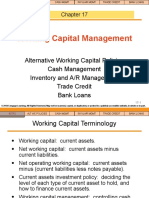

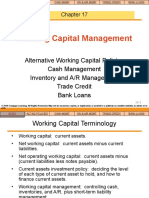

Working Capital Management - Brigham

Working Capital Management - Brigham

You might also like

- A Folklore Bestiary (High-Res) (OSE)Document160 pagesA Folklore Bestiary (High-Res) (OSE)Digs31100% (2)

- Audit of Cash Test BanksDocument270 pagesAudit of Cash Test BanksAldrin Zolina100% (2)

- Budget Proposal: Creation of Print Media, TV Station, and Radio StationDocument6 pagesBudget Proposal: Creation of Print Media, TV Station, and Radio StationAldrin Zolina100% (1)

- Quiz (6 Items X 5 Points) : Problem Solving For Management Science Name: Section: Date: ScoreDocument1 pageQuiz (6 Items X 5 Points) : Problem Solving For Management Science Name: Section: Date: Scorephillip quimenNo ratings yet

- Chapter 03 Gross EstateDocument16 pagesChapter 03 Gross EstateNikki Bucatcat0% (1)

- Audit of Inventories: Problem No. 1Document272 pagesAudit of Inventories: Problem No. 1Aldrin Zolina100% (13)

- Revised Corporation Code - SummaryDocument34 pagesRevised Corporation Code - SummaryAldrin ZolinaNo ratings yet

- Case StudyDocument8 pagesCase StudyCleofe Mae Piñero AseñasNo ratings yet

- Gifts From The Sales Representative 1Document1 pageGifts From The Sales Representative 1Mj Salusada100% (2)

- The Application of Budgets and Budgetary Control On The Performance of Small and Medium-Sized Enterprises (Smes)Document18 pagesThe Application of Budgets and Budgetary Control On The Performance of Small and Medium-Sized Enterprises (Smes)P.S.VP JahnaviNo ratings yet

- BF Case Study Sweet Beginnings Co 1Document3 pagesBF Case Study Sweet Beginnings Co 1Bryan Caadyang100% (1)

- Competitivenes AssignmentDocument3 pagesCompetitivenes AssignmentTristan Zambale100% (1)

- BDO Unibank 2020 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2020 Annual Report Financial SupplementsDanNo ratings yet

- Moldez INT03 QUIZDocument3 pagesMoldez INT03 QUIZVincent Larrie MoldezNo ratings yet

- AGA Company Manufactures and Sells A Product ForDocument6 pagesAGA Company Manufactures and Sells A Product ForSeemabians KazmiNo ratings yet

- Portal1.Passportindia - Gov.in AppOnlineProject Secure ViewDraftAction Arn 13-0007206836Document2 pagesPortal1.Passportindia - Gov.in AppOnlineProject Secure ViewDraftAction Arn 13-0007206836patelaxayNo ratings yet

- WG I Monitor Backspin Relay and Probe Manual Rev 7 0Document14 pagesWG I Monitor Backspin Relay and Probe Manual Rev 7 0elch310scridbNo ratings yet

- Chapter 9 Expanding Customer RelationshipsDocument27 pagesChapter 9 Expanding Customer RelationshipsSherren Marie NalaNo ratings yet

- Project Classification:: Advantages of Net Present Value (NPV)Document5 pagesProject Classification:: Advantages of Net Present Value (NPV)Orko AbirNo ratings yet

- Horizontal Analysis Interpretation PDFDocument2 pagesHorizontal Analysis Interpretation PDFAlison JcNo ratings yet

- Theories: Basic ConceptsDocument20 pagesTheories: Basic ConceptsJude VeanNo ratings yet

- Financial Management BSATDocument9 pagesFinancial Management BSATEma Dupilas GuianalanNo ratings yet

- Balanced ScorecardDocument14 pagesBalanced ScorecardLand DoranNo ratings yet

- AE 18 Financial Market Prelim ExamDocument3 pagesAE 18 Financial Market Prelim ExamWenjunNo ratings yet

- Chapter 1Document7 pagesChapter 1Lhea Tomas Bicera-AlcantaraNo ratings yet

- Managerial Finance by Gtman 5th EditionDocument17 pagesManagerial Finance by Gtman 5th EditionIrfan Yaqoob100% (1)

- Debt RestructuringDocument2 pagesDebt RestructuringDañella Jane Baisa0% (1)

- Financial Statements Analysis - ComprehensiveDocument60 pagesFinancial Statements Analysis - ComprehensiveGonzalo Jr. RualesNo ratings yet

- 09 - Chapter 9 Cost of CapitalDocument56 pages09 - Chapter 9 Cost of Capitalhunkie100% (1)

- Master in Business Administration Mba 308 - Financial ManagementDocument5 pagesMaster in Business Administration Mba 308 - Financial ManagementJhaydiel JacutanNo ratings yet

- Chapter 5 Financial Markets and InstitutionsDocument12 pagesChapter 5 Financial Markets and InstitutionsHamis Rabiam MagundaNo ratings yet

- FM - Cost of CapitalDocument26 pagesFM - Cost of CapitalMaxine SantosNo ratings yet

- Module 2 - Topic 4Document8 pagesModule 2 - Topic 4Moon LightNo ratings yet

- CH 13#6Document13 pagesCH 13#6jjmaducdoc100% (1)

- Krystal Guile Dagatan - Activity 2Document6 pagesKrystal Guile Dagatan - Activity 2Krystal Guile DagatanNo ratings yet

- WC - Merits and DemeritsDocument23 pagesWC - Merits and DemeritsARUN100% (1)

- Valuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitDocument41 pagesValuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitArundhati SinhaNo ratings yet

- Mid-Sem Answers and SolutionsDocument26 pagesMid-Sem Answers and SolutionsAmeer Zahar50% (2)

- Chapter 6 - Strategic ManagementDocument21 pagesChapter 6 - Strategic ManagementnadineNo ratings yet

- Draft 1Document5 pagesDraft 1Precious Dorothy magduraNo ratings yet

- MGT-4 Modules 1-5Document15 pagesMGT-4 Modules 1-5RHIAN B.No ratings yet

- Chapter 12Document34 pagesChapter 12Kad SaadNo ratings yet

- Leverages PROBLEMS AND SOLUTIONSDocument7 pagesLeverages PROBLEMS AND SOLUTIONSrashidNo ratings yet

- Asuprin Activity Worksheet: Compiled By: A. S. MALQUISTODocument5 pagesAsuprin Activity Worksheet: Compiled By: A. S. MALQUISTOLynNo ratings yet

- Reed's Clothier Case StudyDocument6 pagesReed's Clothier Case StudyColleen Sieger Mueller0% (2)

- Group 1Document16 pagesGroup 1Mariann Jane GanNo ratings yet

- Role of Financial Management in OrganizationDocument8 pagesRole of Financial Management in OrganizationTasbeha SalehjeeNo ratings yet

- Finman Module 8Document42 pagesFinman Module 8Jennyveive RiveraNo ratings yet

- Direct Method or Cost of Goods Sold MethodDocument2 pagesDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNo ratings yet

- FinMan Module 2 Financial Markets & InstitutionsDocument13 pagesFinMan Module 2 Financial Markets & Institutionserickson hernanNo ratings yet

- Chapter 9 Financial Forecasting For Strategic GrowthDocument18 pagesChapter 9 Financial Forecasting For Strategic GrowthMa. Jhoan DailyNo ratings yet

- Managerial Economics Assignment 3 PDFDocument2 pagesManagerial Economics Assignment 3 PDFSakinaNo ratings yet

- Examination About Investment 16Document2 pagesExamination About Investment 16BLACKPINKLisaRoseJisooJennieNo ratings yet

- 4.1 Debt and Equity FinancingDocument13 pages4.1 Debt and Equity FinancingAliza UrtalNo ratings yet

- The Key To Effective SWOT Analysis - Include AQCD Factors: ActionableDocument10 pagesThe Key To Effective SWOT Analysis - Include AQCD Factors: Actionablesaad bin sadaqatNo ratings yet

- MAS Integration Exercise 1 Cost BehaviorDocument4 pagesMAS Integration Exercise 1 Cost BehaviorNycole joi CondeNo ratings yet

- AIS Chap 8 NotesDocument7 pagesAIS Chap 8 NotesKrisshaNo ratings yet

- AE8 - Group1 - Chapter 2Document44 pagesAE8 - Group1 - Chapter 2adarose romaresNo ratings yet

- Contingent Assets and Contingent LiabilitiesDocument5 pagesContingent Assets and Contingent LiabilitiesRonan Ferrer100% (1)

- Factors Affecting Cost of CapitalDocument40 pagesFactors Affecting Cost of CapitalKartik AroraNo ratings yet

- An Update On The Philippine Banking Industry Group7Document9 pagesAn Update On The Philippine Banking Industry Group7Queen TwoNo ratings yet

- Managerial Economics and Business Strategy - Ch. 1 - The Fundamentals of Managerial Economics PDFDocument36 pagesManagerial Economics and Business Strategy - Ch. 1 - The Fundamentals of Managerial Economics PDFRayhanNo ratings yet

- Chapter 16 - Working Capital Management 1Document36 pagesChapter 16 - Working Capital Management 1Phán Tiêu TiềnNo ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementAnna WilliamsNo ratings yet

- EFM4, CH 17, Slides, 07-02-18Document34 pagesEFM4, CH 17, Slides, 07-02-18Nicholas Malvin SaputraNo ratings yet

- Working Capital ManagementDocument25 pagesWorking Capital ManagementJaveria LeghariNo ratings yet

- Sesi 12-Working Capital ManagementDocument33 pagesSesi 12-Working Capital Managementdias khairunnisaNo ratings yet

- EFM4, CH 20, Slides, 07-02-18Document30 pagesEFM4, CH 20, Slides, 07-02-18SyifaNo ratings yet

- FM Week 13Document35 pagesFM Week 13shaikhsafwan7788No ratings yet

- Parental Involvement Scale - Guide To QuestionnaireDocument2 pagesParental Involvement Scale - Guide To QuestionnaireAldrin ZolinaNo ratings yet

- Parents As Para-TeachersDocument3 pagesParents As Para-TeachersAldrin ZolinaNo ratings yet

- TranscribedDocument5 pagesTranscribedAldrin ZolinaNo ratings yet

- 2 Example Problems CH 7 8Document30 pages2 Example Problems CH 7 8Aldrin Zolina100% (1)

- Review in Regulatory Framework For Business Transactions Activity - Notes 2 Semester - Academic Year 2021-2022Document3 pagesReview in Regulatory Framework For Business Transactions Activity - Notes 2 Semester - Academic Year 2021-2022Aldrin ZolinaNo ratings yet

- Estate Tax Pre TestDocument7 pagesEstate Tax Pre TestAldrin ZolinaNo ratings yet

- Patnubay Personal EssayDocument2 pagesPatnubay Personal EssayAldrin ZolinaNo ratings yet

- TesdaDocument3 pagesTesdaAldrin ZolinaNo ratings yet

- GEC 104 Activity 6Document1 pageGEC 104 Activity 6Aldrin ZolinaNo ratings yet

- Public International LawDocument5 pagesPublic International LawAldrin ZolinaNo ratings yet

- The Lived Experience of Filipino Nurses' Work in COVID-19 Quarantine Facilities: A Descriptive Phenomenological StudyDocument11 pagesThe Lived Experience of Filipino Nurses' Work in COVID-19 Quarantine Facilities: A Descriptive Phenomenological StudyAldrin Zolina100% (1)

- Review 105 - Day 13 P1: Notes ReceivableDocument21 pagesReview 105 - Day 13 P1: Notes ReceivableAldrin ZolinaNo ratings yet

- Internal Audit Unlocking Value TelecomDocument20 pagesInternal Audit Unlocking Value TelecomAldrin ZolinaNo ratings yet

- The Correct Cash and Cash Equivalent Balance On December 31, 2018 IsDocument7 pagesThe Correct Cash and Cash Equivalent Balance On December 31, 2018 IsAldrin ZolinaNo ratings yet

- Disease and Health Priority Risks and Future TrendsDocument14 pagesDisease and Health Priority Risks and Future TrendsAldrin ZolinaNo ratings yet

- Connection Lost - Modern FamilyDocument3 pagesConnection Lost - Modern FamilydanNo ratings yet

- Rebecca Mead. A Fuller Picture of Artemisia GentileschiDocument8 pagesRebecca Mead. A Fuller Picture of Artemisia GentileschiLevindo PereiraNo ratings yet

- J. Robert OppenheimerDocument3 pagesJ. Robert OppenheimerKath DeguzmanNo ratings yet

- 4PS FinalDocument44 pages4PS Finalcorazon lopez100% (2)

- Cultural Education in The Philippines PDFDocument31 pagesCultural Education in The Philippines PDFAyllo CortezNo ratings yet

- Certification: To Whom It May ConcernDocument6 pagesCertification: To Whom It May ConcernRinkashime Laiz TejeroNo ratings yet

- Macr 009Document1 pageMacr 009Graal GasparNo ratings yet

- Chapter - 6: General Financial Rules 2017Document40 pagesChapter - 6: General Financial Rules 2017PatrickNo ratings yet

- ESIC by CA Pranav ChandakDocument15 pagesESIC by CA Pranav ChandakMehak Kaushikk100% (1)

- Queenie BalagDocument4 pagesQueenie Balagapi-276829441No ratings yet

- Conflict of Interests PolicyDocument4 pagesConflict of Interests PolicyHira DaudNo ratings yet

- CRIM ASIATICO Vs PEOPLEDocument2 pagesCRIM ASIATICO Vs PEOPLEBug RancherNo ratings yet

- Kick Off Meeting BPI 2020Document70 pagesKick Off Meeting BPI 2020Stella AngelicaNo ratings yet

- Mississippi Innocence Project and Innocence Project Client Eddie Lee Howard PDFDocument2 pagesMississippi Innocence Project and Innocence Project Client Eddie Lee Howard PDFWLBT NewsNo ratings yet

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document2 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Never SmileNo ratings yet

- Balochistan Labour Welfare: Quota of Applied Post Desire Test CityDocument3 pagesBalochistan Labour Welfare: Quota of Applied Post Desire Test CityFahad Khan TareenNo ratings yet

- Plea Bargaining Framework in Drugs CasesDocument6 pagesPlea Bargaining Framework in Drugs CasesMack Hale BunaganNo ratings yet

- 2009 Statistical Data of Davao RegionDocument11 pages2009 Statistical Data of Davao RegionLeo ConstantineNo ratings yet

- People vs. UmanitoDocument11 pagesPeople vs. UmanitoisaaabelrfNo ratings yet

- Landmark Group Leading Retail Conglomerate in The Middle East & IndiaDocument25 pagesLandmark Group Leading Retail Conglomerate in The Middle East & IndiadurgakingerNo ratings yet

- Iptvgreat Vs Falcon TVDocument6 pagesIptvgreat Vs Falcon TVAparajita LamiaNo ratings yet

- Eurodisney PDFDocument2 pagesEurodisney PDFLoliNo ratings yet

- Japan Secuireties 2018Document381 pagesJapan Secuireties 2018TôThànhPhongNo ratings yet

- Chapter 16 Advanced Accounting Solution ManualDocument94 pagesChapter 16 Advanced Accounting Solution ManualVanessa DozonNo ratings yet

- Mark Antony: Marcus Antonius (14 January 83 BC - 1 August 30 BC), Commonly Known inDocument26 pagesMark Antony: Marcus Antonius (14 January 83 BC - 1 August 30 BC), Commonly Known inapollodoro87No ratings yet

- Supreme CourtDocument5 pagesSupreme CourtDivyasri JeganNo ratings yet

Download as ppt, pdf, or txt

You might also like

- A Folklore Bestiary (High-Res) (OSE)Document160 pagesA Folklore Bestiary (High-Res) (OSE)Digs31100% (2)

- Audit of Cash Test BanksDocument270 pagesAudit of Cash Test BanksAldrin Zolina100% (2)

- Budget Proposal: Creation of Print Media, TV Station, and Radio StationDocument6 pagesBudget Proposal: Creation of Print Media, TV Station, and Radio StationAldrin Zolina100% (1)

- Quiz (6 Items X 5 Points) : Problem Solving For Management Science Name: Section: Date: ScoreDocument1 pageQuiz (6 Items X 5 Points) : Problem Solving For Management Science Name: Section: Date: Scorephillip quimenNo ratings yet

- Chapter 03 Gross EstateDocument16 pagesChapter 03 Gross EstateNikki Bucatcat0% (1)

- Audit of Inventories: Problem No. 1Document272 pagesAudit of Inventories: Problem No. 1Aldrin Zolina100% (13)

- Revised Corporation Code - SummaryDocument34 pagesRevised Corporation Code - SummaryAldrin ZolinaNo ratings yet

- Case StudyDocument8 pagesCase StudyCleofe Mae Piñero AseñasNo ratings yet

- Gifts From The Sales Representative 1Document1 pageGifts From The Sales Representative 1Mj Salusada100% (2)

- The Application of Budgets and Budgetary Control On The Performance of Small and Medium-Sized Enterprises (Smes)Document18 pagesThe Application of Budgets and Budgetary Control On The Performance of Small and Medium-Sized Enterprises (Smes)P.S.VP JahnaviNo ratings yet

- BF Case Study Sweet Beginnings Co 1Document3 pagesBF Case Study Sweet Beginnings Co 1Bryan Caadyang100% (1)

- Competitivenes AssignmentDocument3 pagesCompetitivenes AssignmentTristan Zambale100% (1)

- BDO Unibank 2020 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2020 Annual Report Financial SupplementsDanNo ratings yet

- Moldez INT03 QUIZDocument3 pagesMoldez INT03 QUIZVincent Larrie MoldezNo ratings yet

- AGA Company Manufactures and Sells A Product ForDocument6 pagesAGA Company Manufactures and Sells A Product ForSeemabians KazmiNo ratings yet

- Portal1.Passportindia - Gov.in AppOnlineProject Secure ViewDraftAction Arn 13-0007206836Document2 pagesPortal1.Passportindia - Gov.in AppOnlineProject Secure ViewDraftAction Arn 13-0007206836patelaxayNo ratings yet

- WG I Monitor Backspin Relay and Probe Manual Rev 7 0Document14 pagesWG I Monitor Backspin Relay and Probe Manual Rev 7 0elch310scridbNo ratings yet

- Chapter 9 Expanding Customer RelationshipsDocument27 pagesChapter 9 Expanding Customer RelationshipsSherren Marie NalaNo ratings yet

- Project Classification:: Advantages of Net Present Value (NPV)Document5 pagesProject Classification:: Advantages of Net Present Value (NPV)Orko AbirNo ratings yet

- Horizontal Analysis Interpretation PDFDocument2 pagesHorizontal Analysis Interpretation PDFAlison JcNo ratings yet

- Theories: Basic ConceptsDocument20 pagesTheories: Basic ConceptsJude VeanNo ratings yet

- Financial Management BSATDocument9 pagesFinancial Management BSATEma Dupilas GuianalanNo ratings yet

- Balanced ScorecardDocument14 pagesBalanced ScorecardLand DoranNo ratings yet

- AE 18 Financial Market Prelim ExamDocument3 pagesAE 18 Financial Market Prelim ExamWenjunNo ratings yet

- Chapter 1Document7 pagesChapter 1Lhea Tomas Bicera-AlcantaraNo ratings yet

- Managerial Finance by Gtman 5th EditionDocument17 pagesManagerial Finance by Gtman 5th EditionIrfan Yaqoob100% (1)

- Debt RestructuringDocument2 pagesDebt RestructuringDañella Jane Baisa0% (1)

- Financial Statements Analysis - ComprehensiveDocument60 pagesFinancial Statements Analysis - ComprehensiveGonzalo Jr. RualesNo ratings yet

- 09 - Chapter 9 Cost of CapitalDocument56 pages09 - Chapter 9 Cost of Capitalhunkie100% (1)

- Master in Business Administration Mba 308 - Financial ManagementDocument5 pagesMaster in Business Administration Mba 308 - Financial ManagementJhaydiel JacutanNo ratings yet

- Chapter 5 Financial Markets and InstitutionsDocument12 pagesChapter 5 Financial Markets and InstitutionsHamis Rabiam MagundaNo ratings yet

- FM - Cost of CapitalDocument26 pagesFM - Cost of CapitalMaxine SantosNo ratings yet

- Module 2 - Topic 4Document8 pagesModule 2 - Topic 4Moon LightNo ratings yet

- CH 13#6Document13 pagesCH 13#6jjmaducdoc100% (1)

- Krystal Guile Dagatan - Activity 2Document6 pagesKrystal Guile Dagatan - Activity 2Krystal Guile DagatanNo ratings yet

- WC - Merits and DemeritsDocument23 pagesWC - Merits and DemeritsARUN100% (1)

- Valuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitDocument41 pagesValuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitArundhati SinhaNo ratings yet

- Mid-Sem Answers and SolutionsDocument26 pagesMid-Sem Answers and SolutionsAmeer Zahar50% (2)

- Chapter 6 - Strategic ManagementDocument21 pagesChapter 6 - Strategic ManagementnadineNo ratings yet

- Draft 1Document5 pagesDraft 1Precious Dorothy magduraNo ratings yet

- MGT-4 Modules 1-5Document15 pagesMGT-4 Modules 1-5RHIAN B.No ratings yet

- Chapter 12Document34 pagesChapter 12Kad SaadNo ratings yet

- Leverages PROBLEMS AND SOLUTIONSDocument7 pagesLeverages PROBLEMS AND SOLUTIONSrashidNo ratings yet

- Asuprin Activity Worksheet: Compiled By: A. S. MALQUISTODocument5 pagesAsuprin Activity Worksheet: Compiled By: A. S. MALQUISTOLynNo ratings yet

- Reed's Clothier Case StudyDocument6 pagesReed's Clothier Case StudyColleen Sieger Mueller0% (2)

- Group 1Document16 pagesGroup 1Mariann Jane GanNo ratings yet

- Role of Financial Management in OrganizationDocument8 pagesRole of Financial Management in OrganizationTasbeha SalehjeeNo ratings yet

- Finman Module 8Document42 pagesFinman Module 8Jennyveive RiveraNo ratings yet

- Direct Method or Cost of Goods Sold MethodDocument2 pagesDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNo ratings yet

- FinMan Module 2 Financial Markets & InstitutionsDocument13 pagesFinMan Module 2 Financial Markets & Institutionserickson hernanNo ratings yet

- Chapter 9 Financial Forecasting For Strategic GrowthDocument18 pagesChapter 9 Financial Forecasting For Strategic GrowthMa. Jhoan DailyNo ratings yet

- Managerial Economics Assignment 3 PDFDocument2 pagesManagerial Economics Assignment 3 PDFSakinaNo ratings yet

- Examination About Investment 16Document2 pagesExamination About Investment 16BLACKPINKLisaRoseJisooJennieNo ratings yet

- 4.1 Debt and Equity FinancingDocument13 pages4.1 Debt and Equity FinancingAliza UrtalNo ratings yet

- The Key To Effective SWOT Analysis - Include AQCD Factors: ActionableDocument10 pagesThe Key To Effective SWOT Analysis - Include AQCD Factors: Actionablesaad bin sadaqatNo ratings yet

- MAS Integration Exercise 1 Cost BehaviorDocument4 pagesMAS Integration Exercise 1 Cost BehaviorNycole joi CondeNo ratings yet

- AIS Chap 8 NotesDocument7 pagesAIS Chap 8 NotesKrisshaNo ratings yet

- AE8 - Group1 - Chapter 2Document44 pagesAE8 - Group1 - Chapter 2adarose romaresNo ratings yet

- Contingent Assets and Contingent LiabilitiesDocument5 pagesContingent Assets and Contingent LiabilitiesRonan Ferrer100% (1)

- Factors Affecting Cost of CapitalDocument40 pagesFactors Affecting Cost of CapitalKartik AroraNo ratings yet

- An Update On The Philippine Banking Industry Group7Document9 pagesAn Update On The Philippine Banking Industry Group7Queen TwoNo ratings yet

- Managerial Economics and Business Strategy - Ch. 1 - The Fundamentals of Managerial Economics PDFDocument36 pagesManagerial Economics and Business Strategy - Ch. 1 - The Fundamentals of Managerial Economics PDFRayhanNo ratings yet

- Chapter 16 - Working Capital Management 1Document36 pagesChapter 16 - Working Capital Management 1Phán Tiêu TiềnNo ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementAnna WilliamsNo ratings yet

- EFM4, CH 17, Slides, 07-02-18Document34 pagesEFM4, CH 17, Slides, 07-02-18Nicholas Malvin SaputraNo ratings yet

- Working Capital ManagementDocument25 pagesWorking Capital ManagementJaveria LeghariNo ratings yet

- Sesi 12-Working Capital ManagementDocument33 pagesSesi 12-Working Capital Managementdias khairunnisaNo ratings yet

- EFM4, CH 20, Slides, 07-02-18Document30 pagesEFM4, CH 20, Slides, 07-02-18SyifaNo ratings yet

- FM Week 13Document35 pagesFM Week 13shaikhsafwan7788No ratings yet

- Parental Involvement Scale - Guide To QuestionnaireDocument2 pagesParental Involvement Scale - Guide To QuestionnaireAldrin ZolinaNo ratings yet

- Parents As Para-TeachersDocument3 pagesParents As Para-TeachersAldrin ZolinaNo ratings yet

- TranscribedDocument5 pagesTranscribedAldrin ZolinaNo ratings yet

- 2 Example Problems CH 7 8Document30 pages2 Example Problems CH 7 8Aldrin Zolina100% (1)

- Review in Regulatory Framework For Business Transactions Activity - Notes 2 Semester - Academic Year 2021-2022Document3 pagesReview in Regulatory Framework For Business Transactions Activity - Notes 2 Semester - Academic Year 2021-2022Aldrin ZolinaNo ratings yet

- Estate Tax Pre TestDocument7 pagesEstate Tax Pre TestAldrin ZolinaNo ratings yet

- Patnubay Personal EssayDocument2 pagesPatnubay Personal EssayAldrin ZolinaNo ratings yet

- TesdaDocument3 pagesTesdaAldrin ZolinaNo ratings yet

- GEC 104 Activity 6Document1 pageGEC 104 Activity 6Aldrin ZolinaNo ratings yet

- Public International LawDocument5 pagesPublic International LawAldrin ZolinaNo ratings yet

- The Lived Experience of Filipino Nurses' Work in COVID-19 Quarantine Facilities: A Descriptive Phenomenological StudyDocument11 pagesThe Lived Experience of Filipino Nurses' Work in COVID-19 Quarantine Facilities: A Descriptive Phenomenological StudyAldrin Zolina100% (1)

- Review 105 - Day 13 P1: Notes ReceivableDocument21 pagesReview 105 - Day 13 P1: Notes ReceivableAldrin ZolinaNo ratings yet

- Internal Audit Unlocking Value TelecomDocument20 pagesInternal Audit Unlocking Value TelecomAldrin ZolinaNo ratings yet

- The Correct Cash and Cash Equivalent Balance On December 31, 2018 IsDocument7 pagesThe Correct Cash and Cash Equivalent Balance On December 31, 2018 IsAldrin ZolinaNo ratings yet

- Disease and Health Priority Risks and Future TrendsDocument14 pagesDisease and Health Priority Risks and Future TrendsAldrin ZolinaNo ratings yet

- Connection Lost - Modern FamilyDocument3 pagesConnection Lost - Modern FamilydanNo ratings yet

- Rebecca Mead. A Fuller Picture of Artemisia GentileschiDocument8 pagesRebecca Mead. A Fuller Picture of Artemisia GentileschiLevindo PereiraNo ratings yet

- J. Robert OppenheimerDocument3 pagesJ. Robert OppenheimerKath DeguzmanNo ratings yet

- 4PS FinalDocument44 pages4PS Finalcorazon lopez100% (2)

- Cultural Education in The Philippines PDFDocument31 pagesCultural Education in The Philippines PDFAyllo CortezNo ratings yet

- Certification: To Whom It May ConcernDocument6 pagesCertification: To Whom It May ConcernRinkashime Laiz TejeroNo ratings yet

- Macr 009Document1 pageMacr 009Graal GasparNo ratings yet

- Chapter - 6: General Financial Rules 2017Document40 pagesChapter - 6: General Financial Rules 2017PatrickNo ratings yet

- ESIC by CA Pranav ChandakDocument15 pagesESIC by CA Pranav ChandakMehak Kaushikk100% (1)

- Queenie BalagDocument4 pagesQueenie Balagapi-276829441No ratings yet

- Conflict of Interests PolicyDocument4 pagesConflict of Interests PolicyHira DaudNo ratings yet

- CRIM ASIATICO Vs PEOPLEDocument2 pagesCRIM ASIATICO Vs PEOPLEBug RancherNo ratings yet

- Kick Off Meeting BPI 2020Document70 pagesKick Off Meeting BPI 2020Stella AngelicaNo ratings yet

- Mississippi Innocence Project and Innocence Project Client Eddie Lee Howard PDFDocument2 pagesMississippi Innocence Project and Innocence Project Client Eddie Lee Howard PDFWLBT NewsNo ratings yet

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document2 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Never SmileNo ratings yet

- Balochistan Labour Welfare: Quota of Applied Post Desire Test CityDocument3 pagesBalochistan Labour Welfare: Quota of Applied Post Desire Test CityFahad Khan TareenNo ratings yet

- Plea Bargaining Framework in Drugs CasesDocument6 pagesPlea Bargaining Framework in Drugs CasesMack Hale BunaganNo ratings yet

- 2009 Statistical Data of Davao RegionDocument11 pages2009 Statistical Data of Davao RegionLeo ConstantineNo ratings yet

- People vs. UmanitoDocument11 pagesPeople vs. UmanitoisaaabelrfNo ratings yet

- Landmark Group Leading Retail Conglomerate in The Middle East & IndiaDocument25 pagesLandmark Group Leading Retail Conglomerate in The Middle East & IndiadurgakingerNo ratings yet

- Iptvgreat Vs Falcon TVDocument6 pagesIptvgreat Vs Falcon TVAparajita LamiaNo ratings yet

- Eurodisney PDFDocument2 pagesEurodisney PDFLoliNo ratings yet

- Japan Secuireties 2018Document381 pagesJapan Secuireties 2018TôThànhPhongNo ratings yet

- Chapter 16 Advanced Accounting Solution ManualDocument94 pagesChapter 16 Advanced Accounting Solution ManualVanessa DozonNo ratings yet

- Mark Antony: Marcus Antonius (14 January 83 BC - 1 August 30 BC), Commonly Known inDocument26 pagesMark Antony: Marcus Antonius (14 January 83 BC - 1 August 30 BC), Commonly Known inapollodoro87No ratings yet

- Supreme CourtDocument5 pagesSupreme CourtDivyasri JeganNo ratings yet