesAcc AssignmentKashémNo ratings yet

- Financial Model For BrandsDocument60 pagesFinancial Model For BrandsAnjali SrivastavaNo ratings yet

- Software Asssociates11Document13 pagesSoftware Asssociates11Arslan ShaikhNo ratings yet

- SecD Group7 PrestigeDocument10 pagesSecD Group7 PrestigePushpendra Kumar RaiNo ratings yet

- Financial Statement Analysis QuestionsDocument11 pagesFinancial Statement Analysis QuestionsShrunaliNo ratings yet

- EE Financial ProjectionsDocument2 pagesEE Financial Projectionsnishatmridula06No ratings yet

- Answer Key To Test #3 - ACCT-312 - Fall 2019Document8 pagesAnswer Key To Test #3 - ACCT-312 - Fall 2019Amir ContrerasNo ratings yet

- Teodoro M. Luansing College of Rosario: Accounts Dr. CRDocument8 pagesTeodoro M. Luansing College of Rosario: Accounts Dr. CRSamantha Alice LysanderNo ratings yet

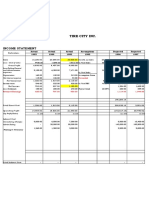

- Tire City IncDocument18 pagesTire City IncSoumyajitNo ratings yet

- Analysis of Sales VolumeDocument10 pagesAnalysis of Sales VolumeBharathi RajuNo ratings yet

- Relevant Cost Exercise SolutionDocument14 pagesRelevant Cost Exercise SolutionHimadri DeyNo ratings yet

- A. Calculate The Break-Even Dollar Sales For The MonthDocument25 pagesA. Calculate The Break-Even Dollar Sales For The MonthPriyankaNo ratings yet

- Managerial Accounting - Final Project - Yahya Patanwala.12028Document4 pagesManagerial Accounting - Final Project - Yahya Patanwala.12028Yahya SaifuddinNo ratings yet

- Managerial Final Project Study NotesDocument8 pagesManagerial Final Project Study NotesShawn KPNo ratings yet

- ManAc Midterms Chuckie ChukieDocument2 pagesManAc Midterms Chuckie ChukieVAUGHN MARTINEZNo ratings yet

- PrestigeDocument13 pagesPrestigeMona SahooNo ratings yet

- Seatwork 4 - Decentralized OperationsDocument3 pagesSeatwork 4 - Decentralized OperationsJessaLyza CordovaNo ratings yet

- Angel's Pizza Pro Forma Income Statement January 2019 - December 2019Document5 pagesAngel's Pizza Pro Forma Income Statement January 2019 - December 2019Rimar LuayNo ratings yet

- CVP MC 1920 W KeyDocument6 pagesCVP MC 1920 W KeyGale RasNo ratings yet

- Management AccountingDocument6 pagesManagement AccountingBornyNo ratings yet

- Software ExcelDocument12 pagesSoftware ExcelparvathysiyyerNo ratings yet

- Intacc 3 Ans To Chap 1 ProbsDocument4 pagesIntacc 3 Ans To Chap 1 ProbsMhico MateoNo ratings yet

- 6 Section - CustomerDocument41 pages6 Section - CustomerFenandoNo ratings yet

- This Study Resource Was Shared Via: RequiredDocument1 pageThis Study Resource Was Shared Via: RequiredJalaj GuptaNo ratings yet

- Chapter 6 CVP Analysis - Part I - LMSDocument43 pagesChapter 6 CVP Analysis - Part I - LMSPiece of WritingsNo ratings yet

- AHM13e Chapter - 03 - Solution To Problems and Key To CasesDocument24 pagesAHM13e Chapter - 03 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Software Associates CoursewareDocument27 pagesSoftware Associates CoursewareAISHWARYA SONINo ratings yet

- Cost & Management Accounting MBADocument4 pagesCost & Management Accounting MBAashwinimore811No ratings yet

- Chapter 5 - A2, B1, & 59Document5 pagesChapter 5 - A2, B1, & 59詹鎮豪No ratings yet

- AccountingDocument7 pagesAccountingDaniela Pedrosa100% (1)

- SD17 Hybrid F5 Section C Answers Clean Proof PDFDocument12 pagesSD17 Hybrid F5 Section C Answers Clean Proof PDFShaksham SharmaNo ratings yet

- Business Break EvenDocument2 pagesBusiness Break Eventaona madanhireNo ratings yet

- WHOLESALE and RETAIL EXAM QUESTIONS WITH MODEL ANSWERS - SEPT 2017Document3 pagesWHOLESALE and RETAIL EXAM QUESTIONS WITH MODEL ANSWERS - SEPT 2017chelasimunyolaNo ratings yet

- Hasil Abnormal ReturnDocument1 pageHasil Abnormal ReturnSurya KeceNo ratings yet

- Department AccountingDocument12 pagesDepartment AccountingRajesh NangaliaNo ratings yet

- Problem Solving AssignmentDocument13 pagesProblem Solving AssignmentRajesh MongerNo ratings yet

- Financial Plan OkDocument7 pagesFinancial Plan OkSYED ARSALANNo ratings yet

- What Is A Segment?: in Financial ReportingDocument74 pagesWhat Is A Segment?: in Financial ReportingJerianne PascoNo ratings yet

- f9 Answer-Mock-Exam-F9Document9 pagesf9 Answer-Mock-Exam-F9amalthomas557No ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Capital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisFrom EverandCapital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisNo ratings yet

- Illustration On Double Column Cash BookDocument1 pageIllustration On Double Column Cash BookBharathi RajuNo ratings yet

- Introduction of The Company: Mckinsey's 7's Framework: Functions and ProcessDocument1 pageIntroduction of The Company: Mckinsey's 7's Framework: Functions and ProcessBharathi RajuNo ratings yet

- Name: Rajesh Kumar K.R SRN: PES1PG19MB274 Company: Exotalent Consultancy Services LLPDocument6 pagesName: Rajesh Kumar K.R SRN: PES1PG19MB274 Company: Exotalent Consultancy Services LLPBharathi RajuNo ratings yet

- FInal Internship Report-Rajesh Kumar K.R (MB274)Document58 pagesFInal Internship Report-Rajesh Kumar K.R (MB274)Bharathi RajuNo ratings yet

- Name: SRN: Company:: Meghna Ashwin Kurunji PES1PG19MB091 Exotalent Consultancy Services LLPDocument8 pagesName: SRN: Company:: Meghna Ashwin Kurunji PES1PG19MB091 Exotalent Consultancy Services LLPBharathi RajuNo ratings yet

- Raspberry Pi Based Solar Street Light: (IEEE-2015)Document4 pagesRaspberry Pi Based Solar Street Light: (IEEE-2015)Bharathi RajuNo ratings yet

- Global Foreign-Exchange Markets: International BusinessDocument20 pagesGlobal Foreign-Exchange Markets: International BusinessBharathi RajuNo ratings yet

- Qwikcilver Corporate Reward SolutionsDocument6 pagesQwikcilver Corporate Reward SolutionsBharathi RajuNo ratings yet

- Sms SynopsisDocument6 pagesSms SynopsisBharathi RajuNo ratings yet

- Chap 9 IBDocument20 pagesChap 9 IBBharathi RajuNo ratings yet

- Question Bank UM19MB602: Introduction To Machine Learning Unit 4: Decision TreeDocument4 pagesQuestion Bank UM19MB602: Introduction To Machine Learning Unit 4: Decision TreeBharathi RajuNo ratings yet

- Python Networking PDFDocument4 pagesPython Networking PDFBharathi RajuNo ratings yet

- Question Bank UM19MB602: Introduction To Machine Learning Unit 3: Classification ProblemsDocument2 pagesQuestion Bank UM19MB602: Introduction To Machine Learning Unit 3: Classification ProblemsBharathi RajuNo ratings yet

- Question Bank UM19MB602: Introduction To Machine Learning Unit 2: Regression MethodsDocument1 pageQuestion Bank UM19MB602: Introduction To Machine Learning Unit 2: Regression MethodsBharathi RajuNo ratings yet

- 6.density Chart 20 - 08 - 20 - Day6Document13 pages6.density Chart 20 - 08 - 20 - Day6Bharathi RajuNo ratings yet

- Proportional Symbol MapDocument5 pagesProportional Symbol MapBharathi RajuNo ratings yet

- Proportional Symbol MapDocument5 pagesProportional Symbol MapBharathi RajuNo ratings yet

- OB Billgates Leadership Final VDocument16 pagesOB Billgates Leadership Final VBharathi RajuNo ratings yet

- 1st Quarter SummativeDocument4 pages1st Quarter SummativeGlychalyn Abecia 23No ratings yet

- FM AssignmentDocument10 pagesFM Assignmentshingirai kasaeraNo ratings yet

- Sun SilkDocument15 pagesSun SilkArjun KapoorNo ratings yet

- SWOT Titan FinalDocument29 pagesSWOT Titan FinalMukesh Manwani100% (1)

- Sale Data Analysis - Group Project Statistics.Document15 pagesSale Data Analysis - Group Project Statistics.Trang CaoNo ratings yet

- Learings-Gagan Singh Mokha: INTRODUCTION: What Is Not Strategy-Day To Day Plans Broad Principles For Governing TheDocument5 pagesLearings-Gagan Singh Mokha: INTRODUCTION: What Is Not Strategy-Day To Day Plans Broad Principles For Governing ThegaganNo ratings yet

- MGH Case Study MTNDocument17 pagesMGH Case Study MTNZeeh MaqandaNo ratings yet

- Questionpaper ALevelPaper3 June2018 - 3Document36 pagesQuestionpaper ALevelPaper3 June2018 - 3evansNo ratings yet

- The Ultimate Affiliate Marketing Cheat SheetDocument11 pagesThe Ultimate Affiliate Marketing Cheat SheetVash Memar0% (1)

- Sumec Textile PresentationDocument42 pagesSumec Textile PresentationmechiniNo ratings yet

- SUMMER TRAINING REPORT KoyalDocument69 pagesSUMMER TRAINING REPORT KoyalNARENDERNo ratings yet

- Jonathan's PresentationDocument9 pagesJonathan's PresentationJonathan AbishekNo ratings yet

- Phifer - Major FinalDocument106 pagesPhifer - Major Finalraj kumarNo ratings yet

- Marketing Interview Questions and Answers Guide.: Global GuidelineDocument30 pagesMarketing Interview Questions and Answers Guide.: Global GuidelineAMITAVA ROYNo ratings yet

- What Is Strategic Audit?: Strategy Implementation Requires A Firm To EstablishDocument3 pagesWhat Is Strategic Audit?: Strategy Implementation Requires A Firm To EstablishDSAW VALERIONo ratings yet

- CHAPTER 1 - The Meaning of Marketing Communications in Travel and Tourism-1Document19 pagesCHAPTER 1 - The Meaning of Marketing Communications in Travel and Tourism-1Haziq AujiNo ratings yet

- Fashion Business PlanDocument12 pagesFashion Business PlanMAVERICK MONROE100% (1)

- Research Paper On Social MediaDocument6 pagesResearch Paper On Social Mediauifjzvrif100% (1)

- Oil Transportation Ltd. Business PlanDocument37 pagesOil Transportation Ltd. Business PlansaraNo ratings yet

- Big BasketDocument10 pagesBig BasketvigneshNo ratings yet

- Marketing For Hospitality and Tourism 7th Edition Kotler Test BankDocument7 pagesMarketing For Hospitality and Tourism 7th Edition Kotler Test Bankkaylayoungfpkgwdbjcz100% (28)

- Man Environment Interaction of Naz BasinDocument28 pagesMan Environment Interaction of Naz BasinTp TpNo ratings yet

- Analisis Strategi Pemasaran Dalam Meningkatkan PenjualanDocument8 pagesAnalisis Strategi Pemasaran Dalam Meningkatkan Penjualanhanahnuza channelNo ratings yet

- Cramble Brew Business PlanDocument34 pagesCramble Brew Business Plan2A, Valencia, Maxene V.No ratings yet

- A. Cases Midterm: Chap 1: Puma Gives The Boot To Cardboard Shoe BoxesDocument17 pagesA. Cases Midterm: Chap 1: Puma Gives The Boot To Cardboard Shoe BoxesVương HườngNo ratings yet

- Retail Store Design: 2. International Case StudyDocument3 pagesRetail Store Design: 2. International Case StudyNisha LamixaneNo ratings yet