Download as ppt, pdf, or txt

You might also like

- PWC SOX Section 404 Practical Guidance For Management PDFDocument154 pagesPWC SOX Section 404 Practical Guidance For Management PDFGouyez Benallal Mouad100% (1)

- The Business Value of Design-FrogDocument20 pagesThe Business Value of Design-Frogxiaonan lu100% (1)

- Energy Policy: SciencedirectDocument11 pagesEnergy Policy: Sciencedirectdiyah100% (1)

- Cru Rental StudentDocument19 pagesCru Rental StudentRowann AwsmmNo ratings yet

- Presentation On Mergers and Acquisition of ONGC and Imperial EnergyDocument9 pagesPresentation On Mergers and Acquisition of ONGC and Imperial EnergyKarthik GhorpadeNo ratings yet

- Ongc FinalDocument35 pagesOngc FinalSurmeet SinghNo ratings yet

- Oil India Ongc ComparisionDocument35 pagesOil India Ongc ComparisionAlakshendra Pratap TheophilusNo ratings yet

- Mergers & Acquisitions in Oil & Energy SectorsDocument12 pagesMergers & Acquisitions in Oil & Energy SectorsadityatildaNo ratings yet

- Thermal Power ProjectDocument40 pagesThermal Power ProjectHinal GangarNo ratings yet

- Ongc Growth StrategyDocument10 pagesOngc Growth StrategydhavalmevadaNo ratings yet

- Brief Report On NTPCDocument7 pagesBrief Report On NTPCChandra ShekharNo ratings yet

- ONGC - Stock Update 240921Document14 pagesONGC - Stock Update 240921Mohit MauryaNo ratings yet

- South - Kore EIADocument16 pagesSouth - Kore EIAZ pristinNo ratings yet

- Iocl Project ReportDocument63 pagesIocl Project ReportVaishnavi ShawNo ratings yet

- FM Presentation On Capital Structure Analysis of FirmsDocument22 pagesFM Presentation On Capital Structure Analysis of FirmsRaiza SideequeNo ratings yet

- Q-1 Executive Summary of The Company and The Industry?: Reliance Industries Limited IsDocument13 pagesQ-1 Executive Summary of The Company and The Industry?: Reliance Industries Limited Israjat_singlaNo ratings yet

- ONGC TejasPatilDocument10 pagesONGC TejasPatilTejas PatilNo ratings yet

- Turcas Petrol Investor Presentation November 2012: Bloomberg: TRCAS TI Reuters: TRCAS - ISDocument35 pagesTurcas Petrol Investor Presentation November 2012: Bloomberg: TRCAS TI Reuters: TRCAS - ISqu1627No ratings yet

- History of ONGC: After 1990Document16 pagesHistory of ONGC: After 1990samzzzzzNo ratings yet

- ReportDocument26 pagesReportapchawareNo ratings yet

- Chennai Petroleum Corporation LimitedDocument4 pagesChennai Petroleum Corporation Limitedhell_quit1No ratings yet

- ADRO Financial Analysis - FBPDocument32 pagesADRO Financial Analysis - FBPFranklyn BerrisNo ratings yet

- ONGC DocumentDocument4 pagesONGC DocumentKnt Nallasamy GounderNo ratings yet

- Chapter-1 Company ProfileDocument43 pagesChapter-1 Company Profilekapil devNo ratings yet

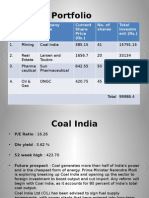

- Portfolio: SR.N o Sector Company Name Current Share Price (RS.) No. of Shares Total Investm Ent (RS.)Document3 pagesPortfolio: SR.N o Sector Company Name Current Share Price (RS.) No. of Shares Total Investm Ent (RS.)NinadTambeNo ratings yet

- OIL India, 1st February 2013Document10 pagesOIL India, 1st February 2013Angel BrokingNo ratings yet

- Electrosteel Solvency Report - IPAICDocument8 pagesElectrosteel Solvency Report - IPAICAbhinav SinglaNo ratings yet

- N Case Study Analysis NDocument11 pagesN Case Study Analysis NPiyush Mehta CfaNo ratings yet

- RIL Macquarie 10 July 06Document50 pagesRIL Macquarie 10 July 06alokkuma05No ratings yet

- Company DetailsDocument30 pagesCompany DetailssudehelyRNo ratings yet

- Andhra Petrochemicals LTD: Investment SummaryDocument4 pagesAndhra Petrochemicals LTD: Investment Summaryjobs rkNo ratings yet

- Case 2 Group 2Document9 pagesCase 2 Group 2Astha AryaNo ratings yet

- Financial Analysis and Valuation TRACK A COMPANY - Gas Authority of India LTDDocument15 pagesFinancial Analysis and Valuation TRACK A COMPANY - Gas Authority of India LTDHuzaifa ShamsiNo ratings yet

- Presentation On Summer Internship/ Training in Ongc LTDDocument34 pagesPresentation On Summer Internship/ Training in Ongc LTDlokesh_bhatiyaNo ratings yet

- Presentation On Summer Internship/ Training in Ongc LTDDocument34 pagesPresentation On Summer Internship/ Training in Ongc LTDsanoojnairNo ratings yet

- Hindustan Petroleum Corporation LimitedDocument11 pagesHindustan Petroleum Corporation Limitedshabila_momin4976No ratings yet

- Analyst Meet 2013Document44 pagesAnalyst Meet 2013anon_481361080No ratings yet

- Annual Reports ONGC Annual Report 10-11Document256 pagesAnnual Reports ONGC Annual Report 10-11Amit VirmaniNo ratings yet

- Balance Sheet AnalysisDocument4 pagesBalance Sheet AnalysisArchit GuptaNo ratings yet

- Performance Appraisal of OngcDocument83 pagesPerformance Appraisal of Ongcvipul tandonNo ratings yet

- Merged Group 9Document34 pagesMerged Group 9gaurav malhotraNo ratings yet

- E-Procurement Process at Ongc: A Report OnDocument64 pagesE-Procurement Process at Ongc: A Report OnDevesh GaurNo ratings yet

- NFL Annual Report 2011-2012Document108 pagesNFL Annual Report 2011-2012prabhjotbhangalNo ratings yet

- IOC Research InsightDocument4 pagesIOC Research InsightHARSH GARODIANo ratings yet

- Analysis Oil and Gas SectorDocument37 pagesAnalysis Oil and Gas SectorLakshay KalraNo ratings yet

- Eq Ad Ani Power BaseDocument4 pagesEq Ad Ani Power BaseNaresh BitlaNo ratings yet

- Assignment OF Banking and Working Capital ON Financial Accounts and Working Capital OF GailDocument9 pagesAssignment OF Banking and Working Capital ON Financial Accounts and Working Capital OF GailSachin Kumar BassiNo ratings yet

- Prepared By: - Jyoti, Manish & YogeshDocument26 pagesPrepared By: - Jyoti, Manish & YogeshJustto Make UsmileNo ratings yet

- Module 1 Energy Scenario - AuditDocument136 pagesModule 1 Energy Scenario - AuditNeha B50% (2)

- Sector 2: Oil & Gas Company 1: BPCL General OverviewDocument5 pagesSector 2: Oil & Gas Company 1: BPCL General Overviewxilox67632No ratings yet

- Sustainability: GRI G3.0 Compliant A Level ReportDocument88 pagesSustainability: GRI G3.0 Compliant A Level ReportanuNo ratings yet

- Business Diversification Strategies of Energy Companies in India A Study of OilDocument27 pagesBusiness Diversification Strategies of Energy Companies in India A Study of Oiladiti pathakNo ratings yet

- ONGCDocument17 pagesONGCChetan GajeraNo ratings yet

- Essar Ar2012Document153 pagesEssar Ar2012Hiren TarapraNo ratings yet

- ONGC Corporate Presentation: J.P Morgan Global Oil & Gas Conference, London 5-6 November 2018Document32 pagesONGC Corporate Presentation: J.P Morgan Global Oil & Gas Conference, London 5-6 November 2018Arun Preet Singh JohalNo ratings yet

- Neyveli Lignite LTD Stake ValuationDocument13 pagesNeyveli Lignite LTD Stake ValuationAjay BagariaNo ratings yet

- Oil & Natural Gas IndustryDocument20 pagesOil & Natural Gas IndustryaabidsNo ratings yet

- JSW Energy IMPDocument20 pagesJSW Energy IMPvraj.patelsmpic090No ratings yet

- ONGCDocument3 pagesONGCSathish Kumar RNo ratings yet

- B K BakhshiDocument21 pagesB K Bakhshirahulmehta631No ratings yet

- 1.1 Energy OverviewDocument53 pages1.1 Energy OverviewDurg Singh AjarNo ratings yet

- A Comparative Study On The Stock Price of Companies in Power SectorDocument20 pagesA Comparative Study On The Stock Price of Companies in Power Sectormpx123No ratings yet

- Oil companies and the energy transitionFrom EverandOil companies and the energy transitionNo ratings yet

- Deeksha V B (2sd18mba08)Document84 pagesDeeksha V B (2sd18mba08)Karthik GhorpadeNo ratings yet

- Presentation On Mergers and Acquisition of ONGC and Imperial EnergyDocument9 pagesPresentation On Mergers and Acquisition of ONGC and Imperial EnergyKarthik GhorpadeNo ratings yet

- KarthikDocument3 pagesKarthikKarthik GhorpadeNo ratings yet

- Servqual Attributes of Tourism IndustryDocument10 pagesServqual Attributes of Tourism IndustryKarthik GhorpadeNo ratings yet

- MODULE 7 Advocacy Against CorruptionDocument8 pagesMODULE 7 Advocacy Against Corruptionnewlymade641No ratings yet

- CBR - Zomato - MarketingDocument28 pagesCBR - Zomato - MarketingNishant SoniNo ratings yet

- 2GO Group IncDocument9 pages2GO Group IncPocari OnceNo ratings yet

- MCCH Construction Services: Project: MC-18-022 (Masville, Paranaque) Period CoveredDocument1 pageMCCH Construction Services: Project: MC-18-022 (Masville, Paranaque) Period CoveredChester VitugNo ratings yet

- AFCAP Transaid Final Report - Transport Operator Associations and Rural Access v5Document190 pagesAFCAP Transaid Final Report - Transport Operator Associations and Rural Access v5Yayew MaruNo ratings yet

- Intercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupDocument60 pagesIntercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupPhil MO JoeNo ratings yet

- Paystubs 03.22.2024 2Document3 pagesPaystubs 03.22.2024 2RangeRoverNo ratings yet

- Far Eastern University: Organization ChartDocument1 pageFar Eastern University: Organization ChartFRANCIS AUGUSTUS RAGATNo ratings yet

- Bank AlfalahDocument40 pagesBank Alfalahmir nida95% (21)

- Ohnmar Lwin (EMBA - 28)Document90 pagesOhnmar Lwin (EMBA - 28)MinnNo ratings yet

- Assignment On Postal Life InsuranceDocument5 pagesAssignment On Postal Life Insurancesabbir HossainNo ratings yet

- Fact Finders Report Greater Egg Harbor PDFDocument109 pagesFact Finders Report Greater Egg Harbor PDFGallowayTwpNewsNo ratings yet

- AMULDocument11 pagesAMULkeshav956No ratings yet

- Marketing: Managing Profitable Customer RelationshipsDocument19 pagesMarketing: Managing Profitable Customer Relationshipsazwan ayop100% (3)

- Goldman Sachs Alumni: Currently Serving Name Current Title in Obama Administration Former Goldman Sachs TitleDocument4 pagesGoldman Sachs Alumni: Currently Serving Name Current Title in Obama Administration Former Goldman Sachs TitleuighuigNo ratings yet

- Planning and RoutingDocument50 pagesPlanning and RoutingAnand DubeyNo ratings yet

- Your Current Account Terms 1Document28 pagesYour Current Account Terms 1sinisa simicNo ratings yet

- UK Banking StructureDocument35 pagesUK Banking StructureSabiha Farzana MoonmoonNo ratings yet

- Farlin Final Case Analysis 2 Mis 112Document4 pagesFarlin Final Case Analysis 2 Mis 112api-700323027No ratings yet

- Telecom Cost StructureDocument16 pagesTelecom Cost Structurepuneet1955No ratings yet

- Chapter 8Document44 pagesChapter 8Victoria Damsleth-AalrudNo ratings yet

- Company Name Last Historical Date Currency: State Bank of India (SBIN) 31-Mar-19 in Crore INRDocument40 pagesCompany Name Last Historical Date Currency: State Bank of India (SBIN) 31-Mar-19 in Crore INRshivam vermaNo ratings yet

- Startup Policy 2022 27 KanEng 4Document27 pagesStartup Policy 2022 27 KanEng 4Sayed GajendergadNo ratings yet

- 5,000 UnitsDocument3 pages5,000 UnitsJohn Rosales BelarmaNo ratings yet

- 15 - Deepak Gupta 1Document4 pages15 - Deepak Gupta 1Virendra ChaudhariNo ratings yet

- Cox and Kings ReportDocument116 pagesCox and Kings ReportRitesh pandey100% (1)

- Feenstra Taylor Econ CH04Document66 pagesFeenstra Taylor Econ CH04mar1a_leeNo ratings yet